- Food Ingredients & Additives

- Molasses Market

Molasses Market Size, Share and Growth Forecast, 2026 - 2033

Molasses Market by Application (Food & Beverage, Animal Feed, Biofuels & Alcohol, Industrial & Fermentation, Agriculture & Environmental, Pharmaceutical), Source (Sugarcane Molasses, Sugar Beet Molasses), Grade (Light Molasses, Dark Molasses, Blackstrap Molasses, Sulfured Molasses, Unsulfured Molasses), and Regional Analysis for 2026 - 2033

Molasses Market Share and Trends Analysis

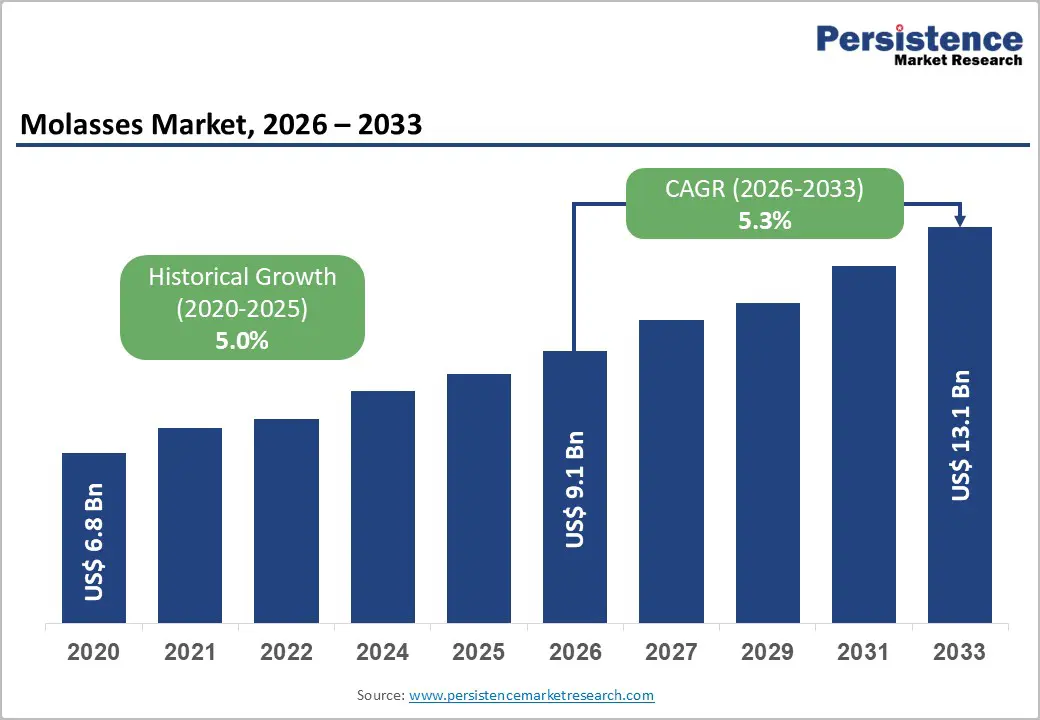

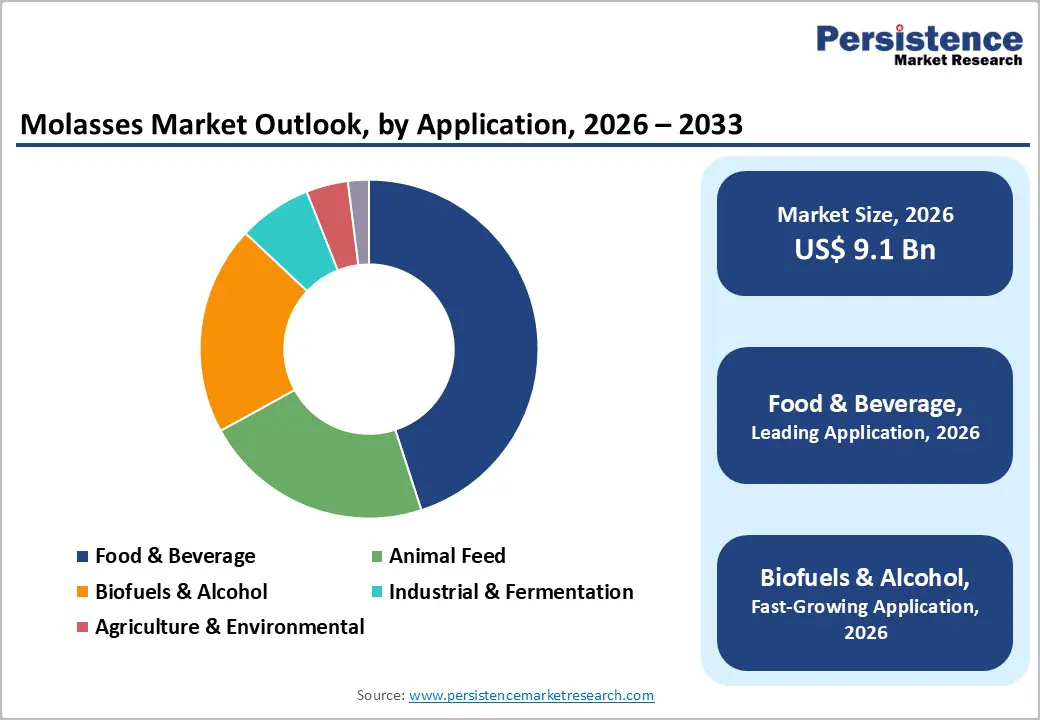

The global molasses market size is likely to be valued at US$ 9.1 billion in 2026 and is projected to reach US$ 13.1 billion by 2033, growing at a CAGR of 5.3% during the forecast period 2026–2033.

The molasses market is growing steadily due to evolving consumer preferences for natural, minimally processed sweeteners and clean-label food ingredients, which are increasing its use in bakery, confectionery, and beverage applications. Its functional benefits, including high mineral content, energy density, and fermentable sugars, make it a cost-effective input for animal feed, ethanol production, and industrial fermentation processes. Expansion of biofuel blending programs is significantly boosting demand from distilleries. Additionally, rapid urbanization, rising disposable incomes, and dietary shifts in emerging markets are driving higher consumption of processed foods and protein, strengthening molasses demand across multiple industrial and agricultural value chains.

Key Industry Highlights

- Leading Application Segments: Food & beverage is expected to lead with around 45% revenue share in 2026, while biofuels & alcohol is projected to be the fastest-growing segment at a 6.8% CAGR through 2033, driven by expanding ethanol blending mandates and renewable energy policies.

- Dominant Source Type: Sugarcane molasses is anticipated to dominate with approximately 65% share in 2026, while sugar beet molasses is likely to witness the fastest growth at a 6.2% CAGR during 2026–2033, particularly across Europe with strong regional supply chains.

- Leading Grade Segment: Blackstrap molasses is expected to hold the largest share at 40% in 2026 due to its high nutrient concentration and widespread use in animal feed and fermentation, while unsulfured molasses is projected to be the fastest-growing grade at a 6.5% CAGR through 2033, driven by rising demand for clean-label and food-grade products.

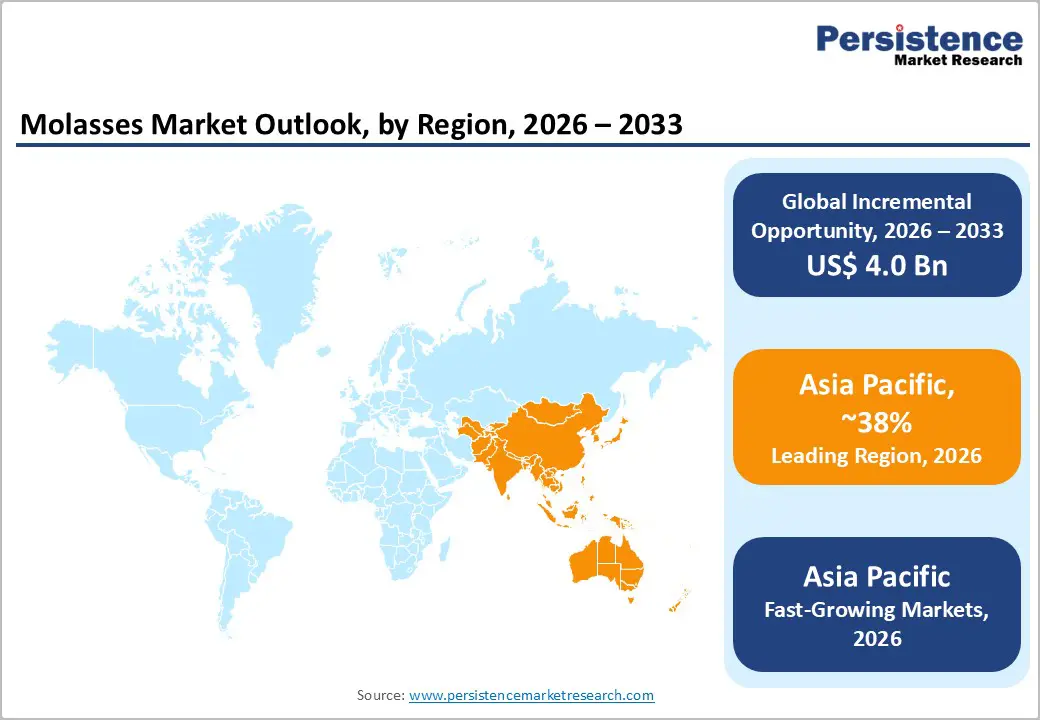

- Regional Leadership: Asia Pacific is poised to lead with an estimated 38% share in 2026 and register the fastest growth at 7.1% CAGR through 2033, supported by large-scale sugar production, expanding industrial applications, and favorable government initiatives.

- Key Industry Drivers: Market growth is increasingly shaped by investments in ethanol capacity expansion and the rising importance of fermentation industries, strengthening demand across industrial applications.

- Emerging Opportunity Areas: Growing emphasis on sustainable agriculture and bio-based chemicals is expected to create new growth avenues, with increasing adoption in soil conditioning, organic fertilizers, and green industrial processes.

| Key Insights | Details |

|---|---|

|

Molasses Market Size (2026E) |

US$ 9.1 Bn |

|

Market Value Forecast (2033F) |

US$ 13.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.0% |

DRO Analysis

Driver - Rising Demand for Biofuels and Ethanol Blending Policies

Global energy transition strategies are creating a significant surge in demand for molasses in biofuels and alcohol production. The U.S. Renewable Fuel Standard (RFS) program announced an upward revision of biofuel blending obligations for 2026, increasing required ethanol volumes in gasoline to reduce greenhouse gas emissions. Simultaneously, the European Union’s Renewable Energy Directive (RED III) set more ambitious targets for renewable liquid fuels, encouraging member states to boost bioethanol uptake. These policy updates strengthen market clarity for ethanol producers globally and create structural demand pull for fermentable feedstocks such as molasses. Analysts also note that global biofuel consumption trends are accelerating investments in new distillation and storage infrastructure, further supporting feedstock demand.

Molasses is favored as a feedstock because of its high fermentable sugar content and cost advantage over alternative raw materials. Major ethanol producers in Brazil and the U.S. reported expanded intake agreements with sugar mills through 2025, signaling industry alignment with regulatory trends. Publicly available government data from the U.S. Energy Information Administration (EIA) shows rising ethanol throughput in U.S. distilleries in 2025, underpinned by blending requirements. This combination of policy signals and operational commitments is reinforcing molasses as a strategic ingredient in renewable fuel supply chains and supporting long?term capital investment decisions in integrated sugar?ethanol facilities. Furthermore, increasing global energy security concerns are motivating countries to reduce dependence on imported fuels, indirectly sustaining molasses demand.

Expansion of the Livestock Industry and Industrial Fermentation

The global livestock sector is witnessing sustained growth, particularly across Asia Pacific, Latin America, and parts of Africa, driven by rising per?capita protein consumption. Molasses is increasingly used as a high?energy feed supplement and binding agent in compound feed, improving nutritional intake while helping control formulation costs. The Food and Agriculture Organization (FAO) reported steady growth in global feed production in 2025, reflecting ongoing expansion of the poultry and swine sectors. Nutrient?rich molasses enhances digestibility and feed conversion ratios, making it a preferred choice for feed formulators seeking cost?effective energy sources. The rising adoption of mechanized feed production and modern livestock management practices is further supporting molasses integration across commercial operations.

Simultaneously, industrial fermentation applications are expanding, with 2025 production data highlighting increases in yeast and enzyme output across Europe and North America. The European Commission’s bioeconomy strategy updates emphasized support for fermentation?based manufacturing, including incentives for renewable feedstocks and circular production processes. Molasses, a reliable by?product of sugar processing, is benefiting from these frameworks, as manufacturers seek consistent supply sources for industrial enzymes, organic acids, and bio?based chemicals. These macro?trends are creating structural demand for molasses beyond traditional feed use, reinforcing its role as a versatile ingredient in multiple industrial value chains. Rising investments in sustainable production facilities are expected to further accelerate adoption in both traditional and emerging industrial applications.

Restraints - Volatility in Sugar Production and Raw Material Availability

Molasses availability is inherently linked to sugarcane and sugar beet production, which are affected by seasonal patterns and climate variability. In the 2025/26 crop cycle, Brazil’s national sugarcane harvest contracted by ~1.6% with productivity declining by 3.8%, highlighting environmental and agronomic pressures on raw material supply. Weather events such as droughts, floods, and unseasonal rainfall in major producing regions exacerbate fluctuations, causing significant supply imbalances. Ethanol distilleries and industrial fermentation sectors, which rely on predictable feedstock volumes, are particularly sensitive to these variations. Price volatility and uncertainty make long-term planning challenging for producers and end-users alike. These factors also influence global trade flows, as countries adjust import and export strategies in response to local production shortfalls.

Global molasses price movements in Q2 2025 reflected this volatility, with significant regional variation due to crop fluctuations and climatic conditions. Supply uncertainty pressures logistics, storage, and procurement strategies, forcing operators to maintain higher inventories or rely on alternative sourcing. Smaller producers often face higher exposure to risk, discouraging large-scale investments and limiting operational flexibility. Investors and downstream manufacturers must account for potential disruptions, which can ripple across ethanol, feed, and fermentation industries. Collectively, these factors limit market stability, creating persistent structural challenges for molasses supply chains and impacting global pricing dynamics.

Regulatory Constraints and Environmental Compliance Costs

Molasses?based industries, particularly ethanol distilleries, operate under strict environmental regulations governing wastewater discharge, air emissions, and effluent management. For example, in late 2025, the Government of India’s Union Ministry of Finance issued Customs Notification No.?48/2025, formally removing export duty on cane molasses to nil, a policy shift affecting supply flows but also signaling how export and environmental regulations are actively influencing industry economics. Compliance with regional standards across major markets often requires significant investments in treatment plants, monitoring systems, and reporting mechanisms to meet water and air quality norms. These upgrades substantially raise operational costs, particularly for small and medium distilleries with limited capital buffers.

Rising environmental expectations are leading regulators to mandate advanced wastewater management practices, including Zero Liquid Discharge (ZLD) systems, which ensure that no liquid industrial effluent leaves a facility, a baseline requirement in several distillery jurisdictions as of 2026, reflecting tightening policy enforcement. These requirements can delay capacity expansions, increase permitting timelines, and restrict operational flexibility, especially for new facilities. Evolving standards, including periodic reviews of discharge limits and real?time compliance reporting, further increase long?term planning complexity. As a result, compliance costs and regulatory pressures act as key restraints, influencing profitability, capital investment decisions, and strategic planning across the molasses industry.

Opportunities - Emerging Demand for Sustainable Agriculture and Circular Bio?Inputs

Molasses is increasingly leveraged as a bio?based soil conditioner, organic fertilizer, and microbial stimulant, supporting sustainable and regenerative agriculture. Governments and agriculture bodies globally are advancing climate?smart farming initiatives that elevate demand for eco?friendly soil enhancers and organic inputs. For example, India’s National Policy on Biofuels 2018, amended for 2025–26, explicitly promotes using agricultural residues and renewable feedstocks such as molasses for diversified bio?production applications, demonstrating policy support for circular agricultural value chains. Molasses improves soil microbial activity, enhances nutrient retention, and supports crop resilience, making it attractive for farms transitioning away from synthetic fertilizers.

The opportunity is particularly pronounced in Asia Pacific and Europe, where soil health programs and organic certification frameworks are expanding market pull for renewable inputs. European Union member states are incentivizing organic amendments to improve carbon sequestration and soil biodiversity, creating regulatory tailwinds for molasses?based products. Adoption by agricultural cooperatives and commercial farms adds scale, generating consistent demand. As sustainability metrics become integral to agricultural financing and procurement standards, molasses stands to benefit from increasingly institutionalized demand for circular bio?inputs, positioning it as a core ingredient in next?generation agriculture.

Expansion of Bio?Based Industrial Applications and Biorefineries

The transition toward bio?based industrial production is unlocking new avenues for molasses beyond traditional food and feed applications. Countries and regions are incentivizing renewable feedstocks for sustainable manufacturing, which is driving uptake of molasses in fermentation?based biorefineries that produce specialty chemicals, organic acids, and bio-materials. In 2026, at Germany’s Biotech Days, federal policymakers and industry leaders highlighted biotechnology’s role as a key driver of industrial competitiveness, emphasizing support for bio-based chemical manufacturing and green industrial processes. These initiatives underscore growing markets for biodegradable and sustainable chemical intermediates, creating concrete opportunities for molasses as an economical, renewable feedstock in emerging bio-industrial applications.

Additionally, industrial players are investing in precision fermentation and biotechnological platforms that repurpose sugar industry by?products into high?value molecules. A leading Latin American sugar company announced plans in 2026 to build a large?scale precision fermentation facility adjacent to its sugar mill to produce value?added proteins and bio?compounds, illustrating how legacy agricultural sectors are repositioning for advanced biomanufacturing. These developments show that molasses is increasingly recognized as a versatile renewable substrate that supports industrial diversification, circular economy models, and sustainable supply chains, creating long?term demand opportunities for producers and end?users in emerging bio?industrial markets.

Category-wise Analysis

Application Insights

The food & beverage segment is likely to be the leading application, estimated to account for 45% of the global molasses market in 2026, due to its extensive use as a natural sweetener, flavor enhancer, and colorant in bakery products, confectionery, beverages, and other processed foods. The global shift toward clean-label, plant-based ingredients is driving demand, as consumers increasingly prefer natural alternatives to artificial additives. In 2025, industry reports highlighted innovation in natural sweeteners and fortified formulations as a key trend, with molasses being integrated into both mainstream and niche products. Manufacturers are reformulating recipes to meet health-conscious preferences, emphasizing transparency and functional benefits, which further reinforces molasses’ dominance in food applications.

The biofuels & alcohol segment is projected to be the fastest-growing application, projected to expand at a 6.8% CAGR through 2033, driven by global renewable energy policies and expanding ethanol production infrastructure. Molasses is a cost-effective, high-sugar feedstock for fermentation, making it a preferred choice for ethanol production in regions such as Europe and North America. In 2025, the European Commission’s Renewable Energy Directive update reinforced blending targets for ethanol in transport fuels, directly supporting molasses-based ethanol use. Industrial players have simultaneously invested in upgrading distilleries and fermentation facilities to meet higher biofuel mandates, positioning molasses as a key input in the renewable energy value chain. The convergence of policy incentives, investment, and renewable energy demand makes this segment a major driver of molasses market growth.

Source Insights

Sugarcane molasses is expected to remain the dominant source, accounting for approximately 65% of the global market in 2026, due to high production volumes in Brazil, Southeast Asia, and Latin America. Its high sugar content and cost efficiency make it ideal for applications in food, feed, ethanol, and industrial fermentation. In 2025, global reports highlighted that sugarcane co-products were increasingly being optimized for industrial and biofuel use, reflecting structural demand for consistent, high-volume feedstocks. Integrated processing infrastructure enables stable supply and logistics for industrial users, reinforcing sugarcane molasses’ market leadership. Demand across multiple sectors, including food and renewable energy, is expected to sustain this dominance through the forecast period.

Sugar beet molasses is anticipated as the fastest-growing source, projected to register a 6.2% CAGR through 2033, particularly in Europe, where sugar beet cultivation and processing are well-established. In 2025, European producers such as Tereos and Nordzucker emphasized maximizing value from sugar beet by-products, including molasses, to meet growing demand in fermentation, feed, and bio-based chemical applications. Policies encouraging local sourcing and sustainability, along with efforts to reduce waste streams, have further strengthened the adoption of beet molasses as a high-value feedstock. With regional processing campaigns supporting consistent supply, sugar beet molasses is positioned to outpace other sources in growth while complementing sugarcane molasses in global market demand.

Regional Insights

North America Molasses Market Trends

North America holds a significant position in the global molasses market, supported by diversified demand across animal feed, industrial fermentation, and renewable ethanol production. In mid?2025, U.S. molasses price trends remained firm, with levels around US?$285–$295/MT, reflecting sustained consumption from ethanol distilleries and livestock feed formulators, even amid broader commodity fluctuations. ([turn0news0]) The United States leads regional market activity with advanced feed manufacturing infrastructure and robust fermentation sectors producing yeast, organic acids, and bio?based intermediates. Regulatory frameworks from the U.S. Environmental Protection Agency (EPA) and renewable fuel mandates continue to promote molasses use in bioethanol and sustainable manufacturing.

North America also benefits from well?developed processing and logistics networks that support stable supply flows to domestic and export markets. Canada contributes demand through growing livestock feed production and agricultural inputs, reinforcing regional consumption diversity. In 2025, several North American ethanol plants reported expanded molasses procurement to offset corn price volatility, demonstrating molasses’ strategic role as a feedstock. Investments in circular economy initiatives and bio?based production were highlighted by industry gatherings as central to future competitiveness. These structural dynamics ensure stable growth and resilient molasses demand.

Europe Molasses Market Trends

Europe has a mature and steadily advancing molasses market, anchored by strong demand in livestock feed, agricultural inputs, and fermentation?based industries. Demand is underpinned by extensive sugar beet processing activities across Germany, France, Spain, and neighboring countries, which generate significant volumes of beet molasses as a co?product. In 2025, European sugar beet processors reported optimized utilization of beet by-products for animal feed and industrial fermentation as a priority strategy amid evolving agricultural outputs. The region’s sustainability directives and bioeconomy strategies, including implementation plans for renewable fuels and sustainable agriculture, have reinforced molasses’ role as a low-carbon feedstock for bioethanol, soil conditioners, and renewable chemical intermediates.

Sugar beet molasses aligns with Europe’s environmental policy priorities, particularly in organic farming and soil health initiatives, which are increasingly adopted as part of national agricultural frameworks. Reports from late 2025 also noted adjustments in beet acreage due to market conditions, amplifying the focus on efficient by-product utilization to sustain feedstock supply chains. Additionally, European animal feed producers expanded molasses incorporation in response to rising feed efficiency standards and nutritional optimization trends. Combined with continued investments in fermentation capacity and renewable inputs, Europe is maintaining a steady regional molasses market, reinforcing its role as a key contributor to global demand alongside Asia Pacific.

Asia Pacific Molasses Market Trends

Asia Pacific is poised to lead with an estimated 38% share in 2026 and register the fastest growth at 7.1% CAGR through 2033, with momentum driven by expanding sugarcane cultivation, industrial application diversification, and supportive regional policies. The region’s growth is propelled by large-scale sugar production in China, Thailand, Indonesia, and ASEAN nations that ensures a cost-efficient and abundant molasses supply. In 2025, regional sugar mills and industrial stakeholders reported expanded utilization of sugarcane co-products, including molasses, to support rising demand from livestock feed, bioethanol, and industrial fermentation, highlighting molasses’ shifting role beyond traditional markets.

Rapid industrialization, increasing global protein consumption, and government support for bio-based chemicals and renewable energy initiatives further drive molasses demand across Asia Pacific. Policy forums in 2025 emphasized renewable feedstock integration for sustainable manufacturing and agricultural innovation, creating structured demand signals for molasses in both established and emerging value chains. The region also benefits from favorable labor and production costs, enabling large-scale operations. Investments in fermentation infrastructure and biofuel capacity continue to expand, securing long-term growth and reinforcing Asia Pacific as the primary growth engine of the global molasses market through the forecast period.

Competitive Landscape

The global molasses market is moderately consolidated, with leading players such as Cargill, Cosan, Mitr Phol Group, Südzucker, and Archer Daniels Midland (ADM) collectively controlling a significant portion of revenue. These established companies leverage integrated sugar processing and ethanol production capabilities, extensive supply chains, and long-standing relationships with industrial and agricultural customers. They also invest in R&D and sustainability initiatives to enhance product quality, develop value-added molasses derivatives, and meet evolving regulatory and environmental standards.

Regional and niche competitors, including Tereos, Fuchs Sugar, and Thai Roong Ruang Group, focus on specialized product lines, local markets, and strategic supply partnerships. Challenges such as volatile sugar production, raw material availability, and compliance with environmental regulations act as barriers to new entrants. However, growing demand from biofuels, industrial fermentation, and sustainable agriculture sectors enables innovation-led smaller players to capture opportunities through partnerships and value-added solutions. Market consolidation is expected to rise gradually, driven by mergers, capacity expansion, and strategic collaborations that enhance geographic reach and technological capability.

Key Industry Developments

- In July 2025, Hartree expanded its footprint in soft commodities by acquiring ED&F Man’s Liquid Products (molasses, feed), Sugar, Volcafe, and Cotton units, leveraging established logistics and market expertise. The European Commission approved the deal, enabling Hartree to strengthen its global position in agricultural commodities alongside energy trading.

- In February 2025, Cargill acquired the remaining 50% stake in SJC Bioenergia, gaining control of two industrial plants in Goiás for sugar, ethanol, and renewable energy production. This move enhances Cargill’s biofuels portfolio, increases molasses-related ethanol output, and aligns with Brazil’s growing sustainable fuel demand.

Companies Covered in Molasses Market

- Archer Daniels Midland Company

- Cargill, Incorporated

- Wilmar International Limited

- Louis Dreyfus Company

- Tereos Group

- Südzucker AG

- Associated British Foods plc

- Raízen

- Mitr Phol Group

- Balrampur Chini Mills Ltd.

- Shree Renuka Sugars Limited

- American Crystal Sugar Company

- COFCO International

- Nordzucker AG

Frequently Asked Questions

The global molasses market is projected to reach US$ 9.1 billion in 2026.

Rising demand in food, biofuels, and industrial fermentation drives molasses consumption globally.

The market is expected to grow at a CAGR of 5.3% from 2026 to 2033.

Bio-based chemicals, sustainable agriculture inputs, and renewable energy applications offer significant growth potential.

Cargill, Cosan, Mitr Phol Group, Südzucker, and Archer Daniels Midland (ADM) are leading market players.