- Marine

- Naval Vessels MRO Market

Naval Vessels MRO Market Size, Share, and Growth Forecast, 2026 – 2033

Naval Vessels MRO Market by Product Type (Engine MRO, Dry Dock MRO, Others), Vessel Type (Frigates, Destroyers, Corvettes, Auxiliary Vessels), and Regional Analysis for 2026 – 2033

Naval Vessels MRO Market Size and Trends Analysis

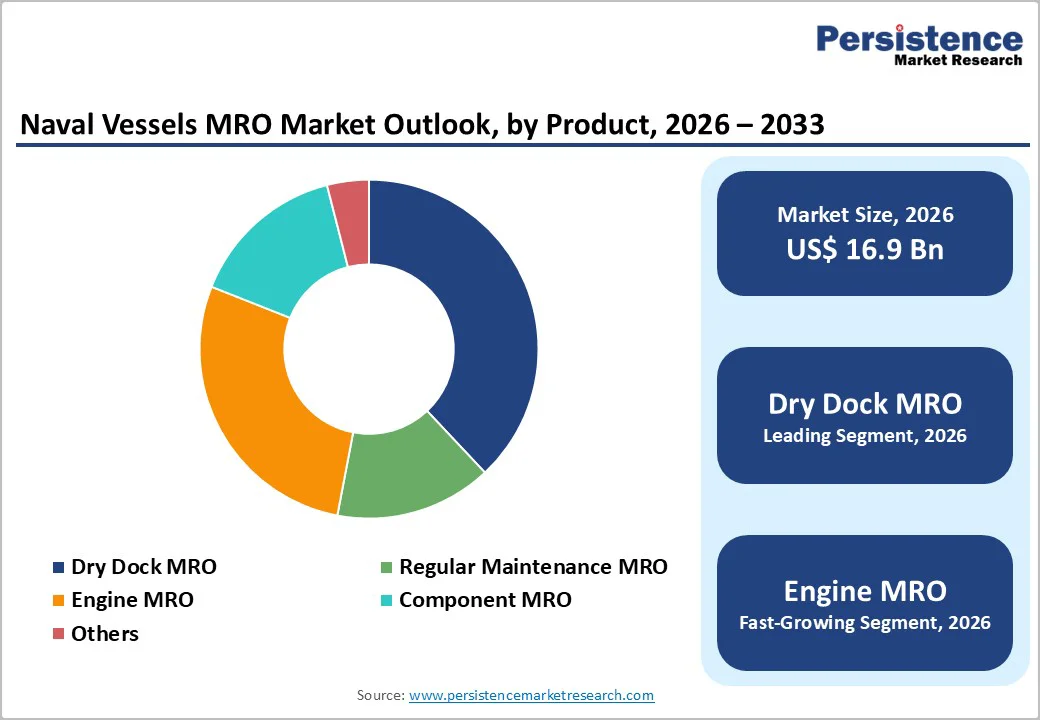

The global naval vessels MRO market size is likely to be valued at US$16.9 billion in 2026 and is expected to reach US$24.8 billion by 2033, growing at a CAGR of 5.6% during the forecast period from 2026 to 2033, driven by rising defense budgets amid escalating maritime security concerns, coupled with the increasing need to maintain and extend the operational life of aging naval fleets. As navies prioritize fleet availability and mission readiness, demand for scheduled maintenance, dry-dock services, and system overhauls continues to rise. The adoption of advanced MRO (Maintenance, Repair, and Overhaul) technologies, including predictive maintenance, digital twins, condition-based monitoring, and automation, is improving maintenance efficiency and reducing downtime.

Key Industry Highlights:

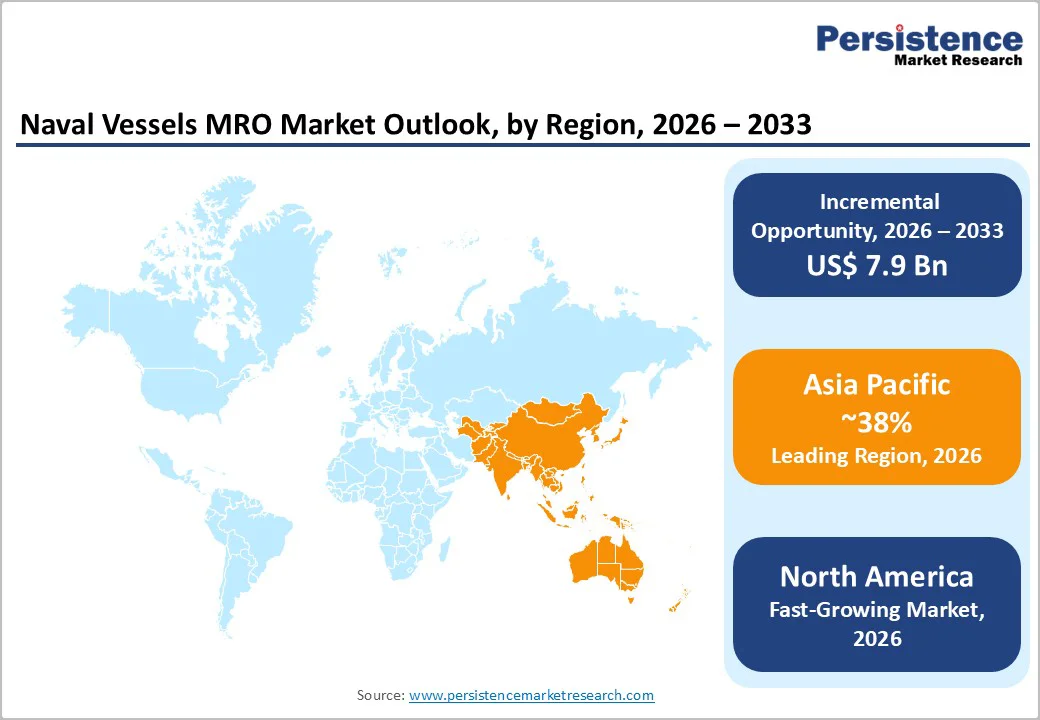

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by rapid fleet expansion, strong domestic shipbuilding capabilities, rising maritime security concerns, and increasing investments in naval MRO infrastructure.

- Fastest-growing Region: North America is likely to be the fastest-growing region in the naval vessels MRO in 2026, driven by increased U.S. defense spending, fleet modernization and life-extension programs, and rising submarine and advanced maintenance requirements.

- Leading Product Type: Dry dock MROs are projected to represent the leading product type in 2026, accounting for 39% of the revenue share, driven by mandatory inspections and major overhaul requirements.

- Leading Vessel Type: Destroyers and frigates are anticipated to be the leading vessel type, accounting for over 50% of the revenue share in 2026, supported by their extensive deployment across global naval fleets.

| Key Insights | Details |

|---|---|

| Naval Vessels MRO Market Size (2026E) | US$16.9 Bn |

| Market Value Forecast (2033F) | US$24.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Service Life Extension and Platform Modernization to Drive the Frequency and Complexity of Naval MROs

Many naval forces are keeping ships in service well beyond their original design lives due to budget limitations, lengthy timelines for new vessel construction, and changing security priorities. To ensure continued readiness, frigates, destroyers, submarines, and auxiliary vessels undergo regular overhauls, structural maintenance, and system refurbishments. These efforts sustain consistent demand for dry dock operations, engine maintenance and repair, and component-level servicing, providing a reliable revenue stream for naval MRO providers.

Life-extension initiatives are increasingly paired with modernization measures, including propulsion system upgrades, combat system improvements, sensor replacements, and the integration of digital maintenance technologies. Instead of pursuing full fleet replacement, navies are implementing phased upgrade programs to enhance the performance, efficiency, and survivability of aging platforms. This strategy raises both the frequency and technical sophistication of maintenance activities, favoring service providers with specialized expertise. As a result, life-extension programs not only prolong vessel service life but also reinforce long-term demand for comprehensive, high-value naval MRO services across key maritime regions.

Skilled Labor Shortages

Maintenance and overhaul operations in the naval sector require a highly specialized workforce. Naval MRO activities rely on skilled engineers, welders, naval architects, electronics experts, and technicians capable of servicing complex propulsion systems, combat electronics, and mission-critical platforms. The availability of such talent is increasingly constrained by an aging workforce, limited training pipelines, and strong competition from commercial shipbuilding, offshore energy, and other industrial sectors. These shortages often result in extended maintenance timelines, schedule slippages, and higher operating costs for both naval operators and MRO service providers.

The growing technological complexity of modern naval vessels is also intensifying skills requirements. Advanced digital architectures, integrated combat systems, and hybrid or next-generation propulsion technologies require continuous upskilling, certification, and specialized training. In many regions, stringent security clearance processes and regulatory restrictions further limit workforce mobility, making rapid staffing and redeployment challenging. As a result, even well-funded MRO programs may experience execution delays due to manpower constraints. Without targeted workforce development initiatives, expanded training programs, and greater adoption of automation and digital support tools, skilled labor shortages will continue to limit the efficiency and growth of naval vessel MRO activities.

Adoption of Performance-Based Logistics (PBL) Contracts

Navies are increasingly transitioning from traditional, task-based maintenance approaches to outcome-focused sustainment models. Under performance-based logistics (PBL) arrangements, MRO providers are compensated according to predefined performance indicators, such as vessel availability, reliability, and turnaround times, instead of being paid per individual repair or service. This model aligns the objectives of defense forces and service providers, promoting operational efficiency, cost management, and long-term optimization of naval assets throughout their lifecycle.

PBL contracts also foster closer collaborations between navies and MRO providers, encouraging investments in predictive maintenance, digital monitoring systems, and integrated logistics support. Providers are motivated to implement advanced analytics, condition-based maintenance, and efficient spare-parts management to achieve performance targets. For navies, PBL arrangements help reduce total lifecycle costs and enhance fleet readiness. MRO companies provide stable, multi-year revenue streams and strengthen long-term client relationships. As naval fleets grow more complex and operational requirements intensify, the adoption of PBL contracts is expected to transform sustainment strategies and drive sustained growth in the naval MRO market.

Category-wise Analysis

Product Type Insights

The dry dock MRO segment is expected to lead the naval vessels MRO market, accounting for approximately 39% of total revenue in 2026, driven by mandatory regulatory requirements and the critical nature of hull and structural integrity. Naval vessels are required to undergo periodic dry-docking for inspections, corrosion control, hull repairs, and major structural refurbishments to maintain seaworthiness and combat readiness. These activities demand specialized infrastructure, certified facilities, and skilled labor, making dry dock services both capital-intensive and indispensable. As naval fleets age, the frequency and scope of dry dock overhauls increase, further strengthening this segment’s dominance. For example, the U.S. Navy’s scheduled dry-dock maintenance of Arleigh Burke–class destroyers involves extensive hull inspections, propulsion alignment, and system upgrades.

Engine MRO is likely to represent the fastest-growing segment in 2026, driven by rising complexity in naval propulsion systems and increasing focus on fuel efficiency and operational reliability. Modern naval vessels are adopting advanced propulsion technologies, including hybrid, integrated electric propulsion, and energy-efficient engines, which require specialized maintenance and frequent performance optimization. Engine MRO demand is also driven by the transition toward condition-based and predictive maintenance models, enabling early fault detection and reduced unplanned downtime. An example is the engine upgrade and sustainment programs for modern frigates and destroyers in European and Asia Pacific navies, where propulsion efficiency and endurance are critical mission parameters.

Vessel Type Insights

Destroyers are projected to lead, capturing around 50% of the total revenue share in 2026, driven by their widespread deployment and multi-role operational profiles. These vessels serve as the backbone of modern naval fleets, performing air defense, anti-submarine warfare, surface combat, and escort missions. Their high operational tempo necessitates frequent maintenance, system upgrades, and lifecycle overhauls. For example, sustainment of Aegis-equipped destroyers requires continuous MRO support for radar systems, combat management software, propulsion, and structural components. Frigates similarly demand regular maintenance as they are heavily utilized in patrol and littoral operations.

Frigates are likely to be the fastest-growing vessel type in 2026, driven by increased procurement and deployment by emerging and mid-sized navies seeking cost-effective, multi-role platforms. Modern frigates feature modular designs, shorter build cycles, and advanced combat systems, which quickly transition into sustainment and MRO phases. For example, the induction of next-generation frigates by Asia Pacific and the Middle Eastern navies, where sustained operational readiness is achieved through structured MRO programs. These vessels are widely used for maritime security, anti-piracy operations, and regional patrols, resulting in high utilization rates. As frigates enter service in larger numbers, the demand for engine maintenance, component upgrades, and periodic overhauls rises accordingly.

Regional Insights

North America Naval Vessels MRO Market Trends

North America is likely to be the fastest-growing region in 2026, driven by sustained defense spending, an aging naval fleet, and a strong emphasis on fleet readiness and modernization. The U.S. dominates the regional market, driven by the world’s largest naval fleet and continuous maintenance requirements for destroyers, aircraft carriers, submarines, and auxiliary vessels. Life-extension programs for legacy platforms, combined with strict regulatory oversight under U.S. Navy maintenance frameworks, are sustaining demand for dry dock services, engine overhauls, and component-level MRO. The adoption of advanced maintenance technologies such as predictive analytics, digital twins, and condition-based monitoring is improving maintenance efficiency while reducing unplanned downtime across naval assets.

In North America, naval MRO activities are increasingly consolidated among major defense contractors and shipyards, supported by long-term sustainment agreements. For instance, Huntington Ingalls Industries plays a pivotal role in maintaining U.S. Navy aircraft carriers and surface combatants through extensive depot-level maintenance and modernization initiatives. The region is also seeing growing investment in infrastructure enhancements and submarine sustainment, particularly for next-generation platforms and allied programs. Overall, North America’s naval MRO market is evolving toward technology-enabled, performance-driven sustainment models that enhance operational readiness and ensure long-term fleet availability.

Europe Naval vessels MRO Market Trends

Europe is likely to be a significant market for naval vessels MRO in 2026, due to increased defense spending by NATO member states and collaborative maintenance initiatives aimed at enhancing fleet readiness amid evolving security challenges in the region. European navies operate diverse fleets of surface combatants, submarines, and auxiliary vessels, which drives continuous demand for comprehensive maintenance, overhaul, and modernization services. Countries such as the U.K., France, Germany, and Italy are at the forefront of regional MRO activity, supported by established shipyard infrastructure and long-term sustainment contracts. There is also a strong emphasis on digitalization and sustainability, with the adoption of predictive analytics, modular upgrades, and eco-friendly practices gaining traction among MRO providers.

Europe is witnessing a notable trend toward increasing cross-border cooperation and the adoption of performance-based maintenance frameworks, enabling cost efficiencies and the shared use of specialized facilities for complex naval vessel overhauls. European navies are extending the service life of legacy vessels through phased modernization programs and integrating advanced maintenance technologies such as digital twin systems to reduce unplanned downtime. Regulatory compliance and environmental mandates are influencing MRO practices, propelling investments in green maintenance solutions. These trends collectively position Europe as a significant and increasingly sophisticated market for naval vessels MRO.

Asia Pacific Naval Vessels MRO Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by rapid growth and strategic importance due to rising defense expenditures, expanding naval fleets, and strengthening maritime security imperatives. Countries such as China, India, and Australia are modernizing and expanding their surface combatants, submarines, and support vessels, driving sustained demand for MRO services. This trend is supported by proactive government policies focused on indigenous defense manufacturing, public-private partnerships, and the expansion of local shipyard infrastructure, which enhance regional MRO capacity and efficiency. The increasing adoption of predictive maintenance, digital diagnostics, and automation technologies is improving service turnaround times and fleet readiness.

Increased international collaboration and capacity building, where local shipyards secure strategic MRO contracts that extend beyond national navies. For example, partnerships and agreements such as Master Ship Repair Agreements with foreign navies are elevating the technical capabilities of regional yards and fostering deeper defense cooperation. Such collaborations not only support operational readiness across allied fleets but also position Asia Pacific as a competitive MRO hub capable of handling complex overhaul work previously concentrated in Western shipyards. These developments underscore the region’s evolving role as a pivotal contributor to naval sustainment ecosystems.

Competitive Landscape

The global naval vessels MRO market exhibits a moderately fragmented structure, driven by the presence of a mix of established defense giants and specialized regional players competing for government contracts and technological leadership. Companies are adopting strategic initiatives such as facility expansions, digital technology integration, joint ventures, and service diversification to strengthen their competitive position. For example, Huntington Ingalls Industries has expanded dry-dock capacity to handle more vessels annually, while Lockheed Martin is advancing AI-driven diagnostics to improve maintenance outcomes and reduce unplanned downtime.

With key leaders including BAE Systems, General Dynamics, Huntington Ingalls Industries, Lockheed Martin, Northrop Grumman, Raytheon, URS Corporation, and Saab AB, the competitive landscape reflects both broad defense portfolios and deep naval sustainment expertise. These players compete through long-term government contracts, advanced technological offerings, integrated logistics support, and strategic partnerships with shipyards and allied vendors. They emphasize service quality, turnaround time, and cost efficiency to win multi-year MRO agreements with national navies.

Key Industry Developments:

- In August 2025, India commissioned two Project 17A stealth frigates, INS Udaygiri and INS Himgiri, built by Mazagon Dock Shipbuilders (MDL) and Garden Reach Shipbuilders (GRSE). This marked the first simultaneous commissioning of frontline warships from two Indian shipyards. Equipped with advanced weapons and systems, the frigates bolster India’s maritime combat capabilities and strengthen naval presence in the Indian Ocean Region.

- In March 2025, Hindustan Shipyard Limited (HSL) emerged as a key catalyst in positioning India as a regional naval MRO hub, following its successful financial and operational turnaround that demonstrated naval MRO as a revenue-generating and growth-oriented business rather than a cost center. Leveraging its strategic location on India’s eastern coast at Visakhapatnam, close to major Indian Ocean shipping lanes and chokepoints such as the Strait of Malacca, HSL is well-placed to service naval and commercial vessels operating between the Pacific and Indian Oceans.

Companies Covered in Naval Vessels MRO Market

- BAE Systems

- General Dynamics

- Huntington Ingalls Industries

- Lockheed Martin

- Raytheon

- URS Corporation

- Saab AB

- Northrop Grumman

Frequently Asked Questions

The global naval vessels MRO market is projected to reach US$16.9 billion in 2026.

Rising defense spending, aging naval fleets requiring life-extension, increasing maritime security challenges, and the need to maintain high fleet readiness.

The naval vessels MRO market is expected to grow at a CAGR of 5.6% from 2026 to 2033.

The key opportunities include the adoption of performance-based logistics contracts, expansion of indigenous and regional MRO hubs, and increasing submarine and advanced vessel sustainment demand.

BAE Systems, General Dynamics, Huntington Ingalls Industries, Northrop Grumman, Lockheed Martin, and Raytheon are the leading players.