- Specialty & Fine Chemicals

- Matting Agents Market

Matting Agents Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Matting Agents Market By Product Type (Organic, Inorganic), Formulation (Waterborne, Solventborne, Powder, UV/EB), by Application (Industrial Coatings, Wood Coatings, Leather Coatings, Architectural), and Regional Analysis for 2025 - 2032

Matting Agents Market Size and Trends

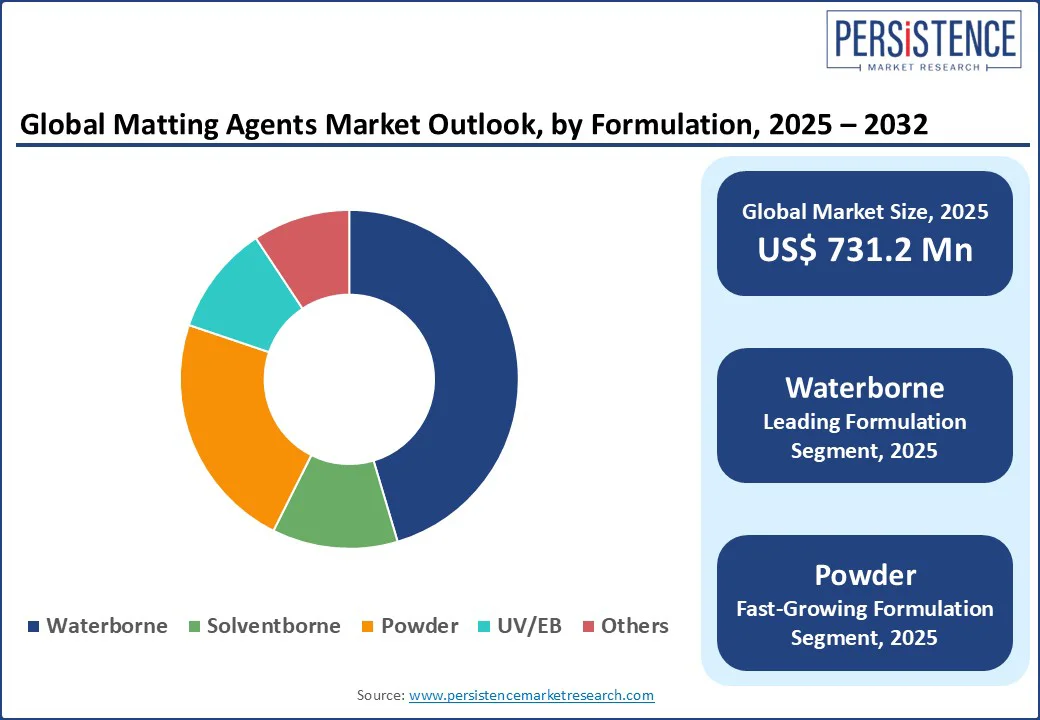

The matting agents market size is likely to be valued at US$ 731.2 Mn in 2025 and is estimated to reach US$ 974.6 Mn in 2032, growing at a CAGR of 4.8% during the forecast period 2025-2032. Matting agents have become a key value driver in the global coatings market, enabling manufacturers to meet evolving aesthetic, functional, and regulatory demands across diverse applications. These additives are no longer confined to basic gloss reduction. Instead, they are strategically leveraged to deliver differentiated surface finishes, improve coating performance, and improve user appeal in various sectors. With demand rising for low-VOC, matte, and multifunctional coatings, the market is transforming. It is attributed to innovations in formulation science, material development, and environmental compliance pressures.

Key Industry Highlights

- Key players are engaging in strategic collaborations with resin and coating manufacturers to co-develop optimized systems.

- Increasing preference for ultra-matte coatings in luxury vehicles and electric car models is predicted to boost opportunities.

- Consumer preference for low-sheen, stain-resistant coatings in residential and commercial interiors is expected to fuel the market.

- Waterborne formulation will likely account for nearly 45.4% share in 2025 as it ensures compatibility with modern resin systems in decorative and industrial coatings.

- Architectural application is poised to witness steady growth as leading paint brands are extending matte product lines to meet demand in luxury housing and commercial spaces.

- Government policies promoting low-VOC, eco-friendly paints in North America are spurring high in demand for compatible matting agents.

|

Global Market Attribute |

Key Insights |

|

Matting Agents Market Size (2025E) |

US$ 731.2 Mn |

|

Market Value Forecast (2032F) |

US$ 974.6 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

4.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.1% |

Market Dynamics

Driver - Booming Paints and Coatings Industry Fuels Demand

Rapid expansion of the paints and coatings industry, particularly in architectural and industrial applications, is propelling the matting agents market growth. There is increasing pressure on manufacturers to offer not just aesthetic appeal but also surface functionality such as anti-glare and stain resistance. Both are heavily reliant on matting agents. Demand for low-sheen and velvet-finish wall paints is spurring the adoption of silica-based and wax-based matting agents that offer precise control over gloss levels.

In the automotive industry, the popularity of matte and satin finishes in luxury and electric vehicles is further fueling the use of high-performance matting agents. For example, BMW’s Frozen Paint series and Porsche’s PTS (Paint to Sample) matte options have expanded globally, pushing demand for coatings that require superior dispersion and surface uniformity. These finishes often utilize specialty matting agents that maintain durability and UV resistance without compromising the matte effect.

Restraint - Durability Trade-offs and Dispersion Issues Challenge Growth

One of the key technical limitations hampering the wide adoption of matting agents is the potential compromise in durability, primarily in high-traffic or outdoor applications. Matte coatings typically have a more open surface structure, which can make them susceptible to abrasion, staining, and dirt pickup. In industrial environments or exterior architectural uses, this presents a performance trade-off. For example, a 2023 study published by the European Coatings Journal noted that matte-finished polyurethane coatings showed up to 25% lower abrasion resistance compared to their glossy counterparts.

Achieving uniform dispersion of matting agents, mainly in low-VOC or high-solids formulations, presents another key challenge. Several matting agents tend to agglomerate or settle during formulation, leading to surface defects such as haze, streaks, or gloss inconsistencies. It is problematic in waterborne systems, which are increasingly being adopted due to environmental regulations. These issues are further aggravated when matting agents interact unpredictably with new resin chemistries such as bio-based or UV-curable systems.

Opportunity - Engineered Nanostructures and Hybrid Polymers Expand Scope

The emergence of nanotechnology and advanced polymer systems is creating new opportunities for matting agents. Nanostructured matting agents such as those engineered using precipitated silica or aluminum oxide nanoparticles, offer precise control over surface topography at the microscopic level. They enable ultra-matte finishes without sacrificing transparency or mechanical performance. Advanced polymer systems, including hybrid polyurethane-acrylics and fluoropolymer blends, are increasingly being used in automotive, aerospace, and high-end architectural coatings.

They require matting agents with superior compatibility and dispersion. Traditional matting agents often fail to integrate effectively with these polymers due to viscosity or polarity mismatches. New surface-modified or organically treated matting agents are hence being engineered specifically for such systems. Nanotechnology is further providing multifunctional performance from matting agents, transforming them from mere gloss reducers to smart additives.

Category-wise Analysis

Formulation Insights

By formulation, the market is divided into waterborne, solventborne, powder, UV/EB, and others. Among these, the waterborne segment is poised to account for nearly 45.4% of the matting agents market share in 2025 due to their ability to comply with strict norms, especially concerning Volatile Organic Compound (VOC) emissions. They are also capable of meeting modern performance and aesthetic standards in coatings. Waterborne formulations further enable superior formulation flexibility, allowing matting agents to be combined with additives that impart anti-scratch, anti-blocking, and soft-touch properties.

Powder formulations are gaining momentum owing to their solvent-free nature, excellent durability, and compatibility with energy-efficient curing technologies. These inherently contain no VOCs, making them a preferred choice in regions with stringent emissions regulations. Achieving consistent matte finishes in powder coatings is technically challenging due to the solid nature of the formulation and the dynamics of melt-mixing and curing. To address this, specialized matting agents are now being used in tandem with proprietary matting additives.

Application Insights

Based on application, the market is segregated into industrial coatings, wood coatings, leather coatings, architectural, and others. Out of these, the architectural segment will likely hold around 41.7% of share in 2025 backed by increasing demand for durable, low-sheen finishes in both interior and exterior environments. Residential and commercial construction sectors account for the most prominent volume of paint usage globally. With the surging trend toward velvet, satin, and ultra-matte wall finishes, matting agents have become a core component of decorative coating formulations.

Industrial coatings represent an important application area due to their increasing use in protective and functional coatings across general manufacturing, heavy machinery, appliances, and infrastructure sectors. These coatings often require semi-matte to low-gloss finishes to reduce glare, improve operator safety, and mask wear over time. The segment is also evolving due to rising demand for aesthetic-functional duality in industrial design. Equipment manufacturers increasingly seek coatings that not only protect against corrosion and abrasion but also present a premium, modern matte finish.

Regional Insights

North America Matting Agents Market Trends

North America is currently experiencing a notable shift propelled by the increasing demand for sustainable and performance-backed coatings. A key trend is the rising demand for low-gloss architectural coatings, mainly in high-end residential and commercial projects. According to the American Coatings Association, matte and eggshell finishes accounted for nearly 48% of interior paint sales in the U.S. in 2023. This shows a clear departure from the earlier preference for glossy aesthetics. The shift is compelling formulators to rely heavily on high-efficiency matting agents that ensure visual consistency and scrub resistance.

In the U.S. matting agents market, the automotive refinish segment is embracing these agents due to the rising popularity of custom matte and satin finishes in the aftermarket and premium segments. Axalta Coating Systems and PPG Industries have developed matte-clearcoat systems that incorporate proprietary matting technologies to ensure ease of blending, weathering resistance, and compatibility with VOC norms. The country also serves as a hotbed for formulation innovation, with various additive suppliers focusing on surface-modified silica and thermoplastic waxes developed for new-generation coatings.

Europe Matting Agents Market Trends

Europe is being accelerated by the region's strict environmental norms, demand for low-VOC coatings, and preference for natural-looking finishes. The EU’s evolving REACH framework and the Green Deal have boosted the transition toward waterborne and bio-based coating systems. This has further prompted formulators to shift to silica-based and wax-treated matting agents that help maintain performance in low-emission environments. In 2024, over 62% of architectural coatings sold in Western Europe were waterborne, according to the European Council of the Paint, Printing Ink and Artists’ Colors Industry.

It highlights a rising demand for matting agents that ensure uniform dispersion and gloss reduction in these systems. The wood and furniture coatings segment in Scandinavia, Germany, and Italy has become a key demand center for ultra-matte finishes. Brands such as Jotun, Teknos, and AkzoNobel are developing coating lines with sub-10 GU gloss levels to replicate raw wood aesthetics. These finishes require highly engineered matting agents that offer not just surface dulling but also clarity, stain resistance, and touch-friendly texture.

Asia Pacific Matting Agents Market Trends

Asia Pacific is predicted to account for approximately 39.8% share in 2025 owing to booming construction activity and a surge in local manufacturing of paints and coatings. In China, India, and Vietnam, the adoption of matte and low-gloss coatings in architectural applications has risen steadily. It is evident in urban residential developments where muted, dust-masking finishes are preferred over conventional gloss. As per the China National Coatings Industry Association, matte interior wall coatings saw a 31% year-on-year growth in sales volume in 2023.

The wood coatings segment in Asia Pacific is further contributing to matting agent demand, primarily in Southeast Asia where export-oriented furniture manufacturing is thriving. Malaysia and Indonesia are key players in the global furniture supply chain. They are increasingly opting for waterborne and UV-curable matte coatings to comply with Western environmental standards. This trend is compelling local formulators to incorporate novel matting agents, often imported or custom-developed through partnerships with global suppliers.

Competitive Landscape

The global matting agents market is characterized by material science innovations, strategic expansions by multinational chemical companies, and increasing emphasis on customized formulations. A small number of global players dominate the market, each leveraging proprietary silica or wax-based technologies to maintain differentiation. They are heavily investing in research and development to launch high-performance matting agents that cater to low-VOC and waterborne coatings. Small-scale players are disrupting the landscape by delivering cost-competitive products that are made for local consumption.

Key Industry Developments

- In February 2025, Cabot Corporation launched a new dry fumed silica matting agent called CAB-O-SIL MT-6460 fumed silica for wood and leather coating applications. The highly efficient matting additive provides good matting performance, superior clarity at lower loadings, and smooth surface appearance.

- In July 2024, Coval Technologies introduced Coval Matting Agent that can be added to the gloss finish of Coval coatings to create a satin or matte finish. The new agent offers ease and versatility for installers, distributors, and end users.

Companies Covered in Matting Agents Market

- Evonik Industries AG

- W. R. Grace & Co.-Conn.

- Baltimore Innovations Ltd.

- Huber Engineered Materials

- PQ Corporation

- Huntsman International LLC

- Thomas Swan & Co. Ltd.

- Lu’An Jietonda New Material Co., Ltd.

- PPG Industries, Inc.

- Deuteron GmbH

- IMERYS S.A.

- Others

Frequently Asked Questions

The matting agents market is projected to reach US$ 731.2 Mn in 2025.

Expansion of premium interior décor trends and increased adoption of UV-curable coatings are the key market drivers.

The matting agents market is poised to witness a CAGR of 4.8% from 2025 to 2032.

Strategic collaborations with resin manufacturers and the expansion of matte finishes in sustainable construction are the key market opportunities.

Evonik Industries AG, W. R. Grace & Co.-Conn., and Baltimore Innovations Ltd. are a few key market players.