- Non-food Packaging

- Medical Device Packaging Materials Market

Medical Device Packaging Materials Market Size, Share, and Growth Forecast, 2026 - 2033

Medical Device Packaging Materials Market by Material (Plastics, Polyethylene Fibers/LDPE, Others), Packaging Type (Plastic Films, Trays & Blisters, Others), Sterility Application, Device Category, and Regional Analysis for 2026 - 2033

Medical Device Packaging Materials Market Size and Trends Analysis

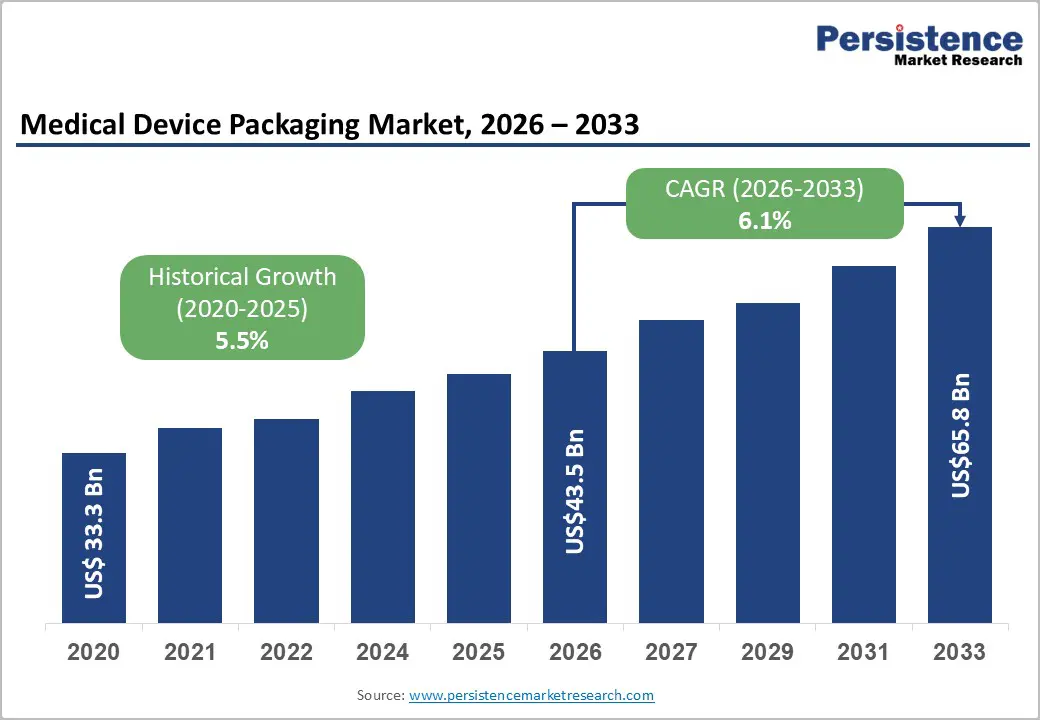

The global medical device packaging materials market size is likely to be valued at US$43.5 billion in 2026 and is expected to reach US$65.8 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033, driven by heightened regulatory focus on sterile barrier integrity and labeling compliance across key healthcare systems, along with increasing demand for medical devices fueled by aging populations and the rising prevalence of chronic diseases.

Additionally, the continued expansion of medical device manufacturing, particularly in the Asia Pacific region, is boosting the need for validated, high-performance packaging materials.

Key Industry Highlights

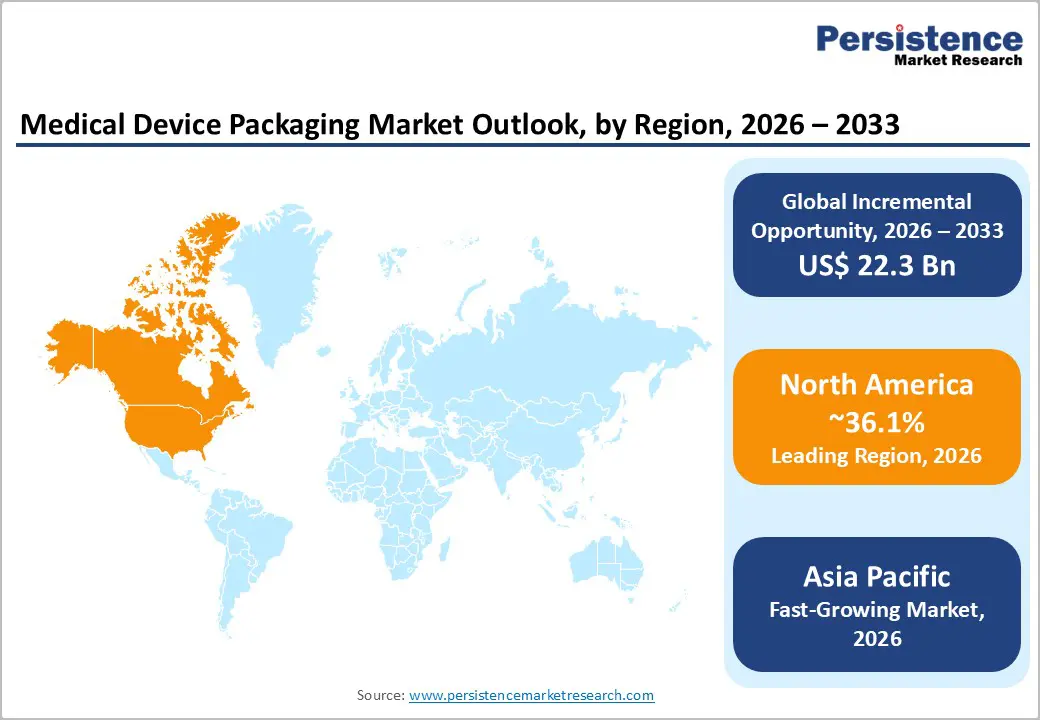

- Leading Region: North America is projected to account for approximately 36.1% of the market share, driven by strong regulatory frameworks, advanced healthcare infrastructure, and high medical device production.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, supported by rapid industrialization, increasing healthcare investments, and expanding domestic manufacturing.

- Investment Plans: Significant investments are being directed toward regional manufacturing expansion and technical development centers, particularly in Asia Pacific and North America, to enhance supply chain resilience and meet rising demand for sterile packaging solutions.

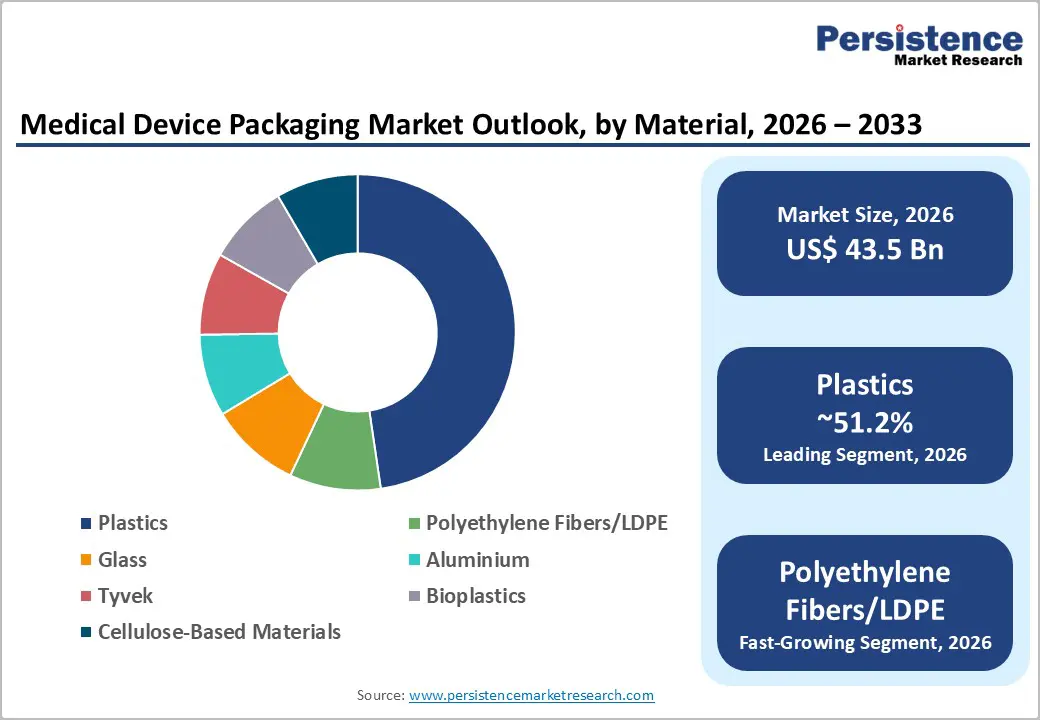

- Dominant Material: Plastics are anticipated to hold over 51.2% market share, due to their versatility, cost efficiency, and compatibility with various sterilization methods.

- Leading Packaging Type: Plastic films are estimated to capture approximately 37.4% of market share, driven by their adaptability, barrier properties, and suitability for high-volume medical packaging applications.

| Key Insights | Details |

|---|---|

| Medical Device Packaging Materials Market Size (2026E) | US$43.5 Bn |

| Market Value Forecast (2033F) | US$65.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5% |

DRO Analysis

Driver Analysis - Stringent Sterility and Regulatory Compliance Requirements Driving Material Innovation

Regulatory frameworks governing medical device packaging are becoming increasingly stringent, particularly in the U.S. and Europe. Standards for terminally sterilized medical devices require validated sterile barrier systems, material compatibility, and robust sealing processes. Unique Device Identification (UDI) requirements mandate traceability at multiple packaging levels, reinforcing the need for durable printing surfaces and tamper-evident designs. These requirements are elevating the performance standards for packaging materials, driving adoption of high-barrier films, specialized polymers, and advanced substrates such as spunbond polyethylene. The regulatory burden also increases switching costs, strengthening long-term supplier relationships and favoring companies with proven validation capabilities and compliance expertise.

Aging Global Population Expanding Demand for Medical Devices and Packaging

Demographic shifts are a primary demand driver for medical device packaging materials. The global population aged 60 and above continues to rise significantly, leading to increased incidence of chronic diseases and higher utilization of medical devices such as implants, diagnostic kits, and surgical instruments. This demographic trend directly translates into higher consumption of sterile and protective packaging formats. Aging populations also drive demand for home healthcare solutions and wearable devices, which require packaging that ensures both product integrity and ease of use. As healthcare systems adapt to long-term care needs, packaging solutions must support extended shelf life, safe distribution, and patient-centric design.

Expansion of Medical Device Manufacturing in Emerging Markets

The growth of medical device manufacturing in emerging economies is creating substantial demand for compliant packaging materials. Government-led initiatives to promote domestic production, particularly in Asia Pacific, are accelerating investments in manufacturing infrastructure and medical device parks. This expansion increases the need for localized packaging supply chains capable of meeting international quality standards. Packaging suppliers are responding by establishing regional technical centers and production facilities, enabling faster product development, reduced lead times, and enhanced customer support. The shift toward localized manufacturing ecosystems is expected to significantly boost demand for both flexible and rigid packaging materials.

Restraint Analysis - High Validation Costs and Complex Qualification Processes

Medical device packaging requires extensive validation to ensure sterility, durability, and regulatory compliance. Processes such as seal integrity testing, transport simulation, sterilization compatibility, and shelf-life validation add significant time and cost to product development. These requirements create barriers for smaller manufacturers and limit the frequency of packaging redesigns. The cost of revalidation often exceeds raw material costs, making packaging changes economically challenging. This dynamic can slow innovation and reinforce dependence on existing validated solutions.

Sustainability Pressures on Conventional Packaging Materials

Environmental concerns are increasingly influencing packaging material selection. Traditional materials such as plastics and high-performance barrier substrates face scrutiny due to recyclability challenges and carbon footprint considerations. Healthcare providers and regulatory bodies are pushing for sustainable alternatives, including recyclable, biodegradable, and low-emission materials. While this transition creates opportunities, it also introduces risks for suppliers that rely heavily on conventional materials. Companies must invest in sustainable innovation while maintaining compliance with strict sterility and performance requirements, which can be technically complex and cost-intensive.

Opportunity Analysis - Localization and Supply Chain Optimization in Asia Pacific

Rapid industrialization and healthcare infrastructure development in Asia Pacific present significant growth opportunities. The establishment of medical device manufacturing hubs is driving demand for locally sourced packaging materials that meet global regulatory standards. Suppliers that offer integrated services, including design, prototyping, and validation, can gain a competitive advantage by embedding themselves early in the product development lifecycle. Localization also reduces logistics costs and enhances supply chain resilience, making it an attractive strategy for global and regional players.

Growth of Diagnostics, Wearables, and Home Healthcare Devices

The increasing adoption of diagnostic devices, wearable technologies, and home healthcare solutions is creating demand for innovative packaging formats. These applications often require non-sterile or semi-sterile packaging that prioritizes convenience, portability, and user safety. Packaging solutions must balance protection with accessibility, supporting rapid deployment and ease of use. This segment is particularly attractive due to shorter product cycles and higher volumes, offering opportunities for cost-efficient and scalable packaging designs.

Advancements in Sustainable and High-Performance Materials

Innovation in sustainable packaging materials represents a key opportunity for market players. Developments in recyclable polymers, bio-based materials, and lightweight structures are enabling companies to reduce environmental impact without compromising performance. Advanced coatings and material engineering are improving barrier properties and sterilization compatibility. Companies that successfully integrate sustainability with operational efficiency, such as reducing waste and improving line speeds, can differentiate themselves and capture premium market segments.

Category-wise Analysis

Material Insights

The plastics segment is expected to dominate the material segment, accounting for an anticipated share of over 51.2% of the market in 2026. Their widespread adoption is driven by versatility, cost efficiency, and compatibility with multiple sterilization methods such as ethylene oxide (EtO), gamma radiation, and electron beam sterilization. Plastics are extensively used in films, pouches, thermoformed trays, and blister packaging, supporting applications ranging from disposable medical supplies like syringes and IV sets to complex surgical instruments. Materials such as polyethylene (PE), polypropylene (PP), and polyethylene terephthalate (PET) are commonly used due to their excellent barrier properties, durability, and ease of processing. Their ability to maintain product integrity while enabling high-speed manufacturing makes them indispensable in large-scale medical device production environments.

High-density spunbond polyethylene fibers and LDPE are expected to be the fastest-growing material segment. These materials offer superior microbial barrier performance, high tear resistance, and clean peel characteristics, which are essential for sterile packaging applications. For example, spunbond polyethylene materials are widely used in packaging for surgical kits, implants, and catheter systems, where maintaining sterility is critical. Their compatibility with a broad range of sterilization techniques, including low-temperature processes, enhances their suitability for high-value and sensitive medical devices. Growth is driven by increasing demand for reliable sterile barrier systems, particularly in advanced surgical procedures and implantable device packaging, where product safety and extended shelf life are paramount.

Packaging Type Insights

Plastic films are anticipated to lead the packaging type segment, capturing an anticipated 37.4% share of total revenue in 2026. Their dominance stems from their adaptability in forming, sealing, and printing processes, making them suitable for a wide variety of medical applications. Films are widely used in flexible packaging formats such as pouches and wraps, offering cost-effective solutions for high-volume production. They also support advanced barrier properties against moisture, oxygen, and contaminants, while enabling clear labeling and traceability. For instance, flexible film-based pouches are commonly used for packaging disposable gloves, diagnostic kits, and wound care products due to their lightweight and efficient design.

Trays and blisters are expected to be the fastest-growing packaging type due to increasing demand for sterile and protective packaging solutions. These formats provide enhanced structural integrity, product visibility, and ease of handling, which are critical for surgical instruments, implants, and pre-assembled medical kits. For example, thermoformed trays are widely used for orthopedic implants and surgical toolkits, ensuring secure placement and aseptic presentation in operating rooms. Blister packs are also gaining traction in packaging smaller medical devices and diagnostic components. The ability of these formats to maintain sterility while improving operational efficiency in clinical settings is driving their adoption, particularly in high-precision and high-value applications.

Regional Insights

North America Medical Device Packaging Materials Market Trends - Regulatory-Driven Sterile Packaging Demand & Capacity Expansion

North America is projected to lead the market, accounting for approximately 36.1% of market share in 2026, with the U.S. serving as the primary growth engine. The region’s dominance is supported by its advanced healthcare infrastructure, stringent regulatory framework, and a high concentration of medical device manufacturers. Strict compliance requirements related to sterility validation, labeling accuracy, and traceability continue to drive demand for high-performance packaging materials such as sterile barrier films, Tyvek-based solutions, and rigid trays. The strong regulatory environment increases the need for validated packaging systems, reinforcing long-term supplier relationships.

The region benefits from a well-established innovation ecosystem characterized by continuous product development and technological advancements. Companies such as Amcor and DuPont have made significant investments in expanding healthcare packaging capabilities across North America. For instance, DuPont expanded its sterile packaging manufacturing capacity in Costa Rica to better serve the Americas, improving supply chain resilience and reducing lead times for medical device manufacturers. Similarly, Amcor’s continued investments in ISO 13485-certified facilities strengthen compliance capabilities and support high-quality production standards. These developments are enhancing regional supply reliability while enabling faster product commercialization, particularly for sterile and high-value medical devices.

Europe Medical Device Packaging Materials Market Trends - MDR Compliance & Shift toward Sustainable High-Barrier Packaging

Europe represents a mature and highly regulated market, with key contributions from countries such as Germany, the U.K., France, and Spain. The region’s strong emphasis on regulatory compliance, particularly under the Medical Device Regulation (MDR), drives demand for advanced packaging materials that ensure traceability, sterility, and product safety. Harmonized regulations across the European Union create a consistent framework for packaging requirements, increasing the need for high-performance materials and validated packaging systems.

The presence of a large number of small and medium-sized medical device manufacturers creates demand for specialized packaging solutions and technical support services. Companies such as Klöckner Pentaplast and Wipak are actively developing sustainable and high-barrier packaging solutions tailored to European regulatory standards. For example, KP has expanded its focus on recyclable high-barrier films for healthcare applications, aligning with the region’s circular economy goals. Wipak also continues to invest in sustainable flexible packaging innovations, supporting reduced environmental impact without compromising sterility. These initiatives are influencing market dynamics by accelerating the shift toward eco-friendly materials while maintaining compliance with strict regulatory requirements.

Asia Pacific Medical Device Packaging Materials Market Trends - Rapid Growth via Healthcare Expansion & Localized Manufacturing Investments

Asia Pacific is expected to be the fastest-growing region in the medical device packaging materials market, driven by rapid industrialization, expanding healthcare infrastructure, and rising domestic demand for medical devices. Countries such as China, Japan, and India are leading growth, supported by government initiatives, increasing healthcare expenditure, and a growing focus on domestic manufacturing capabilities. The region’s cost advantages and availability of skilled labor make it an attractive hub for global medical device production.

Recent developments highlight strong momentum in regional capacity expansion and localization. Amcor established a coating facility in Malaysia to produce advanced medical packaging substrates, enhancing supply chain efficiency and reducing dependence on imports. Nelipak launched a technical development center in Singapore, enabling faster packaging design, prototyping, and validation for regional customers. In India, government-backed initiatives such as medical device parks and production-linked incentives are encouraging both domestic and international players to expand manufacturing operations. These developments are strengthening the regional ecosystem by improving access to high-quality packaging materials, accelerating time-to-market, and supporting the transition toward localized and resilient supply chains.

Competitive Landscape

The global medical device packaging materials market is moderately fragmented, with a mix of global leaders and regional players. Leading companies maintain strong positions through extensive product portfolios, advanced material technologies, and established customer relationships. Market competition is driven by innovation, regulatory compliance, and the ability to provide integrated packaging solutions. While large players dominate high-value segments, smaller companies compete through specialization and niche offerings.

Key players focus on innovation, regulatory compliance, and geographic expansion to maintain a competitive advantage. Strategies include investment in sustainable materials, development of high-performance packaging solutions, and expansion of regional manufacturing capabilities. Companies are also emphasizing integrated service offerings to enhance customer retention and reduce time-to-market.

Key Industry Developments:

- In October 2025, Amcor showcased patient-centric and sustainable healthcare packaging innovations at CPHI Frankfurt, focusing on improving usability, performance, and environmental impact in medical packaging solutions.

- In December 2025, Nelipak completed the acquisition of Merrill’s Packaging, strengthening its footprint in healthcare manufacturing hubs and expanding its capabilities in custom sterile packaging solutions.

Companies Covered in Medical Device Packaging Materials Market

- Amcor

- DuPont

- Nelipak

- Oliver Healthcare Packaging

- TekniPlex Healthcare

- Wipak

- Klöckner Pentaplast

- Sonoco

- SCHOTT

- Greiner Bio-One

- Sealed Air

- Berry Global

- Constantia Flexibles

- UFP Technologies

- ProAmpac

- SteriPack Group

Frequently Asked Questions

The global medical device packaging materials market is estimated to be valued at US$43.5 billion in 2026.

The medical device packaging materials market is projected to reach US$65.8 billion by 2033.

Key trends include the rising adoption of sterile barrier packaging, increasing focus on sustainable and recyclable materials, growing demand for high-performance polymers, and expansion of localized manufacturing and supply chains, particularly in Asia Pacific.

Plastics are the leading material segment, accounting for over 51.2% of the market share, supported by their versatility, cost efficiency, and compatibility with sterilization processes.

The medical device packaging materials market is expected to grow at a CAGR of 6.1% from 2026 to 2033, driven by regulatory compliance requirements and increasing medical device demand.

Major players include Amcor, DuPont, Nelipak, Oliver Healthcare Packaging, and TekniPlex Healthcare.