- Beverages

- Caffeinated Sparkling Water Market

Caffeinated Sparkling Water Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Caffeinated Sparkling Water Market is segmented by Product Type (Unflavored Caffeinated Sparkling Water, Flavored Caffeinated Sparkling Water), Packaging Type (Plastic Bottles, Cans, Glass Bottles), Sales Channel (Supermarkets & Hypermarkets, Convenience Stores, Specialty Store, Online Retail, Others), and Regional Analysis, 2026 - 2033

Caffeinated Sparkling Water Market Share and Trends Analysis

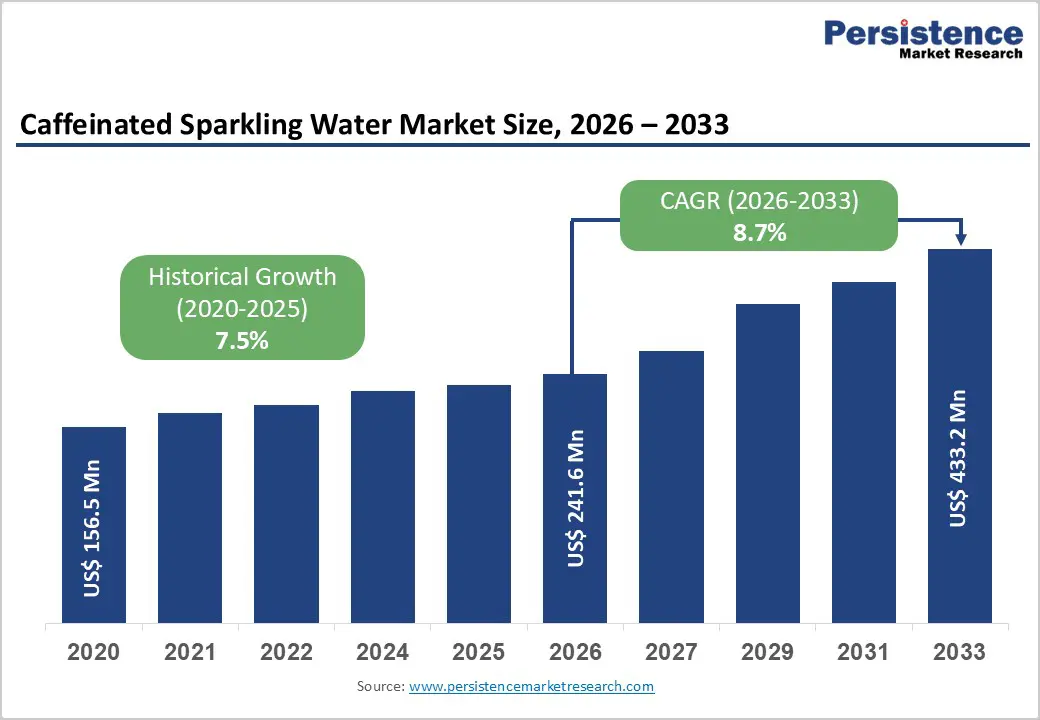

The global caffeinated sparkling water market size is expected to be valued at US$ 241.6 million in 2026 and projected to reach US$ 433.2 million by 2033, growing at a CAGR of 8.7% between 2026 and 2033.

This growth is primarily driven by rising health consciousness among global consumers and increasing demand for clean-label functional beverages. The transition from sugary carbonated soft drinks to unsweetened, caffeinated alternatives represents a fundamental shift in the beverage landscape, particularly among millennial and Gen Z demographics seeking sustained energy without the subsequent sugar crash.

Key Industry Highlights:

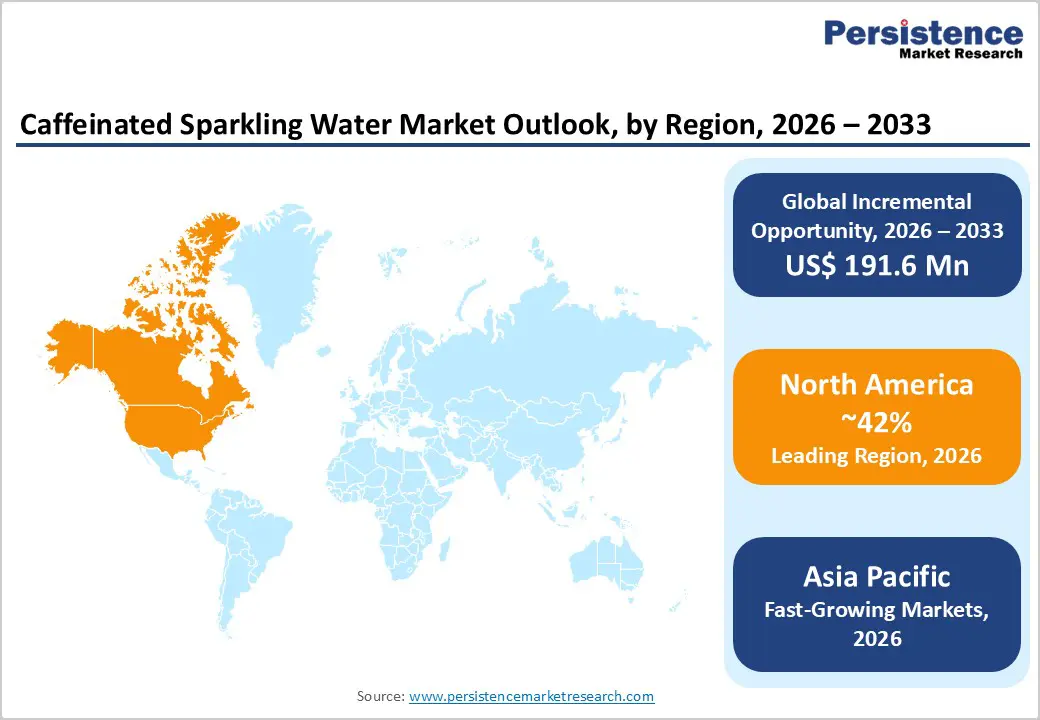

- Leading Region: North America dominated the landscape with a 42% market share in 2025, driven by high health awareness, a mature retail sector, and the strong presence of major beverage corporations.

- Fastest Growing Region: Asia Pacific is set to experience the highest growth rate due to rapid urbanization, increasing disposable incomes, and a booming e-commerce sector in China, India, and Japan.

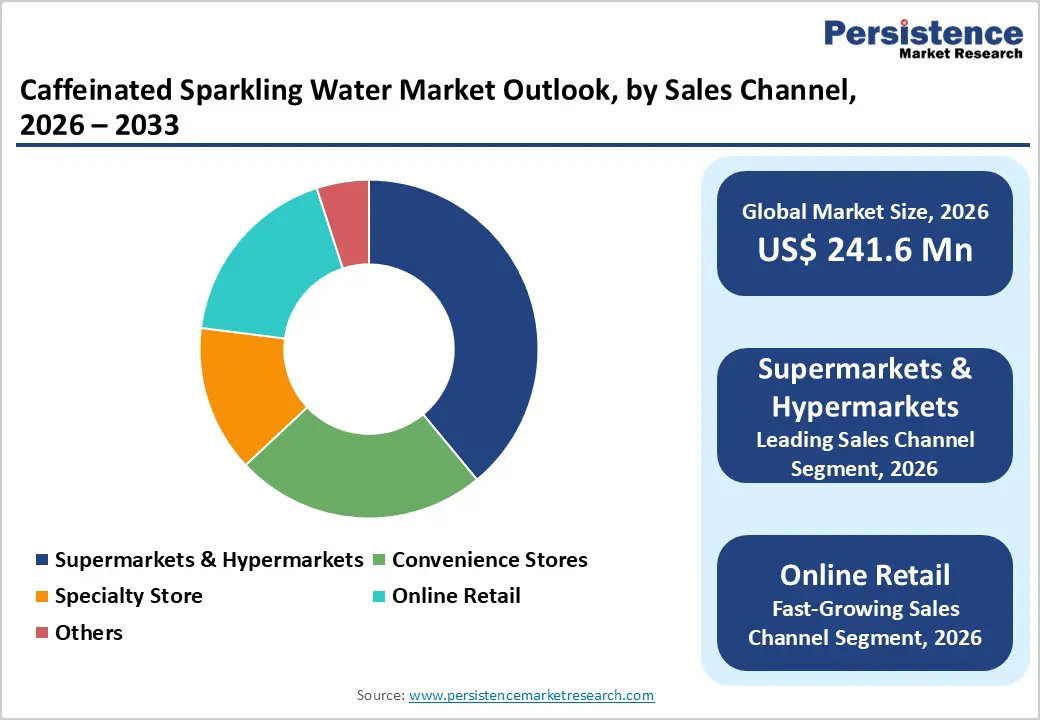

- Dominant Sales Channel: Supermarkets & Hypermarkets remain the leading sales channel, accounting for 39% of the market in 2025, providing high product visibility and bulk purchasing options for families.

- Fastest Growing Segment: Online Retail is the quickest-expanding distribution channel, fueled by the convenience of subscription models and the growing consumer preference for home delivery of beverage cases.

- Key Opportunity: The integration of adaptogens and nootropics into caffeinated water offers a significant growth avenue, catering to the rising demand for holistic wellness and "clean" cognitive enhancement.

| Key Insights | Details |

|---|---|

| Caffeinated Sparkling Water Market Size (2026E) | US$ 241.6 Mn |

| Market Value Forecast (2033F) | US$ 433.2 Mn |

| Projected Growth (CAGR 2026 to 2033) | 8.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.5% |

Market Dynamics

Driver - Increased Demand for Convenience and Functional Hydration

Fast-paced urban lifestyles are accelerating demand for beverages that combine portability with measurable functional benefits. Caffeinated sparkling water directly addresses this need by offering hydration and light energy stimulation in a single, ready-to-drink format. As consumers juggle work, fitness, and social commitments, there is a growing preference for products that fit seamlessly into daily routines without requiring preparation or refrigeration planning. The slim can format and single-serve packaging further enhance impulse purchases and on-the-go consumption.

Beyond convenience, the concept of functional hydration is reshaping category positioning. Shoppers increasingly expect beverages to deliver more than refreshment, seeking added value such as natural caffeine, electrolytes, or botanical extracts. Caffeinated sparkling water satisfies this expectation while maintaining zero-sugar and low-calorie credentials. This dual positioning as both a hydration enhancer and a mild energy source is expanding consumption occasions, driving penetration across convenience stores, supermarkets, and digital retail channels worldwide.

Restraints - Regulatory uncertainty around caffeine content

Evolving scrutiny over stimulant levels in mainstream beverages is creating compliance complexities for manufacturers in the global caffeinated sparkling water market. Regulatory authorities across North America, Europe, and parts of Asia maintain varying thresholds for permissible caffeine content, labeling disclosures, and marketing claims, particularly for products positioned as energy enhancers. Inconsistent global standards increase reformulation costs and complicate cross-border expansion strategies. Authorities are also paying closer attention to youth consumption patterns and cumulative caffeine intake from multiple sources, which may lead to stricter warning labels or advertising restrictions. For emerging brands, navigating these fragmented regulatory frameworks can delay product launches and raise legal risk exposure. This uncertainty constrains innovation flexibility and heightens operational costs, ultimately moderating the market’s growth trajectory despite strong consumer demand.

Opportunity - Premiumization of caffeinated sparkling water through botanical, adaptogen, and nootropic functional ingredients

Value creation in the global caffeinated sparkling water market is increasingly shifting from basic caffeine fortification to advanced functional positioning. Brands are elevating product portfolios by incorporating botanical extracts, adaptogens such as ashwagandha and ginseng, and nootropic ingredients including L-theanine and lion’s mane mushroom. This strategic layering of benefits transforms the category from a simple zero-calorie energy alternative into a multifunctional wellness beverage. Consumers are demonstrating a willingness to pay a premium for formulations that promise focus, stress balance, and cognitive clarity alongside hydration.

This premiumization trend opens higher-margin opportunities and supports brand differentiation in a crowded shelf environment. Functional ingredient storytelling, clean-label transparency, and clinically referenced benefits enhance perceived value and encourage trial among health-conscious urban consumers. As wellness culture matures globally, beverages positioned at the intersection of energy, mental performance, and holistic health are likely to command stronger loyalty and sustained growth momentum.

Category-wise Analysis

Product Type Insights

The flavored, caffeinated sparkling water segment is the dominant force in the market, capturing a significant share of revenue. Consumers increasingly prefer flavored variants over Unflavored Caffeinated Sparkling Water due to the sensory appeal and the ability of fruit extracts to mask the naturally bitter profile of caffeine. Popular flavors such as lime, grapefruit, and berry have become staples for brands like Talking Rain and Cascade Ice Sparkling Water. The segment's dominance is supported by the fact that many consumers use these beverages as healthy mixers or as a direct replacement for flavored sodas. As companies continue to innovate with complex, multi-layered flavor profiles, this segment is expected to maintain its leading position throughout the forecast period ending in 2033.

Sales Channel Insights

The supermarkets & hypermarkets segment accounted for a dominant 39% market share in 2025. These large-scale retail outlets provide extensive shelf space, allowing consumers to compare various brands such as Celsius Holdings, Inc., HiBall, and Tru. The ability to purchase in bulk and the frequent "buy-one-get-one" promotions make hypermarkets the primary destination for household beverage shopping. Conversely, Online Retail is identified as the fastest-growing segment through 2033. The shift is driven by the rise of e-grocery platforms and the convenience of home delivery. As consumers become more comfortable purchasing heavy beverage cases online, the digital channel is expected to see a surge in specialized "discovery" sets and subscription services for premium caffeinated water brands.

Regional Insights

North America Caffeinated Sparkling Water Market Trends and Insights

North America remains the largest market for caffeinated sparkling water, holding a dominant 42% market share in 2025. In the U.S., strong demand is driven by consumers shifting away from sugary carbonated drinks toward zero-calorie, functional hydration options. Canada mirrors this pattern, supported by rising health awareness and expanding shelf space for better-for-you beverages across major retail chains. Urban penetration and high disposable income levels further reinforce premium beverage adoption across both markets.

Millennials are a central growth engine, prioritizing clean energy, natural caffeine sources, and ingredient transparency. Functional additions such as green tea extract, ginseng, L-theanine, and adaptogens are increasingly influencing purchasing decisions. Brands operating in North America are leveraging limited-edition flavors, sleek can formats, and digital marketing strategies to maintain engagement. The region’s mature retail infrastructure and strong innovation pipeline continue to position it at the forefront of the evolution of caffeinated sparkling water.

Asia Pacific Caffeinated Sparkling Water Market Trends and Insights

Asia Pacific is projected to be the fastest-growing segment for caffeinated sparkling water through 2033. This rapid expansion is fueled by the massive population bases and rising disposable incomes in China, India, and Japan. Urbanization in these economies has led to a surge in demand for ready-to-drink functional beverages among the working-class population. In China, the "Genki Forest" phenomenon has sparked a broader interest in zero-sugar sparkling drinks, creating an entry point for caffeinated variants that promise "clean energy."

Manufacturing advantages in the region also play a role, as local production helps keep retail prices competitive. In India and ASEAN countries, the growth of the Online Retail sector and the expansion of modern trade (supermarkets) are making these premium products more accessible to the middle class. The region’s growth dynamics are further supported by a growing "coffee culture" that is gradually diversifying into alternative caffeine formats. As international brands like The Coca-Cola Company increase their regional footprint, the Asia Pacific market is expected to become a major contributor to global revenue.

Competitive Landscape

The competitive landscape of the caffeinated sparkling water market is characterized by moderate consolidation, with a few global beverage giants holding significant influence, while a vibrant group of niche players and startups drives innovation. Companies like PepsiCo, The Coca-Cola Company, and Keurig Dr Pepper leverage their massive distribution networks and marketing budgets to dominate shelf space in Supermarkets & Hypermarkets. Their strategy often involves acquiring successful smaller brands or launching "flanker" products under existing popular labels. Key differentiators employed by leaders include brand loyalty, flavor variety, and the ability to scale production to lower unit costs. Emerging business models are increasingly focusing on D2C platforms and sustainability-centric branding to appeal to eco-conscious and tech-savvy younger consumers.

Key Developments:

- In February 2026, bubly™ Sparkling Water, a PepsiCo brand, launched limited-edition galactic-inspired flavors in collaboration with Illumination and Nintendo to celebrate The Super Mario Galaxy Movie. The partnership reflects the growing use of entertainment tie-ins to drive brand engagement and limited-time purchase momentum in the sparkling beverage segment.

- In September 2025, Talking Rain Beverage Company introduced Sparkling Ice Caffeine Cherry Cola in a convenient canned format, reinforcing the trend toward hybridization between sparkling water and functional caffeinated beverages.

- In February 2025, Tru secured $4.6 million in funding while strengthening its alignment with Polar Beverage, signaling strategic collaboration to expand distribution and scale within the better-for-you sparkling drinks category.

Companies Covered in Caffeinated Sparkling Water Market

- PepsiCo

- The Coca-Cola Company

- Nestlé S.A.

- Keurig Dr Pepper

- Celsius Holdings, Inc.

- Cascade Ice Sparkling Water

- HiBall

- Volay Brands, LLC

- Tru

- Talking Rain

- Others

Frequently Asked Questions

The global caffeinated sparkling water market is projected to be valued at US$ 241.6 Mn in 2026.

Increased Demand for Convenience and Functional Hydration is driving demand for Caffeinated Sparkling Water market.

The Global Caffeinated Sparkling Water market is poised to witness a CAGR of 8.7% between 2026 and 2033.

Premiumization of caffeinated sparkling water through botanical, adaptogen, and nootropic functional ingredient is key opportunity in the Caffeinated Sparkling Water market.

Key industry leaders include PepsiCo, The Coca-Cola Company, Nestlé S.A., Keurig Dr Pepper, Celsius Holdings, Inc., Tru, Talking Rain, and Others.