- Technology

- Metaverse in Automotive Market

Metaverse in Automotive Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Metaverse in Automotive Market by Product Type (Hardware, Software, Services), Technology (Virtual Reality (VR), Augmented Reality (AR), Mixed Reality (MR), Extended Reality (XR), Non-Fungible Tokens (NFTs), Blockchain, Others), Application (Simulation, Design, & Prototyping, Virtual Showrooms, Marketing & Advertising, In-Vehicle Experiences, Remote Collaboration, Training & Maintenance, Others), and Regional Analysis for 2025 - 2032

Metaverse in Automotive Market Share and Trends Analysis

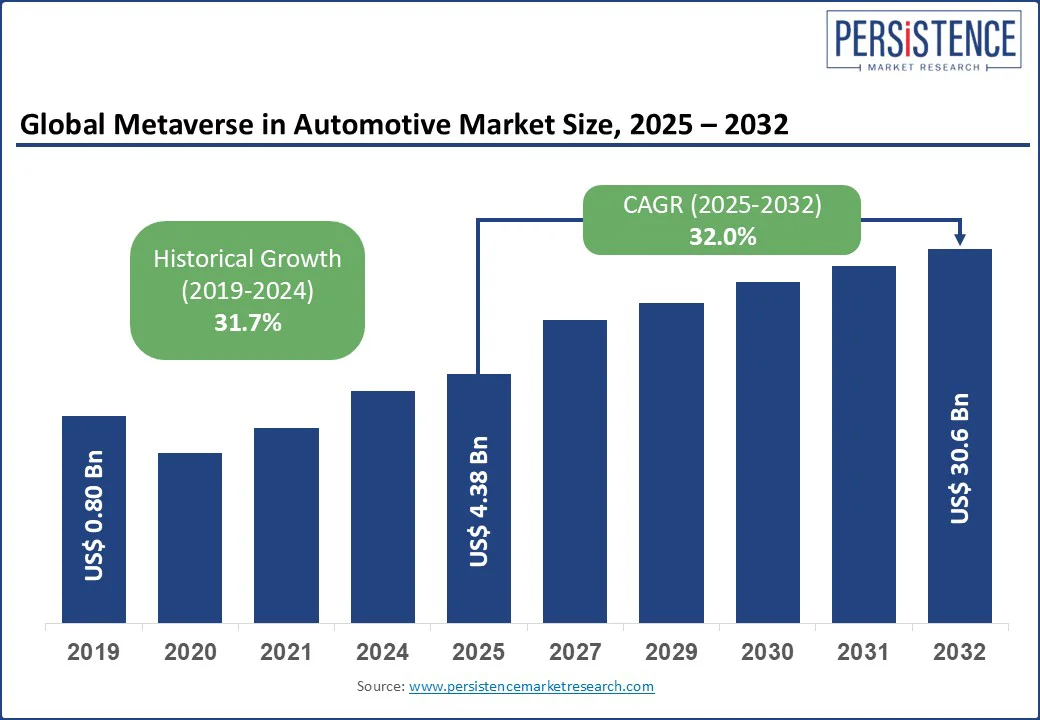

The global metaverse in automotive market size is likely to be valued at US$ 4.38 billion in 2025, and is estimated to reach US$ 30.6 billion by 2032, growing at a CAGR of 32.0% during the forecast period 2025-2032. Remote vehicle diagnostics via augmented reality (AR) tools, blockchain-backed automotive non-fungible tokens (NFTs) for digital ownership, and AI-integrated in-vehicle experiences are generating new monetization opportunities in this market.

As an immersive, persistent digital ecosystem integrating virtual reality (VR), augmented reality, blockchain, and real-time 3D content, the metaverse is bringing about an unprecedented transformation in how businesses engage, design, and deliver product and service experiences to their customers. In the automotive sector, this convergence is not just reinventing consumer interaction, but also redefining manufacturing, R&D, and retail strategies across the value chain.

The global metaverse in automotive market growth is aided by the adoption of digital twins for virtual prototyping, immersive training modules, and virtual showrooms by original equipment manufacturers (OEMs) to reduce overheads and improve market entry efficiency and timing of their offerings. For instance, BMW’s partnership with Nvidia to build a digital twin of its factory using Omniverse testifies to how metaverse platforms are enabling real-time collaboration in design and production. Meanwhile, brands such as Hyundai and MG Motor are pioneering metaverse-enabled customer engagement through virtual dealerships and immersive car-buying experiences, particularly targeting Gen Z buyers in APAC and North America.

Key Industry Highlights:

- The software sub-segment is projected to dominate the product type category in 2025, accounting for approximately 40% of the market revenue share, driven by the growing demand for immersive virtual showrooms and simulation tools.

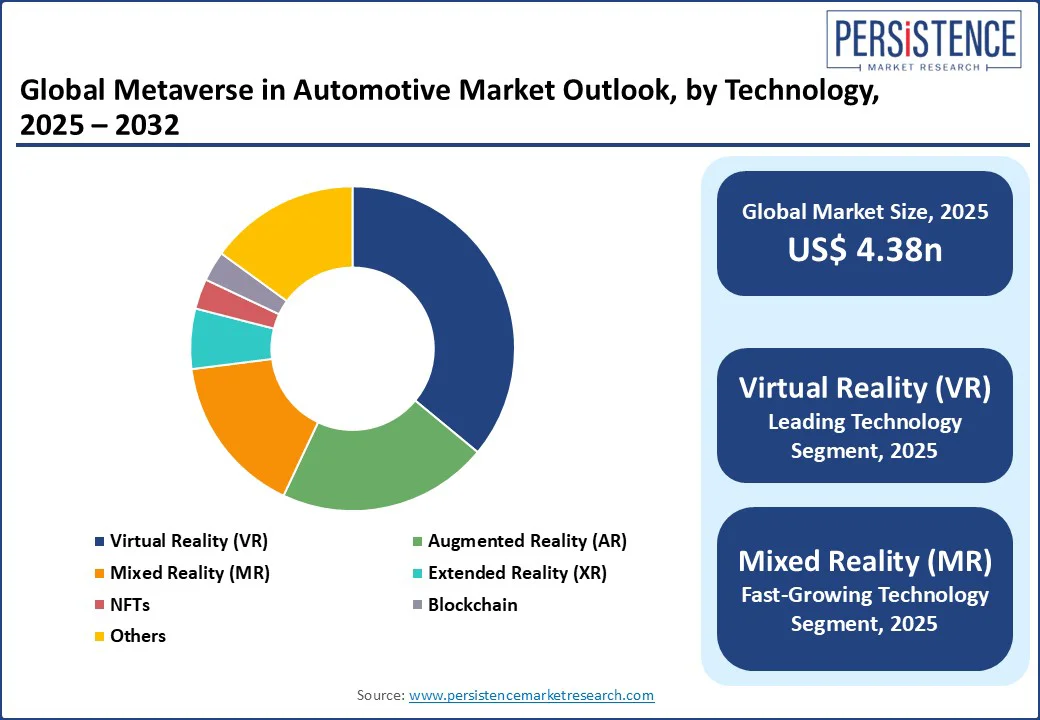

- Within the technology segment, virtual reality (VR) will hold a commanding position in 2025, securing around 36% of the revenue share due to its scalability across virtual showrooms, design prototyping, and training scenarios.

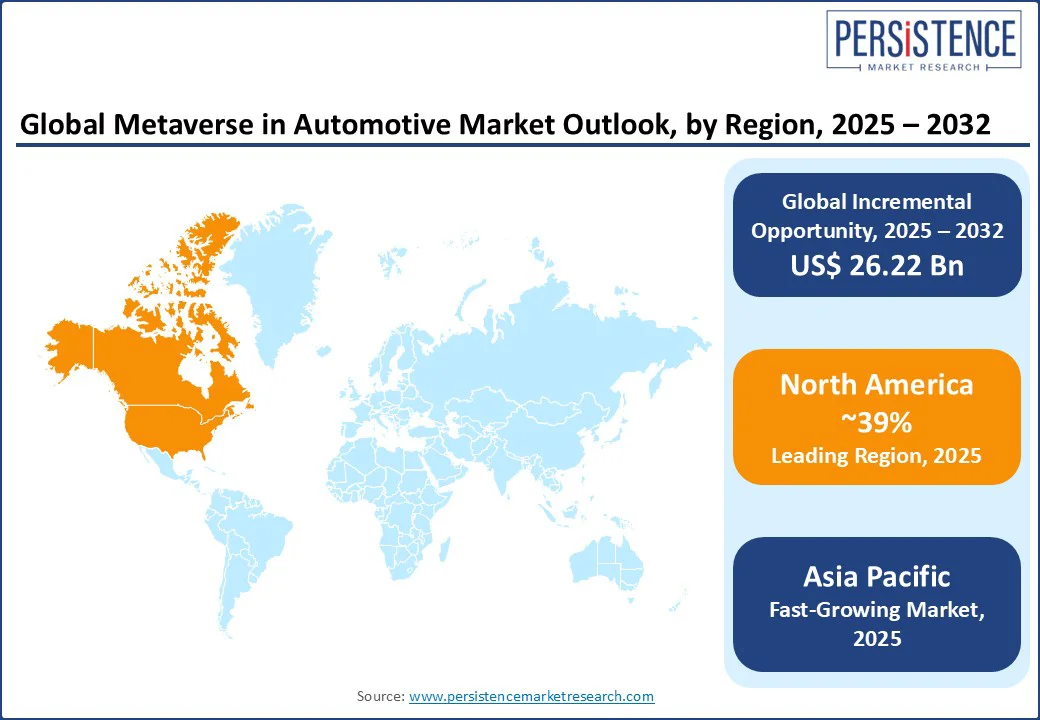

- Asia Pacific is poised to be the fastest-growing regional market during the forecast period 2025–2032, propelled by aggressive automotive digitization efforts in China, Japan, and South Korea.

- North America is expected to retain the largest regional share of 39% in 2025, powered by an early adoption of metaverse platforms by leading automakers such as Ford and Tesla.

- The discernible inclination for software-defined vehicles (SDVs) among consumers is pushing automakers to integrate AR/VR experiences, digital twins, and AI personalization into design and customer engagement.

- The widening application of digital twins for R&D and virtual prototyping by OEMs is accelerating the adoption of the metaverse in manufacturing workflows, reducing time-to-market, and enhancing cost efficiencies.

- The incorporation of AI and extended reality tools is resulting in the development of new monetization opportunities in vehicle sales, aftersales, and immersive brand storytelling.

- The competitive landscape of the metaverse in automotive market features a strong presence of automotive giants such as BMW, Hyundai, and GM, tech leaders such as Microsoft and NVIDIA, and mobility startups, investing heavily in simulation, cloud XR, and metaverse content creation platforms.

|

Global Market Attributes |

Key Insights |

|

Metaverse in Automotive Market Size (2025E) |

US$ 4.38 Bn |

|

Market Value Forecast (2032F) |

US$ 30.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

32.0% |

|

Historical Market Growth (CAGR 2019 to 2024) |

31.7% |

Market Dynamics

Driver - Increasing Deployment of Digital Twin Technology in Automotive R&D to Catalyze Metaverse Integration

An upcoming growth determinant for the metaverse in automotive market is the steadily expanding adoption of digital twin technology in R&D and production in the auto sector. As OEMs face mounting pressure to shorten development cycles and bring down prototyping costs, virtual replicas of vehicles, components, and manufacturing systems are enabling real-time simulation, collaboration, and iteration across global teams. For instance, BMW’s use of NVIDIA’s Omniverse platform to build a full-scale digital twin of its Regensburg plant has reportedly cut planning time by nearly 30% while improving design accuracy and enhancing worker training through immersive, synchronized virtual environments. This convergence of industrial metaverse platforms, simulation-driven design, and extended reality (XR) technologies is speedily transitioning from being an experimental tool to an indispensable component in the automotive industry.

The widening use of software-defined vehicles (SDVs) and the growing complexity of embedded electronics further amplify the integral role of digital twins, since traditional physical testing methods are proving to be increasingly inadequate in today’s day and age. By integrating AI-powered simulation engines, cloud-based collaborative design tools, and real-time data feeds into a unified virtual framework, automakers can not only optimize performance and safety parameters but also test UX features in the metaverse before launching their products.

Restraint - Fragmented Operability of Smart Technology Ecosystems to Stultify Market Growth

The acute lack of standardized, interoperable technology ecosystems across platforms, hardware, and simulation engines poses a major obstacle in the growth path of the metaverse in the automotive market. Unlike the traditional enterprise software space, the metaverse landscape is currently considered fragmented, marked by proprietary VR/AR devices, closed gaming engines, and siloed digital twin frameworks. These factors have significantly hampered cross-functional integration of metaverse systems in automotive use cases. For instance, while automakers such as Hyundai and Nissan are experimenting with virtual dealerships on platforms such as Zepeto or Roblox, these environments often fall short of the wherewithal necessary for industrial-grade fidelity and API compatibility to sync with enterprise-grade CAD/CAM systems, product lifecycle management (PLM) software, or real-time vehicle telemetry, which are the most essential tools in design, testing, and digital manufacturing.

This technological disjunction makes scalability, data portability, and cybersecurity challenging, impacting full-scale metaverse adoption a high-friction process for OEMs and Tier 1 suppliers. The absence of universally accepted XR standards, including those that are still evolving under OpenXR and Metaverse Standards Forum, means that integrating a VR-based showroom with a blockchain-based vehicle ownership layer or a digital twin simulation with AR-guided maintenance will require custom middleware and significant developer overhead. Consequently, promising pilots often get stalled way before they can be deployed enterprise-wide, diminishing the return on investment (ROI) and dampening investor confidence.

Opportunity - Immersive Commerce in Virtual Showrooms to be the Next Frontier for Automotive Retail

Probably the most lucrative opportunity in the metaverse in automotive market lies in the transformation of automotive retail through immersive commerce and virtual showrooms, particularly as tech-savvy consumers demand richer, frictionless buying experiences. According to Accenture, nearly 72% of car buyers under 40 prefer a hybrid or fully digital purchase journey. More importantly, automakers are responding with full force to these changing preferences. MG Motor India’s “MGVerse” and Hyundai’s “Mobility Adventure” on Roblox are apt examples of how virtual environments are evolving from marketing novelties into pragmatic, transactional platforms. These extended reality spaces combine blockchain-secured digital identities, NFT-based loyalty programs, and AI-guided assistants to replicate and enhance the physical dealership model.

An even more crucial consideration is that these platforms enable OEMs to collect high-value behavioral data, personalize offerings, and reduce customer acquisition costs by a significant margin by eliminating real estate and inventory constraints. As Web3 and edge computing infrastructure mature, automotive e-commerce in the metaverse could generate billions in new revenue streams, especially in fast-growing markets such as India, Brazil, and the UAE, where physical dealership coverage is sparse, but smartphone and XR adoption is accelerating.

Category-wise Analysis

Technology Insights

Virtual reality (VR) is expected to be the leading technology sub-segment in 2025, capturing roughly 36% market revenue share. The apex position of VR is primarily attributed to its scalability across virtual showrooms, design prototyping, and training scenarios. For example, BMW and Ford have been widening the use of VR platforms such as NVIDIA’s Omniverse and Gravity Sketch to simulate vehicle manufacturing workflows and decode ergonomic performance before physical assembly, cutting planning time by 30% and boosting the quality and efficiency of innovation, as per an analysis by McKinsey & Company. This association is deepening immersive customer engagement and catalyzing simulation-driven R&D, cementing VR as the primary metaverse enabler for automotive OEMs.

On the other hand, mixed reality (MR) is anticipated to be the fastest-growing sub-segment through 2032, as the convergence of virtual overlays with physical reality facilitates real-time diagnostics, AR-guided maintenance, and collaborative design functions across enterprise environments. Mixed reality heads-up display (HUD) systems, such as those engineered by WayRay and Raythink, superimpose navigation cues, hazard alerts, and maintenance guidance directly into the user's field-of-view, supporting not just drivers and vehicle occupants but also dealer mechanics with real-time insights. Apart from this, MR also aids collaborative virtual factory layouts where design teams can apply design changes, overlay interactive annotations, and conduct live ergonomics evaluations, even across continents.

Product Type Insights

The software sub-segment is estimated to hold the largest revenue share of nearly 40% in the product segment in 2025. Software platforms are the key to building the most immersive metaverse experiences, powering simulation and modeling, virtual showroom platforms, and AR/VR applications for both customers and engineers. OEMs such as BMW and Hyundai are already leveraging platforms built atop Unity or Unreal Engine and Nvidia’s Omniverse to run real-time digital twins, speeding up virtual prototyping and team collaboration. The result is that design iterations have shorter turnarounds, physical prototyping costs are drastically reduced, and production planning in the automotive R&D pipeline is well-optimized. The increasing demand for simulation-driven design, interactive 3D user interfaces, and UI/UX enhancements is in line with the upsurge in software engagements across the value chain.

Services in the form of metaverse consulting, content development, integration, and analytics are quickly becoming the sub-segment exhibiting the most promising growth. With automakers constantly grappling with interoperability issues across VR/AR headsets, CAD/PLM systems, and blockchain identity layers, the reliance of the auto industry on bespoke consulting solutions to build coherent metaverse strategies is rising at a considerable pace. Similarly, companies such as Holoride and WayRay are partnering with Tier-1 integrators to deliver tailor-made AR HUD content and XR-based training modules in dealerships and service centers. This trend in the services category is offering new value propositions in content creation, training, and experience personalization, while also enabling scalable deployment of metaverse use cases for OEMs and suppliers.

Regional Insights

North America Metaverse in Automotive Market Trends

With an expected metaverse in automotive market share of around 39%, North America is set to be the leading region. The market here is anchored by software innovations in AR, VR, and XR spearheaded by Silicon Valley's tech giants such as Meta Platforms, NVIDIA, and Unity Technologies. Advanced digital infrastructure, abundant R&D investment, and early-adopter consumers are the factors augmenting the deployments of immersive technologies across OEMs, from virtual showrooms to AI-guided design prototyping. For instance, Acura’s virtual showroom in Decentraland and manufacturer-led digital twin pilots illustrate the massive gains that await players in the metaverse space. This ecosystem has ensured the expanded adoption of metaverse solutions across both B2B and B2C verticals in the region. Even though the region faces a plateauing growth trajectory due to a saturating market, robust regulatory frameworks supportive of IP and data protection, combined with high digital literacy, are still encouraging companies to innovate with confidence.

Asia Pacific Metaverse in Automotive Market Trends

Asia Pacific is envisaged to be the fastest-growing regional market for metaverse in automotive, projected to showcase a staggering CAGR of approximately 35% through 2032. Consumers in the region have shown high receptivity to virtual showrooms, AR-guided EV configurators, and immersive marketing underpinned by the rapid uptake of electric vehicles. For example, Maruti Suzuki’s ARENAVerse in India and Raythink’s AR-HUD rollout in China highlight the high pace of innovation in immersive design, interactive test drives, and real-time user engagement before the delivery of vehicles. Supplementing these developments are government-led initiatives, such as India’s Digital India and smart manufacturing policies in China, which are fueling the adoption of cutting-edge digital technologies across industries, benefiting the metaverse in automotive market.

Europe Metaverse in Automotive Market Trends

Europe as a market is making substantial contributions through sustainability-aligned metaverse use cases and enterprise-grade deployments. Being home to automotive giants such as Volkswagen, BMW, and McLaren, the regional market sits in a favorable environment owing to the steadily rising deployment platforms that mix NFT-based loyalty programs, blockchain-secured virtual showrooms, and compliant digital twin systems focused on emissions tracking. A notable example is Fiat’s metaverse store initiative, which was initially launched in Italy and then expanded to France and the U.K., which is reflective of Europe’s auto OEMs’ focus on tailored, high-fidelity experiences that mesh with strict vehicular safety standards and carbon emission regulations of the European Union (EU). For companies to succeed in Europe, metaverse applications must have interoperability functionalities with vehicle compliance systems and must also strictly adhere to eco-design frameworks.

Competitive Landscape

In the dynamic competitive landscape of the global metaverse in automotive market, the most essential drivers are rooted in the confluence of strategic partnerships and software platform dominance. Leading software-platform providers such as NVIDIA and Roblox have entrenched their position by joining forces with OEMs for digital twin platforms and simulation and virtual showroom solutions. For example, when BMW integrated NVIDIA’s Omniverse platform across its facilities globally, it enabled virtual factory commissioning and immersive design prototyping, reducing production planning cycles by up to 30%. The growing symbiotic relationship between software providers and automakers has elevated innovation in immersive 3D UX, AI-powered simulation, and metaverse-enabled marketing.

Another promising area is the rising wave of specialist XR and metaverse startups, including Holoride, Metadome.ai, and StradVision, is intensifying competition through bespoke AR/VR services, in-car entertainment, and photorealistic virtual brand experiences. For instance, Metadome.ai’s creation of MGVerse for MG Motor involves hyper-realistic 3D configurators, avatar zones, and virtual test drives, unifying cloud XR and AI for enhanced customer engagement The entry and the subsequent proliferation of niche innovators are actively promoting innovation in virtual dealership, in-vehicle XR, and experiential service layers.

Key Industry Developments

- In June 2025, Toyota Motor Corporation partnered with Unity Technologies to develop the graphical user interface (GUI) for its next-generation in-car Human Machine Interface (HMI). Leveraging Unity's real-time 3D technology, this collaboration aims to enhance the in-car experience by creating advanced digital cockpits that connect drivers, vehicles, and society. Unity’s platform helps Toyota streamline the entire HMI development process by minimizing rework, optimizing workflows, and improving data management, enabling faster and more efficient creation of high-performance, stable user interfaces.

- In June 2025, Mercedes-Benz entered into a partnership with NVIDIA to create digital twins of its real-life factories using NVIDIA’s Omniverse platform. These digital twins are virtual, metaverse-esque 3D replicas of physical manufacturing plants that will empower Mercedes to plan, design, and optimize factory layouts and production workflows virtually before making costly physical changes. The initiative is part of Mercedes-Benz’s broader MO360 digital production ecosystem, linking around 30 plants worldwide with real-time data to increase flexibility and scalability in manufacturing.

- In April 2025, Audi and Siemens teamed up to implement the world's first virtual programmable logic controllers (PLCs) with safety functions, which replace traditional hardware controllers with software-based automation running on a cloud platform called Edge Cloud 4 Production (EC4P). This move is seen as enabling centralized, flexible, and highly scalable control of manufacturing processes remotely, vastly improving agility, efficiency, and security on the shop floor. The virtual PLCs allow for rapid deployment, configuration, and maintenance across many controllers simultaneously, reducing downtime and administrative overhead.

Companies Covered in Metaverse in Automotive Market

- NVIDIA Corporation

- Microsoft Corporation

- Roblox Corporation

- Unity Technologies

- Meta Platforms, Inc.

- BMW Group

- Mercedes‑Benz Group AG

- Toyota Motor Corporation

- Ford Motor Company

- General Motors Company

- Hyundai Motor Company

- Nissan Motor Co., Ltd.

- Honda Motor Co., Ltd.

- Stellantis N.V.

- Volvo Car AB

- Eccentric Engine (Metadome.ai)

- holoride GmbH

- StradVision, Inc.

- Varjo Technologies Oy

Frequently Asked Questions

The metaverse in automotive market is projected to reach US$ 4.38 billion in 2025.

The increase in the adoption of digital twins for virtual prototyping, immersive training modules, and virtual showrooms by auto OEMs is driving the market.

The metaverse in automotive market is poised to witness a CAGR of 32.0% from 2025 to 2032.

The transformation of automotive retail through immersive commerce and the expansion of extended reality spaces across car showrooms are key market opportunities.

NVIDIA Corporation, Roblox Corporation, and Meta Platforms are a few key market players.