- Healthcare Services

- Neurology Services Market

Neurology Services Market Size, Share, and Growth Forecast, 2026 – 2033

Neurology Services Market by Service Type (Diagnostics, Monitoring, Therapeutics, Surgical), Indication (Attention-Deficit/Hyperactivity Disorder (ADHD), Mental Health, Stroke, Concussion, Dementia, Multiple Sclerosis, Psychotic Disorder, Others), Service Provider (Neurofeedback Clinics, Clinics, Hospitals, Neurorehabilitation Centers, Academic & Research Institutes), and Regional Analysis for 2026-2033

Neurology Services Market Share and Trends Analysis

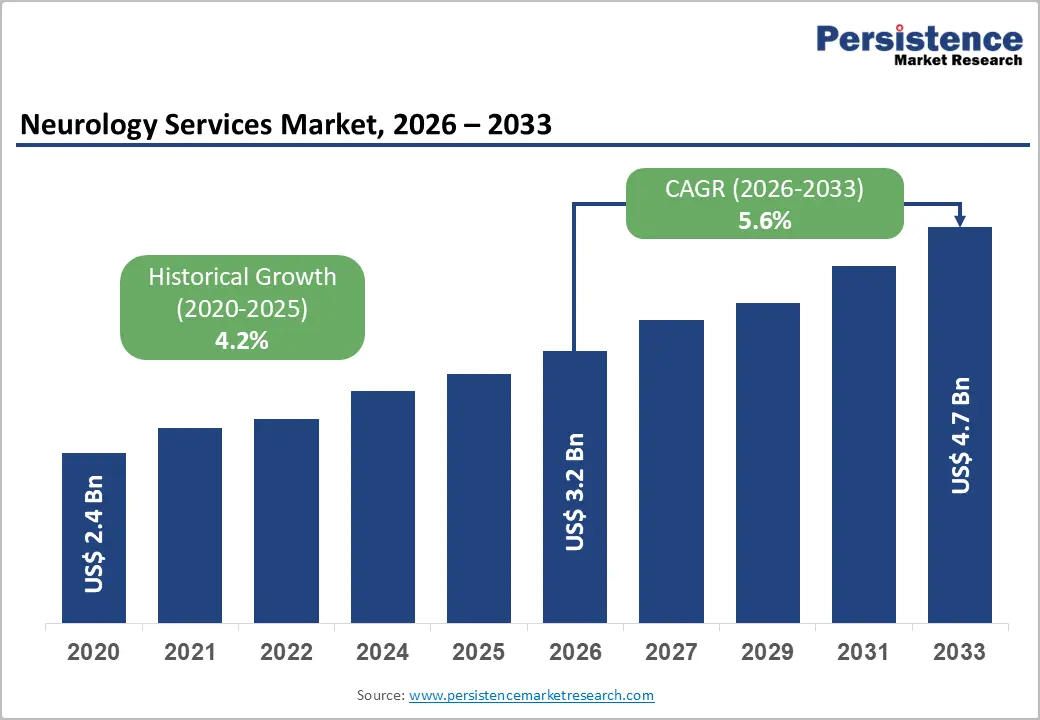

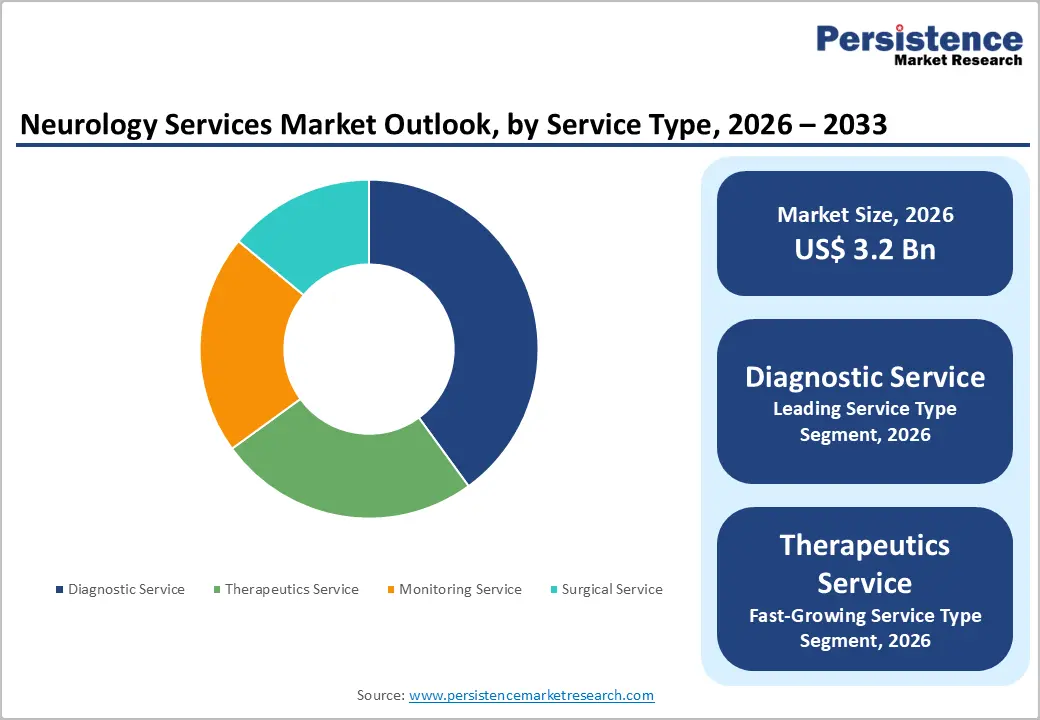

The global neurology services market size is likely to be valued at US$ 3.2 billion in 2026, and is projected to reach US$ 4.7 billion by 2033, growing at a CAGR of 5.6% during the forecast period 2026−2033.

Market expansion is driven by population aging and rising prevalence of neurological disorders, resulting in increased clinical consultations and long-term care requirements. Expanded clinical awareness and advanced diagnostic capabilities contribute to higher service adoption across urban and semi-urban centers. Integration of digital health and telemedicine platforms enhances service accessibility and patient adherence, enabling remote monitoring and follow-up.

Technological innovations, including AI-assisted diagnostics, neuroimaging, and wearable monitoring devices, improve operational efficiency and enable personalized care. Development of healthcare infrastructure, particularly in emerging markets, increases capacity for specialized neurology services.

Key Industry Highlights

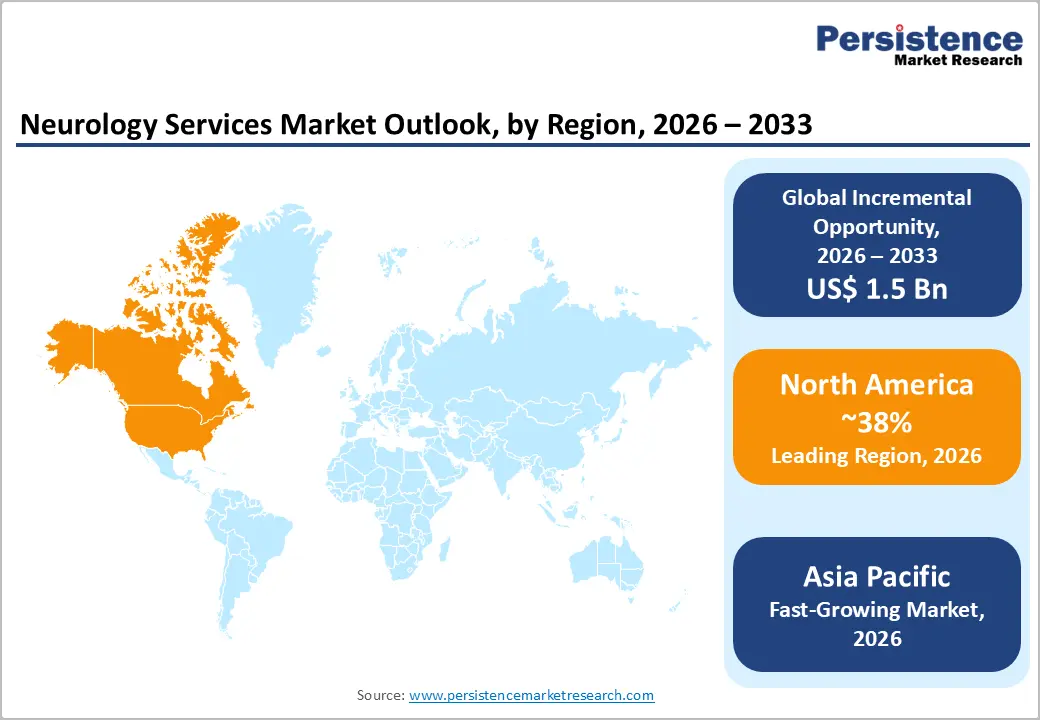

- Dominant Region: North America is projected to command approximately 38% market share in 2026, supported by advanced healthcare infrastructure in the United States and Canada.

- Fastest-growing Regional Market: Asia Pacific is forecast to be the fastest-growing market between 2026 and 2033, driven by healthcare expansion in China and India.

- Leading Service Type: Diagnostic services are slated to account for about 40% revenue share in 2026, due to strong use of magnetic resonance imaging (MRI), computed tomography (CT), and electroencephalogram (EEG) for early disease detection.

- Fastest-growing Service Type: Therapeutic services are likely to be the fastest-growing through 2033, fueled by the widening use of targeted drugs and neurostimulation therapies.

- January 2026: Novartis AG signed a US$ 1.7 billion licensing deal with SciNeuro Pharmaceuticals to develop new antibody therapies for Alzheimer disease.

| Key Insights | Details |

|---|---|

| Neurology Services Market Size (2026E) | US$ 3.2 Bn |

| Market Value Forecast (2033F) | US$ 4.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growing Neurological Disorder Prevalence

Escalating incidence of neurological disorders significantly increases demand for specialized clinical evaluation, imaging diagnostics, and long-term disease management. Disorders such as stroke, dementia, epilepsy, Parkinson disease, and migraine require continuous monitoring, rehabilitation programs, and pharmacological management delivered through specialized clinical settings. In 2025, the World Health Organization (WHO) reported that neurological conditions affect more than 3 billion individuals worldwide, representing a substantial clinical burden that requires structured neurological care services and multidisciplinary treatment frameworks. This large patient population increases demand for neurologists, neuroimaging diagnostics, neurocritical care units, and rehabilitation programs within healthcare systems.

Healthcare systems increasingly prioritize early detection, continuous monitoring, and multidisciplinary intervention strategies for neurological conditions, strengthening demand for advanced neurological care delivery models. Progressive neurological diseases frequently produce long-term disability, cognitive decline, and functional impairment, requiring integrated care pathways that include diagnostics, pharmacological therapy, rehabilitation, and cognitive support services. Such clinical complexity encourages expansion of specialized treatment centers, neurorehabilitation units, and digital monitoring platforms that support long-term disease management.

Adoption of Telehealth and Digital Platform

Digital health ecosystems and teleconsultation platforms reshape neurological care delivery by reducing geographic barriers and enabling continuous specialist interaction. Remote consultations support evaluation of chronic neurological conditions that require frequent follow-ups, medication adjustments, and symptom monitoring. Video-based assessments, integrated electronic health records, and secure communication systems allow clinicians to review imaging results, track clinical progression, and coordinate multidisciplinary treatment plans without physical visits. A survey by the American Medical Association reported that 98% of neurologists used telehealth in clinical practice, demonstrating widespread integration of virtual consultation tools in neurological care delivery during 2025.

Remote monitoring technologies and digital platforms strengthen long-term neurological management through continuous data collection and early clinical intervention. Wearable monitoring devices, smartphone-based neurological assessment tools, and cloud-connected diagnostic systems allow clinicians to track symptoms such as motor changes, seizure activity, and cognitive fluctuations in real time. Chronic neurological disorders require prolonged monitoring and rehabilitation support; digital platforms facilitate regular follow-ups without frequent hospital visits. Telestroke networks and remote neurological consultations enable faster specialist input in emergency scenarios, improving treatment timelines in regions lacking neurologists.

High Cost of Neurological Treatments

Escalating treatment expenditure represents a major structural barrier within neurological care delivery. Clinical management of brain and nerve disorders requires a combination of advanced diagnostic imaging, long-term pharmacotherapy, neurosurgical procedures, rehabilitation programs, and continuous monitoring services. These interventions demand specialized infrastructure, trained neurologists, and high-precision equipment such as magnetic resonance imaging systems and neurophysiological testing platforms. Pharmaceutical innovation further intensifies cost pressure. Biologic drugs, disease-modifying therapies, and gene-based treatments involve complex research pipelines, regulatory evaluation, and highly controlled manufacturing environments.

Economic burden increases further through lifelong disease management requirements. Disorders such as Alzheimer disease, Parkinson disease, epilepsy, and multiple sclerosis frequently require continuous medication, periodic imaging assessments, rehabilitation services, and caregiver support across many years. Health insurance coverage limitations and reimbursement disparities across regions shift a significant portion of expenses toward households and healthcare providers. Advanced therapies, including precision biologics and gene-targeted interventions, require specialized treatment centers, cold-chain logistics, and strict monitoring protocols, which elevate operational costs for hospitals and neurology clinics.

Shortage of Trained Neurologists

Limited availability of specialized neurological professionals creates a structural constraint across clinical care systems and referral networks. Training pathways for neurology remain lengthy and resource-intensive, requiring extended residency, subspecialty fellowships, and advanced clinical infrastructure. Many medical graduates select other specialties that offer shorter training timelines or broader employment flexibility, reducing the annual pipeline of neurologists entering practice. Geographic concentration of specialists within major metropolitan hospitals further restricts access across rural and semi-urban healthcare networks.

Structural and operational factors further intensify workforce limitations. Neurological conditions frequently require complex diagnostic evaluation, continuous monitoring, and long-term management, which increases physician workload and consultation time per patient. High clinical workload, administrative responsibilities, and limited reimbursement structures reduce workforce retention and contribute to professional burnout. Retirement of experienced neurologists combined with slower replacement through new training programs reduces available expertise within healthcare systems.

Development of Personalized Neurology Therapies

Personalized neurology therapies represent a significant opportunity due to the clinical complexity and heterogeneity of neurological disorders. Conditions such as stroke, dementia, Parkinson disease, epilepsy, and multiple sclerosis demonstrate varied genetic, molecular, and environmental characteristics across patient populations. Standardized treatment pathways often deliver limited therapeutic response in diverse patient groups, which increases clinical demand for individualized treatment strategies. Precision-based interventions using genomic analysis, biomarker profiling, and advanced neuroimaging enable clinicians to identify disease subtypes and tailor treatment protocols according to specific neurological pathways. Integration of personalized treatment planning improves therapeutic targeting, enhances treatment response, and reduces adverse effects in long-term neurological care.

The rising burden of neurological conditions further reinforces the strategic value of individualized therapeutic models. According to the U.S. Centers for Disease Control and Prevention (CDC), around 795,000 individuals experience stroke each year in the United States, demonstrating a substantial neurological disease burden requiring long-term clinical management. Precision-driven neurology approaches support early disease stratification, targeted pharmacological interventions, and patient-specific rehabilitation planning. Integration of genomic medicine, biomarker-based diagnostics, and digital neurological monitoring tools facilitates development of tailored clinical pathways that align with patient-level disease progression patterns. Healthcare providers increasingly prioritize precision neurology programs within specialized neurological clinics, research hospitals, and academic medical centers.

Integration of AI and ML in Diagnostics

Artificial intelligence (AI) and machine learning (ML) technologies create strong opportunity within neurological diagnostics through capacity to process complex clinical data, imaging outputs, and patient monitoring signals with high computational precision. Neurological conditions require interpretation of multiple data streams such as magnetic resonance imaging, electroencephalography signals, genetic markers, and behavioral assessments. Conventional diagnostic workflows require extensive specialist interpretation, creating delays in treatment initiation. Machine learning models analyze imaging patterns, neurological signals, and longitudinal clinical records simultaneously, enabling earlier detection of abnormalities and improved clinical decision support. The application of predictive analytics strengthens identification of disease progression patterns and treatment response indicators.

Another structural factor strengthening this opportunity involves increasing demand for diagnostic accuracy and workforce efficiency within neurological care systems. Neurological disorders require early identification to prevent irreversible damage and long-term disability, yet clinical resources remain limited in several healthcare systems. Artificial intelligence enables automated interpretation of neuroimaging and clinical datasets, reducing diagnostic burden on specialists and improving consistency of evaluation. According to the World Health Organization, 64% of countries reported active use of AI-assisted diagnostics in health systems in 2025, demonstrating expanding integration of algorithm-supported clinical tools in disease detection and screening.

Category-wise Analysis

Service Type Insights

Diagnostic service is poised to lead with a forecasted 40% of the neurology services market revenue share in 2026, owing to high demand for early disease detection, precision neuroimaging, and routine monitoring protocols. Adoption of MRI, CT scans, EEG, and advanced imaging modalities by hospitals and specialized clinics drives segment revenue. Clinical preference for evidence-based diagnostics ensures repeated utilization, while technological advancements increase throughput and reduce operational overhead. Structured diagnostic pathways in stroke units, dementia clinics, and epilepsy centers require periodic imaging and neurological evaluation, strengthening service demand.

Therapeutics service is anticipated to be the fastest-growing segment between 2026 and 2033, fueled by expanding adoption of targeted pharmacological interventions, neurostimulation techniques, and minimally invasive therapies. Increasing prevalence of chronic neurological disorders necessitates long-term treatment regimens, driving recurring revenue streams. Provider preference for effective interventions combined with improved patient adherence supports segment growth. Expanding use of disease-modifying therapies, neuromodulation devices, and infusion-based treatments strengthens service demand across specialized neurology clinics and hospitals.

Indication Insights

Stroke is likely to be the leading segment with a projected 35% market share in 2026, due to high incidence, established clinical protocols, and government-supported preventive initiatives. Stroke units in hospitals provide comprehensive care, including diagnostics, therapeutics, and rehabilitation services. Consumer trust in specialized care and structured clinical pathways promotes adoption. Rapid triage systems and emergency neurological response teams enable early diagnosis and treatment, improving patient outcomes and increasing service utilization. Standardized protocols involving neuroimaging, thrombolytic therapy, and rehabilitation programs require coordinated multidisciplinary care.

Dementia is expected to grow the fastest between 2026 and 2033, driven by aging populations, rising public awareness, and increased screening initiatives. Digital health tools enable remote cognitive monitoring and early intervention, improving treatment adherence. Emerging therapeutics targeting disease modification and symptom management expand commercial opportunities. Memory clinics, community screening programs, and specialized neurology departments are expanding diagnostic and therapeutic services for cognitive disorders. Cognitive assessment platforms supported by digital applications allow physicians to track behavioral and neurological changes over time.

Regional Insights

North America Neurology Services Market Trends

North America is expected to dominate with an estimated 38% of the neurology services market share in 2026, reflecting a highly developed neurological care ecosystem, strong clinical research infrastructure, and advanced diagnostic capabilities. The United States and Canada represent the central contributors to regional service revenue due to dense concentration of tertiary hospitals, neuroscience institutes, and specialized stroke centers. High utilization of magnetic resonance imaging, computed tomography, electroencephalography, and positron emission tomography enables early detection and continuous monitoring of complex neurological conditions. Large hospital networks in the United States operate integrated neurology departments that combine diagnostics, therapeutic procedures, neurocritical care, and rehabilitation services under coordinated clinical frameworks.

Another defining factor supporting regional dominance involves strong adoption of technology-enabled neurological care combined with high healthcare expenditure and clinical workforce specialization. Hospitals and neuroscience centers across the United States implement artificial intelligence–supported neuroimaging interpretation, robotic surgical platforms, and digital neurological monitoring systems that improve diagnostic precision and treatment efficiency. Widespread availability of neurologists, neurosurgeons, neuropsychologists, and rehabilitation specialists enables multidisciplinary treatment frameworks for stroke, neurodegenerative diseases, epilepsy, and traumatic brain injury.

Europe Neurology Services Market Trends

Europe represents a mature neurological healthcare landscape characterized by structured public health systems, advanced clinical networks, and coordinated neurological research programs. Countries such as Germany, France, and the United Kingdom maintain large hospital systems equipped with specialized neurology departments, stroke units, and neurorehabilitation centers that support comprehensive management of neurological disorders. Germany demonstrates strong capacity through technologically advanced hospitals that integrate neuroimaging platforms, neurocritical care units, and multidisciplinary treatment teams. France maintains extensive neurological diagnostic networks supported by national health insurance coverage that enables broad patient access to imaging and therapeutic services.

Healthcare systems across Italy, Spain, and the Netherlands emphasize long-term neurological care through rehabilitation programs, cognitive care services, and community-based neurological support structures. Italy supports specialized neurological institutes that provide integrated services including diagnostic imaging, neurosurgical procedures, and post-treatment rehabilitation programs for stroke and neurodegenerative disorders. Spain continues expansion of regional stroke networks that link emergency response units with advanced neurological hospitals to ensure rapid treatment delivery. The Netherlands demonstrates strong implementation of digital health technologies, enabling remote neurological consultations and continuous monitoring of chronic neurological conditions.

Asia Pacific Neurology Services Market Trends

Asia Pacific is forecasted to be the fastest-growing market for neurology services between 2026 and 2033, stimulated by expanding neurological disease burden, rapid healthcare infrastructure development, and increasing government focus on early diagnosis and treatment of brain disorders. China demonstrates strong expansion through large-scale hospital construction programs and national neurological disease prevention initiatives that strengthen stroke management capacity and neuroimaging access. India shows accelerated service expansion through rising investment in tertiary care hospitals, growth of private neurology clinics, and increasing availability of advanced diagnostic technologies in metropolitan healthcare networks. Healthcare policy reforms across several economies support expansion of medical insurance coverage and funding for neurological treatment programs.

Another structural factor supporting rapid expansion involves rising integration of advanced treatment technologies and specialized clinical training programs across major healthcare systems. Japan demonstrates strong adoption of precision neurological diagnostics, robotics-assisted neurosurgery, and high-resolution neuroimaging platforms within university hospitals and specialized neuroscience centers. South Korea continues expansion through technology-driven hospitals and advanced neuromodulation therapy programs for conditions such as Parkinson disease and epilepsy. Expansion of memory clinics, stroke centers, and neurorehabilitation facilities strengthens long-term neurological care capacity.

Competitive Landscape

The global neurology services market structure features moderate fragmentation, with leading organizations maintaining strong influence through advanced therapeutics, neurodiagnostic technologies, and integrated treatment platforms. Leading players include F. Hoffmann-La Roche Ltd, Pfizer Inc., Novartis AG, Medtronic, and Siemens Healthcare Private Limited, collectively holding an estimated 25–30% market share. Competitive positioning is shaped by extensive research capabilities, global healthcare partnerships, and technological innovation across neurological diagnostics and treatment systems.

Competition across the industry extends beyond pharmaceutical development toward integrated neurological care solutions that combine diagnostics, therapeutic interventions, and digital health technologies. Hospitals and specialized neurology centers increasingly collaborate with technology developers and pharmaceutical manufacturers to strengthen treatment pathways and expand clinical capabilities. Medical technology providers continue development of artificial intelligence–supported neuroimaging platforms and data-driven neurological monitoring tools that enhance diagnostic precision and workflow efficiency.

Key Industry Developments

- In January 2026, Zydus Hospitals acquired the Vadodara Institute of Neurological Sciences (VINS) Hospital, integrating the 50-bed specialized neuro facility with its 300-bed multispecialty hospital to strengthen neurology and neurosurgery services and expand access to advanced neurological care in Gujarat.

- In October 2025, Ram Manohar Lohia Institute of Medical Sciences in Lucknow initiated installation of a Gamma Knife system designed to deliver high-precision, non-invasive treatment for brain tumors and neurological disorders, supported by government investment to expand advanced neuro care capacity.

- In April 2025, Quest Diagnostics launched the AD-Detect™ Abeta 42/40 and p-tau217 Evaluation blood test to help physicians confirm Alzheimer disease pathology in patients with mild cognitive impairment or dementia, supporting earlier and less invasive neurological diagnosis.

Companies Covered in Neurology Services Market

- F. Hoffmann-La Roche Ltd

- Pfizer Inc.

- Medtronic

- Novartis AG

- Siemens Healthcare Private Limited

- GE HealthCare.

- Abbott.

- Boston Scientific Corporation

- Johnson & Johnson

- Biogen

Frequently Asked Questions

The global neurology services market is projected to reach US$ 3.2 billion in 2026.

Rising prevalence of neurological disorders, aging population, and increasing adoption of advanced diagnostic and therapeutic technologies are driving the market.

The market is poised to witness a CAGR of 5.6% from 2026 to 2033.

Expansion of AI-assisted diagnostics, growth of tele-neurology services, and development of advanced neurotherapeutics are creating significant opportunities.

Some of the key market players include F. Hoffmann-La Roche Ltd, Pfizer Inc., Medtronic, Novartis AG, and Siemens Healthcare Private Limited.