- Medical Devices

- Nephrology Lasers Market

Nephrology Lasers Market Size, Share, and Growth Forecast, 2025 - 2032

Nephrology Lasers Market by Product Type (Holmium Lasers, Thulium Lasers, Others), Application (Kidney Stone Management, Tumor Ablation, Others), End-use (Hospitals, Ambulatory Surgical Centers, Specialty Clinics, Others), and Regional Analysis for 2025 - 2032

Nephrology Lasers Market Size and Trends Analysis

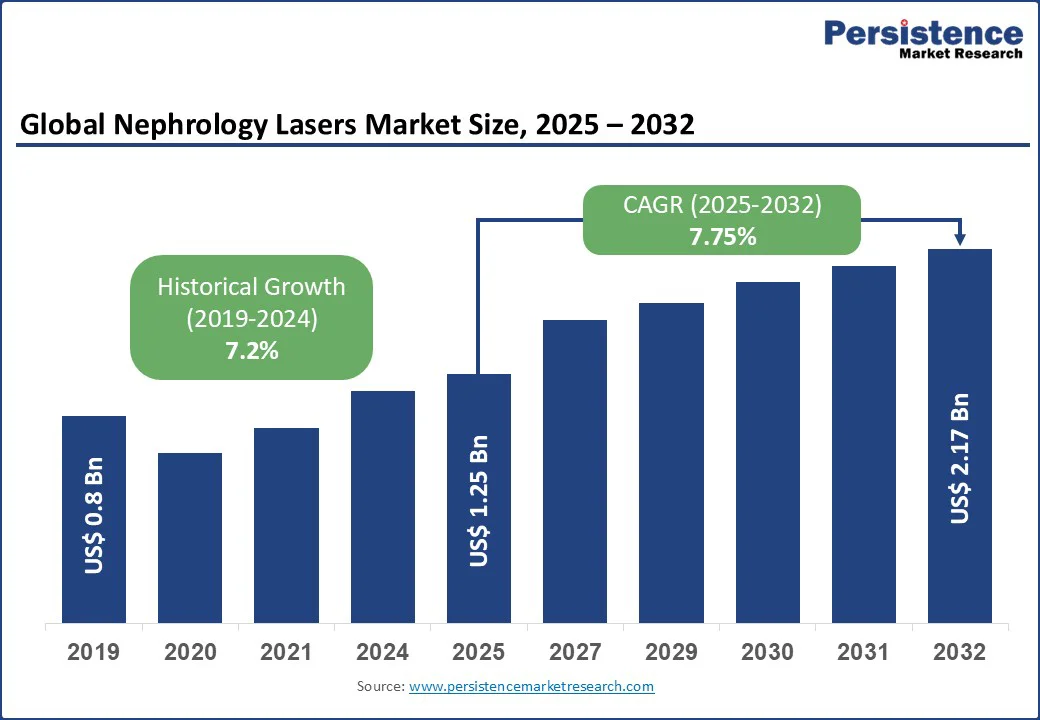

The global nephrology lasers market size is likely to be valued at US$1.25 Bn in 2025 and reach US$2.17 Bn by 2032, growing at a CAGR of 7.75% during the forecast period from 2025 to 2032.

Key Industry Highlights

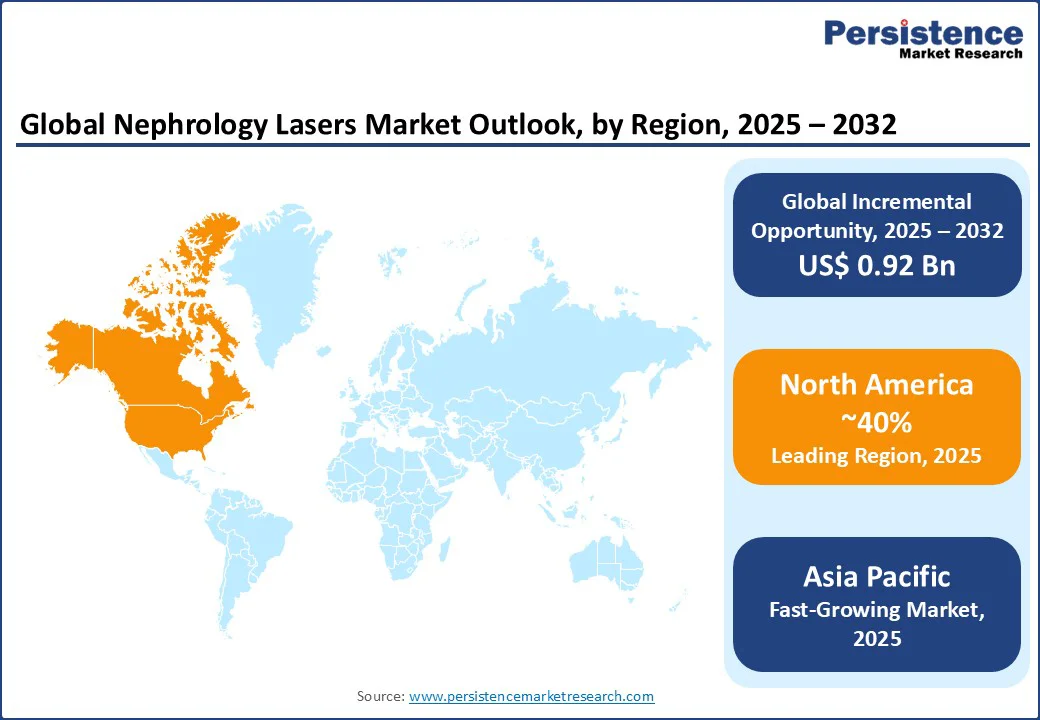

- Leading Region: North America, commanding a 40% market share in 2025, driven by the high prevalence of kidney stones, advanced healthcare systems, and the strong presence of key players in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by increasing healthcare investments, rising kidney disease cases, and growing adoption of minimally invasive technologies in countries such as India and China.

- Investment Plans: Asia Healthcare Holdings (AHH), backed by GIC and TPG, announced a ? 400 crore investment over the next 4-5 years into the Asian Institute of Nephrology and Urology (AINU), aiming to expand and double its hospital network. This represents a major regional investment in nephrology care infrastructure.

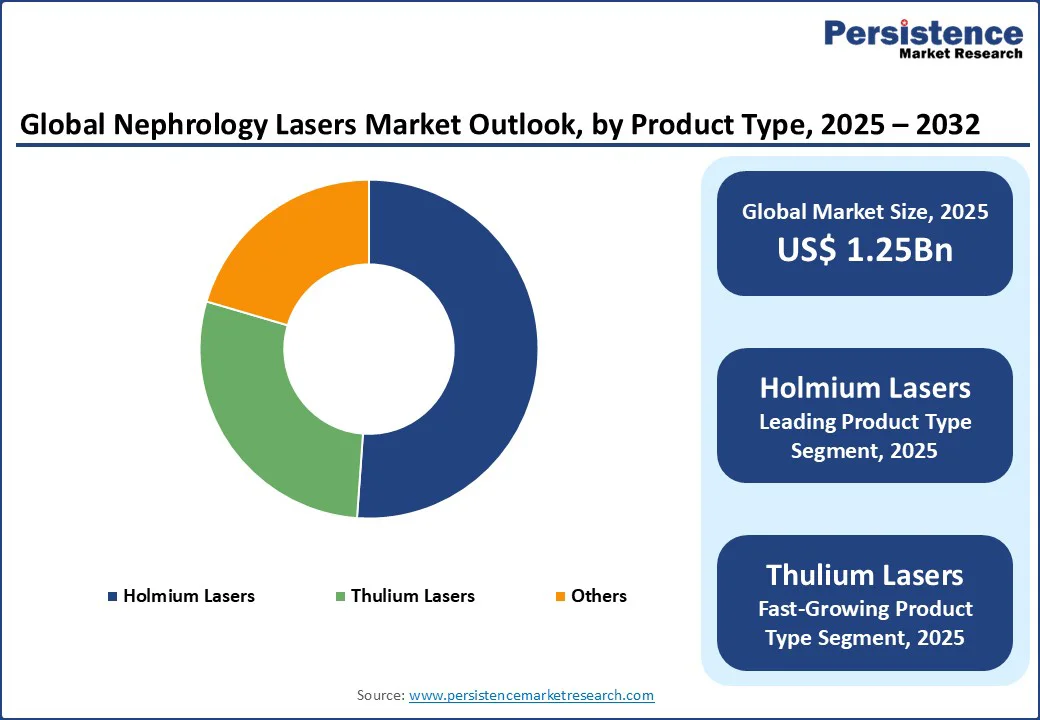

- Dominant Product Type: Holmium lasers is expected to account for 45% share in 2025 of the nephrology lasers market share due to their widespread use in kidney stone management and versatility in urological applications.

- Leading End-use: Hospitals, contributing over 60% of market revenue, driven by their advanced infrastructure and high volume of nephrological procedures.

| Global Market Attribute | Key Insights |

|---|---|

| Nephrology Lasers Market Size (2025E) | US$ 1.25Bn |

| Market Value Forecast (2032F) | US$ 2.17Bn |

| Projected Growth (CAGR 2025 to 2032) | 7.75% |

| Historical Market Growth (CAGR 2019 to 2024) | 7.2% |

The nephrology lasers industry is witnessing significant growth, propelled by the increasing prevalence of kidney-related disorders, advancements in laser technology, and a rising preference for minimally invasive procedures. Nephrology lasers, such as Holmium and Thulium lasers, are valued for their precision and efficacy in treating conditions such as kidney stones and tumors, offering reduced recovery times and fewer complications.

The expansion of healthcare infrastructure, particularly in developed and emerging markets, and the growing adoption of advanced laser systems in urological procedures further drive market growth.

Rising Prevalence of Kidney-related Disorders Prompts the Urgency for Treatment Solutions

The increasing incidence of kidney-related disorders, such as kidney stones and chronic kidney disease (CKD), is a primary driver of the global nephrology lasers market. According to the National Kidney Foundation, approximately 10% of the global population is affected by CKD, with kidney stones impacting 1 in 10 individuals worldwide.

Government initiatives, such as the U.S. National Institutes of Health funding research on laser-based treatments, further support market growth. In emerging markets such as India, rising healthcare awareness and investments in urological care are boosting adoption, ensuring sustained market expansion through 2032.

High Costs and Regulatory Challenges Limit Adoption

High costs associated with nephrology laser systems and stringent regulatory frameworks pose significant challenges to market growth, particularly for smaller healthcare providers. The acquisition and maintenance of advanced laser systems, such as Holmium and Thulium lasers, can cost upwards of $100,000, limiting accessibility in low-resource settings. Additionally, regulatory bodies such as the U.S. FDA and the European Medicines Agency enforce rigorous safety and efficacy standards, increasing compliance costs for manufacturers.

In July 2023, the FDA announced a recall for multiple models of Boston Scientific's Flexiva Pulse 242 laser fibers, which are used in urological procedures. The recall was due to concerns about the devices not meeting quality standards. In emerging markets such as Africa, limited regulatory oversight and inconsistent quality standards further hinder market penetration. At the same time, consumer skepticism about the long-term efficacy of laser treatments also restricts widespread adoption.

Growing Demand for Minimally Invasive Procedures

The rising preference for minimally invasive procedures presents significant opportunities for the nephrology lasers market. Consumers and healthcare providers are increasingly opting for laser-based treatments, such as lithotripsy and tumor ablation, due to their precision, reduced recovery times, and minimal side effects.

In the Asia Pacific, companies such as Olympus Corporation have reported growth in sales of Thulium laser systems for urological applications in 2024. Government initiatives, such as the EU’s Health Programme, which promotes advanced medical technologies, encourage innovation in laser systems.

Hospitals and ambulatory surgical centers are investing in portable and high-precision laser devices, enabling brands such as Lumenis Ltd. and Quanta System S.p.A. to capitalize on premiumization trends through 2032, aligning with global healthcare goals of improving patient outcomes.

The demand for minimally invasive procedures, such as laser lithotripsy, has surged due to their precision, reduced recovery times, and lower complication rates compared to traditional surgeries. For instance, Boston Scientific Corporation reported an increase in sales of its Holmium laser systems in 2024, driven by their efficacy in kidney stone fragmentation.

Category-wise Analysis

Product Type Insights

- Holmium lasers dominate the nephrology lasers market, holding approximately 45% of the market share in 2025. Their widespread use in kidney stone management, due to their effectiveness in fragmenting stones and minimal tissue damage, makes them a preferred choice in urology. Companies such as Boston Scientific Corporation and Lumenis Ltd. lead with advanced Holmium laser systems, such as the Lumenis Pulse 120H integrated with MOSES technology, which enhances precision in procedures across North America and Europe.

- Thulium lasers are the fastest-growing segment, driven by their superior performance in stone ablation and tissue vaporization. They offer superior hemostatic properties, reduced postoperative complications, and are increasingly preferred in BPH treatments. In India, large medical institutions such as Safdarjung Hospital in New Delhi are integrating TFL technology into their urology departments. The hospital is acquiring a thulium fiber laser as part of an initiative to enhance diagnostic and treatment capabilities, aiming to benefit a significant portion of its daily patient load.

Application Insights

- Kidney stone management is the leading application, accounting for over 50% of the market share for the nephrology lasers market in 2025. The high global prevalence of kidney stones, particularly in North America and the Asia Pacific, drives demand for laser lithotripsy. Companies such as Olympus Corporation and Cook Medical offer advanced laser systems for precise stone fragmentation, supported by innovations such as MOSES technology for improved procedural outcomes.

- Tumor ablation is the fastest-growing application, fueled by the rising incidence of kidney cancers and the demand for minimally invasive treatments. Laser-based tumor ablation offers precision and reduced recovery times, with companies such as Richard Wolf GmbH and Quanta System S.p.A. expanding their offerings to meet growing needs in Europe and North America.

End-use Insights

- Hospitals dominate the end-use segment, contributing over 60% of market revenue in 2025. Their advanced infrastructure, skilled professionals, and high patient volumes make them the primary setting for nephrological laser procedures. Major players, such as Karl Storz SE & Co. KG and Stryker Corporation, supply hospitals with cutting-edge laser systems, particularly in North America and Europe.

- Ambulatory surgical centers (ASCs) are the fastest-growing end-use segment, driven by their cost-effectiveness and ability to perform outpatient procedures. The convenience of same-day discharge and increasing adoption of minimally invasive laser treatments, supported by companies such as Dornier MedTech GmbH, fuel their growth in the Asia Pacific and North America.

Regional Insights

North America Nephrology Lasers Market Trends

North America leads the global market, holding approximately 40% of the worldwide market share in 2025. A study analyzing data from the National Health and Nutrition Examination Survey (NHANES) reported a prevalence of kidney stones at 8.8% among U.S. adults, equating to roughly 1 in 11 individuals. The American Urological Association reports an annual increase in laser lithotripsy procedures, reflecting strong consumer demand for minimally invasive treatments.

Major players, such as Boston Scientific Corporation and Lumenis Ltd., drive innovation with advanced laser systems such as the MOSES-enabled Holmium lasers. The U.S. benefits from significant government funding, such as NIH grants for urological research, enhancing market growth. Canada’s well-established healthcare system further supports adoption, ensuring North America’s leadership through 2032.

Asia Pacific Nephrology Lasers Market Trends

Asia Pacific is the fastest-growing regional market for the nephrology lasers market, propelled by rising healthcare investments and increasing kidney disease prevalence in countries such as India and China. Combining urology lasers with advanced imaging technologies allows for real-time visualization, enabling surgeons to perform procedures more accurately and safely.

Government initiatives, such as India’s National Health Mission, promote advanced medical technologies, boosting the adoption of Holmium and Thulium lasers. Companies such as Olympus Corporation and Quanta System S.p.A. are expanding their presence, with China reporting an increase in laser lithotripsy procedures in 2024. Rising disposable incomes and health awareness further accelerate market growth.

Europe Nephrology Lasers Market Trends

Europe is the second fastest-growing region in the nephrology lasers market, driven by stringent regulatory frameworks and rising demand for minimally invasive procedures in countries such as Germany and France. Recent studies indicate a significant shift towards laser treatments in Europe.

From 2019 to 2023, the proportion of transurethral resection of the prostate (TURP) cases declined from 74% to 64.5%, while laser treatment and minimally invasive surgical treatment (MIST) cases increased by 8.2% and 1.11%, respectively, on average, fueled by consumer preference for advanced treatments.

The EU’s Health Programme supports innovation in medical technologies, encouraging companies such as Karl Storz SE & Co. KG and Richard Wolf GmbH to develop high-precision laser systems. Germany’s advanced healthcare infrastructure and France’s focus on urological research further drive market expansion, positioning Europe as a key growth region through 2032.

Competitive Landscape

The global nephrology lasers market is highly competitive, with key players such as Boston Scientific Corporation, Lumenis Ltd., and Quanta System S.p.A. dominating through extensive product portfolios and global distribution networks. Regional players, such as Dornier MedTech GmbH and Richard Wolf GmbH, focus on specialized offerings in Europe and the Asia Pacific.

Companies are investing in technological advancements, such as Thulium laser systems and portable devices, to enhance market share, driven by the demand for minimally invasive solutions.

Key Industry Developments:

- July 2025: The LEONARDO Duster is a Super-Pulsed Thulium Fiber Laser (TFL) device approved by the FDA for urological procedures like laser lithotripsy. Compared to Holmium:YAG lasers, it offers potentially higher lithotripsy efficiency, a lower risk of stone retropulsion, and enhanced safety due to limited penetration depth and temperature increase within the tissue.

- April 2024: Quanta System S.p.A. unveiled the Cyber Ho Magneto, a Holmium laser system incorporating Quanta Magneto Technology™. This innovation was introduced during the 39th European Association of Urology Congress (EAU) in Paris. The Cyber Ho Magneto is the first laser system to harness the peak power of Holmium and convert it into a much longer pulse duration, providing dusting capabilities comparable to Thulium Fiber Lasers (TFL).

Companies Covered in Nephrology Lasers Market

- Boston Scientific Corporation

- Olympus Corporation

- Cook Medical

- Lumenis Ltd.

- Dornier MedTech GmbH

- Richard Wolf GmbH

- Karl Storz SE & Co. KG

- Stryker Corporation

- EDAP TMS S.A.

- Quanta System S.p.A.

- Becton, Dickinson and Company

- Others

Frequently Asked Questions

The Nephrology Lasers market is projected to reach US$1.25 Bn in 2025.

The rising prevalence of kidney-related disorders and increasing demand for minimally invasive procedures are the key market drivers.

The Nephrology Lasers market is poised to witness a CAGR of 7.75% from 2025 to 2032.

The growing demand for minimally invasive procedures is the key market opportunity.

Boston Scientific Corporation, Olympus Corporation, Lumenis Ltd., and Quanta System S.p.A. are a few key market players.