- Specialty & Fine Chemicals

- Neopentyl Glycol Market

Neopentyl Glycol Market Size, Share, and Growth Forecast 2025 - 2032

Neopently Glycol Market by Grade (Flakes, Molten, Slurry), Application (Lubricants, Plasticizers, Coatings & Resins, Others), Industry (Automotive, Construction, Electronics, Pharmaceuticals), and Regional Analysis 2025 - 2032

Neopentyl Glycol Market Share and Trends Analysis

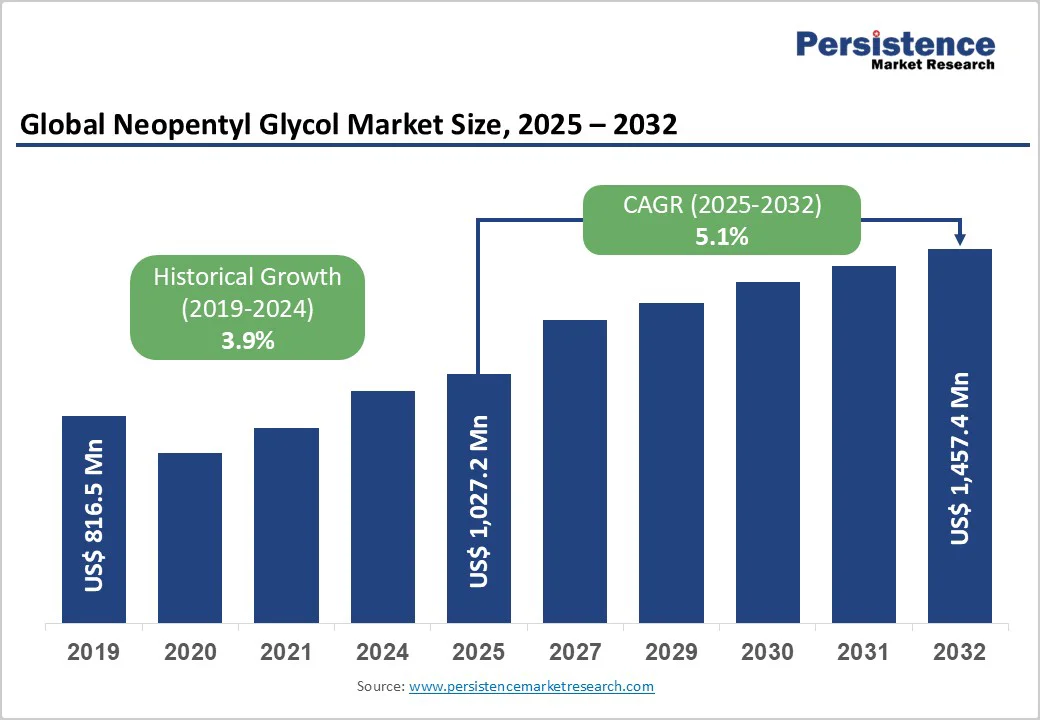

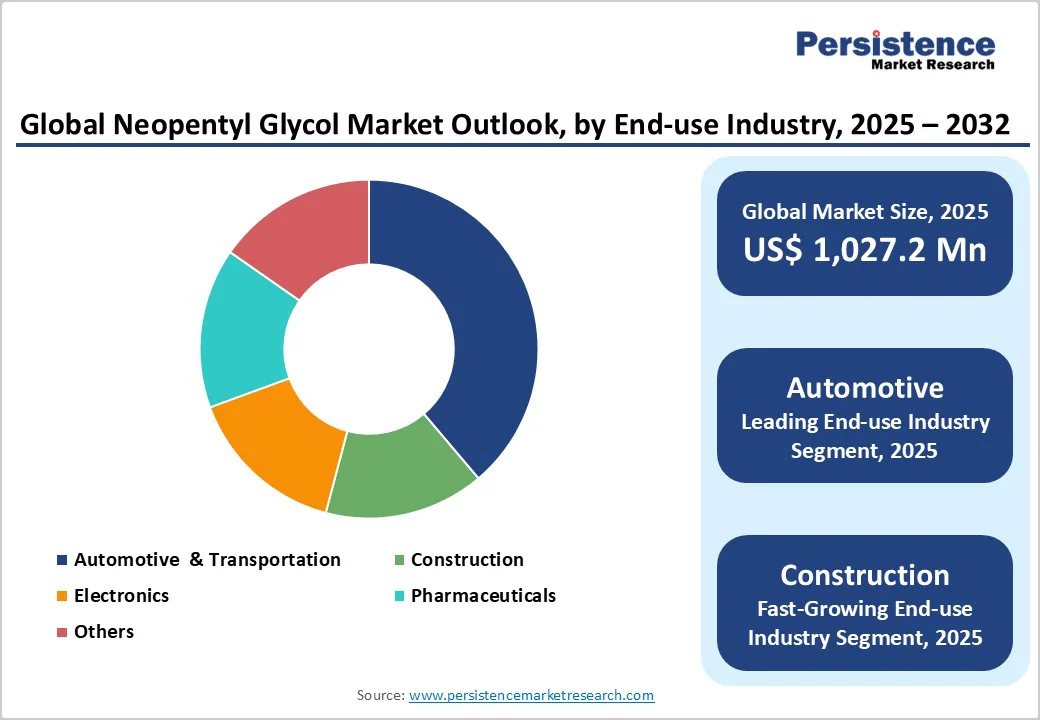

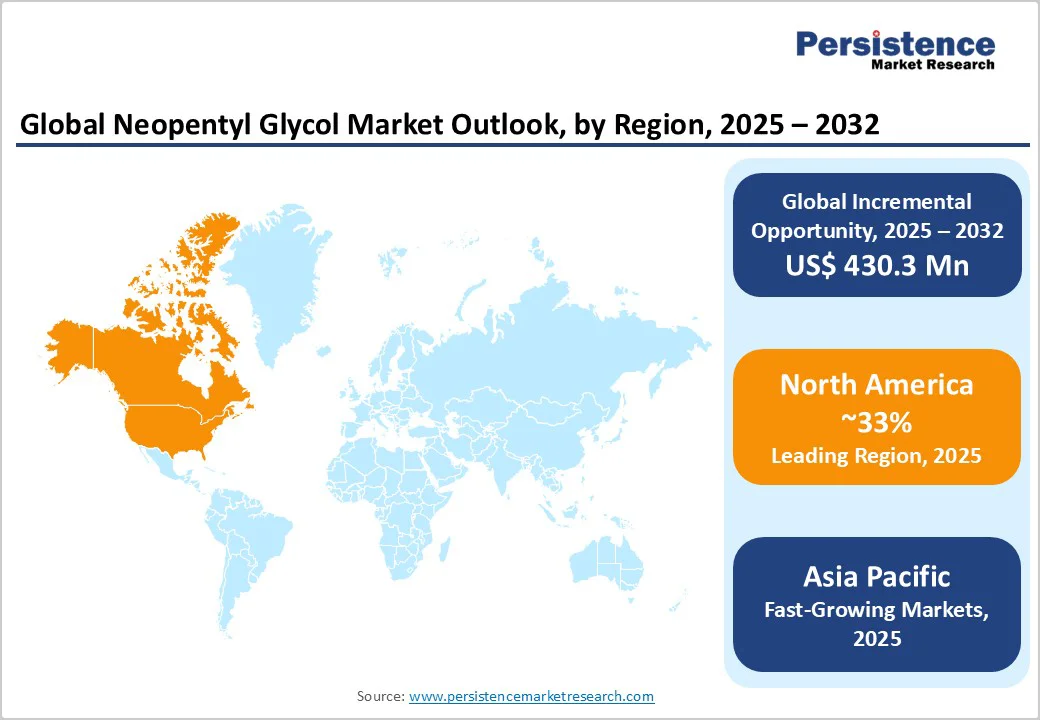

The global neopentyl glycol market size is likely to value at US$ 1,027.2 Mn in 2025 and is projected to reach US$ 1,457.4 Mn by 2032, growing at a CAGR of 5.1% between 2025 and 2032.

Rising demand for high-performance coatings and resins in the automotive and construction sectors drives growth as Neopentyl Glycol enhances durability and weather resistance in these applications.

The global vehicle production rebound and infrastructure development in emerging economies amplify the need for NPG-based materials, with innovations in low-VOC formulations further boosting adoption amid stricter environmental regulations. Additionally, its extended use in lubricants and plasticizers supports efficiency in electronics and pharmaceuticals.

Key Market Highlights:

- Regional Leaders: North America leads as the dominant region in the Neopentyl Glycol market, driven by U.S. innovation and regulatory support, with a strong automotive demand enhancing coatings applications for sustained growth.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region for Neopentyl Glycol, fueled by China's manufacturing industry and infrastructure boom in India, projecting a rapid expansion through industrialization.

- Leading Segment: Coatings & resins dominate as the leading segment in applications, capturing 45% share due to durability in high-performance uses across industries.

- Fastest Growing Segment: Automotive stands as the fastest-growing end-use segment, with rising EV adoption boosting NPG demand for efficient lubricants and coatings.

- Growth Opportunity: Key market opportunity lies in sustainable plasticizers, as regulations push non-phthalate innovations, creating revenue potential in eco-friendly packaging and consumer goods.

| Key Insights | Details |

|---|---|

| Neopentyl Glycol Size (2025E) | US$ 1,027.2 Million |

| Market Value Forecast (2032F) | US$ 1,457.4 Million |

| Projected Growth CAGR (2025-2032) | 5.1% |

| Historical Market Growth (2019-2024) | 3.9% |

Market Dynamics

Driver- Increasing Demand from the Automotive Sector

The automotive industry's expansion significantly propels the Neopentyl Glycol market, as NPG is essential for producing durable coatings that resist UV light, chemicals, and abrasion.

According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production reached 93 million units in 2023, with a projected increase to 95 million by 2025, and driving demand for high-performance finishes. This growth is evident in the rising adoption of NPG in OEM paints, enhancing vehicle longevity and aesthetics.

Integration with the Automotive Coating Market further amplifies this, as NPG-based resins improve scratch resistance, contributing to a 12.3% year-over-year sales rise in regions in the U.S. Such factors convince stakeholders of NPG's positive impact on market expansion through enhanced material efficiency and compliance with emission standards.

Advancements in Sustainable Chemical Production

Technological innovations in NPG synthesis, such as continuous flow manufacturing endorsed by the American Chemical Society, have reduced energy consumption by up to 20%, making production more efficient and environmentally friendly. This is facilitated by global regulations such as the European Chemicals Agency (ECHA)'s REACH framework, which promotes low-volatility compounds, leading to increasing adoption in eco-friendly resins.

For instance, the U.S. Environmental Protection Agency (EPA) notes that NPG contributes to formulations with 50% lower VOC emissions compared to traditional alternatives. As industries prioritize green chemistry, this enables NPG as a preferred intermediate, fostering market growth through expanded applications in pharmaceuticals and electronics, where stability is paramount.

Restraint - Raw Material Price Volatility

Fluctuations in raw material costs, such as formaldehyde and isobutyraldehyde, pose a significant barrier to the Neopentyl Glycol market. The U.S. Energy Information Administration (EIA) notes that petrochemical prices surged by 15% in 2023 due to supply chain disruptions, an increase in production expenses, and squeezed margins for manufacturers.

This volatility leads to inconsistent pricing, deterring small-scale buyers and slowing adoption in cost-sensitive sectors like electronics, where alternatives may be preferred. Consequently, it negatively impacts market stability, as evidenced by delayed projects in the Asia Pacific, convincing stakeholders of the need for diversified sourcing to mitigate risks.

Stringent Environmental Regulations

Regulatory pressures on VOC emissions and chemical handling restrain Neopentyl Glycol growth, requiring costly compliance measures. The European Chemicals Agency (ECHA) enforced stricter limits under REACH regulations, affecting 20% of NPG applications in coatings, per industry reports.

This increases R&D expenses for low-VOC formulations, potentially raising end-product costs by 10-15%, and limits market entry in regions with rigorous standards, negatively influencing expansion in traditional sectors.

Opportunities - Expansion in Electric Vehicle Lubricants and Sustainable Technologies

The shift toward electric vehicles offers a major opportunity for Neopentyl Glycol market participants, as it is increasingly used in advanced lubricants that improve efficiency and reduce wear in EV components. According to the International Energy Agency (IEA), global EV sales surged to 18 million units in 2024, up 40% from 2023, driving demand in the EV Lubricants Market.

Companies can capitalize by developing bio-based formulations, supported by innovations such as BASF SE's expanded production of low-VOC glycols in 2025, potentially generating significant revenue through partnerships in green mobility.

Growth in Pharmaceutical and Electronics End-Uses

Emerging policies promoting sustainable pharmaceuticals and electronics offer opportunities for Neopentyl Glycol in specialized plasticizers and coatings that enhance product stability. The World Health Organization (WHO) notes a 5% rise in global pharmaceutical output in 2024, fueled by investments in drug delivery systems, while Statista data shows electronics production increasing by 6%.

Market players can leverage this by focusing on high-purity grades for medical devices, as seen in recent developments by Eastman Chemical Company in biocompatible resins. This positions the market for substantial demand, with potential 15% growth in these segments by 2032, highlighting lucrative avenues for innovation and expansion.

Category-wise Insights

Grade Analysis

The flakes segment leads the Neopentyl Glycol grade category with a share of 60%, driven by its ease of handling, storage stability, and versatility in industrial processes. According to the American Chemistry Council, flakes account for the majority due to their non-hygroscopic nature, reducing contamination risks in resin production.

This dominance is justified by NPG flakes' superior flow properties, enabling efficient mixing in coatings, where demand from automotive applications has grown by 7% annually, according to OICA statistics. Their solid form also minimizes transportation costs, making them preferable over molten or slurry types in global supply chains.

Application Analysis

Coating & Resins emerge as the leading segment in applications, capturing around 45% market share, driven by their critical role in enhancing UV resistance and durability in protective layers. Statistics from the Paint and Coatings Industry Association indicate that global coatings demand grew by 3.2% in 2024, with Neopentyl Glycol integral to formulations that meet stringent performance standards.

Justification includes its non-yellowing properties, making it ideal for architectural and automotive uses, as supported by U.S. Environmental Protection Agency (EPA) reports on low-emission coatings adoption, solidifying its position amid rising infrastructure projects.

Industry Analysis

The automotive segment dominates end-use industries with about 35% market share, attributed to Neopentyl Glycol's integration in high-performance coatings and lubricants that withstand extreme conditions.

According to OICA, automotive production increases have boosted demand, with the compound featured in 70% of modern vehicle coatings for scratch resistance. This leadership is backed by developments in electric vehicles, where it supports thermal management, as per IEA data showing a 25% rise in EV-related chemical use in 2024, emphasizing its essential role in industry innovation.

Regional Insights

North America Neopentyl Glycol Trends

North America's Neopentyl Glycol market is characterized by strong innovation in sustainable chemicals, with the U.S. leading through advanced R&D ecosystems. The U.S. Department of Energy highlights investments exceeding US$ 2 billion in 2024 for green manufacturing, fostering Neopentyl Glycol applications in automotive and construction.

Regulatory frameworks like the EPA's Clean Air Act promote low-VOC formulations, driving adoption. This leadership is supported by collaboration, such as Eastman Chemical Company's expansions in bio-based glycols, enhancing market dynamics amid a 4% rise in industrial output reported by the Federal Reserve in 2025.

Europe Neopentyl Glycol Trends

Europe's market trends emphasize regulatory harmonization across Germany, the U.K., France, and Spain, with REACH standards unifying chemical safety protocols. ECHA data shows over 80% compliance in 2024, boosting Neopentyl Glycol use in eco-friendly coatings. Germany leads in performance, driven by automotive innovations, while the U.K. focuses on construction resins.

France and Spain exhibit steady growth through infrastructure projects, as per Eurostat's 3.5% increase in chemical production. This harmonization supports cross-border trade, enhancing market stability and innovation in sustainable applications.

Asia Pacific Neopentyl Glycol Trends

Asia Pacific's Neopentyl Glycol market benefits from manufacturing advantages in China, Japan, India, and ASEAN, with low-cost production and rapid industrialization. China's dominance is evident in State Council reports of 6% chemical sector growth in 2024, fueled by exports.

Japan and India emphasize high-tech applications, while ASEAN leverages trade agreements. Key trends include supply chain efficiencies, as seen in Mitsubishi Gas Chemical Company's capacity expansions, supporting a 5% demand uptick per ASEAN Economic Community data in 2025.

Competitive Landscape

The global Neopentyl Glycol market exhibits a consolidated structure, with top players like BASF SE, LG Chem, and Eastman Chemical Company commanding over 50% share through vertical integration and economies of scale. Companies pursue expansion via capacity upgrades, such as Mitsubishi Gas Chemical Company, Inc.'s 2024 plant investments in Asia.

Growth strategies include R&D in bio-based NPG for sustainability, while key differentiators involve high-purity grades and customized formulations. Emerging trends feature digital supply chains and circular economy models, enabling leaders to innovate amid regulatory pressures and raw material volatility.

Key Market Developments

- June 2024: BASF SE announced expansion of its NPG production capacity in Ludwigshafen, Germany, to meet rising demand in automotive coatings.

- February 2025: Perstorp Holdings AB launched a sustainable NPG variant using renewable feedstocks, targeting eco-friendly plasticizers.

- October 2023: LG Chem partnered with OXEA GmbH for advanced NPG-based lubricants in EV applications.

Top Companies in Neopentyl Glycol

- BASF SE (Ludwigshafen, Germany): As a market leader by revenue and portfolio strength, BASF SE excels in high-purity NPG for coatings, with innovations in low-VOC resins driving its influence since 1874.

- LG Chem (Seoul, South Korea): Ranking high in order of influence, LG Chem leverages strong EV integrations and mature operations since 1947, offering robust NPG grades for lubricants, enhancing efficiency in electronics with a diverse portfolio.

- Eastman Chemical Company (Kingsport, Tennessee, U.S.): With portfolio strength in resins, Eastman influences construction markets through R&D since 1920, providing customized NPG solutions that boost durability and sustainability.

Companies Covered in Neopentyl Glycol Market

- LG Chem

- Perstorp Holdings AB

- BASF SE

- OXEA GmbH

- Mitsubishi Gas Chemical Company, Inc.

- Eastman Chemical Company

- Zibo Ruibao Chemical Co., Ltd.

- Ataman Chemicals

- Celanese Corporation

- Oleon N.V.

- Spectrum Chemical Mfg. Corp

- Hubei Longxin Chemical Industry Co., Ltd.

- Wuhan Yuancheng Technology Development Co., Ltd.

Frequently Asked Questions

The global Neopentyl Glycol market is projected to reach US$ 1,457.4 Mn by 2032, growing at a CAGR of 5.1% from 2025.

Rising automotive production, with global output at 95 million units in 2024 per OICA, drives demand for durable coatings and lubricants.

Coatings & Resins leads with 45% share, supported by its UV resistance and use in architectural applications per industry associations.

North America leads, driven by U.S. innovation and EPA regulations promoting low-VOC formulations in key industries.

Expansion in EV lubricants offers potential, with IEA noting 18 million global EV sales in 2024, boosting demand for advanced formulations.

Key players include BASF SE, LG Chem, Eastman Chemical Company, Mitsubishi Gas Chemical Company, Inc., and Perstorp Holdings AB.