- Non-food Packaging

- Offset Packaging Market

Offset Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Offset Packaging Market By Printing Type (Sheet-Fed Offset, Web-Fed Offset, Others), Material (Paper & Board, Plastic, Others), End-Use Industry and Regional Analysis for 2026 - 2033

Offset Packaging Market Size and Trends Analysis

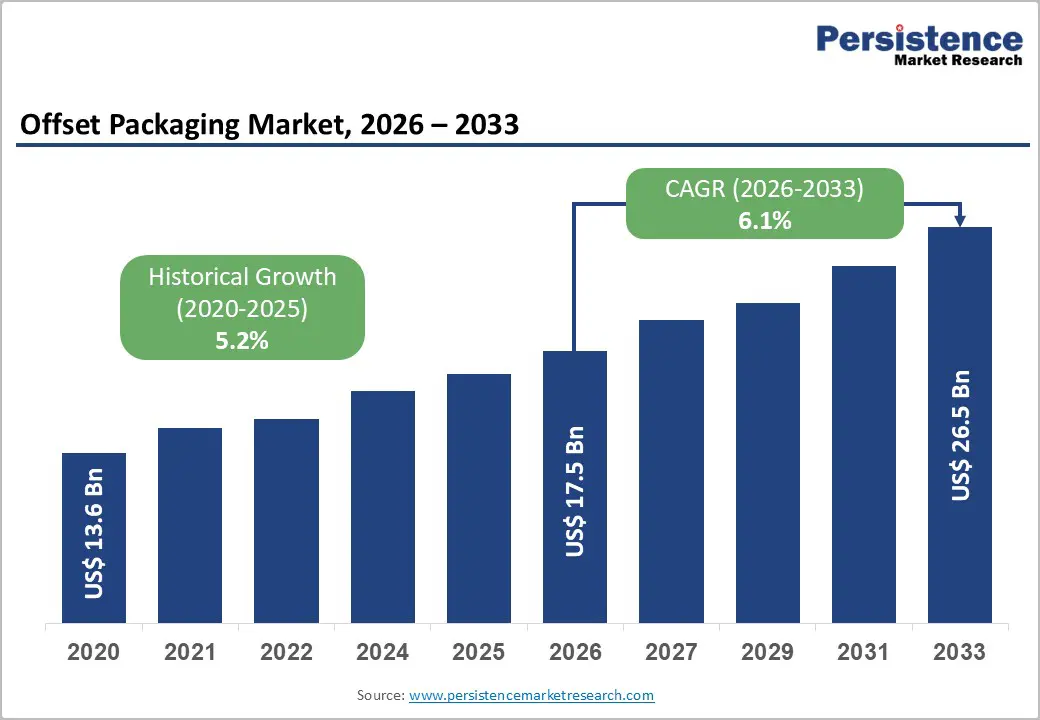

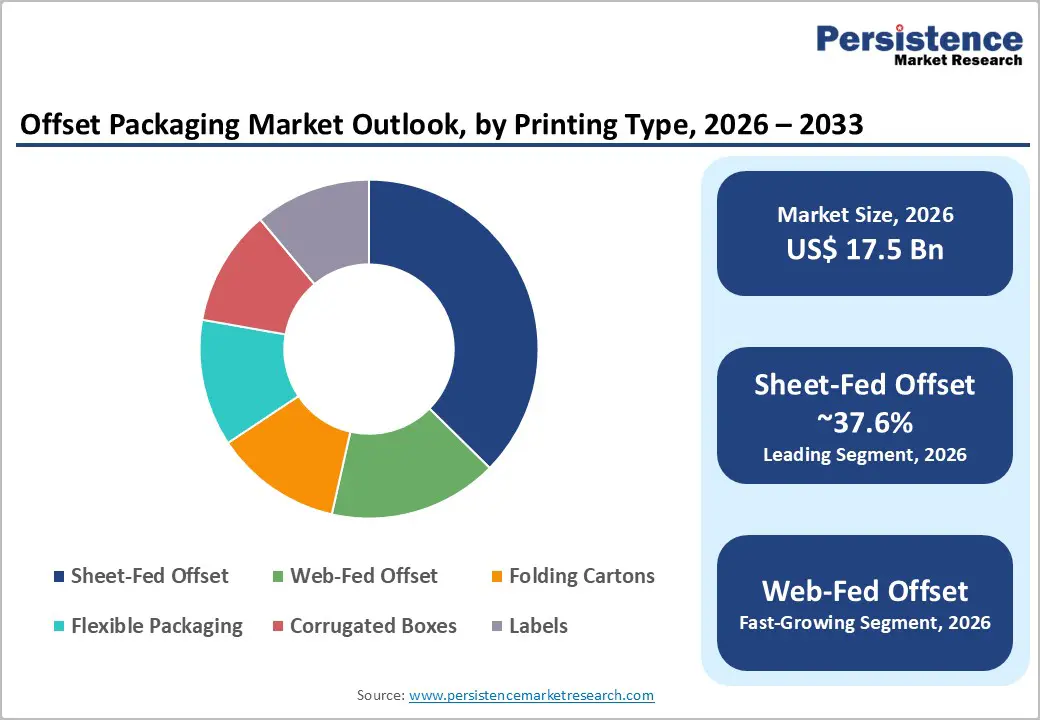

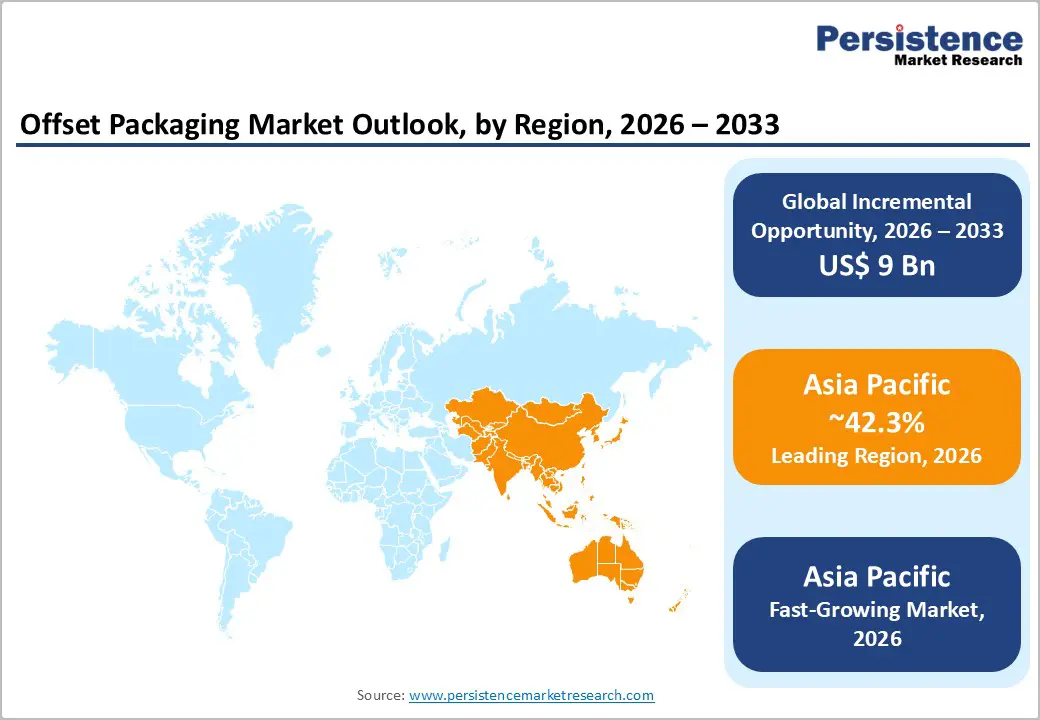

The global offset packaging market size is likely to be valued at US$17.5 billion in 2026 and is expected to reach US$26.5 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033, driven by rising demand for high-quality printed packaging in the food, beverage, and pharmaceutical sectors. Increasing regulatory emphasis on sustainable and recyclable materials is accelerating the shift toward paper-based packaging formats. Technological advancements in offset printing and the growing importance of premium branding are reinforcing the role of offset packaging in global supply chains.

Key Industry Highlights

- Leading Region: Asia Pacific is projected to account for approximately 42.3% of the market share, driven by strong manufacturing capacity, rising consumption, and expanding packaging infrastructure.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, supported by rapid industrialization, increasing demand for packaged goods, and continuous investments in localized production.

- Investment Plans: Companies are increasingly investing in automation, sustainable packaging solutions, and regional manufacturing expansion, particularly in Asia Pacific, to improve efficiency, reduce lead times, and meet evolving regulatory requirements.

- Dominant Printing Type: Sheet-fed offset is the dominant printing type, holding an estimated 37.6% share, owing to its superior print quality and suitability for premium packaging applications.

- Leading Material: The paper & board segment is estimated to account for over 68.4% of the market share, supported by high recyclability, regulatory backing, and strong demand from food and pharmaceutical packaging industries.

| Key Insights | Details |

|---|---|

|

Offset Packaging Market Size (2026E) |

US$17.5 Bn |

|

Market Value Forecast (2033F) |

US$26.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.2% |

DRO Analysis

Driver Analysis - Sustainability-Driven Packaging Transformation Supporting Offset Adoption

Growing regulatory pressure on packaging waste management and recyclability is significantly influencing material selection and printing technologies. Governments across developed economies are implementing stricter guidelines for recyclable and reusable packaging, encouraging the use of paper and board substrates. Offset printing aligns well with these materials due to its superior print quality and compatibility with sustainable packaging formats such as folding cartons and corrugated boxes. High recycling rates of paper-based packaging further strengthen its economic and environmental viability. As brands shift toward eco-friendly packaging to meet regulatory and consumer expectations, offset printing continues to benefit from increased adoption across environmentally compliant packaging solutions.

Regulatory Compliance in Food and Pharmaceutical Packaging Driving Demand

Stringent regulations governing labeling, traceability, and safety in the food and pharmaceutical industries are key drivers of the offset packaging market. Packaging must include detailed product information, batch tracking, and compliance labeling, which requires high precision and consistent print quality. Offset printing offers the accuracy and reliability necessary for such applications, particularly in folding cartons, inserts, and labels. In pharmaceuticals, strict control over packaging materials and labeling processes further reinforces the need for high-quality printing technologies. This regulatory environment ensures sustained demand for offset packaging, as companies prioritize compliance and product integrity.

Growth in E-Commerce and Premium Branding Enhances Packaging Requirements

The expansion of e-commerce and changing consumer preferences are increasing the demand for visually appealing and durable packaging. Brands are investing in premium packaging designs to improve shelf visibility and enhance the unboxing experience. Offset printing is widely used for short- to medium-run packaging where high-resolution graphics and color consistency are critical. The need for differentiated packaging in competitive retail environments further supports demand. As online retail continues to grow, packaging is evolving into a key branding tool, thereby strengthening the role of offset printing in delivering high-quality visual presentation.

Restraint Analysis - High Capital Investment and Operational Costs

Offset printing equipment requires substantial capital investment, including installation, maintenance, and workflow integration. Advanced offset presses used in packaging applications are highly sophisticated and often involve automation and digital integration, increasing upfront costs. Small and mid-sized converters may face challenges in upgrading or expanding capacity due to financial constraints. Long payback periods and high operational costs, including skilled labor and maintenance, can limit market entry and slow technology adoption, particularly in price-sensitive regions.

Increasing Competition from Digital and Flexographic Printing Technologies

Offset printing faces growing competition from digital and flexographic printing, especially in applications requiring shorter print runs or variable data printing. Digital printing offers faster turnaround times and customization capabilities, while flexographic printing is widely used for flexible packaging and large-volume production. As packaging requirements diversify, customers increasingly evaluate alternative technologies based on cost, speed, and flexibility. This competitive pressure may limit the growth of offset printing in certain segments, particularly where rapid production and personalization are critical.

Opportunity Analysis - Expansion of Packaging Production in Asia Pacific

Asia Pacific presents significant growth opportunities due to rapid industrialization, expanding consumer markets, and increasing investments in packaging infrastructure. Countries such as China, India, and Southeast Asian economies are witnessing strong demand for packaged goods across food, pharmaceuticals, and consumer products, driven by urbanization and rising disposable incomes. The rapid expansion of organized retail and e-commerce platforms is further accelerating the need for high-quality printed packaging. Localization of manufacturing and supply chains is encouraging global and regional players to establish new production facilities and printing operations within the region, reducing dependency on imports and improving turnaround times. In addition, government initiatives supporting domestic manufacturing and industrial development are attracting investments in packaging technologies. These factors collectively position Asia Pacific as a key growth engine for offset packaging, particularly in folding cartons, labels, and high-volume consumer packaging applications.

Development of Barrier-Coated Paper Packaging

Advancements in barrier coating technologies are enabling paper-based packaging to replace plastic in a growing number of applications. These coatings improve resistance to moisture, grease, and oxygen, making paper suitable for packaging food, beverages, and personal care products that traditionally relied on multi-layer plastic materials. Offset printing is particularly well-suited for such substrates, as it delivers high-resolution graphics and consistent print quality even on coated surfaces. This innovation is gaining traction among brands seeking to meet sustainability targets while maintaining product protection and shelf appeal. For example, barrier-coated paper is increasingly being used in takeaway food packaging, dry food cartons, and cosmetic packaging. As regulatory pressure on plastic usage intensifies, the adoption of these advanced paper solutions is expected to accelerate, creating new growth avenues for offset packaging providers.

Integration of Smart Packaging and Digital Features

The integration of smart packaging technologies, including RFID tags, QR codes, and interactive labels, is creating new value propositions across the packaging industry. These features enable real-time product tracking, authentication, and enhanced consumer engagement through digital interfaces. Offset printing plays a crucial role in this transformation by providing a high-quality platform for embedding these technologies into packaging designs without compromising visual appeal. For instance, QR-enabled packaging allows consumers to access product information, promotional content, or traceability data, while RFID integration supports inventory management and anti-counterfeiting measures in sectors such as pharmaceuticals and luxury goods. This convergence of traditional printing with digital functionality is enabling packaging to evolve from a protective medium into a communication and data-driven tool, thereby increasing its strategic importance and economic value in the supply chain.

Category-wise Analysis

Printing Type Insights

Sheet-fed offset dominates the market with an anticipated share of approximately 37.6% in 2026, primarily due to its suitability for high-quality, short- to medium-run packaging applications. It is widely used in folding cartons, labels, and premium retail packaging where precision, color consistency, and finishing quality are essential. Industries such as food, cosmetics, and pharmaceuticals rely heavily on sheet-fed offset for brand differentiation and regulatory compliance. For instance, premium cosmetic brands and pharmaceutical cartons often require intricate graphics, fine typography, and batch-level labeling, all of which are efficiently handled by sheet-fed presses.

The technology’s ability to process a wide range of substrates, including coated paperboard, metallized sheets, and specialty finishes, further strengthens its position. It is particularly preferred for high-value packaging such as luxury confectionery boxes, personal care packaging, and OTC pharmaceutical cartons, where visual appeal directly influences consumer purchasing decisions. Continuous advancements in automation, color management systems, and inline finishing capabilities are also improving operational efficiency, reinforcing sheet-fed offset as the preferred solution for premium packaging segments.

Web-fed offset is expected to be the fastest-growing segment, driven by its efficiency in large-scale production. This printing type is widely adopted in applications such as corrugated packaging liners, large-volume labels, and mass-produced consumer goods packaging. Its high-speed operation, combined with lower per-unit production costs, makes it particularly suitable for industries requiring consistent output at scale, including FMCG, beverages, and household products.

For example, beverage carton packaging and bulk food product cartons often utilize web-fed offset printing to achieve cost efficiency while maintaining consistent branding across large production volumes. The technology also supports continuous printing processes, reducing downtime and improving throughput. As demand for standardized packaging increases in emerging markets and global supply chains become more volume-driven, web-fed offset is expected to gain further traction, especially among large converters focused on operational efficiency and cost optimization.

Material Insights

The paper and board segment is expected to dominate, with an anticipated share exceeding 68.4% in 2026, driven by strong sustainability credentials, recyclability, and regulatory support. These materials are extensively used in food, beverage, and pharmaceutical packaging, where safety, compliance, and environmental considerations are critical. Offset printing performs exceptionally well on paper-based substrates, delivering high-resolution graphics, vibrant colors, and efficient production for folding cartons, corrugated boxes, and labels.

For instance, bakery packaging, cereal boxes, and pharmaceutical cartons predominantly use paperboard due to its ease of printing and recyclability. Increasing consumer preference for eco-friendly packaging and government regulations promoting circular economy practices are accelerating the shift toward paper-based materials. Innovations such as lightweight board grades and barrier-coated paper are further expanding application areas, reinforcing the long-term dominance of paper and board in offset packaging.

Plastic materials represent the fastest-growing segment, particularly in flexible and specialty packaging applications. Plastics offer superior barrier properties, durability, and flexibility, making them ideal for products requiring extended shelf life, moisture resistance, and product protection. Offset printing technologies are increasingly being adapted to print on synthetic substrates such as PET, PP, and laminated films, broadening their applicability in this segment.

Examples include flexible packaging for snacks, personal care sachets, and pharmaceutical blister packs, where plastic substrates provide both functionality and visual appeal. Despite growing environmental concerns, the demand for plastic packaging remains strong in sectors where performance requirements outweigh sustainability considerations. However, ongoing developments in recyclable and bio-based plastics are expected to reshape this segment, enabling a balance between functionality and environmental responsibility while sustaining growth in offset-compatible plastic packaging.

Regional Insights

North America Offset Packaging Market Trends - Sustainable, Regulated, and Technology-Driven Offset Packaging Growth

North America remains a key market for offset packaging, supported by strong demand from food, healthcare, and e-commerce sectors. The U.S. leads the region, with a well-established packaging infrastructure and high adoption of advanced printing technologies. Regulatory requirements for food safety and pharmaceutical labeling continue to drive demand for high-quality, precision-based packaging solutions. The region also benefits from high recycling rates for paper-based packaging, reinforcing the shift toward sustainable materials and supporting the dominance of paperboard-based offset applications.

Technological innovation and automation are central to market evolution in North America. Companies such as Graphic Packaging Holding Company and International Paper are expanding their sustainable packaging portfolios, particularly in recyclable folding cartons and fiber-based solutions. At the same time, Amcor continues to invest in responsible packaging innovations, including recyclable and lightweight packaging formats.

On the equipment side, Komori Corporation has strengthened its U.S. footprint through installations of advanced offset presses, enabling converters to improve productivity and reduce waste. These developments are enhancing regional competitiveness while enabling converters to meet evolving regulatory and brand-owner requirements. Growth opportunities remain strong in premium packaging, pharmaceutical labeling, and e-commerce-ready solutions, where compliance, durability, and visual appeal are critical.

Europe Offset Packaging Market Trends - Regulation-Led Circular Packaging and Innovation in Offset Printing

Europe is characterized by a strong regulatory framework and a clear focus on sustainability, making it a structurally important market for offset packaging. The implementation of stricter packaging waste regulations across the European Union is accelerating the adoption of recyclable and reusable materials, particularly paper and board. Countries such as Germany, the U.K., France, and Spain play a significant role, supported by advanced manufacturing capabilities and strong demand for high-quality, compliant packaging.

The region is also a hub for innovation in packaging and printing technologies. Companies such as Mondi plc and Stora Enso are actively developing sustainable packaging solutions, including fiber-based alternatives to plastic and recyclable barrier-coated paper. Heidelberger Druckmaschinen AG has introduced advanced offset presses and collaborated on barrier-coating technologies, enabling converters to expand into flexible paper packaging applications.

Similarly, BOBST Group SA is focusing on digitalization and automation in converting processes, improving efficiency, and reducing material waste. These developments are directly influencing the regional market by accelerating the transition toward circular packaging systems. Europe’s strong regulatory push, combined with technological leadership, continues to position it as a critical market for sustainable offset packaging innovation.

Asia Pacific Offset Packaging Market Trends - High-Volume Expansion and Manufacturing-Led Offset Packaging Growth

Asia Pacific is the largest and fastest-growing region, holding approximately 42.3% of the market share. The region’s growth is driven by rapid industrialization, expanding consumer markets, and increasing demand for packaged goods across key economies such as China, India, Japan, and ASEAN countries. Strong growth in food, pharmaceuticals, and consumer goods sectors is driving demand for high-volume, cost-efficient packaging solutions, where offset printing plays a crucial role.

The region benefits from cost-effective manufacturing, a large labor force, and increasing investments in packaging infrastructure. Localization of production is a major trend, as seen with Avery Dennison Corporation establishing an RFID and labels manufacturing facility in Pune, India, to support regional supply chains and smart packaging adoption. Komori Corporation has also expanded its presence in Asia through new packaging press launches and participation in major industry exhibitions, reinforcing its focus on high-growth markets. Meanwhile, Heidelberger Druckmaschinen AG continues to strengthen its footprint in India and Southeast Asia through installations targeting pharmaceutical and packaging converters.

Large regional packaging producers and global converters are also investing in new plants and capacity expansions to meet rising domestic demand. These developments are improving production efficiency, reducing lead times, and enabling faster response to market needs. The region’s dynamic economic environment, combined with increasing adoption of advanced printing technologies and sustainable packaging practices, makes Asia Pacific the central growth engine for the offset packaging market over the forecast period.

Competitive Landscape

The global offset packaging market is moderately fragmented, with a mix of global packaging companies and specialized printing technology providers. No single company dominates the market across all segments, leading to intense competition based on product quality, innovation, and service capabilities. Market participants focus on expanding their product portfolios, improving operational efficiency, and strengthening their global presence to maintain competitiveness.

Key players are focusing on technological innovation, sustainability, and geographic expansion. Companies are integrating digital capabilities with traditional offset printing, investing in eco-friendly materials, and expanding operations in high-growth regions. Differentiation is achieved through advanced printing technologies, efficient production processes, and value-added packaging solutions.

Key Industry Developments

- In February 2026, Koenig & Bauer AG supported Packrite in investing in a new Rapida 164 eight-color offset press, enhancing large-format packaging production speed, color consistency, and efficiency for high-end corrugated packaging applications.

- In March 2026, Koenig & Bauer AG launched its “IMPACT” strategic framework, focusing on digital transformation, automation, and packaging-focused innovation to strengthen its technological leadership in the global printing and packaging market.

Companies Covered in Offset Packaging Market

- Amcor

- International Paper

- Graphic Packaging Holding Company

- Mondi plc

- Stora Enso

- Smurfit Westrock

- WestRock Company

- DS Smith

- Sonoco Products Company

- Huhtamaki

- Tetra Pak

- Heidelberger Druckmaschinen AG

- Koenig & Bauer AG

- Komori Corporation

- BOBST Group SA

- Avery Dennison Corporation

Frequently Asked Questions

The offset packaging market is estimated to be valued at US$ 17.5 billion in 2026.

The offset packaging market is expected to reach US$ 26.5 billion by 2033.

Key trends include the shift toward recyclable paper-based packaging, adoption of barrier-coated paper solutions, integration of smart packaging technologies such as RFID and QR codes, and growing demand for premium, high-quality printed packaging across consumer-facing industries.

Paper & board is the leading material segment, accounting for over 68.4% of the market share, due to its recyclability, regulatory support, and strong compatibility with offset printing technologies.

The offset packaging market is projected to grow at a CAGR of 6.1% from 2026 to 2033.

Some of the major players include Amcor, International Paper, Graphic Packaging Holding Company, Mondi plc, and Stora Enso.