- Pharmaceuticals

- Neoadjuvant Therapies Market

Neoadjuvant Therapies Market Size, Share, and Growth Forecast, 2026 - 2033

Neoadjuvant Therapies Market by Therapy, Cancer Indication, Route of Administration, End-user, and Regional Analysis for 2026 – 2033

Neoadjuvant Therapies Market Size and Trends Analysis

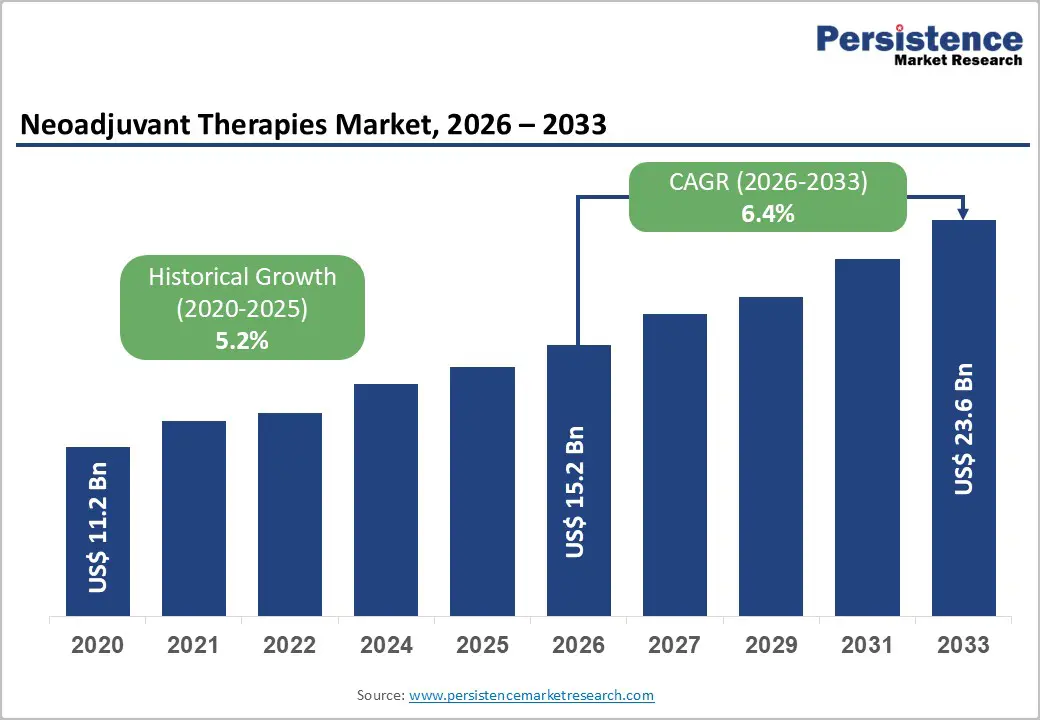

The global neoadjuvant therapies market size is likely to be valued at US$15.2 billion in 2026, and is expected to reach US$23.6 billion by 2033, growing at a CAGR of 6.4% during the forecast period from 2026 to 2033, driven by the increasing prevalence of targeted cancer treatments, rising demand for tumor reduction before surgery, and advancements in combinational therapy drugs.

Growing demand for effective, personalized neoadjuvant therapies, especially in breast cancer and lung cancer (NSCLC & SCLC), is accelerating adoption across cancer indications. Advances in intravenous and oral routes are further boosting uptake by offering more patient-friendly, efficient options. Increasing recognition of neoadjuvant therapies as critical for improving surgical outcomes in emerging oncology markets remains a major driver of market growth.

Key Industry Highlights:

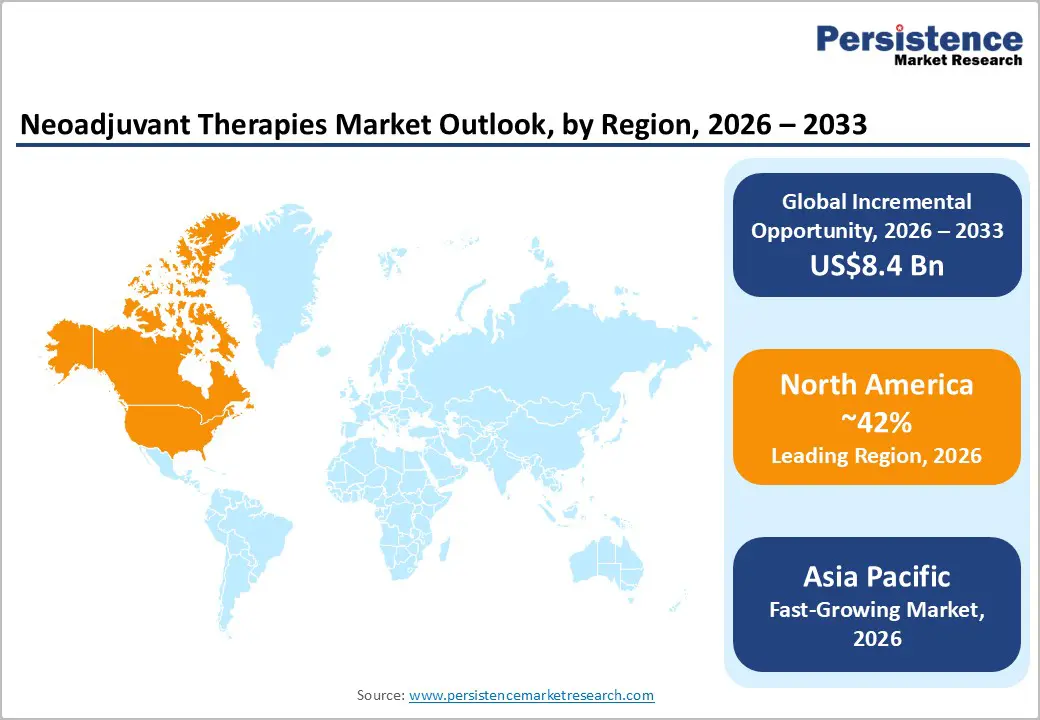

- Leading Region: North America, anticipated to account for a 42% market share in 2026, driven by advanced oncology research, high cancer incidence, and strong innovation in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rising cancer burden, expanding healthcare access, and growing investments in targeted therapies in China and India.

- Dominant Therapy Type: Combinational therapy drugs, which hold approximately 45% of the market share, as they provide synergistic effects to improve tumor response.

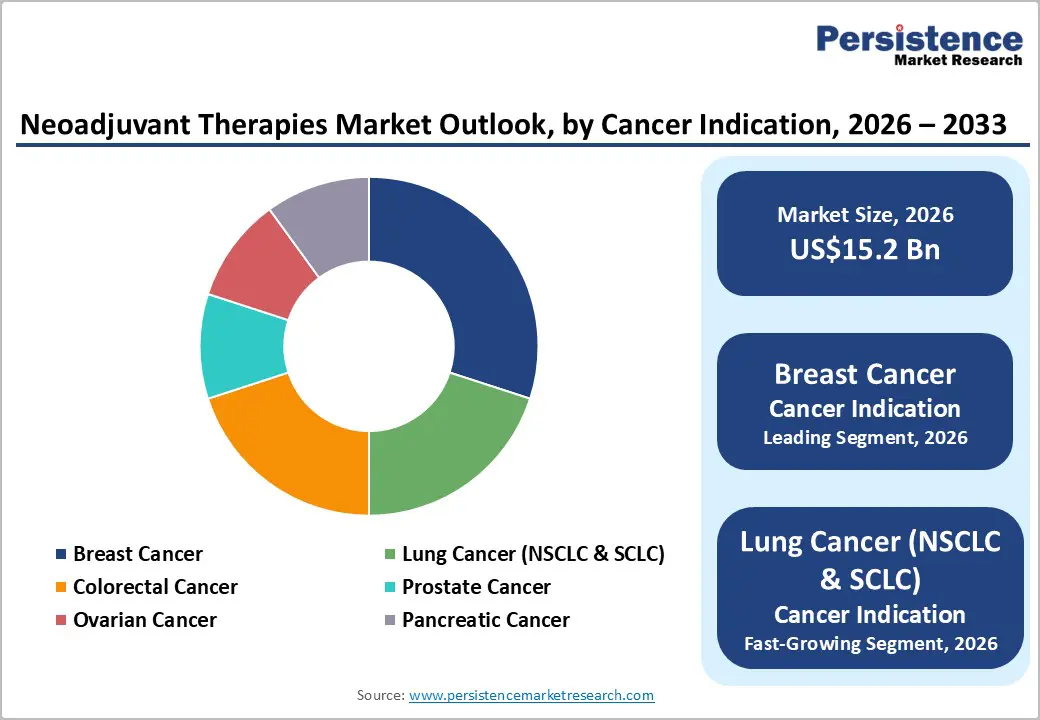

- Leading Cancer Indication: The breast cancer segment is expected to lead the market, holding approximately 30% of the share in 2026.

- Leading Route of Administration: Intravenous, to contribute nearly 50% of the market revenue, due to direct delivery and efficacy in chemotherapy.

- Leading End-user: Hospitals, contributing nearly 50% of market revenue due to specialized oncology units and surgical integration.

| Report Attribute | Details |

|---|---|

|

Neoadjuvant Therapies Market Size (2026E) |

US$15.2 Bn |

|

Market Value Forecast (2033F) |

US$23.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Targeted Cancer Treatments

The rising prevalence of targeted cancer treatments reflects a major shift in oncology toward precision-based care that focuses on the specific molecular and genetic characteristics of tumors. Unlike conventional chemotherapy, which affects both cancerous and healthy cells, targeted therapies are designed to interfere with defined pathways responsible for tumor growth, progression, and survival. Advances in genomic profiling and biomarker testing have enabled clinicians to identify actionable mutations, allowing therapies to be matched more accurately to individual patients.

Growing clinical evidence has demonstrated that targeted treatments can deliver improved response rates, longer progression-free survival, and reduced systemic toxicity compared to traditional approaches. This has increased physician confidence and expanded their use across a wide range of cancers, including breast, lung, colorectal, and hematological malignancies. Continuous investments in research and development have accelerated the discovery of novel targets and the approval of next-generation drugs, further strengthening adoption.

High Development and Clinical Trial Costs

High development and clinical trial costs present a significant barrier for companies advancing next-generation neoadjuvant therapies and novel combinations. Developing innovative grades such as targeted NACT, personalized NAHT, or multi-drug combinations requires extensive research, biomarker testing, and advanced delivery technologies that are far more expensive than standard treatments. Efficacy is an even greater challenge: many refined variants, response-enhanced formulations, and stability-improved products are sensitive to resistance, toxicity, and heterogeneity, requiring rigorous optimization to ensure they remain effective throughout regimens. Achieving long-term performance often involves costly phase II/III trials, sophisticated imaging, and the use of high-grade APIs, which significantly increase R&D expenditures.

Meeting stringent regulatory expectations for pCR rates, safety data, and clinical consistency requires multiple validation studies under various conditions and across several patient cohorts. This adds both time and financial burden to development timelines. Scaling up manufacturing requires controlled facilities, specialized logistics, and quality-assurance systems, further driving up overall costs. For smaller biotechs, these challenges can limit pipeline expansion or delay commercialization.

Advancements in Combinational and Personalized Delivery Platforms

Advancements in combinational and personalized neoadjuvant therapies delivery platforms are transforming the global oncology landscape by addressing two major challenges, resistance barriers and patient variability. Combinational platforms are engineered to achieve synergistic effects, reducing reliance on single agents and enabling better tumor shrinkage in neoadjuvant settings. Innovations, such as immuno-chemo hybrids, targeted NAHT, biomarker-guided NACT, and multi-drug regimens, significantly improve response rates and reduce recurrence, lowering treatment costs for providers and patient campaigns.

Progress in personalized platforms, including genomic profiling, adaptive dosing, oral/intravenous combos, and AI-predicted therapies, supports more tailored care by stimulating individual response, the therapy’s first line of defense against suboptimal outcomes. These formats eliminate one-size-fits-all, enhance tolerability, and allow versatile use without over-treatment, making them highly suitable for mass cancer programs. New technologies such as nano-delivery, bio-adhesive vectors, and VLP-based carriers further enhance precision and response.

Category-wise Analysis

Therapy Type Insights

Combinational therapy drugs are expected to dominate the market, accounting for approximately 45% of the revenue share in 2026. Its dominance is driven by synergistic efficacy, large multimodal programs, and strong global demand for improved responses. Combinational therapy drugs provide enhanced reduction, ensure survival, and contribute to outcomes, making them suitable for large-scale oncology campaigns. In oncology, 65% of late-stage clinical trials now involve combination therapies targeting immune checkpoints such as PD-1/PD-L1 alongside chemotherapies or targeted agents. This approach has improved response rates in cancers such as non-small cell lung cancer (NSCLC), where adding pembrolizumab to chemotherapy increased median survival to 22 months compared to 10.7 months with chemotherapy alone.

Neoadjuvant chemotherapy drugs (NACT) are likely to be the fastest-growing segment, due to their established role and expanding use in solid tumors. Their cytotoxic profile makes them ideal for targeted debulking, reducing surgery risks. Continuous innovations in regimens are further strengthening their appeal, driving rapid adoption across North America and Europe, where demand for pre-surgical options is accelerating. The European Commission (EC) has approved nivolumab (Opdivo) in combination with platinum-based chemotherapy for the neoadjuvant treatment of patients with resectable non–small cell lung cancer (NSCLC) at high risk of recurrence with tumor cell PD-L1 expression of at least 1%.

Cancer Indication Insights

The breast cancer segment is expected to lead the market, holding approximately 30% of the share in 2026, driven by high incidence, large HER2 programs, and strong global demand for pre-surgical reduction. Their dominance continues as guidelines expand neoadjuvant use. Rising adoption of lung cancer therapies and expanded colorectal campaigns highlight the growing focus on multi-indication benefits. Roche’s Kadcyla® (trastuzumab emtansine) has become a cornerstone in early-stage HER2-positive breast cancer management globally. After neoadjuvant therapy (pre-surgery), Kadcyla is used as an adjuvant treatment for patients with residual invasive disease, significantly reducing the risk of recurrence or death compared with continued standard HER2-targeted therapy alone.

The lung cancer (NSCLC & SCLC) segment is likely to be the fastest-growing segment, due to strong momentum in targeted therapies and expanding inclusion in neoadjuvant protocols. The growing shift toward immuno-combinations, along with better resectability, accelerates the adoption. Advancements in PD-L1 inhibitors and continued progress of chemo-immuno blends entering trials drive market growth. Merck & Co.’s Keytruda® (pembrolizumab) continues to expand its role in lung cancer care, being approved for multiple NSCLC indications, including neoadjuvant and adjuvant settings, and adopted widely in the first-line treatment regimens. Keytruda’s broad use across lung cancer subtypes has helped drive strong clinical uptake worldwide, supporting the rising demand for advanced immunotherapy in lung oncology.

Route of Administration Insights

The intravenous segment is projected to dominate the market, contributing nearly 50% of revenue in 2026, due to remaining the primary route for direct delivery, large infusion programs, and management of systemic therapies requiring precise dosing. Their strong integration, trained oncologists, and ability to handle high-volume or combinational blends drive higher consumption. Intravenous routes are leading NACT rollouts as well as administering emerging NAHT trials. Intravenous (IV) administration dominating oncology treatment is Cetuximab, developed by ImClone Systems, which is widely used in the treatment of metastatic colorectal cancer and head and neck cancer. Cetuximab is administered as an intravenous infusion, allowing the monoclonal antibody to directly enter the bloodstream to target the epidermal growth factor receptor (EGFR) on cancer cells, which is critical for systemic efficacy in these solid tumors.

Oral represents the fastest-growing segment, driven by its strong convenience presence and expanding role in hormonal therapies. They offer convenient, quick, and accessible dosing, attracting patients who prefer home, low-invasion settings. Increased outreach programs, adherence focus, and wider availability of routine and premium orals further accelerate uptake, boosting rapid adoption across both urban and semi-urban areas. IBRANCE is the first and only FDA-approved oral inhibitor of CDKs 4 and 6,2, which are key regulators of the cell cycle that trigger cellular progression.3,4 IBRANCE is approved in more than 50 countries.

End-user Insights

Hospitals are estimated to dominate the market, with approximately 50% share in 2026, due to the high volume of oncology care and strong global emphasis on specialized treatments. Regular protocol schedules, patient requirements, and widespread access to infusion centers drive consistent demand. Rising focus on clinics and research institutes further strengthens hospital leadership. Apollo Hospitals Enterprise Ltd. is one of the leading hospital networks globally and a major player in oncology care, treating over 125,000 cancer patients per year through its integrated cancer treatment facilities, including infusion centers, surgical oncology units, and advanced diagnostics. Apollo’s comprehensive cancer program spans chemotherapy, radiation therapy, immunotherapy, and surgical care, reflecting how hospitals serve as primary hubs for high-volume oncology treatment delivery and complex therapeutic regimens.

Biotech and pharma companies are likely to be the fastest-growing field, driven by the rising need for clinical trials, vulnerability to innovation, and expanding adoption of R&D. Advancements in product development, tailored formulations, and expanding collaborations in novel drug development are supporting rapid market uptake. Growing adoption across academic institutions, clinics, and other high-technology sectors is further fueling growth. The collaboration between BioNTech and Bristol Myers Squibb (BMS) focused on advancing cancer therapies. In this partnership, BioNTech, originally known for mRNA vaccines, teamed up with Bristol Myers Squibb to co-develop and commercialize BNT327, a next-generation antibody for treating multiple cancer types, including lung and breast cancer.

Regional Insights

North America Neoadjuvant Therapies Market Trends

North America is expected to dominate, accounting for nearly 42% of the global neoadjuvant therapies market in 2026, driven by the region’s advanced oncology infrastructure, strong research and development capabilities, and high public awareness of personalized benefits. Treatment systems in the U.S. and Canada provide extensive support for therapy programs, ensuring wide accessibility of neoadjuvant therapies across breast cancer, lung cancer (NSCLC & SCLC), and colorectal populations. Increasing demand for combinational, convenient, and easy-to-administer forms is further accelerating adoption, as these formats improve response and reduce barriers associated with single-agent formats.

Innovation in neoadjuvant therapies technology, including stable combinational, improved oral delivery, and targeted indication enhancement, is attracting significant investments from both public and private sectors. Government initiatives and FDA campaigns continue to promote use against tumor resistance, surgical risks, and emerging precision threats, creating sustained market demand. The growing focus on ovarian grades and specialty uses, particularly for pancreatic and others, is expanding the target applications for neoadjuvant therapies.

Europe Neoadjuvant Therapies Market Trends

Europe is experiencing strong market growth driven by increasing awareness of pre-surgical benefits, well-established healthcare systems, and government-led cancer programs. Countries such as Germany, France, and the U.K. have well-established oncology frameworks that support routine neoadjuvant use and encourage adoption of innovative therapy delivery methods, including neoadjuvant therapies. These effective formulations are particularly appealing for breast populations, regulation-conscious operators, and lung users, improving resectability and coverage rates.

Technological advancements in neoadjuvant therapies development, such as enhanced combinational, application-targeted delivery, and improved NAHT grades, are further boosting market potential. European authorities are increasingly supporting research and trials for therapies against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, oral options is aligned with the region’s focus on preventive surgery and reducing recurrence. Public awareness campaigns and promotion drives are expanding reach in both urban and rural areas, while suppliers are investing in R&D and novel variants to increase efficacy.

Asia Pacific Neoadjuvant Therapies Market Trends

Asia Pacific is likely to be the fastest-growing market for neoadjuvant therapies during the forecast period, driven by rising cancer incidence, increasing government initiatives, and expanding application programs across the region. Countries such as India, China, Japan, and Southeast Asian nations are actively promoting therapy campaigns to address oncology growth and emerging surgical needs. Neoadjuvant therapies are particularly attractive in these regions due to their cost-effective administration, ease of scaling, and suitability for large-scale treatment drives in both urban and rural populations.

Technological advancements are supporting the development of stable, effective, and easy-to-administer neoadjuvant therapies, which can withstand challenging access conditions and minimize toxicity dependence. These innovations are critical for reaching remote facilities and improving overall response coverage. Growing demand for breast cancer, lung cancer (NSCLC & SCLC), and colorectal applications is contributing to market expansion. Public-private partnerships, increased oncology expenditure, and rising investments in clinical research and manufacturing capacity are further accelerating growth. The convenience of neoadjuvant delivery, combined with improved reduction and reduced risk of complications, positions neoadjuvant therapies as a preferred choice.

Competitive Landscape

The global neoadjuvant therapies market features competition between established pharma giants and emerging biotech innovators. In North America and Europe, Novartis AG and Bayer AG lead through strong R&D, distribution networks, and clinical ties, bolstered by innovative grades and combination programs. In Asia Pacific, Eli Lilly and Company advances with localized solutions, enhancing accessibility. Combinational delivery boosts response, cuts resistance risks, and enables mass integrations across regions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand pipelines, and speed commercialization. Personalized formulations solve variability issues, aiding penetration in precision areas.

Key Industry Developments

- In December 2025, Innovent’s TABOSUN® in combination with TYVYT® was approved in China as the world’s first dual-immune-oncology neoadjuvant therapy for patients with MSI-H/dMMR colon cancer, marking a significant advancement in pre-surgical treatment options for this patient population.

- In June 2025, BioNTech SE and Bristol Myers Squibb announced that an agreement had been entered into for the global co-development and co-commercialization of BioNTech’s investigational bispecific antibody BNT327 across numerous solid tumor types. Under the agreement, the development of this clinical candidate was jointly pursued by BioNTech and BMS to broaden and accelerate its advancement.

Companies Covered in Neoadjuvant Therapies Market

- Novartis AG

- Bayer AG

- Genentech, Inc.

- AbbVie Inc.

- EMD Serono, Inc.

- Eli Lilly and Company

- Bristol-Myers Squibb Company

- Taiho Pharmaceutical Co., Ltd.

- Agios Pharmaceuticals, Inc.

- Janssen Pharmaceutical Companies

- Merck & Co.

Frequently Asked Questions

The global neoadjuvant therapies market is projected to reach US$15.2 billion in 2026.

Drivers include increasing cancer incidence, technological advancements in targeted drugs, and higher R&D spending. Aging populations and personalized medicine adoption further accelerate growth.

The neoadjuvant therapies market is poised to witness a CAGR of 6.4% from 2026 to 2033.

Opportunities encompass AI integration for treatment optimization, biosimilar development to reduce costs, and expansion in high-growth regions such as Asia Pacific.

Novartis AG, Bayer AG, Genentech, Inc., AbbVie Inc., and Eli Lilly and Company are the key players.