- Biotechnology

- Microarrays Market

Microarrays Market Size, Share, Trends, Growth, and Regional Forecast, 2026 - 2033

Microarrays Market by Product (Consumables, Software and Services, and Instruments), Microarray Type (DNA Microarrays, Protein Microarrays, Tissue Microarrays, and Others), Application (Research Applications, Drug Discovery & Development, Disease Diagnostics, and Others), and Regional Analysis from 2026 - 2033

Microarrays Market Share and Trend Analysis

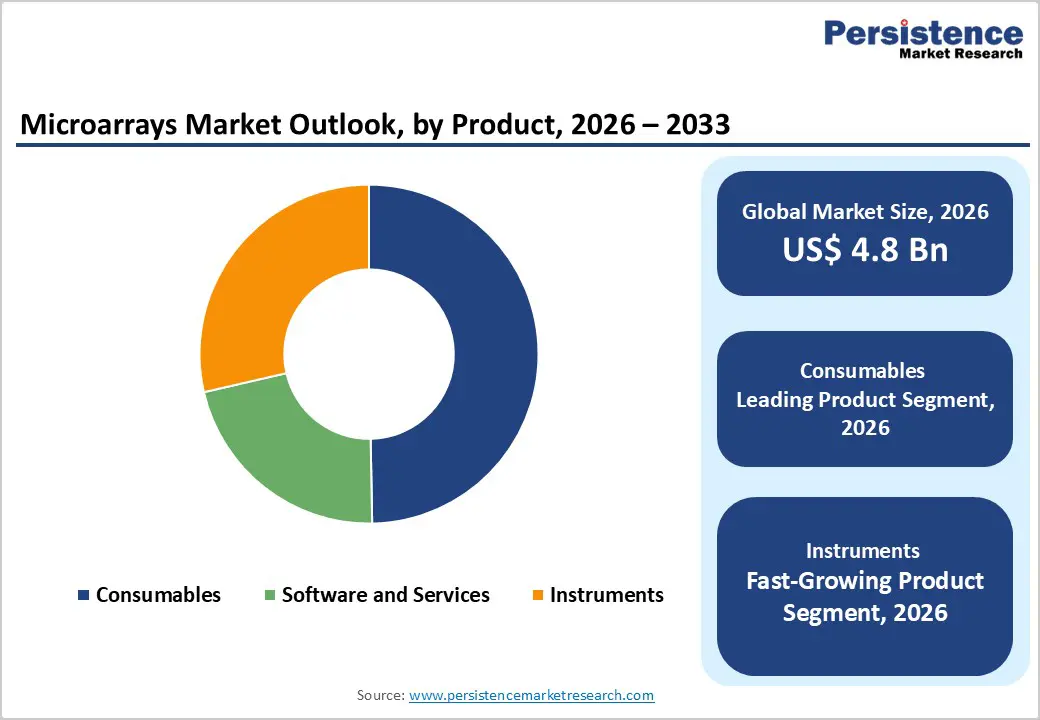

The global microarrays market size is estimated to grow from US$ 4.8 Bn in 2026 to US$ 7.9 Bn by Bn 2033. The market is projected to record a CAGR of 6.4% during the forecast period from 2026 to 2033. Global demand for microarrays is advancing steadily, supported by the growing emphasis on genomics research, molecular diagnostics, and precision medicine. These platforms are extensively utilized for gene expression profiling, SNP analysis, and biomarker discovery, enabling simultaneous evaluation of thousands of genetic sequences with high efficiency. The increasing incidence of cancer, genetic disorders, and infectious diseases is accelerating the need for high-throughput analytical technologies in both research and clinical environments.

Rising awareness around personalized medicine, along with improved access to advanced laboratory infrastructure and bioinformatics tools, is encouraging broader adoption across academic institutes and biotechnology companies. In addition, pharmaceutical firms are incorporating microarrays into drug discovery pipelines for target identification and toxicity studies. Continuous innovation in probe design, array density, and data analytics is enhancing accuracy and reproducibility. Expansion of contract research organizations, growing funding for life sciences, and increasing integration of multi-omics approaches are further supporting sustained market progression across developed and emerging regions.

Key Industry Highlights:

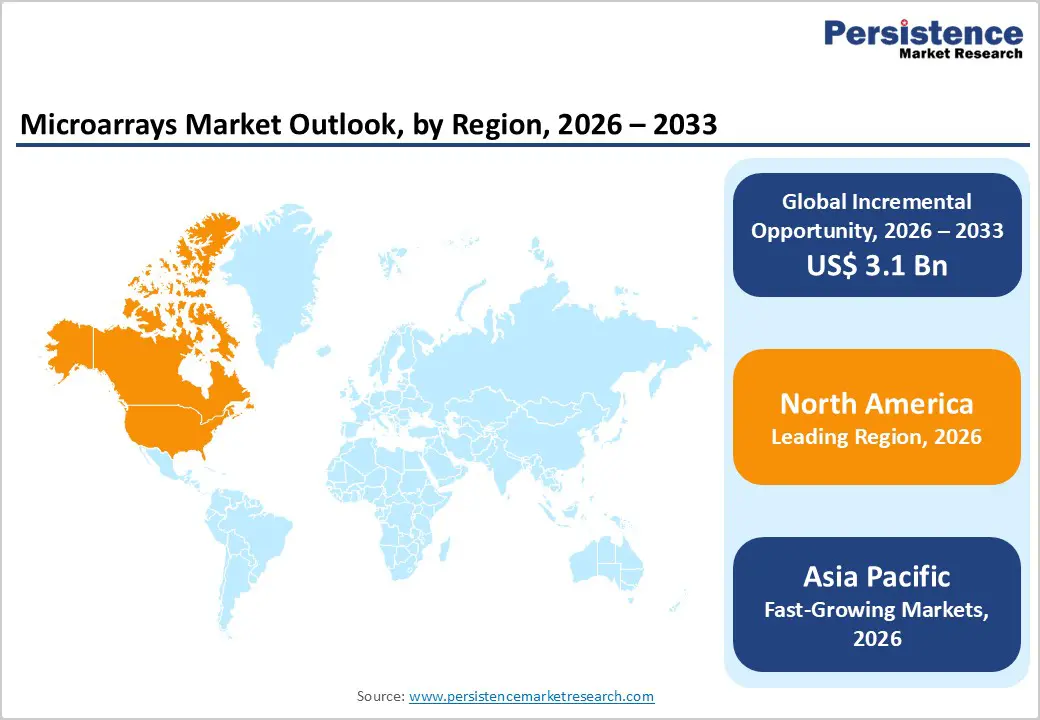

- Leading Region: North America accounts for 48.5% of global revenue, supported by advanced genomics infrastructure, strong presence of biotechnology leaders, and extensive funding for molecular research and precision medicine initiatives.

- Fastest-Growing Region: Asia Pacific represents the fastest-growing region, driven by expanding biotechnology sectors, rising investments in genomics research, and improving access to advanced diagnostic technologies.

- Leading Product Segment: Consumables hold a 49.7% market share, primarily due to their recurring usage in laboratory workflows, including reagents, probes, and microarray kits required for every analysis cycle.

- Fastest-Growing Product Segment: Instruments are witnessing faster growth as laboratories increasingly adopt automated and high-throughput systems to enhance efficiency and data accuracy.

- Leading Microarray Type Segment: DNA Microarrays account for the largest share, supported by their extensive application in gene expression studies, cancer research, and large-scale genomic analysis.

- Fastest-Growing Microarray Type Segment: Protein Microarrays are gaining traction due to their expanding role in proteomics, biomarker identification, and drug discovery applications.

| Key Insights | Details |

|---|---|

|

Microarrays Market Size (2026E) |

US$ 4.8 Bn |

|

Market Value Forecast (2033F) |

US$ 7.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.8% |

DRO Analysis

Driver – Expanding Genomics Research and Growing Integration of Precision Medicine Approaches

A major force accelerating industry growth is the rapid expansion of genomics and molecular biology research, particularly in areas such as oncology, rare diseases, and pharmacogenomics. Microarray platforms enable simultaneous analysis of thousands of genes, making them indispensable tools for gene expression profiling, SNP detection, and biomarker identification. The increasing global burden of cancer and genetic disorders has intensified the need for high-throughput analytical technologies that can support early diagnosis and targeted therapy development. In parallel, the shift toward precision medicine is significantly influencing adoption patterns. Healthcare systems and research institutions are prioritizing patient-specific treatment strategies, where microarrays play a critical role in identifying genetic variations and disease pathways.

Moreover, substantial funding from government bodies and organizations such as the National Institutes of Health and the European Commission continues to strengthen large-scale genomics initiatives. Pharmaceutical and biotechnology companies are also integrating microarrays into drug discovery pipelines for target validation and toxicity assessment. Continuous technological advancements, including improved probe sensitivity and data analysis capabilities, are enhancing reliability and throughput. Collectively, the convergence of research expansion, clinical relevance, and funding support is driving sustained demand across both academic and commercial settings.

Restraints – Competition from Next-Generation Sequencing and Data Complexity Challenges

One of the primary constraints limiting broader adoption is the increasing competition from advanced genomic technologies such as next-generation sequencing (NGS). Platforms developed by companies like Illumina, Inc. offer deeper genomic insights, higher resolution, and the ability to detect novel mutations, which in some cases reduces reliance on microarray-based analysis. As sequencing costs continue to decline, many research institutions and clinical laboratories are gradually shifting toward NGS for comprehensive genomic profiling. Another critical challenge lies in the complexity of data interpretation associated with microarray experiments. These platforms generate large datasets that require sophisticated bioinformatics tools and skilled personnel for accurate analysis. In regions with limited technical expertise or inadequate computational infrastructure, this can restrict effective utilization.

Morever, issues related to cross-hybridization, limited dynamic range, and dependency on pre-designed probes may affect analytical precision in certain applications. Cost considerations also remain relevant, particularly for smaller laboratories that may struggle with the initial investment in instrumentation and ongoing consumable expenses. These technological and operational limitations, combined with evolving alternatives, may moderate growth potential in specific application areas.

Opportunity – Emerging Clinical Diagnostics Applications and Integration with Multi-Omics Technologies

Significant growth potential is emerging from the expanding role of microarrays in clinical diagnostics and translational medicine. While historically concentrated in research environments, these platforms are increasingly being utilized for disease screening, prognostic evaluation, and companion diagnostics. Applications such as cancer classification, genetic disorder identification, and infectious disease detection are creating new avenues for commercialization. Regulatory advancements and validation of diagnostic assays are further supporting their transition into clinical workflows.

Furthermore, the opportunity lies in the integration of microarrays with multi-omics approaches, including genomics, proteomics, and transcriptomics. By combining microarray data with sequencing and proteomic analysis, researchers can achieve a more comprehensive understanding of biological systems and disease mechanisms. This convergence is particularly valuable in drug discovery, where multi-layered data improves target identification and accelerates therapeutic development. Additionally, expanding healthcare infrastructure in emerging economies, including India and China, is increasing access to advanced diagnostic technologies. The rise of contract research organizations and growing investments in biotechnology are further enhancing market penetration. As innovation continues across both research and clinical domains, these factors are expected to unlock substantial long-term opportunities.

Category-wise Analysis

By Product Insights

Consumables are projected to account for 49.7% of global market revenue in 2026, positioning them as the leading product category. Their dominance is primarily attributed to continuous usage across gene expression studies, sequencing workflows, and diagnostic assays, where reagents, slides, and probes are required in every experiment cycle. Unlike instruments, which represent one-time capital investments, consumables generate sustained demand driven by repetitive laboratory operations. The rapid increase in genomics research, particularly in oncology and rare disease studies, has further strengthened segment growth. Additionally, the expansion of clinical testing and biomarker discovery programs is accelerating the consumption rate of microarray kits and reagents. Pharmaceutical and biotechnology companies rely heavily on consumables for drug target validation and toxicogenomics, reinforcing their consistent uptake. Advancements in reagent sensitivity, array density, and assay precision are also enhancing experimental efficiency. With the rising adoption of high-throughput screening and increasing laboratory automation, consumables are expected to maintain their dominant share over the forecast period.

By Application Insights

The research applications segment is expected to hold 46.5% of the global market in 2026, reflecting its central role in microarray utilization. These platforms are extensively applied in gene expression profiling, SNP analysis, and functional genomics, enabling researchers to analyze thousands of genes simultaneously. Academic institutions and research organizations continue to depend on microarrays for large-scale biological investigations, particularly in cancer genomics, immunology, and personalized medicine development. Increasing global funding for life sciences research and the expansion of genomics-based projects are further supporting segment growth. Microarrays also play a vital role in early-stage drug discovery, where they are used to identify disease-associated biomarkers and therapeutic targets. The ability to deliver high-throughput, cost-effective analysis compared to sequencing technologies sustains their relevance in research settings. Furthermore, ongoing technological improvements in array design and data analytics are enhancing accuracy and reproducibility. Collectively, these factors ensure the continued leadership of research applications within the microarrays market.

By End-user Insights

Research & academic institutes are anticipated to contribute 45.1% of total market revenue in 2026, underscoring their dominant position. These institutions represent the primary users of microarray technologies, driven by extensive involvement in genomics, transcriptomics, and proteomics research. Government-funded projects, university-led studies, and collaborations with biotechnology firms are significantly boosting demand for microarray platforms within this segment. Laboratories in academic settings frequently conduct large-scale experiments requiring continuous access to consumables and analytical tools, ensuring steady utilization. In addition, research institutes are at the forefront of innovation, using microarrays to explore disease mechanisms, identify genetic variations, and develop precision medicine approaches. The presence of skilled researchers, advanced laboratory infrastructure, and access to funding further strengthens their position. While pharmaceutical companies and diagnostic laboratories are expanding their usage, academic and research institutions continue to dominate due to their foundational role in scientific discovery and technology adoption.

Region-wise Insights

North America Microarrays Market Trends

North America is projected to capture 48.5% of global revenue in 2026, with the United States representing the largest contributor. The region’s leadership is supported by a highly advanced life sciences ecosystem, strong presence of leading biotechnology firms, and significant investment in genomics research. Federal funding programs and initiatives led by organizations such as the National Institutes of Health continue to accelerate innovation in molecular diagnostics and precision medicine. Microarrays are widely utilized across cancer research, pharmacogenomics, and biomarker discovery, ensuring consistent demand.

Additionally, the region benefits from well-established laboratory infrastructure, early adoption of advanced technologies, and strong collaboration between academia and industry. Pharmaceutical companies actively integrate microarrays into drug development pipelines, particularly for target identification and toxicity screening. Regulatory support and standardized research frameworks further enhance technology adoption. The growing emphasis on personalized healthcare and increasing clinical application of genomic tools are expected to sustain North America’s dominant position throughout the forecast period.

Europe Microarrays Market Trends

Europe represents a well-established yet steadily progressing market for microarrays, supported by robust public healthcare systems and strong research capabilities. Key countries including Germany, United Kingdom, France, Italy, and Spain contribute significantly to regional demand. The region’s growth is driven by increasing focus on genomic medicine, particularly in oncology and rare disease research. Government-backed initiatives and funding programs aimed at advancing molecular diagnostics are supporting widespread adoption of microarray technologies. Research institutions and universities across Europe actively utilize microarrays for gene expression studies and clinical investigations.

Additionally, the presence of established pharmaceutical companies enhances integration of these technologies into drug development workflows. Strict regulatory frameworks ensure high standards of quality and data accuracy, encouraging the use of validated microarray platforms. Although growth is comparatively moderate, continuous advancements in genomics research, coupled with increasing collaboration across European research networks, are expected to sustain stable market expansion in the coming years.

Asia Pacific Microarrays Market Trends

Asia Pacific is expected to witness the fastest growth, registering a CAGR of approximately 7.9% between 2026 and 2033. Countries such as China, India, Japan, and South Korea are driving regional expansion due to rapid advancements in healthcare infrastructure and increasing investment in biotechnology. The region is experiencing a surge in genomics research, supported by government initiatives promoting precision medicine and population-scale genetic studies. Academic institutions and research organizations are expanding their capabilities, leading to higher adoption of microarray platforms. Additionally, the growing pharmaceutical and biotechnology sectors are incorporating microarrays into drug discovery and clinical research processes.

Rising healthcare awareness, improving access to advanced diagnostic technologies, and increasing funding for life sciences research are further accelerating market growth. The expansion of contract research organizations and local manufacturing capabilities is also enhancing technology accessibility. With a large patient pool and increasing focus on personalized medicine, Asia Pacific is emerging as a key growth engine for the global microarrays market.

Competitive Landscape

The global microarrays market is highly competitive, with strong participation from companies such as Thermo Fisher Scientific Inc., Agilent Technologies, Inc., Illumina, Inc., Revvity, Inc., Bio-Rad Laboratories, Inc., and F. Hoffmann-La Roche Ltd. These players leverage advanced genomic technologies, strong bioinformatics capabilities, extensive product portfolios, and established collaborations with research institutes and biopharma firms. Competitive strategies focus on developing high-throughput, cost-efficient, and user-friendly microarray platforms, alongside investments in automation, data analytics, regulatory compliance, and global expansion to support growing demand in genomics research and clinical diagnostics.

Key Developments:

- In November 2025, WCC Biomedical announced a major breakthrough targeting the global pain relief market, highlighting advancements in its microarray-based microneedle patch (MAP) technology. The innovation focuses on enabling precise, painless, and efficient drug delivery, positioning the company to address a multi-billion-dollar market opportunity while improving therapeutic outcomes and patient compliance.

- In October 2025, Thermo Fisher Scientific Inc. launched the Applied Biosystems™ SwiftArrayStudio™ Microarray Analyzer, a platform engineered to enable rapid and scalable sample processing. Alongside this system, the company also introduced two new arrays—the Applied Biosystems Axiom™ PharmacoPro™ Array and the Applied Biosystems Axiom PangenomePro Array. The integrated solution streamlines four critical genotyping workflows into a single device, enhancing operational efficiency and simplifying microarray-based analysis.

- In August 2023, Thermo Fisher Scientific Inc. introduced a new chromosomal microarray, the Applied Biosystems™ CytoScan™ HD Accel array, aimed at enhancing productivity and efficiency in cytogenetics laboratories. The solution delivers an industry-leading two-day turnaround time and enables comprehensive whole-genome analysis, offering deeper insights into chromosomal variations across more than 5,000 clinically relevant regions for prenatal, postnatal, and oncology research applications.

- In July 2023, Arrayjet partnered with Chemspace to enhance and streamline its small molecule microarray (SMM) service portfolio. Through this collaboration, Chemspace’s extensively curated and well-annotated compound libraries have been integrated into Arrayjet’s SMM CRO/CMO offerings, strengthening capabilities in assay development, contract screening, and custom microarray manufacturing.

- In March 2023, Spectrum Solutions acquired Alimetrix, Inc. and Microarrays, Inc. to strengthen its integrated capabilities. This acquisition combines Alimetrix’s CLIA- and CAP-accredited molecular diagnostics expertise with Microarrays, Inc.’s proficiency in array-based product manufacturing, alongside Spectrum’s contract manufacturing and biospecimen collection services, creating a comprehensive end-to-end solutions portfolio.

Companies Covered in Microarrays Market

- Thermo Fisher Scientific Inc.

- Agilent Technologies, Inc.

- Illumina, Inc.

- Revvity, Inc.

- Bio-Rad Laboratories, Inc.

- F. Hoffmann-La Roche Ltd

- Merck KGaA

- Arrayit Corporation

- LC Sciences, LLC

- QIAGEN N.V.

- Molecular Devices, LLC

- Microarrays, Inc.

- Takara Bio Inc.

- CDI Laboratories, Inc.

- Phalanx Biotech Group, Inc.

- Others

Frequently Asked Questions

The global microarrays market is projected to be valued at US$ 4.8 Bn in 2026.

Rising adoption of genomics and precision medicine, increasing R&D funding, and expanding applications in cancer research and gene expression profiling drive the global microarrays market.

The global microarrays market is poised to witness a CAGR of 5.6 % between 2026 and 2033.

Growing clinical diagnostics adoption, emerging markets expansion, and integration with advanced technologies like AI and next-generation sequencing create key opportunities in the global microarrays market.

Thermo Fisher Scientific Inc., Agilent Technologies, Inc., Illumina, Inc., Revvity, Inc., Bio-Rad Laboratories, Inc., and F. Hoffmann-La Roche Ltd are some of the key players in the microarrays market.