- Specialty & Fine Chemicals

- N-octyl Pyrrolidone Market

N-octyl Pyrrolidone Market Size, Share, and Growth Forecast 2026 - 2033

N-octyl Pyrrolidone Market by Grade (Industrial, Pharmaceutical, Other), Application (Pharmaceutical, Agrochemicals, Homecare & Cleaning Agents, Coatings & Paints, Adhesives & Sealants, Other), End-use Industry (Pharmaceutical, Construction, Automotive, Specialty Chemicals, Other), and Regional Analysis for 2026-2033

N-octyl Pyrrolidone Market Size and Trend Analysis

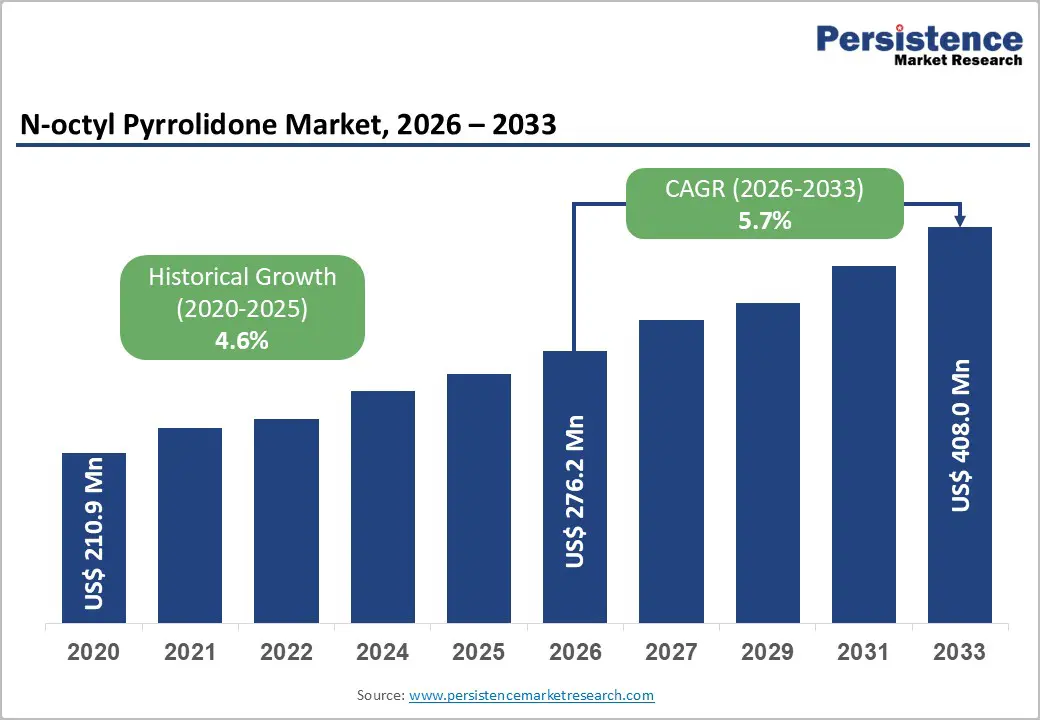

The global N-octyl pyrrolidone market size is supposed to be valued at US$ 276.2 Mn in 2026 and is projected to reach US$ 408.0 Mn by 2033, growing at a CAGR of 5.7% between 2026 and 2033.

The market is primarily driven by the escalating demand for environmentally benign solvents in the agrochemical and electronics industries. As regulatory bodies like the U.S. EPA and ECHA tighten restrictions on toxic solvents like N-methyl-2-pyrrolidone (NMP), N-octyl Pyrrolidone (NOP) is emerging as a preferred "Safer Choice" alternative due to its biodegradability and low aquatic toxicity. Furthermore, the robust expansion of the semiconductor manufacturing sector in the Asia Pacific is fueling the consumption of high-purity cleaning solvents, where NOP's unique surface tension properties are critical for residue-free wafer cleaning.

Key Market highlights

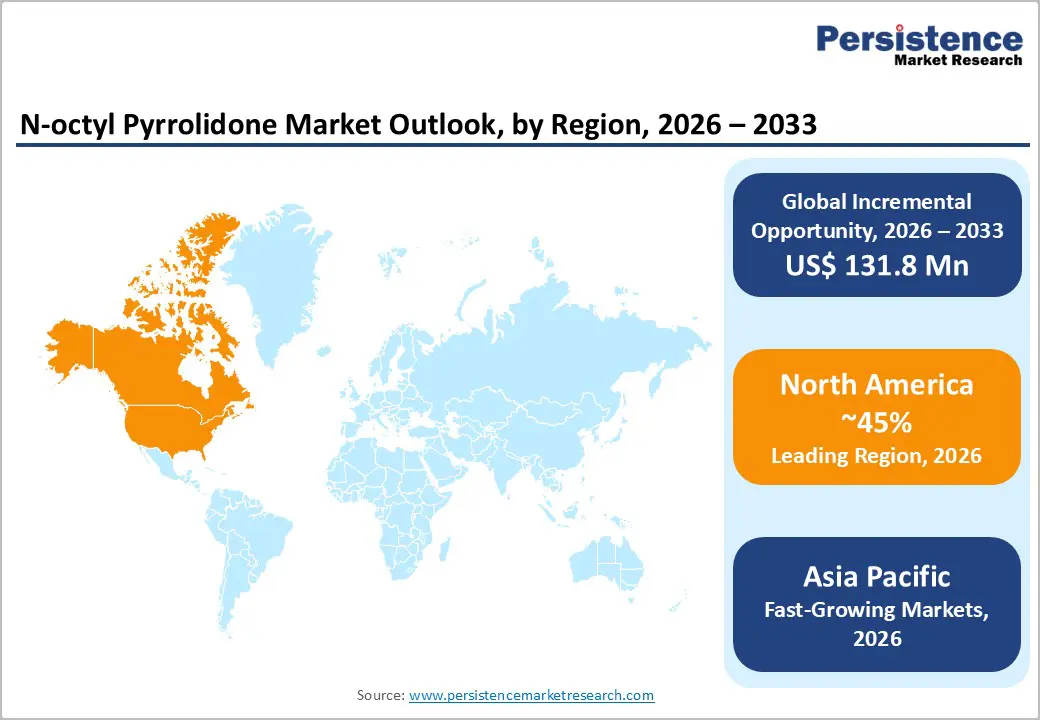

- Leading Region: North America maintains established leadership, accounting for approximately 45% global market share, driven by mature pharmaceutical infrastructure, stringent regulatory compliance frameworks, and established specialty chemical distribution networks supporting sustained premium-priced product demand.

- Fastest Growing Region: The Asia-Pacific region demonstrates the fastest growth trajectory at 6.9% CAGR through 2033, primarily driven by exponential pharmaceutical manufacturing expansion in China and India, aggressive agrochemical sector development supporting agricultural intensification, and rising disposable incomes.

- Dominant Segment: Industrial Grade holds the majority share, fueled by large-volume applications in crop protection formulations and industrial cleaning agents.

- Fastest Growing Segment: The homecare and cleaning agent segment emerges as the fastest-growing application category at 6.5% CAGR through 2033, reflecting intensifying consumer demand for environmentally sustainable cleaning products and major manufacturers' strategic initiatives toward eco-certified formulations.

- Key Market Opportunity: The electric vehicle battery electrolyte and next-generation energy storage applications represent emerging market opportunities with significant long-term potential, as battery material suppliers and equipment manufacturers investigate N-octyl pyrrolidone derivatives for specialized electrolyte formulations supporting accelerating electric vehicle adoption through 2033.

| Report Attribute | Details |

|---|---|

|

N-octyl Pyrrolidone Market Size (2026E) |

US$ 276.2 Mn |

|

Market Value Forecast (2033F) |

US$ 408.0 Mn |

|

Projected Growth CAGR (2026-2033) |

5.7% |

|

Historical Market Growth (2020-2025) |

4.6% |

Market Dynamics

Market Growth Drivers

Pharmaceutical Excipient Demand and Advanced Drug Delivery Systems

The pharmaceutical industry’s transition toward personalized medicine and biologic therapies is significantly increasing the demand for advanced solvent excipients such as N-octyl pyrrolidone. Over 70% of molecules in development pipelines are poorly soluble, necessitating high-performance solvents to enhance drug bioavailability and stability. N-octyl pyrrolidone offers superior solubilization of lipophilic active ingredients while ensuring compatibility with polymeric excipients, making it essential for processes including hot-melt extrusion, spray drying, and injectable formulations.

The global pharmaceutical excipients market is projected to grow at a 6.6% CAGR through 2032, with solvent excipients as the fastest-growing segment. Furthermore, stringent validation requirements from regulatory authorities such as the FDA and European Medicines Agency reinforce N-octyl pyrrolidone’s position as a compliant, reliable choice for leading pharmaceutical manufacturers.

Agrochemical Formulation Expansion and Crop Protection Solutions

The continued expansion of the agrochemical sector, particularly in emerging agricultural economies, is driving significant demand for N-octyl pyrrolidone as a key co-solvent in crop protection formulations. India’s agrochemical industry is projected to grow more than 7% CAGR through 2034, fueled by the need to enhance crop yields and manage pest populations using advanced formulation technologies. N-octyl pyrrolidone serves as an effective emulsifier in pesticide and herbicide formulations, ensuring superior dispersion of hydrophobic active ingredients in aqueous carriers while reducing surfactant requirements and minimizing foam generation during application.

The global agrochemical market is expected rise with specialty solvent adoption accelerating as manufacturers seek performance differentiation and regulatory compliance. Additionally, N-octyl pyrrolidone’s biodegradability and low aquatic toxicity align with stringent environmental regulations, including EU policy revisions promoting sustainable pesticide formulations.

Market Restraints

Regulatory Scrutiny and Health/Environmental Concerns

Escalating regulatory oversight regarding potential reproductive toxicity and bioaccumulation concerns presents a significant constraint on N-octyl pyrrolidone market expansion. The European Union's REACH (Registration, Evaluation, Authorization and Restriction of Chemicals) framework subjects specialty pyrrolidones to mandatory toxicity assessments and usage restrictions in specific applications. Additionally, the U.S. Environmental Protection Agency and international regulatory bodies continue evaluating pyrrolidone compounds' hazard profiles, creating uncertainty regarding future usage permissions and potential application bans in sensitive sectors.

Pharmaceutical manufacturers operating under stringent Good Manufacturing Practice (GMP) requirements increasingly face regulatory pressure to demonstrate complete safety dossiers and explore alternative excipients with lower toxicity concerns. This regulatory complexity extends product development timelines and increases compliance costs, potentially disadvantaging N-octyl pyrrolidone against emerging bio-based solvents positioned as environmentally benign alternatives.

Raw Material Volatility and Supply Chain Disruptions

N-octyl pyrrolidone production fundamentally depends on stable supplies of 2-pyrrolidone base chemicals and octyl amine derivatives, both subject to crude oil price fluctuations and petrochemical supply constraints. Major manufacturing disruptions, including the 2024 refinery maintenance cycles affecting solvent production in North America and Europe, created temporary supply shortages that elevated raw material costs by 12-15% across specialty pyrrolidone producers.

The concentration of production capacity among limited suppliers, primarily BASF SE, Ashland Inc., and Eastman Chemical Company, creates vulnerability to supply disruptions from facility maintenance, geopolitical instability, or capacity reallocation toward higher-margin products. End-user industries, including pharmaceuticals and agrochemicals, demonstrate limited flexibility in formulation modifications, creating inelastic demand that amplifies pricing pressure during supply-constrained periods.

Market Opportunities

Electric Vehicle and Battery Electrolyte Applications

The rapid shift toward electric vehicle adoption and the development of energy storage infrastructure is creating significant opportunities for N-octyl pyrrolidone in advanced battery electrolyte formulations and separator technologies. Manufacturers of lithium-ion batteries increasingly require high-purity solvents that deliver superior ionic conductivity, broad electrochemical stability, and enhanced thermal resistance. While N-methyl-2-pyrrolidone (NMP) has traditionally dominated this segment, research institutions and battery material suppliers are actively exploring N-octyl pyrrolidone derivatives as safer alternatives that maintain comparable electrolytic performance.

The global electric vehicle market is projected to grow at a 12.6% CAGR through 2032, with battery production expected to rise from 1.2 billion kWh in 2024 to 3.4 billion kWh by 2033. This growth trajectory underscores expanding demand for specialty solvents meeting pharmaceutical-grade purity and compatibility with next-generation solid-state battery technologies.

Bio-Based and Green Chemistry Formulations

Growing consumer preference for environmentally sustainable products, coupled with regulatory incentives promoting green chemistry, is creating significant opportunities for N-octyl pyrrolidone in biodegradable cleaning formulations and eco-certified home care products. The global homecare cleaning products market is projected to increase from US$ 270 billion in 2024 to US$ 380 billion by 2032, with sustainable formulations representing the fastest-growing segment at a 5.8% CAGR.

N-octyl pyrrolidone’s biodegradability and compatibility with plant-based surfactants position it as a strategic component for premium eco-friendly cleaning solutions. Leading manufacturers, including Unilever and Procter & Gamble, are investing heavily in sustainable product development, driving demand for specialty solvents that meet ecological standards while ensuring superior cleaning performance. Additionally, rising disposable incomes in Southeast and South Asia are accelerating the adoption of premium, environmentally responsible cleaning products.

Category-wise Insights

Grade Analysis

The industrial-grade N-octyl pyrrolidone segment holds the largest share of the market, accounting for approximately 52% of overall demand across industrial, pharmaceutical, and specialty chemical applications. These formulations, with a minimum purity of 99%, are widely used in crop protection, coatings, adhesives, and cleaning agent manufacturing, supported by consistent demand and competitive pricing compared to higher-purity alternatives. Their dominance reflects established supplier capacity and compatibility with processes tolerating minor impurities.

In contrast, the pharmaceutical-grade segment is projected to grow at a faster 6.8% CAGR through 2033, driven by stringent purity requirements (≥99.5%), comprehensive documentation, and compliance with USP and EP standards for advanced drug delivery systems. Specialty-grade formulations for electronics and semiconductor cleaning represent the fastest-growing micro-segment at 7.2% CAGR, though limited to an 8% market share due to specialized production needs.

Application Analysis

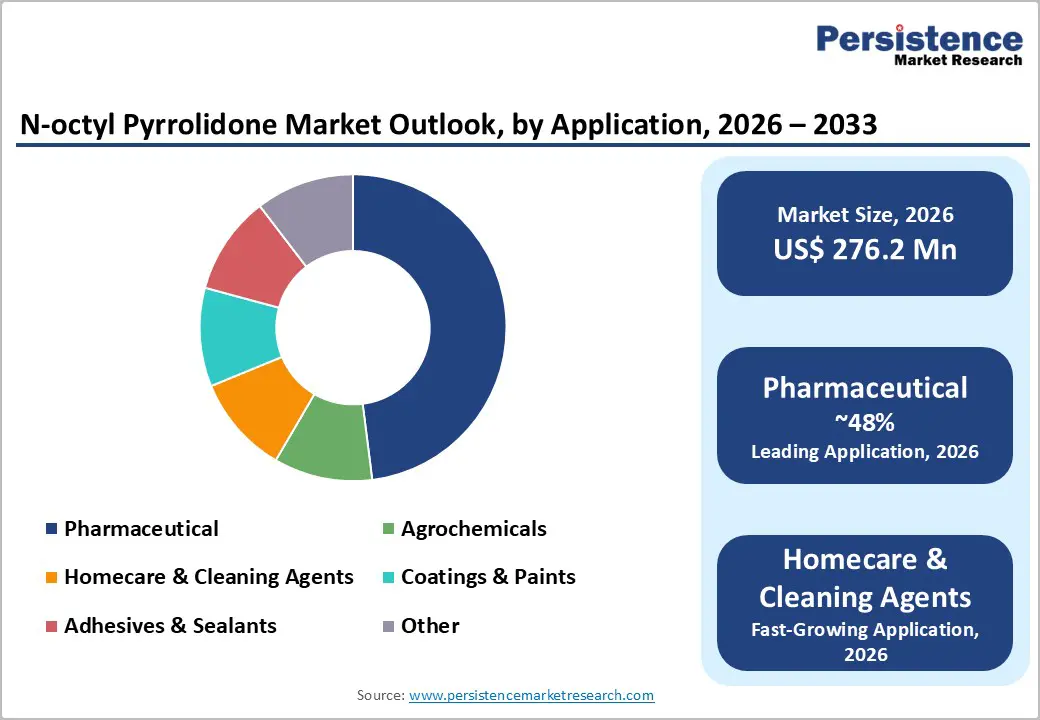

Pharmaceutical applications represent the largest segment of the N-octyl pyrrolidone market, accounting for 48% of total demand. Manufacturers primarily use N-octyl pyrrolidone as a solvent in active pharmaceutical ingredient synthesis, a permeation enhancer in topical and transdermal formulations, and a co-solvent in parenteral injectable preparations. This dominance reflects the growing complexity of modern drug formulations, particularly for lipophilic compounds and biologic therapies requiring advanced solubilization techniques.

The global pharmaceutical market is projected to grow at a 5.4% CAGR through 2032, with solvent excipient demand rising faster at 6.6% CAGR as companies adopt innovative drug delivery systems. Agrochemical applications hold the second-largest share at 32%, while homecare and cleaning agents account for 15%, demonstrating the fastest growth at 6.5% CAGR. Emerging uses in coatings and paints, though smaller, show steady expansion.

End-use Industry Analysis

The pharmaceutical manufacturing industry remains the dominant end-use sector for N-octyl pyrrolidone, accounting for 43% of the overall market share. Manufacturers across North America, Europe, and Asia-Pacific rely on this solvent for active pharmaceutical ingredient synthesis, excipient applications, and advanced drug delivery systems. This leadership reflects the industry’s emphasis on solvent quality, regulatory compliance, and performance reliability, sustaining demand for suppliers capable of meeting GMP standards and providing comprehensive documentation.

Construction and specialty chemicals collectively hold 37% share, utilizing N-octyl pyrrolidone in adhesives, coatings, and industrial solvents. Automotive applications represent 15%, driven by lightweight adhesive systems, protective coatings, and precision cleaning solutions. Emerging opportunities in energy storage and advanced electronics account for 5%, with strong growth potential linked to electric vehicle adoption and semiconductor manufacturing.

Regional Insights

North America N-octyl Pyrrolidone Trends

North America, led by the U.S., holds a dominant position in the N-octyl pyrrolidone market, supported by advanced pharmaceutical manufacturing infrastructure, stringent regulatory frameworks, and mature specialty chemical distribution networks. The U.S. pharmaceutical market, valued at approximately US$ 650 billion in 2024, continues to drive strong demand for high-quality solvent excipients as FDA-approved facilities expand production of complex formulations and biologic therapies. The sector is projected to grow at a 5.2% CAGR through 2032, with solvent excipient demand rising faster due to the shift toward specialized drug delivery systems. BASF SE’s capacity expansion at its Geismar, Louisiana site underscores supplier commitment to regional demand. Rigorous FDA oversight and GMP requirements create high entry barriers, sustaining premium pricing for compliant producers offering validated quality systems.

Europe N-octyl Pyrrolidone Trends

Europe is a strategically important market for N-octyl pyrrolidone, driven by stringent environmental regulations, advanced specialty chemical infrastructure, and growing adoption of sustainable formulation practices. The EU’s REACH framework imposes complex compliance requirements, favoring established suppliers with comprehensive toxicological data and usage documentation. Germany, home to BASF SE’s major operations in Ludwigshafen, maintains strong production capacity supporting both domestic pharmaceutical manufacturing and broader EU markets.

The German pharmaceutical sector consistently demands high-quality solvent excipients from leading manufacturers such as Merck KGaA, Boehringer Ingelheim, and Bayer AG. Additionally, the UK, France, and Spain collectively generate US$ 85 billion in annual pharmaceutical sales, while homecare manufacturers across Europe increasingly adopt eco-certified cleaning formulations, reinforcing N-octyl pyrrolidone’s favorable regulatory status and market growth potential.

Asia Pacific N-octyl Pyrrolidone Trends

Asia-Pacific is the fastest-growing regional market for N-octyl pyrrolidone, driven by rapid pharmaceutical manufacturing expansion, robust agrochemical sector development, and rising disposable incomes fueling demand for premium cleaning products. China leads the region as the world’s largest pharmaceutical producer, with exports exceeding US$ 45 billion annually, creating substantial demand for solvent excipients in API synthesis and formulation processes.

Key manufacturing hubs in Shanghai, Zhejiang, and Jiangsu require continuous N-octyl pyrrolidone supply, supported by major players such as China State Pharmaceutical Group Corporation. India ranks as the second-largest growth driver, with a US$ 65 billion pharmaceutical industry and a thriving agrochemical sector projected to grow at 7% CAGR through 2034. Mature markets in Japan and South Korea, along with emerging Southeast Asian economies, further strengthen regional demand through 2033.

Competitive Landscape

Market Structure Analysis

The N-octyl pyrrolidone market is highly consolidated, with three leading multinational specialty chemical companies, BASF SE, Ashland Inc., and Eastman Chemical Company, collectively accounting for approximately 60% of the global share. BASF SE, headquartered in Ludwigshafen, Germany, leads with about 28% market share, supported by integrated production capabilities and capacity expansions at its Geismar, Louisiana, facility targeting pharmaceutical, agricultural, and coating applications.

Ashland Inc., based in Wilmington, Delaware, holds a roughly 22% share through specialized pyrrolidone production and strong partnerships with pharmaceutical manufacturers requiring high-purity grades. Eastman Chemical Company, headquartered in Kingsport, Tennessee, commands around 18% share, focusing on strategic growth in pharmaceutical and specialty chemical sectors. Secondary players, including Mitsubishi Chemical, LyondellBasell, Nippon Shokubai, and Solvay, collectively represent 28%, while emerging producers in China and India contribute about 4%, primarily serving cost-sensitive industrial-grade applications.

Key Market Developments

August 2022: BASF SE announced significant capacity expansions for N-(2-Hydroxyethyl)-2-Pyrrolidone (HEP) and N-Octyl-2-Pyrrolidone (NOP) production at its Geismar, Louisiana Verbund site, with production targeted for the second half of 2022. The capacity enhancement addresses growing demand from coatings, agrochemicals, digital inks, and automotive industries, reinforcing BASF's market leadership and commitment to sustained supply growth.

March 2024: Ganzhou Zhongneng Industrial Co. Ltd. announced a significant expansion of N-methyl-2-pyrrolidone (NMP) production capacity by 100,000 tons annually, reflecting intensifying capacity investments throughout the broader pyrrolidone industry segment, responding to escalating global demand and market growth opportunities.

November 2024: Mitsubishi Chemical Corporation announced capacity expansions for high-purity specialty solvents, including solvent derivatives used in pharmaceutical and electronics applications, scheduled for implementation in 2024-2025, reflecting a commitment to emerging growth opportunities in Asia-Pacific pharmaceutical manufacturing and precision cleaning applications.

Top Companies in N-octyl Pyrrolidone Market

BASF SE (Germany) is the undisputed global leader in the pyrrolidone value chain, offering a comprehensive portfolio including N-Octyl-2-pyrrolidone dist. The company leverages its massive "Verbund" integration sites in Germany and the U.S. to ensure cost leadership and reliable supply. BASF focuses heavily on the agrochemical sector, positioning its NOP grades as premium co-solvents that comply with the strictest global safety standards.

Ashland Inc. (USA) is a key player known for its specialized surfactant and solvent solutions. Its flagship product, Surfadone™ LP-100, is an industry standard for wetting agents based on N-octyl Pyrrolidone. Ashland differentiates itself through deep technical application support, helping customers in the coatings and industrial cleaning sectors formulate low-VOC, high-performance products that meet complex environmental regulations.

Nippon Shokubai Industries (Japan) is a major force in the Asian chemical market, with strong capabilities in catalysis and organic synthesis. While broadly known for superabsorbent polymers, the company maintains a robust portfolio of pyrrolidone derivatives used in the high-tech electronics sector. Their strategic focus is on high-purity grades required for semiconductor processing, capitalizing on the strong domestic demand in Japan and neighboring South Korea.

Companies Covered in N-octyl Pyrrolidone Market

- BASF SE

- Ashland Inc.

- Eastman Chemical Company

- Mitsubishi Chemical Corporation

- LyondellBasell Industries Holdings

- Nippon Shokubai Industries

- MYJ Chemical

- Solvay S.A.

- Huntsman Corporation

- Dow Chemical Company

Frequently Asked Questions

The global market is projected to reach US$ 408.0 Mn by 2033, growing at a CAGR of 5.7% from 2026 to 2033.

The market is primarily driven by the shift toward safer, less toxic agrochemical formulations and the increasing demand for precision cleaning solvents in the electronics manufacturing industry.

Agrochemicals is the leading application segment, utilizing NOP as a critical co-solvent and surfactant to improve the efficacy and safety of pesticide formulations.

Asia Pacific is expected to be the fastest-growing region, supported by rapid industrialization, expanding semiconductor manufacturing, and strong growth in the agrochemical export sector.

A significant opportunity lies in the development of bio-based N-octyl Pyrrolidone variants to cater to the increasing demand for sustainable and renewable ingredients in personal care and pharmaceutical products.

Key market players include BASF SE, Ashland Inc., Nippon Shokubai Industries, and MYJ Chemical, among others, who dominate the global production and supply landscape.