- Technology

- Macro 3D Printing Market

Macro 3D Printing Market Size, Share, and Growth Forecast, 2026 – 2033

Macro 3D Printing Market by Technology (Fused Deposition Model, Stereolithography, Powder Bed Fusion, Selective Laser Sintering), Component (Hardware, Services, Software), Material, Application, and Regional Analysis 2026 – 2033

Macro 3D Printing Market Size and Trends Analysis

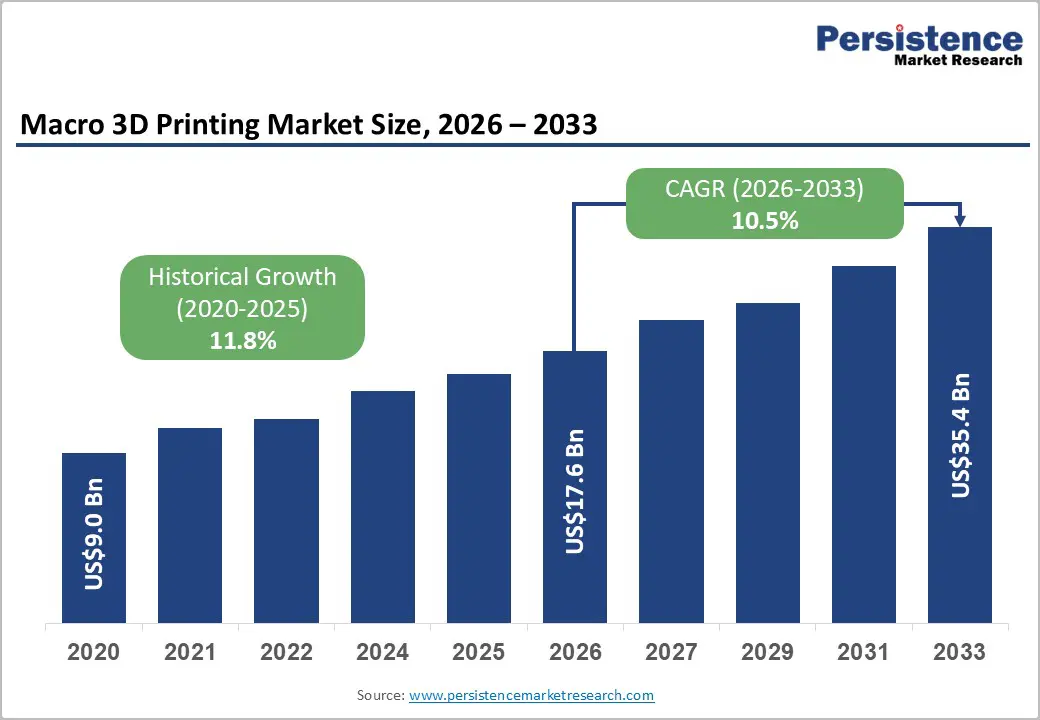

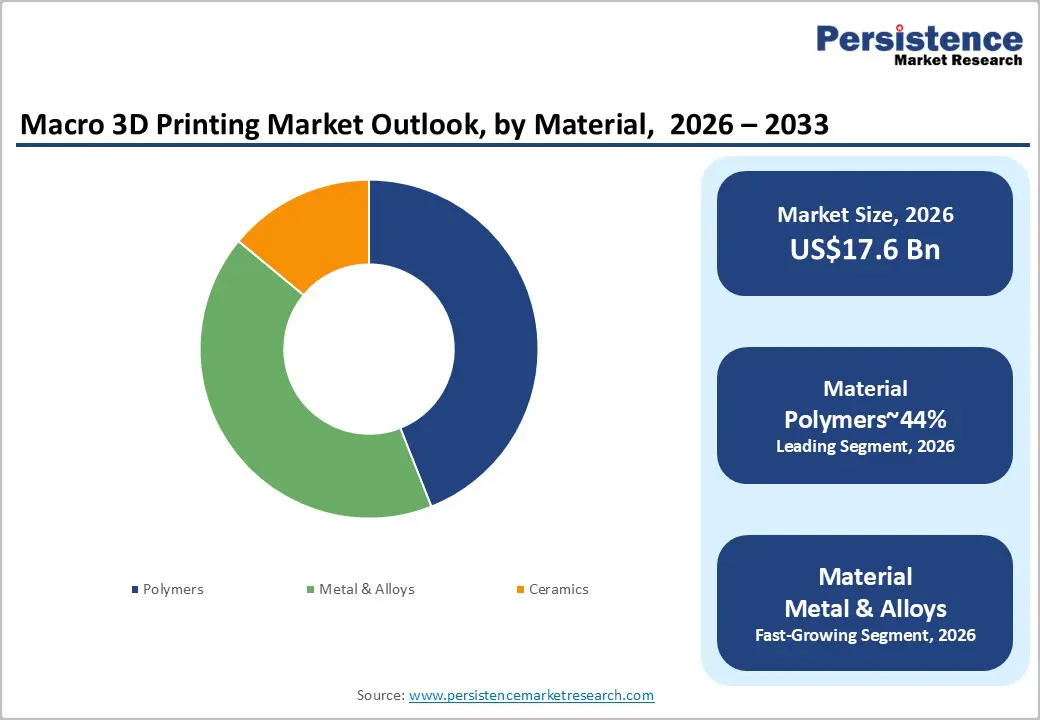

The global macro 3D printing market size is likely to be valued at US$17.6 billion in 2026 and is expected to reach US$35.4 billion by 2033, growing at a CAGR of 10.5% during the forecast period from 2026 to 2033, driven by the industrialization of additive manufacturing (AM), where advancements in print speed, consistency, and material properties, particularly in high-performance thermoplastics and metal alloys, have made it possible to directly produce functional end-use parts.

Regulatory support for sustainable manufacturing is further boosting market expansion across various industries. The integration of AI-powered workflow software and the concept of "digital inventory" are significantly lowering warehousing costs, particularly in the aerospace, automotive, and healthcare sectors.

Key Industry Highlights:

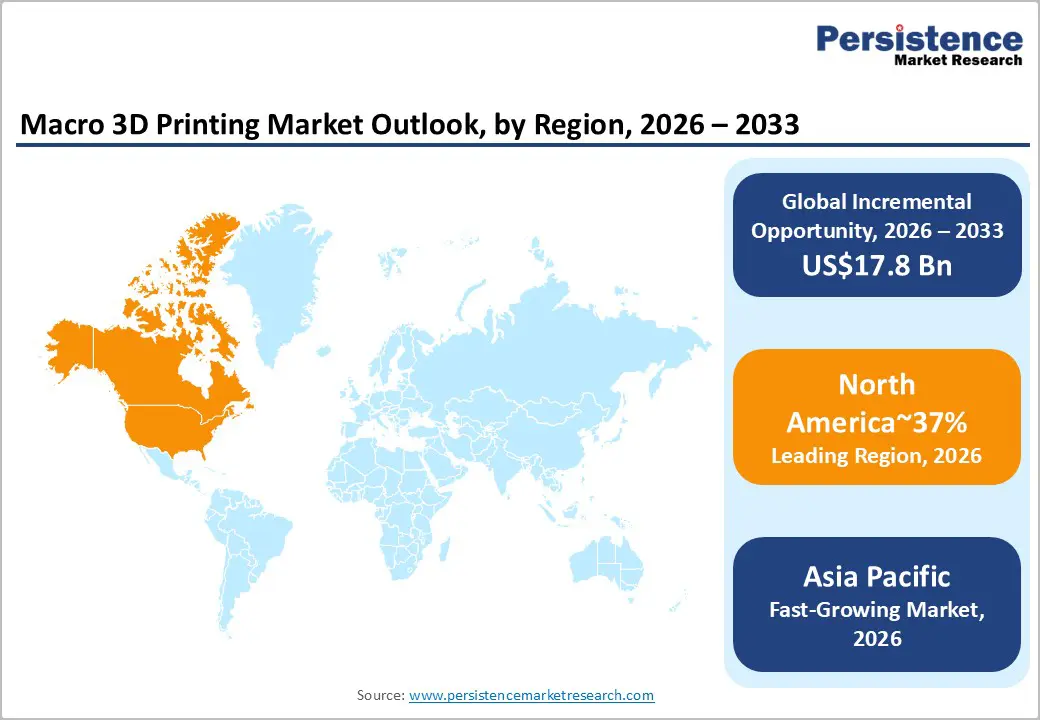

- Leading Region: North America is set to lead the global macro 3D printing market with a 37% share, driven by high-value industrial applications, AI-enabled process control, IoT monitoring, and localized production initiatives.

- Fastest-growing Region: Asia Pacific is expected to be the fastest-growing region, driven by robust industrial growth, government-backed initiatives, and a growing adoption of advanced manufacturing.

- Leading Component: Hardware is expected to lead with 63% share, driven by industrial users prioritizing throughput, quality, and qualification in aerospace, automotive, energy, and construction applications.

- Leading Material: Polymers are expected to remain the leading material segment with roughly 44% share, supported by versatility, cost efficiency, and suitability for prototyping, tooling, and functional parts.

- Key Industry Development: In December 2025, Alquist announced partnerships with Walmart and other retailers to 3D-print more than a dozen commercial structures, enhancing construction efficiency and cost savings through robotic 3D printing for standardized, low-touch production.

| Key Insights | Details |

|---|---|

|

Macro 3D Printing Market Size (2026E) |

US$17.6 Bn |

|

Market Value Forecast (2033F) |

US$35.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

10.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

11.8% |

Market Factors – Growth, Barrier, and Opportunity Analysis

Advancements in Large-Format Additive Manufacturing Technologies

Technological advancements in large-format additive manufacturing (LFAM) have become a key driver for macro-scale adoption across various industrial sectors. Continuous improvements in material extrusion and powder bed fusion technologies have increased build volumes and process stability, enabling the production of large structural components using concrete, polymer composites, and metallic alloys. These innovations reduce reliance on traditional tooling, molds, and fixtures, thus accelerating prototyping and low-volume production in industries such as aerospace, automotive, and heavy equipment manufacturing.

The development of gantry-based systems and multi-axis robotic architectures has expanded LFAM's application beyond controlled factory environments, allowing operations in outdoor, on-site, and challenging environments relevant to construction, defense logistics, and infrastructure maintenance. As a result, additive manufacturing is increasingly integrated into distributed production models for oversized components, further enhancing its commercial potential.

This technological progress is also expanding the market for capital equipment, process software, and qualified feedstock. Enhanced dimensional accuracy, repeatability, and material performance have enabled the transition from experimental prototypes to limited-series manufacturing and functional end-use parts. This transition fuels demand for high-value hardware, recurring materials, and specialized services such as design for additive manufacturing (DfAM), process qualification, and deployment support.

In November 2025, KraussMaffei launched the Power Print Flex modular robotic LFAM system at Formnext, demonstrating significant advancements in hardware design, throughput, and material processing for advanced polymers. This launch underscores the maturation of gantry/robotic systems and the ongoing shift towards industrialized production of large, lightweight components with improved scalability and reliability.

Throughput Limitations and Industrial-Scale Scalability Constraints

Despite rapid advances, macroscale 3D printing remains limited in production throughput and scalability for high-volume manufacturing. The layer-by-layer deposition process is inherently slower than traditional subtractive methods such as injection molding or CNC machining, making it unsuitable for applications requiring high-cycle, consistent production. As a result, large-format additive manufacturing is primarily used for prototyping, tooling, and low- to medium-volume production rather than mass manufacturing.

The economic challenges further hinder widespread adoption. While additive processes excel in customization and rapid iteration, their per-unit costs do not decrease with volume like conventional methods. As output scales, cycle time, machine utilization, and post-processing demands grow linearly, diminishing the advantages of tooling-free production. In high-throughput industries such as automotive and consumer goods, where efficiency and cost are paramount, macro 3D printing struggles to meet production needs, limiting its application to niches where flexibility and design freedom outweigh volume efficiency.

Intelligent Automation via AI–Robotics Convergence

The integration of large-format additive manufacturing (LFAM) with artificial intelligence (AI) and industrial robotics is driving substantial growth in macro-scale production environments. AI-enabled in-process sensing and analytics enable real-time interpretation of thermal profiles, deposition geometry, and interlayer bonding, thereby enabling closed-loop adjustments during fabrication. This enhances first-pass yield, stabilizes process windows, and reduces material waste and rework.

By streamlining commissioning and calibration, intelligent automation minimizes operational risk and variability, addressing challenges that have previously limited adoption among non-specialist manufacturers. As AI-driven monitoring, control, and fault detection become embedded at the system level, LFAM is transitioning from a skill-intensive, operator-dependent process to a more standardized, repeatable industrial production method.

Robotic integration further boosts these improvements, enabling multi-axis deposition, automated part transfer, and in-line finishing within unified production cells. Coordinated control of deposition, handling, and post-processing minimizes manual intervention and enhances throughput consistency across large build volumes. The combination of AI-driven quality assurance and robotic coordination addresses scalability issues, including shortages of skilled operators and performance degradation during extended build times.

Platforms that integrate adaptive control software with robotic motion systems improve equipment utilization, uptime, and cost predictability. In November 2025, Base Materials launched a large-format 3D printing service using the ProXtrude paste system, reducing waste by 58% and production time by 70%. This innovation enables complex, single-piece components with minimal post-processing, supporting the shift toward standardized, industrialized additive manufacturing workflows enabled by advanced automation.

Category–wise Analysis

Component Insights

The hardware segment is projected to dominate, accounting for around 63% of overall demand in 2026, as industrial users continue to prioritize control over throughput, quality, and qualification. Key sectors such as aerospace, automotive, energy, and construction will likely lead the way, with platforms from companies such as Stratasys, 3D Systems, and GE Additive anchoring large-format workflows. Emphasis will be on improving deposition rates, closed-loop calibration, multi-axis architectures, and integrating pellet extrusion and CNC finishing to lower costs and boost repeatability.

Hardware adoption will also benefit from certification-ready ecosystems (AS9100, ISO/ASTM, UL94), supporting end-use production rather than just prototyping. Policy-driven localization and defense qualification programs will sustain capital investment, while AI-driven monitoring and automated systems will reduce scrap and improve production efficiency.

3D printing services will experience the fastest growth, driven by a shift toward on-demand manufacturing, balance-sheet flexibility, and access to specialized expertise. Companies such as Protolabs, Materialize, and Xometry will expand multi-material, multi-process offerings, bundling design validation, post-processing, and compliance documentation into one contract. Enterprises will increasingly favor services to avoid hardware obsolescence and workforce shortages, while AI-driven solutions improve turnaround times and predict failures.

Healthcare and regulated industries are expected to accelerate adoption through patient-specific devices, certified production cells, and GMP-aligned workflows, increasing switching costs and driving broader use cases.

Material Type Insights

Polymers are expected to remain the dominant material segment, accounting for approximately 44% of overall demand in 2026, owing to their versatility, cost-effectiveness, and ease of large-scale processing. Adoption will continue to be strongest in prototyping, tooling, fixtures, and lightweight functional parts, where rapid iteration and low scrap risk are more critical than ultimate strength. Advances in polymer development will focus on higher-performance resins with better flame resistance and thermal stability, enabling use in transportation interiors and industrial enclosures. Sustainability considerations will play a larger role in purchasing decisions, with bio-based and recycled feedstocks gaining traction in sectors, including construction and visual manufacturing.

The expansion of pellet-fed extrusion platforms will improve throughput and reduce material costs, supporting larger parts and longer build cycles. Material portfolios will grow to include flexible, high-temperature, and biocompatible grades, allowing one material class to serve diverse industries such as healthcare, automotive, and industrial tooling. This combination of performance, flexibility, and accessible ecosystems will continue to make polymers the anchor of large-scale additive manufacturing.

Metals and alloys are projected to be the fastest-growing material segment, driven by their critical role in high-value, structural, and mission-critical components. Aerospace, energy, and heavy equipment industries will push for metal additive to optimize weight, consolidate parts, and shorten supply chain cycles. Advancements in deposition rates, multi-source energy delivery, and wire-based processes will enable larger parts and faster production. Development will focus on improving crack resistance and consistency in high-strength aluminum and steel, advancing metal additive into end-use production, and accelerating its adoption over polymers.

Regional Insights

North America Macro 3D Printing Market Trends

North America is expected to lead, holding close to 37% of global revenue in 2026 as adoption shifts from prototyping toward industrial-scale production. The U.S. is likely to continue anchoring this position through sustained investment from defense and aerospace programs, where large-format additive manufacturing is used for lightweight structures, tooling, and mission-critical components. The NASA and the U.S. Department of Defense are anticipated to keep expanding qualified use cases, which should accelerate the demand for high-throughput metal and polymer systems.

The presence of core technology developers such as Stratasys, 3D Systems, and HP also positions the U.S. as the primary innovation hub for next-generation Macro-printers and materials. Canada is expected to strengthen its role in aerospace and industrial tooling applications, while Mexico is likely to benefit from nearshoring trends that push automotive and industrial suppliers to adopt large-format additive manufacturing for localized production.

Investment behavior in the region is likely to remain consolidation-driven, with platform players pursuing acquisitions to integrate hardware, software, and materials into scalable production ecosystems. The market is also expected to see faster uptake of AI-enabled process control and IoT-based monitoring, particularly in U.S. factories targeting repeatable, high-volume output. As supply chains continue to localize, North America is anticipated to prioritize Macro-3D printing for rapid tooling, low-volume end-use parts, and large structural components, reinforcing its leadership position over the medium term. Regulatory frameworks are expected to shape commercialization pathways, with FDA guidance influencing medical device validation, FAA certification requirements extending qualification timelines and costs for flight-critical parts, and ISO/ASTM 52900 standards becoming embedded in defense and industrial contracts.

Europe Macro 3D Printing Market Trends

Europe is anticipated to maintain its position as the second-largest, accounting for approximately 31% of the global share. The region is likely to benefit from a strong industrial base, particularly in Germany, Italy, and the Benelux countries, where OEMs are adopting additive manufacturing to achieve lightweighting, production flexibility, and supply chain localization.

Key growth drivers are expected to include aerospace and automotive adoption, hospital deployment of point-of-care print labs, and the integration of Industry 4.0 technologies such as AI-driven process optimization, hybrid additive-subtractive workflows, and predictive maintenance across production lines. Localized production initiatives, accelerated by the EU Carbon Border Adjustment Mechanism, are likely to encourage the reshoring of high-value components, reducing lead times while meeting carbon neutrality goals.

Country-level developments are anticipated to shape Europe’s market dynamics further. Germany is likely to continue leading in patents, automation expertise, and adoption of high-volume industrial 3D printing in automotive and aerospace. The Netherlands is expected to post the fastest growth due to strong logistics clusters, maritime industries, and innovation funding. France and Italy are likely to accelerate adoption via government-backed innovation hubs and industrial 4.0 investments, while the UK will continue as a significant ecosystem for startups and R&D partnerships. Leading vendors such as EOS GmbH, SLM Solutions, Materialize, Renishaw, and Trumpf are expected to anchor regional growth through high-tech industrial solutions and material innovations.

Asia Pacific Macro 3D Printing Market Trends

Asia Pacific is set to be the fastest-growing region, fueled by robust industrial growth, government-backed initiatives, and a rising embrace of advanced manufacturing sectors. The region's vast manufacturing base, coupled with government programs such as "Smart Factory" and production-linked incentives, positions it as a key player in electronics, automotive, and healthcare. This growth is also driven by the need for resilient supply chains, cost-efficient localized production, and urbanization, pushing demand for smart infrastructure. As equipment and material costs decline, 3D printing becomes more accessible for SMEs in India, Southeast Asia, and other emerging markets, further supporting adoption.

China remains the dominant market, with substantial investments in industrial-scale production, construction-scale 3D printing, and semiconductor integration. Japan, South Korea, and Taiwan are expected to lead in electronics and micro-scale additive manufacturing, including PCBs and medical applications. India, however, is emerging as the fastest-growing market, driven by the “Make in India” initiative and the Production Linked Incentive (PLI) scheme, alongside a surge in domestic healthcare applications like patient-specific implants. India’s adoption in both healthcare and industrial production is expected to accelerate due to favorable policy support and the rise of local AM hardware manufacturers. Key regional players include BLT, Farsoon Technologies, and Wipro 3D.

Competitive Landscape

The global 3D printing market is moderately fragmented but consolidating at the top, with Stratasys, 3D Systems, EOS, HP, and GE Additive accounting for 45–50% of total revenue. These leaders benefit from diversified portfolios across polymer, metal, and hybrid technologies, strategic acquisitions, and strong industrial client bases in aerospace, defense, and healthcare. The rest of the market is divided among niche players in bio-printing, construction, and ultra-large-format printing, alongside desktop and low-volume manufacturers. Competition focuses on material openness, print speed, and integrated software ecosystems, with AI, IoT, and Manufacturing-as-a-Service (MaaS) platforms enhancing operational efficiency and customer retention.

Regionally, North America remains the largest market, driven by aerospace and defense, while Asia Pacific is the fastest-growing, fueled by China’s initiatives and India’s industrial expansion. Key industrial players include Stratasys (polymer AM), 3D Systems (stereolithography), EOS (metal laser sintering), HP (MJF/Metal Jet), and GE Additive (EBM). Disruptors such as Voxeljet, BigRep, and Wipro 3D are shaping niche markets.

Key Industry Developments:

- In September 2025, CEAD partnered with RusselSmith to introduce large-format 3D printing in West Africa, driving localized sustainable manufacturing in energy, maritime, and construction, while boosting supply chain resilience and rapid prototyping in emerging markets.

- In August 2025, COBOD enabled the creation of fire-resistant 3D-printed homes in Colorado, using A1-rated concrete walls to enhance safety and durability in wildfire-prone areas.

- In July 2025, ICON launched affordable 3D-printed homes for sale and broke ground in Austin's Mueller Community, advancing housing affordability with eco-friendly, rapidly constructed homes under US$200K to tackle urban housing shortages.

Companies Covered in Macro 3D Printing Market

- Stratasys Ltd

- 3D Systems Corp.

- GE Additive

- BigRep GmbH

- Titan Robotics

- ICON Technology

- COBOD International

- CEAD Group Specialists

- voxeljet AG

- EOS GmbH

- SLM Solutions

- HP Inc.

- Materialize NV

- Renishaw plc

- Desktop Metal

Frequently Asked Questions

The global macro 3D Printing market is projected to be valued at US$17.6 billion in 2026 and is expected to reach US$35.4 billion by 2033, driven by the industrialization of additive manufacturing and advancements in print speed and material performance.

This shift is fueled by significant improvements in print speed, repeatability, and material properties (especially in high-performance thermoplastics and metal alloys), which enable the direct, cost-effective production of end-use functional parts for industries such as aerospace, automotive, and healthcare.

The macro 3D printing market is forecast to grow at a CAGR of 10.5% from 2026 to 2033, reflecting its expanding role in industrial-scale manufacturing.

North America is the leading regional market, accounting for approximately 37% of global revenue, supported by high-value industrial applications in aerospace and automotive, strong innovation ecosystems, and significant investment in AI-enabled process control and localized production.

The macro 3D printing market is moderately consolidated, with key players including Stratasys Ltd., 3D Systems Corp., GE Additive, EOS GmbH, and HP Inc. competing on technology portfolios, material ecosystems, and integrated software solutions.