- Semiconductor Materials & Components

- Metamaterials Market

Metamaterials Market Size, Share, and Growth Forecast, 2026 – 2033

Metamaterials Market by Product Type (Electromagnetic, Terahertz, Photonic), Technology Type (Passive Metamaterials, Others), Frequency Band (Radio Frequency, Others), End-user Industry (Aerospace & Defense, Others), and Regional Analysis 2026 – 2033

Metamaterials Market Size and Trends Analysis

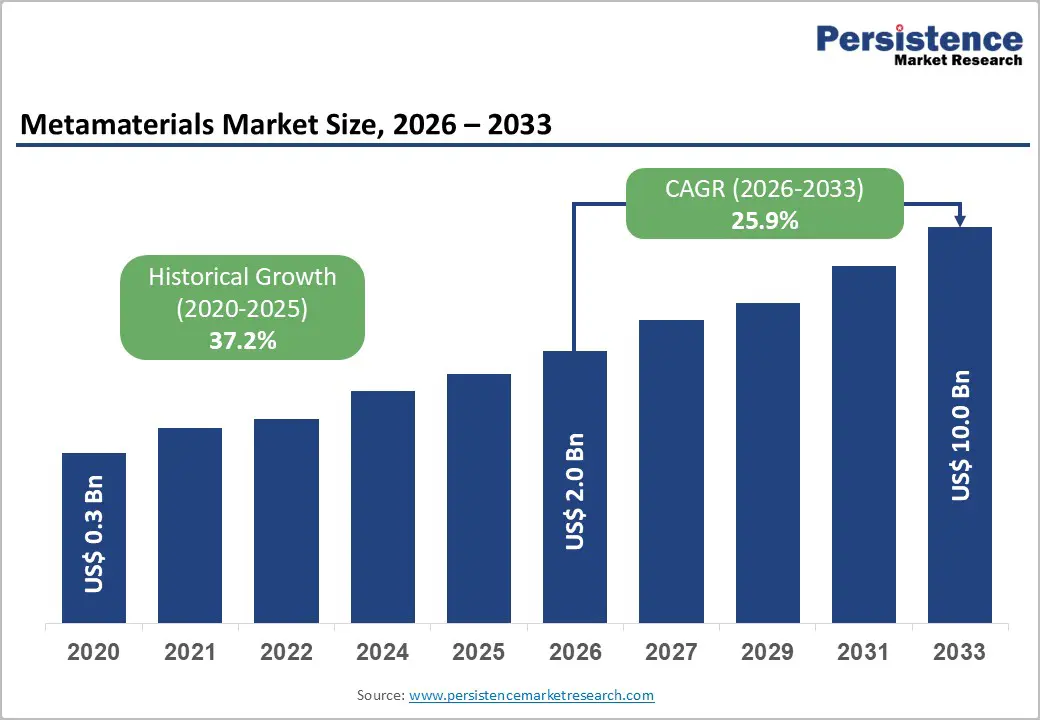

The global metamaterials market size is likely to be valued at US$2.0 billion in 2026 and is expected to reach US$10.0 billion by 2033, growing at a CAGR of 25.9% during the forecast period from 2026 to 2033, driven by increasing demand in sectors such as 5G/6G telecommunications and aerospace radar systems, where metamaterials are enabling compact antennas with advanced beam steering capabilities. Advancements in nanotechnology are enhancing scalable production, while significant defense investments are fueling market expansion. The integration of artificial intelligence with materials science is also improving the design of meta-surfaces, allowing for the manipulation of electromagnetic waves with exceptional precision.

Key Industry Highlights:

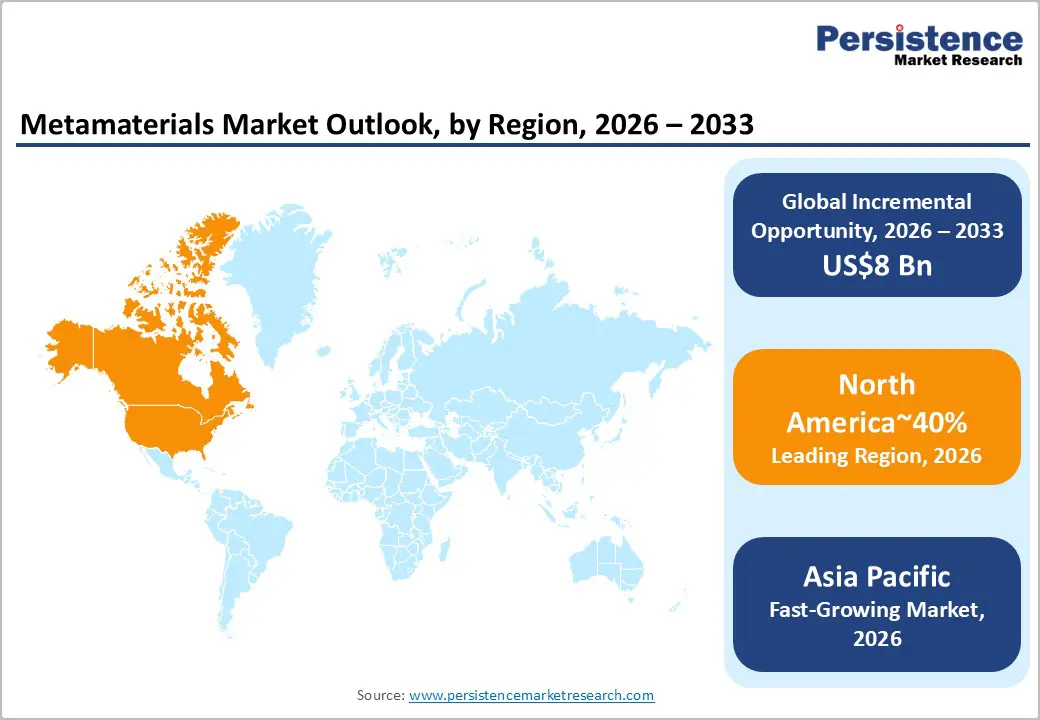

- Leading Region: North America is anticipated to lead with approximately 40% share, supported by strong defense R&D spending, early commercialization of advanced antenna technologies, and a dense ecosystem of metamaterials startups and research institutions.

- Fastest-growing Region: Asia Pacific is expected to be the fastest-growing region, driven by rapid 5G rollout, aggressive 6G research programs, expanding semiconductor and advanced materials manufacturing capacity, and strong government-backed investments in next-generation communications infrastructure.

- Leading Technology Type: Passive metamaterials are expected to remain the leading technology type, accounting for around 72% share, due to their relative maturity, lower cost, and broad deployment across RF and microwave applications.

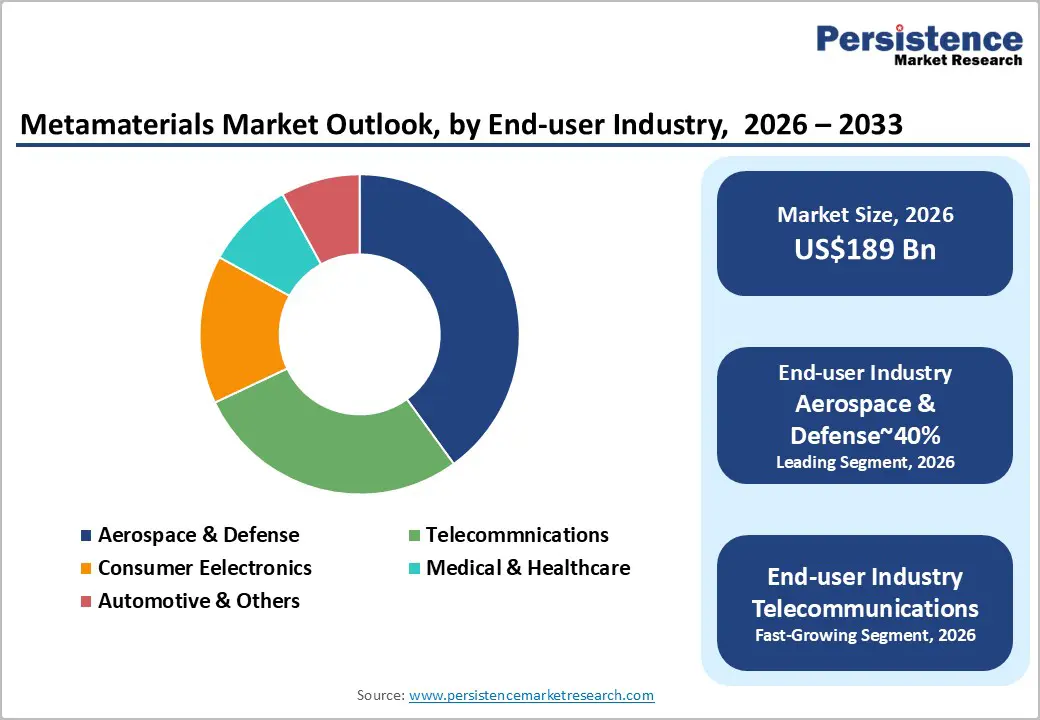

- Leading End-user Industry: Aerospace and defense are anticipated to remain the leading end-user industry, holding around 40% share, driven by sustained investments in advanced radar, electronic warfare, stealth platforms, and sensing technologies that benefit from metamaterial-enabled performance gains.

| Key Insights | Details |

|---|---|

|

Metamaterials Market Size (2026E) |

US$2.0 Bn |

|

Market Value Forecast (2033F) |

US$10.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

25.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

37.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Advanced Communications, Defense Stealth, and Device Miniaturization

The market is driven by applications that push beyond the physical limitations of traditional materials, especially in high-speed communications, defense modernization, and device miniaturization. In 5G and emerging 6G networks, higher-frequency bands face attenuation and line-of-sight issues, which metamaterial-enabled Reconfigurable Intelligent Surfaces and holographic beamforming antennas help overcome by shaping electromagnetic wave propagation. This enhances link reliability in urban areas and supports efficient connectivity for LEO satellites and HAPS platforms.

As networks move to terahertz frequencies in 6G, conventional silicon components struggle, while metamaterial structures enable wave filtering and control at sub-wavelength scales, becoming vital for next-gen wireless and satellite communications. In defense, tunable radar-absorbent metamaterials enhance stealth, while in sensing, metamaterials improve MRI resolution and biosensor sensitivity. In February 2025, Pivotal Commware introduced the Spotlight mmWave FWA Qualifier and Cyclops RF Scanner to optimize holographic beamforming deployments.

Nanotechnology and Photonics Convergence

The convergence of nanotechnology and photonics is a key factor driving the transition of metamaterials from experimental concepts to scalable commercial components. Traditional optics rely on bulk refraction through glass, limiting size, weight, and aberration control. In contrast, nanophotonic metamaterials manipulate light at sub-wavelength scales, enabling precise control of phase, amplitude, and polarization via patterned meta-atoms on semiconductor substrates.

Advances in nanofabrication techniques, such as electron-beam and nanoimprint lithography, have made it possible to produce meta-surfaces on silicon wafers, aligning metamaterial manufacturing with CMOS processes. This breakthrough enables the commercialization of flat optics, dramatically reducing optical stack thickness and mass while enhancing imaging performance. The resulting impact is significant in industries such as consumer electronics, sensing, and compact imaging systems. Further advancements in photonics are pushing the boundaries of conventional optics, allowing for super-resolution and engineered refractive responses. These capabilities are crucial for semiconductor inspection, advanced lithography, and high-precision imaging. In November 2025, Metalenz and UMC will begin mass production of Polar ID, a meta-surface-based face authentication system for smartphones, bringing payment-grade security to compact devices.

Barrier Analysis – Technological Maturity and Standardization Gaps

The market faces significant challenges due to the gap between laboratory-grade performance and industrial-scale manufacturability. Achieving the required functional performance depends on sub-wavelength meta-atoms with nanometer-level precision, where even small deviations in manufacturing can degrade electromagnetic response, impacting yield in high-volume production. Current processes risk defects and tooling degradation, driving up costs and limiting applications to defense, aerospace, and premium electronics. Durability issues under thermal cycling, ultraviolet exposure, and mechanical stress hinder adoption in automotive, telecom, and long-lifecycle infrastructure, extending validation timelines.

Market adoption is also slowed by the lack of unified performance standards, test protocols, and interoperable design libraries, which, combined with the narrowband nature of many metamaterial designs, restrict deployment to niche, single-frequency applications. In April 2025, MIT engineers developed a new 3D printing method for stretchable synthetic metamaterials, aiming to overcome high fabrication costs and enable scalable, flexible additive manufacturing for broader applications in textiles and semiconductors.

Opportunity Analysis - Integration into Autonomous Vehicle Sensors

The automotive sensing stack is shifting from mechanical LiDAR and bulky phased-array radar to solid-state, software-defined systems, opening opportunities for metamaterial-enabled optics and antennas. Meta-surface beam steering and flat metalenses can replace rotating mirrors and gimbals, reducing size, weight, power consumption, and failure points in LiDAR, radar, and V2X sensors. This aligns with OEM goals for sensor miniaturization, aerodynamic integration, and cost reduction, enabling tight packaging in body panels, headlamps, and bumpers without sacrificing field of view or angular resolution.

For Level 4 and Level 5 autonomy, metamaterials support higher channel density and reconfigurable beam patterns, enhancing object detection in adverse conditions. The shift towards platformized sensor architectures and centralized compute in the automotive industry boosts demand for standardized, tunable components. Suppliers offering automotive-grade meta-surfaces with validated durability and scalability are positioned to capture significant market share as autonomous content per vehicle grows. In June 2025, Greenerwave opened a new hub in Toulouse to accelerate satellite communication and automotive sensor innovations.

Active (Tunable) Metamaterials and AI-Defined Surfaces

The convergence of active metamaterials with AI-driven control systems is driving commercialization in the market, transforming the value proposition from static enhancements to software-defined electromagnetic functionality. Unlike passive meta-structures, active meta-surfaces use tunable media such as liquid crystals and MEMS to enable real-time wavefront reconfiguration across RF, mmWave, THz, and optical bands. For OEMs and operators, the economic benefits are clear: software-defined surfaces can replace costly densification in urban networks, while solid-state beam steering improves reliability, reduces wear, and cuts sensor costs in automotive perception systems.

The emerging focus on cognitive metamaterials combines embedded sensing with AI for closed-loop optimization at the physical layer. Suppliers offering automotive- and telco-grade active meta-surfaces with thermal stability and scalable fabrication will capture significant market share. In October 2025, Echodyne launched EchoWare, a software platform to manage MESA radar networks, streamlining radar integration into command-and-control systems with metamaterial hardware.

Category–wise Analysis

Technology Type Insights

Passive metamaterials represent the leading technology segment, accounting for approximately 70% of deployed volumes, with leadership expected to remain stable across the forecast horizon. This segment is anticipated to retain dominance due to proven manufacturability, predictable performance under extreme environmental stress, and scalability across consumer electronics, aerospace platforms, and built infrastructure.

Passive metalens integration into depth sensing and imaging modules is expected to accelerate adoption in compact consumer devices, driven by the replacement of bulky refractive optics with flat, lightweight nanostructured films. Asia Pacific manufacturing scale and North American defense programs are likely to anchor volume demand, supported by building energy performance mandates and aviation certification pathways that favor low-power, maintenance-light materials.

Active/Tunable Metamaterials are anticipated to be the fastest-growing technology segment, driven by rising requirements for real-time adaptability across telecommunications, mobility platforms, and intelligent sensing architectures. Software-defined metasurfaces are likely to become foundational to 6G network design, where dynamic beam steering, interference mitigation, and terahertz signal conditioning cannot be addressed through static materials.

In mobility and defense applications, tunable electromagnetic skins are anticipated to support adaptive signature management, satellite on the move connectivity, and electronic countermeasure agility, reinforcing demand for liquid crystal and phase change material architectures. Supply chain localization around controller ICs and advanced materials processing is expected to shape regional deployment patterns, with Europe and India likely to emerge as critical production hubs for programmable surface platforms as standards alignment and spectrum sharing frameworks mature.

End-user Industry Insights

Aerospace and defense are anticipated to represent the leading technology segment, accounting for approximately 40%of overall technology deployment. This leadership is expected to remain durable as defense platforms increasingly transition from passive electromagnetic structures toward active, software-controlled metasurfaces embedded directly into airframes, randoms, and sensor arrays.

Key defense integrators are anticipated to deepen vertical integration of metamaterial-enabled antennas, radars, and smart skins into platform upgrades and new air dominance architectures, while North America is likely to retain technological leadership due to sustained defense R&D intensity and controlled access to high-performance electromagnetic materials.

The telecommunications segment is anticipated to be the fastest-growing technology, driven by network densification, early 6G testbeds, and the migration toward reconfigurable intelligent surfaces embedded into urban infrastructure. Technology roadmaps increasingly position AI-managed cognitive surfaces as part of the physical layer, enabling real-time beam adaptation based on user density and interference patterns.

Asia Pacific is expected to emerge as the fastest expanding deployment region for telecom-focused metamaterials due to aggressive 5G Advanced rollouts, early 6G field trials, and dense urban connectivity requirements across China, Japan, South Korea, and India.

Regional Insights

North America Metamaterials Market Trends

North America is expected to remain the leading region, accounting for approximately 40% of global market share in 2026, supported by early industrialization of advanced materials manufacturing and dense linkages between defense laboratories and commercial producers. Demand is anticipated to remain structurally reinforced by defense modernization priorities, increasing deployment of low-profile high-gain antennas, and growing interest in terahertz applications for sensing and high-speed communications. National security-oriented sourcing mandates and “Buy American” procurement preferences are expected to strengthen domestic manufacturing incentives for metamaterial-enabled components, particularly within defense, aerospace, and critical communications infrastructure.

Tariff imposition on imported electronics, semiconductors, and metal inputs is likely to increase near-term production costs for OEMs and integrators, introducing margin pressure and procurement volatility for complex RF systems and satellite terminals. The U.S. is expected to anchor regional performance through concentration of high-value defense programmers, leadership in 5G densification, and sustained federal funding for advanced materials research.

Technological updates are likely to prioritize terahertz architectures, adaptive meta-surfaces, and scalable fabrication techniques compatible with semiconductor manufacturing flows, supporting broader diffusion beyond defense into telecom infrastructure, automotive sensing, and advanced industrial communications.

Europe Metamaterials Market Trends

Europe is positioned as a stable R&D and standards-setting anchor, underpinned by regulatory leadership, coordinated public funding, and a policy-driven pivot toward sovereign deep-tech capabilities. Defense and aerospace programs are integrating meta-surfaces into next-generation fighter platforms, while telecom stakeholders are advancing RIS architectures aligned with 6G roadmaps. The introduction of carbon-accountability mechanisms and early governance of AI-controlled active metamaterials is establishing European products as compliance-led benchmarks, strengthening export credibility in regulated markets, and reinforcing Europe’s role as a technology standard-setter rather than a pure volume manufacturer.

External trade dynamics are reshaping Europe’s supply-chain geometry and market posture. Elevated tariffs on transatlantic flows have compressed margins on precision components and RF subsystems, incentivising a stronger “Buy European” procurement bias and accelerating strategic autonomy objectives across semiconductors, photonics, and advanced materials. This corridor is improving cost competitiveness, diversifying away from China-centric production risk, and positioning Europe to offset protectionist headwinds through preferential access to a large testbed market for 6G-aligned deployments.

Asia Pacific Metamaterials Market Trends

Asia Pacific is expected to remain the fastest-growing metamaterials region, having shifted from a research-centric base into the world’s primary high-volume manufacturing engine. The transition is supported by a deepening industrial stack that spans defense-grade electromagnetic designs, tunable components for automotive sensing, and meta-lens integration for smartphones, where weight, form factor, and bill-of-materials pressures favor meta-surface architectures over conventional optics. APAC’s early push into terahertz testbeds is expected to sustain demand for advanced wave-control platforms as silicon approaches physical limits, while electric vehicle platforms continue to prioritize acoustic comfort solutions that rely on engineered lattices rather than passive insulation.

Within this landscape, India and China are positioned to anchor distinct but complementary roles. China is likely to remain concentrated on consolidated, high-volume output for government infrastructure and defense-adjacent applications, even as access to certain foreign markets stays constrained by trade measures and technology controls. India, by contrast, is expected to accelerate as an alternative manufacturing and systems-integration hub, particularly for telecom-facing platforms and scalable meta-optics, supported by duty-free industrial cooperation with Europe under the India–EU framework. At the same time, retaliatory pressures on foreign simulation tools are likely to continue pushing regional firms to invest in domestic design software, tightening vertical integration from modeling to fabrication.

Competitive Landscape

The global metamaterials market is moderately fragmented, with influence split between large aerospace and defense contractors such as Lockheed Martin, Raytheon, and Northrop Grumman, and specialized technology leaders including Kymeta, Echodyne, and Metalenz. The incumbents matter because they embed metamaterials into mission-critical defense and electronic warfare systems, anchoring high-value demand and long development cycles. Competitive positioning centers on intellectual property ownership, fabrication know-how, and access to scalable manufacturing. Leaders pursue aggressive patent strategies to protect unit-cell designs and production methods, while startups increasingly rely on foundry partnerships with major semiconductor manufacturers to achieve scale.

Key Industry Highlights:

- In February 2026, Kymeta and Japan Display Inc. (JDI) signed a master supply agreement to produce next-gen multi-band meta-surface apertures, enabling concurrent Ku/Ka-band operations. This partnership accelerates manufacturing, cuts costs, and fast-tracks the commercialization of advanced satellite terminals.

- In November 2025, Echodyne's MESA radar achieved 100% success in the Red Sands 2025 Exercise, where its EchoShield radar tracked drones with perfect accuracy during the U.S.-Saudi counter-UAS exercise. This validation in real defense operations boosts confidence in metamaterial radars for surveillance and security, spurring adoption in the radar and aerospace sectors.

- In May 2025, Kymeta and Eutelsat OneWeb launched the Goshawk U8, a hybrid flat-panel terminal for government and military multi-orbit use. Leveraging LEO, GEO, and cellular networks, it enhanced sovereign SATCOM capabilities amid growing global defense demands.

Companies Covered in Metamaterials Market

- Kymeta Corporation

- Echodyne Corp

- Meta Materials Inc.

- Metalenz

- Kuang-Chi Technologies

- Greenerwave

- Pivotal Commware

- Fractal Antenna Systems

- Multiwave Technologies

- JEM Engineering

- Teraview

- Anywaves

- Lockheed Martin

- Raytheon Technologies

- Northrop Grumman

- BAE Systems

Frequently Asked Questions

The global metamaterials market is projected to be valued at US$2.0 billion in 2026 and is expected to reach US$10.0 billion by 2033, driven by demand in 5G/6G telecommunications, aerospace radar, and advancements in nanotechnology.

The deployment of 5G, 6G, and satellite communications creates a fundamental need for metamaterials, as they enable compact, high-performance antennas, reconfigurable intelligent surfaces (RIS), and precise beam steering to overcome propagation losses and improve network efficiency where conventional materials fall short.

The metamaterials market is forecast to grow at a CAGR of 25.9% from 2026 to 2033, reflecting rapid adoption across defense, telecommunications, and consumer electronics.

Asia Pacific is the fastest-growing regional market, fueled by rapid 5G rollout, aggressive 6G research, expanding semiconductor manufacturing, and strong government investments in next-generation communications infrastructure.

The metamaterials market is moderately fragmented, with key players including Kymeta Corporation, Echodyne Corp., Meta Materials Inc., Metalenz, and Lockheed Martin. Competition is split between specialized technology innovators and large aerospace & defense contractors integrating metamaterials into high-value systems.