- Biotechnology

- Norovirus Diagnostics Market

Norovirus Diagnostics Market Size, Share, and Growth Forecast 2026 - 2033

Norovirus Diagnostics Market by Product Type (Rapid Test Kits, PCR Kits, ELISA based kits), by End-User (Hospitals, Diagnostics Labs, Clinics), by Regional Analysis, 2026-2033

Norovirus Diagnostics Market Size and Trend Analysis

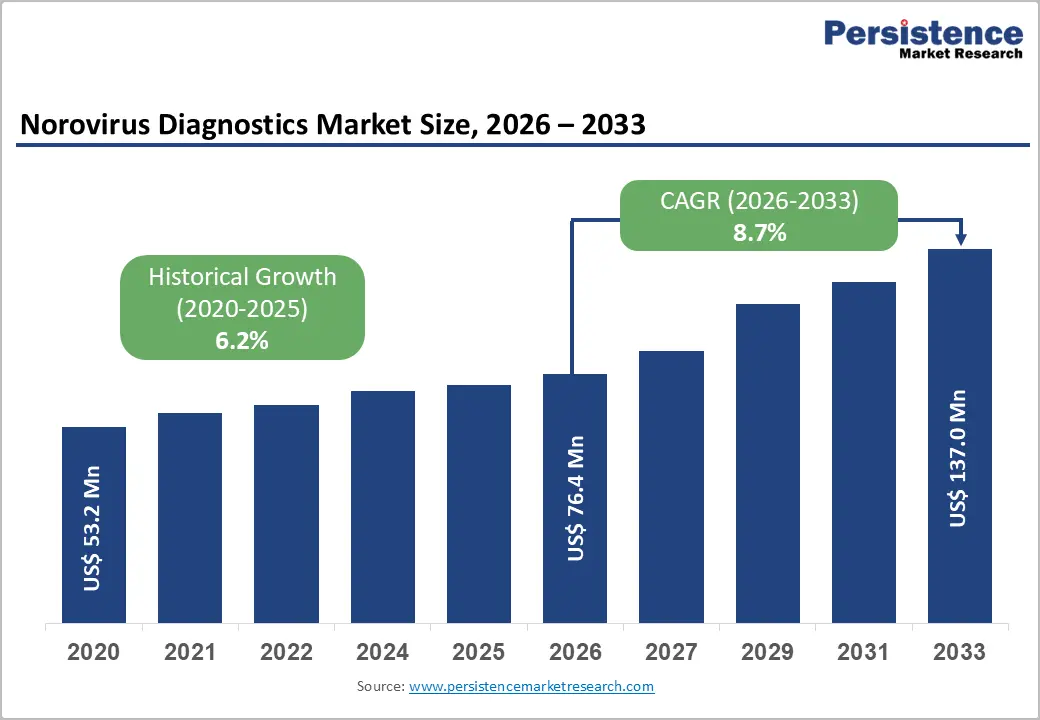

The global norovirus diagnostics market size is expected to be valued at US$ 76.4 million in 2026 and projected to reach US$ 137.0 million by 2033, growing at a CAGR of 8.7% between 2026 and 2033.

Rising incidence of norovirus outbreaks worldwide drives this growth, as CDC reports approximately 19 to 21 million cases annually in the U.S. alone, necessitating rapid and accurate diagnostics. Increasing adoption of advanced testing technologies like PCR supports expansion, with norovirus activity peaking earlier in recent seasons per CDC data, heightening demand in healthcare settings. Public health initiatives and outbreak surveillance further accelerate market momentum.

Key Market highlights

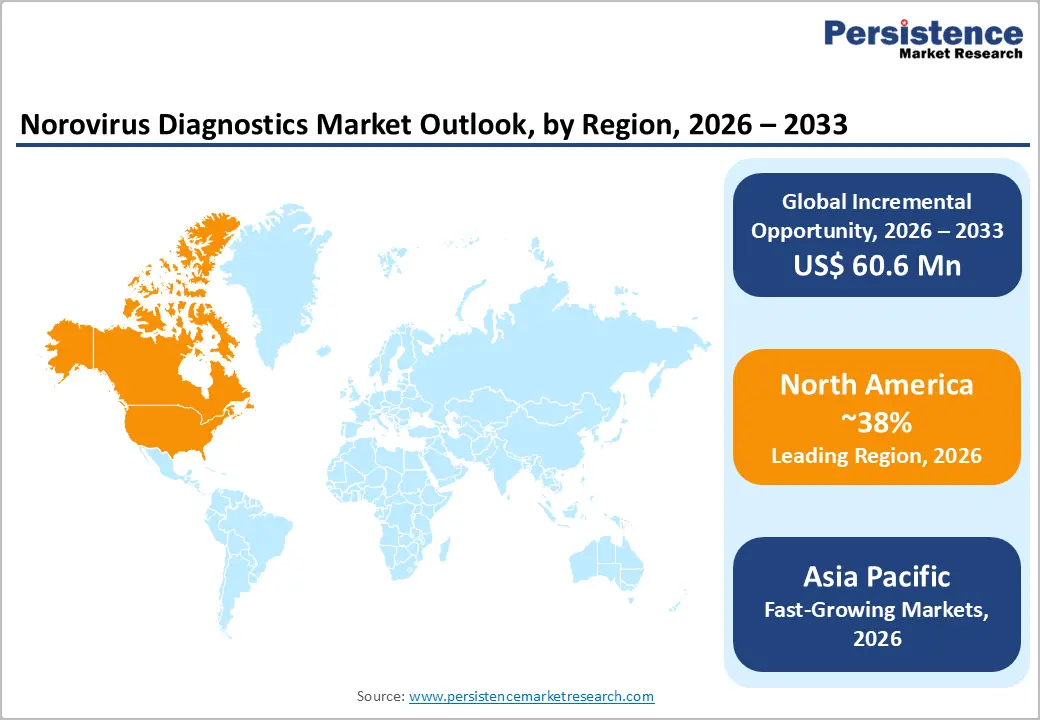

- North America remains the leading region in the norovirus diagnostics market, driven by high outbreak prevalence, advanced healthcare infrastructure, strong R&D investments, and robust regulatory frameworks supporting rapid adoption of innovative diagnostic technologies.

- Asia Pacific is expected to be the fastest?growing regional market, fuelled by Rising norovirus incidence, expanding healthcare access, increasing diagnostic laboratory networks, and government investments in surveillance programs across China, India, Japan, and Southeast Asian countries fuel rapid market growth.

- Rapid diagnostic kits are projected to hold the largest share at 58% in 2026, driven by demand for fast, accurate, and point-of-care detection in outbreak and clinical settings.

- Laboratories account for the largest value share and are growing fastest, as they provide high-volume, reliable testing using advanced molecular and PCR-based diagnostic platforms.

- Point-of-care testing innovations and portable molecular platforms offer real-time detection during outbreaks, enabling companies to expand adoption in clinics, community centers, and resource-limited settings.

| Key Insights | Details |

|---|---|

| Norovirus Diagnostics Market Size (2026E) | US$ 76.4 million |

| Market Value Forecast (2033F) | US$ 137.0 million |

| Projected Growth CAGR (2026-2033) | 8.7% |

| Historical Market Growth (2020-2025) | 6.2% |

Market Dynamics

Driver- Rising Incidence of Norovirus Disease

The rising global incidence of norovirus infections is a key driver for the norovirus diagnostics market. Norovirus is one of the leading causes of acute gastroenteritis and is highly contagious, resulting in frequent outbreaks across healthcare facilities, schools, long-term care centers, and community settings. Recent surveillance data highlight a sharp increase in outbreak activity, significantly exceeding historical seasonal averages. This escalation emphasizes the urgent need for rapid and accurate diagnostic solutions to enable early detection, timely isolation, and effective infection control measures.

The emergence and dominance of highly transmissible strains, such as GII.17, which accounted for a substantial share of recent outbreaks, further intensify diagnostic demand. These strains often spread rapidly within closed and semi-closed environments, increasing the risk of hospital-acquired infections and placing additional pressure on public health systems. As a result, healthcare providers increasingly rely on reliable and sensitive diagnostic tests to limit transmission and manage outbreaks efficiently.

In response to the growing disease burden, leading diagnostic and medical device manufacturers are significantly increasing their investments in research and development. The focus is on developing advanced molecular and immunoassay-based tests that offer higher sensitivity, faster turnaround times, and ease of use. These technological advancements are expected to support wider adoption of norovirus diagnostics in both clinical and surveillance settings.

Additionally, the expanding network of diagnostic laboratories, particularly in emerging economies, is positively influencing market growth. The increasing number of organized diagnostic chains and independent laboratories enhances testing accessibility and routine screening capabilities. Furthermore, rising awareness, improved healthcare infrastructure, and the gradual commercialization of norovirus diagnostics in low- and middle-income countries are creating new growth opportunities, reinforcing the long-term expansion of the global norovirus diagnostics market.

Restraint- Lack of Awareness about Norovirus

The market for norovirus diagnostics is being constrained by both prevalent social and economic factors. The burden of norovirus infection predominance in poor nations and the lack of knowledge about the signs that precede norovirus infection have slowed the growth of the norovirus diagnostics sector.

Furthermore, underdiagnosis of norovirus has negatively impacted patient health and wellbeing because of the internalised shame associated with not contacting doctors for norovirus illness owing to ignorance. Norovirus infection symptoms include cramps, nausea, vomiting, diarrhoea, and low-grade fever. Numerous other infections can potentially give these symptoms. Thus, there is a great likelihood that the illness will be incorrectly identified. Furthermore, most people dismiss these minor symptoms and diagnosis. Therefore, a lack of understanding could prevent the market for diagnosing norovirus infection from expanding.

Additionally, the emergence of potential competitors in the market has led to pricing competition among producers, which has functioned as a barrier to norovirus diagnostics uptake.

Opportunity- Point-of-Care Testing Innovations

Point-of-care testing innovations present a strong growth opportunity for the norovirus diagnostics market, particularly in outbreak-prone settings such as hospitals, long-term care facilities, schools, and cruise ships. POCT enables rapid, real-time detection of norovirus at or near the site of patient care, significantly reducing diagnostic turnaround time compared to centralized laboratory testing. Public health data highlighting thousands of norovirus outbreaks annually in the U.S. reinforces the need for portable, easy-to-use diagnostic tools that support immediate clinical and infection control decisions. As outbreak frequency and case volumes rise, demand for decentralized testing solutions continues to accelerate.

Technological advancements in molecular POCT platforms, especially those based on isothermal amplification, are creating competitive advantages for manufacturers. These platforms combine high sensitivity with minimal infrastructure requirements, making them suitable for clinics and resource-limited settings. Companies integrating such technologies into compact PCR-based kits are well positioned to capture market share, supporting PCR kits as the fastest-growing segment during the forecast period. Additionally, increasing regulatory support, growing clinician preference for rapid diagnostics, and expanding adoption of POCT in emerging markets further strengthen this opportunity, driving sustained revenue growth for innovation-focused diagnostic players.

Category-wise Insights

Product Analysis

Rapid test kits are projected to dominate the norovirus diagnostics market, accounting for an estimated 57.6% market share in 2026. Their leadership is driven by the increasing need for quick, on-site detection during outbreaks, where timely diagnosis is critical to infection control. Rapid kits offer shorter turnaround times, minimal infrastructure requirements, and ease of use, making them suitable for hospitals, clinics, and community settings. As norovirus outbreaks continue to rise globally, demand for rapid and reliable diagnostic solutions is accelerating, supporting strong revenue generation for this segment.

Technological limitations of conventional methods such as ELISA, which lack sufficient sensitivity and are unsuitable for real-time diagnosis, have further shifted preference toward advanced molecular approaches. Polymerase chain reaction (PCR) remains the most widely used technique due to its high accuracy, and manufacturers are increasingly developing faster, more refined rapid PCR-based kits. These innovations enhance sensitivity while reducing processing time, driving broader adoption. As a result, the rapid test kits segment is expected to grow profitably at a CAGR of 10.1% over the forecast period.

End User Analysis

Diagnostic laboratories held the largest value share of the global norovirus diagnostics market in 2026 and are expected to maintain their dominance throughout the forecast period. The rising incidence of norovirus infections globally has led to a substantial increase in diagnostic testing volumes, positioning laboratories as the primary centers for accurate and large-scale testing. Their ability to process high sample loads efficiently makes them the preferred end users compared to hospitals or point-of-care facilities.

Additionally, diagnostic laboratories are better equipped with advanced molecular platforms, skilled personnel, and standardized testing protocols, ensuring reliable and consistent results. The continued expansion of organized diagnostic chains and independent laboratories, particularly in emerging economies, further strengthens this segment’s growth outlook. Increasing investments in laboratory infrastructure and automation also support faster turnaround times and higher throughput. Consequently, diagnostic laboratories are expected to grow at a CAGR of 9.5% during the forecast period, reinforcing their central role in the norovirus diagnostics ecosystem.

Regional Insights

North America Norovirus Diagnostics Market Trends and Insights

North America represents a mature and highly developed market for norovirus diagnostics, with the U.S. accounting for nearly 80% of the regional market share in 2025. This dominance is primarily driven by the high prevalence of norovirus infections, frequent outbreak reporting, and strong surveillance systems across healthcare and community settings. The presence of leading diagnostic companies and advanced laboratory infrastructure further strengthens market growth. Continuous investments in research and development enable rapid innovation in molecular and rapid diagnostic technologies, supporting early detection and outbreak control.

Government initiatives also play a crucial role in market expansion. U.S. authorities have increased focus on strengthening healthcare systems, disease surveillance, and regulatory efficiency. Enhanced regulatory frameworks and faster approval pathways encourage commercialization of innovative diagnostic solutions. For instance, rising approval rates for diagnostic products reflect improved regulatory capacity and support industry growth. Additionally, widespread awareness among healthcare professionals, high testing volumes, and reimbursement coverage for diagnostic procedures contribute to sustained demand. Together, these factors position North America as a key revenue-generating region for the norovirus diagnostics market.

Europe Norovirus Diagnostics Market Trends and Insights

Europe represents a significant and steadily growing market for norovirus diagnostics, supported by strong public health surveillance systems and increasing awareness of foodborne and healthcare-associated infections. Countries such as the UK, Germany, France, and the Nordic nations report frequent norovirus outbreaks, particularly in hospitals, nursing homes, and community care facilities. Robust monitoring by regional health agencies has increased testing demand, reinforcing the need for accurate and timely diagnostic solutions.

The region benefits from well-established healthcare infrastructure and widespread adoption of molecular diagnostic techniques, including PCR-based assays. European laboratories emphasize standardized testing and outbreak containment, driving consistent demand from diagnostic laboratories. Additionally, rising government focus on infection prevention, aging populations vulnerable to gastroenteritis, and cross-border travel contribute to sustained testing volumes. Investments in laboratory automation and rapid diagnostics further enhance efficiency. While regulatory processes are relatively stringent, they ensure high-quality diagnostic adoption, supporting long-term market stability. As a result, Europe continues to demonstrate solid growth potential within the global norovirus diagnostics landscape.

Asia Pacific Norovirus Diagnostics Market Trends and Insights

Asia Pacific is emerging as the fastest-growing region in the norovirus diagnostics market, driven by increasing disease burden, expanding healthcare access, and improving diagnostic infrastructure. Rapid urbanization, dense populations, and rising food safety concerns contribute to higher norovirus transmission across countries such as China, India, Japan, and South Korea. Improved awareness among healthcare providers and patients is leading to higher testing rates, supporting market expansion.

The region is witnessing strong growth in diagnostic laboratories, including both organized chains and independent centers, which enhances accessibility to testing services. Governments are increasingly investing in healthcare modernization, disease surveillance programs, and laboratory capacity building, particularly in emerging economies. Adoption of cost-effective rapid and molecular diagnostic kits is accelerating, supported by local manufacturing and technology transfer. Additionally, increasing commercialization of diagnostics and growing private healthcare expenditure further fuel demand. Collectively, these factors position Asia Pacific as a high-growth opportunity region for norovirus diagnostics over the forecast period.

Competitive Landscape

Market Structure Analysis

The global norovirus diagnostics market is moderately consolidated, dominated by leading multinational diagnostic and medical device companies with strong R&D capabilities. Key players focus on developing rapid, sensitive, and PCR-based molecular kits to address rising outbreak demands. Strategic initiatives, including partnerships, product launches, and geographic expansion, strengthen competitive positioning. Mid-sized and regional players contribute through niche offerings and cost-effective solutions, particularly in emerging markets. Intense focus on innovation, regulatory compliance, and expanding diagnostic laboratory networks shapes market dynamics. The competitive environment encourages continuous technological advancement, supporting broader adoption of rapid and point-of-care testing solutions globally.?

Key Market Developments

- In February 2025, Creative Diagnostics, a prominent producer and supplier of antibodies, antigens, and assay kits, launched its new Norovirus VP1 VLP Panel to advance norovirus research.

- In October 2022, Otsuka Pharmaceutical and Denka launched QuickNavi™-Noro3, a norovirus antigen test kit, for medical institutions across Japan under co-marketing agreement.

Companies Covered in Norovirus Diagnostics Market

- Abbott

- R-Biopharm AG

- ELITechGroup AG

- Danaher Corporation (Cepheid)

- Meridian Bioscience Inc.

- Eiken Chemical Co.

- Altona Diagnostics GmbH

- CerTest Biotec S.L

- Elisabeth Pharmacon, Spol. S Ro

- Qiagen

- Altona Diagnostics GmbH

- Eiken Chemical Co

- Others

Frequently Asked Questions

The global norovirus diagnostics market is expected to reach US$ 76.4 million in 2026.

Rising global norovirus outbreaks, highly contagious strains, increased surveillance, and growing reliance on rapid, accurate diagnostic testing solutions.

North America holds 38% share in 2025, supported by FDA approvals and surveillance.

Expansion of point-of-care molecular diagnostics enabling rapid, on-site detection in outbreak settings and resource-limited healthcare environments.

Leading companies include Abbott, R-Biopharm AG, ELITechGroup AG, Danaher Corporation (Cepheid), Meridian Bioscience Inc. and Others.