- Medical Devices

- Lensometer Market

Lensometer Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Lensometer Market by Product (Manual Lensometer and Automated Lensometer), by Application (Vision Testing, Lens Verification, and Lens Measurement), by End User (Hospitals, Ophthalmic Clinic, Optical Stores, Academic and Research Institutes, and Others), and Regional Analysis from 2026 to 2033

Lensometer Market Share and Trend Analysis

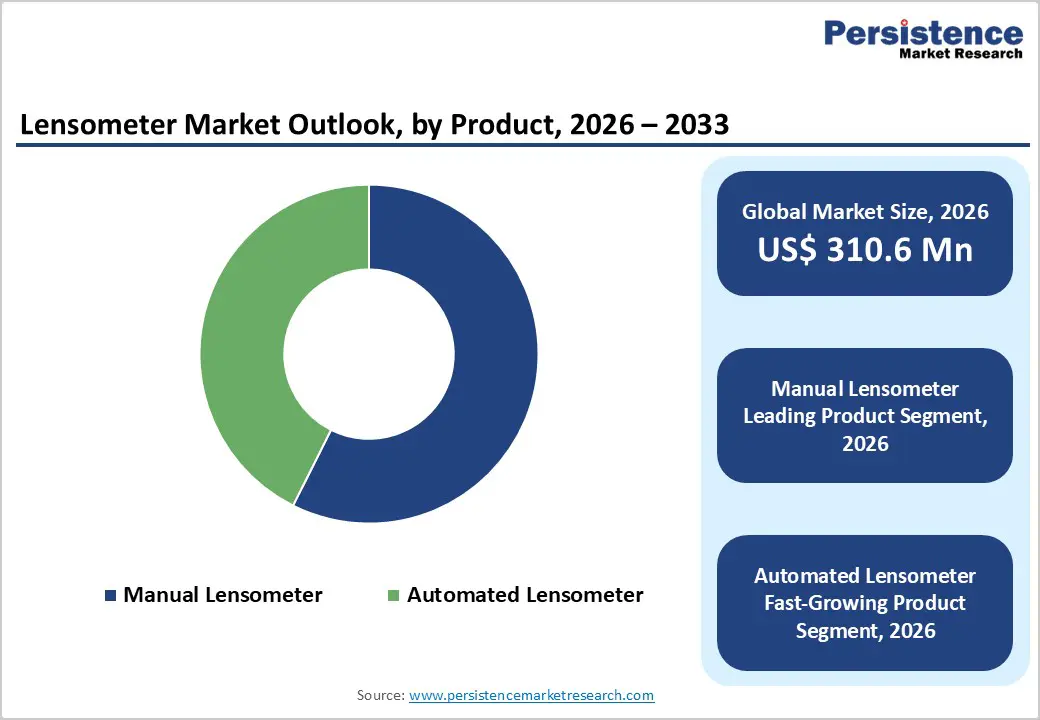

The global Lensometer Market size is estimated to grow from US$ 310.6 Mn in 2026 to US$ 510.2 Mn by 2033. The market is projected to record a CAGR of 5.3% during the forecast period from 2026 to 2033.

Global demand for lensometers is increasing steadily, driven by the rising prevalence of vision disorders such as myopia, hyperopia, astigmatism, and presbyopia, as well as growing awareness of the importance of routine eye examinations and prescription accuracy. Increasing screen exposure, aging populations, and lifestyle-related visual strain are expanding the need for corrective eyewear, thereby supporting sustained demand for lens measurement and verification equipment. Lensometers are widely used across hospitals, ophthalmic clinics, and optical stores to ensure precise lens power measurement, prism correction, and axis alignment during vision testing and dispensing workflows. Growing emphasis on preventive eye care, early diagnosis of refractive errors, and quality assurance in optical dispensing is further accelerating adoption. The expansion of optical retail chains, increased availability of in-store eye testing services, and rising penetration of optometry clinics are driving global market growth. Technological advancements, including the transition from manual to automated and digital lensometers, are improving measurement accuracy, operational efficiency, and workflow integration. Additionally, expanding healthcare infrastructure in emerging markets and rising investments in ophthalmic diagnostics are reinforcing long-term demand for lensometers worldwide.

Key Industry Highlights

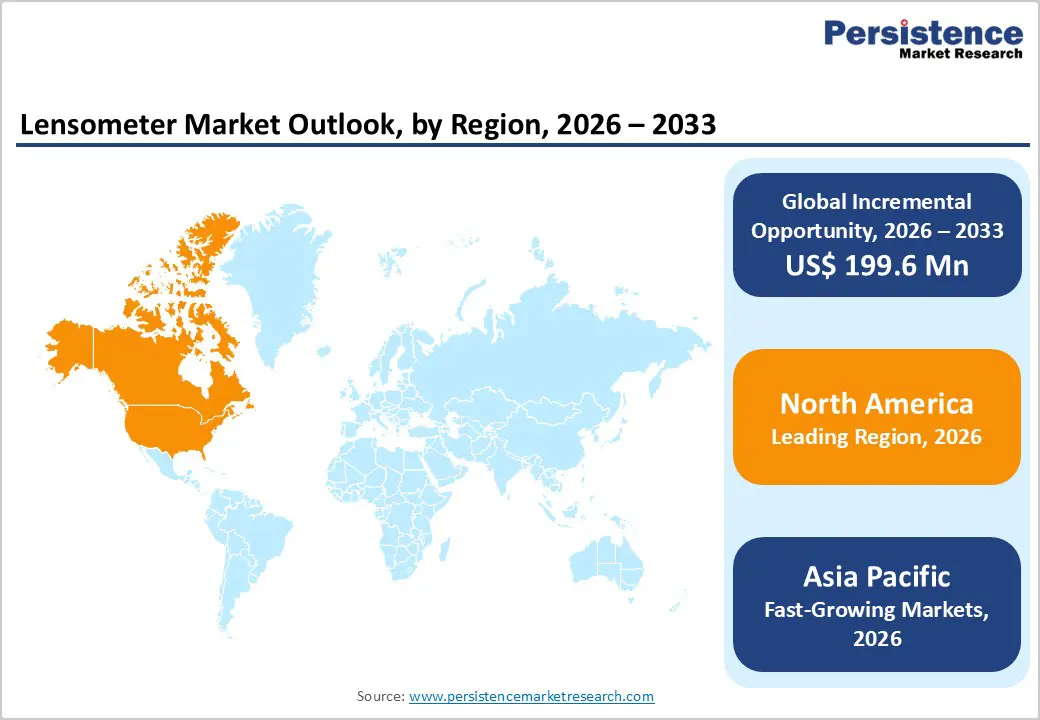

- Leading Region: North America holds the largest share at 47.3%, supported by high awareness of eye health, strong purchasing power, advanced ophthalmic infrastructure, widespread optometry services, and high adoption of diagnostic equipment across hospitals and optical retail chains.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rising prevalence of refractive errors, increasing disposable incomes, rapid urbanization, expanding optical retail networks, government-led vision screening programs, and improving access to eye care services.

- Leading Product Segment: Manual lensometers dominate the market due to operational simplicity, cost-effectiveness, durability, and widespread adoption in small optical stores, clinics, and educational institutions.

- Fastest-Growing Product Segment: Automated lensometers are growing rapidly as providers seek higher accuracy, faster measurement, reduced operator dependency, and digital integration in high-volume clinical and retail settings.

- Leading Application Segment: Vision testing remains the top segment, driven by high volumes of routine eye examinations and increasing demand for accurate prescription validation.

- Fastest-Growing Application Segment: Lens verification is growing rapidly as optical chains prioritize quality control, prescription accuracy, and standardized dispensing practices.

| Global Market Attributes | Key Insights |

|---|---|

| Lensometer Market Size (2026E) | US$ 310.6 Mn |

| Market Value Forecast (2033F) | US$ 510.2 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Dynamics

Driver - Rising Prevalence of Vision Disorders, Growth of Optical Retail, and Technological Advancements

Growth is primarily driven by the increasing global prevalence of refractive errors such as myopia, hyperopia, presbyopia, and astigmatism, which continues to expand the population requiring corrective eyewear. Rising screen exposure, digital device use, and an aging population are significantly increasing the need for routine eye examinations and prescription updates, directly boosting demand for accurate lens measurement tools. Lensometers play a critical role in verifying lens power, alignment, and prism correction during vision assessments, making them indispensable in optical and clinical workflows.

The rapid expansion of optical retail chains, standalone optometry clinics, and in-store eye testing services is further accelerating adoption. Optical stores increasingly rely on efficient and reliable lensometers to support high patient throughput and ensure prescription accuracy. In parallel, technological advancements, particularly the shift from manual to automated and digital lensometers, are improving measurement precision, reducing human error, and enhancing workflow efficiency. Integration with electronic health records and other diagnostic devices is strengthening clinical utility. Growing awareness of preventive eye care, increased access to vision screening programs, and rising healthcare spending in both developed and emerging markets continue to reinforce demand. Together, these factors are creating sustained momentum for lensometer adoption across hospitals, clinics, and optical retail environments.

Restraints - High Equipment Costs, Limited Adoption in Low-Resource Settings, and Training Requirements

The market faces restraints related to the high initial cost of advanced and automated lensometers, which can limit adoption among small optical stores, independent clinics, and facilities in price-sensitive regions. While manual lensometers remain affordable, the growing preference for automated systems presents budget challenges for end users with limited capital expenditure capacity. Ongoing maintenance costs, calibration requirements, and occasional software upgrades further increase the total cost of ownership.

Limited access to trained professionals also acts as a barrier, particularly for digital lensometers that require familiarity with software interfaces and interpretation of automated readings. Inconsistent training standards across regions can lead to underutilization of advanced features, reducing perceived value. Additionally, in rural and underserved areas, basic vision-testing infrastructure may still be lacking, thereby constraining demand for diagnostic equipment. Procurement delays in public hospitals, dependence on distributors, and long replacement cycles for durable diagnostic devices can slow market expansion. Regulatory compliance requirements and certification processes across different countries may also extend product approval timelines. Collectively, these factors create challenges in accelerating adoption, particularly in emerging markets where affordability and skill availability remain key concerns.

Opportunity - Automation, Expansion in Emerging Markets, and Integration with Digital Eye Care

Significant growth opportunities are emerging from increasing automation in ophthalmic diagnostics and expanding eye care infrastructure in emerging markets. Automated and digital lensometers offer faster measurements, improved accuracy, and reduced operator dependency, making them attractive to high-volume optical chains and hospitals. Continuous innovation in compact, user-friendly designs and software-enabled features is expected to accelerate the replacement of older manual systems.

Emerging economies across Asia Pacific, Latin America, and the Middle East present strong untapped potential due to rising awareness of eye health, increasing prevalence of refractive disorders, and rapid expansion of optical retail networks. Government-led vision screening programs, school eye health initiatives, and improved access to optometry services are supporting early diagnosis and the adoption of corrective eyewear. The growing integration of lensometers with digital eye care platforms, electronic medical records, and tele-optometry solutions is opening new application avenues. Mobile and portable lensometers designed for outreach programs and remote settings further expand market reach. Additionally, partnerships between manufacturers, optical chains, and healthcare providers to standardize diagnostic workflows are strengthening demand. As vision care increasingly shifts toward efficiency, accuracy, and digital integration, lensometers are well-positioned to benefit from long-term structural growth trends.

Category-wise Analysis

By Product, Manual Lensometers Lead Due to Operational Simplicity, Cost-Effectiveness, and Strong Adoption in Routine Eye Care

Manual lensometers are projected to dominate the global lensometer market in 2026, accounting for 57.4% of revenue. Their dominance is primarily driven by ease of operation, minimal training requirements, and affordability compared to automated systems. Manual lensometers are widely preferred in small optical stores, independent optometry practices, academic institutions, and resource-limited healthcare settings where cost sensitivity remains high. These devices provide reliable measurements for single-vision and basic multifocal lenses, making them suitable for routine prescription verification. Their robust construction, low maintenance needs, and long operational lifespan further enhance adoption. Additionally, manual lensometers do not rely heavily on software or power stability, making them ideal for emerging markets and rural clinics. Continued demand from developing regions, combined with steady replacement cycles in mature markets, is expected to sustain manual lensometers' global leadership.

By Application, Vision Testing Leads Due to High Volume of Routine Eye Examinations and Prescription Verification

The vision testing segment is expected to dominate the global lensometer market in 2026, capturing 42.0% of revenue. This leadership is driven by the increasing frequency of routine eye examinations and the growing need for accurate prescription validation across optical and clinical settings. Lensometers play a critical role in confirming lens power, axis alignment, and prism correction during vision assessments, particularly for patients requiring corrective eyewear. Rising prevalence of refractive errors such as myopia, hyperopia, and astigmatism-especially among younger and working-age populations—continues to drive demand for vision testing services. Expansion of optical retail chains and in-store eye examination services further boosts usage. Additionally, increased awareness of regular eye health check-ups and preventive vision care is supporting sustained growth. As vision screening volumes rise globally, vision testing remains the largest application area for lensometers.

By End User, Hospitals Lead Due to High Patient Footfall and Integrated Ophthalmic Diagnostic Infrastructure

Hospitals are projected to dominate the global lensometer market in 2026, accounting for 28.0% of revenue. This dominance is attributed to high patient inflow, availability of comprehensive ophthalmic diagnostic services, and the presence of trained eye-care professionals. Hospitals routinely use lensometers for pre- and post-consultation verification of corrective lenses, particularly for surgical patients and individuals with complex vision conditions. Integration of lensometers within broader ophthalmology departments enhances diagnostic accuracy and workflow efficiency. Additionally, hospitals benefit from higher procurement budgets, enabling regular equipment upgrades and the adoption of multiple units across departments. Strong trust in hospital-based eye care services further supports utilization. While optical stores and clinics are growing rapidly, hospitals continue to lead due to institutional purchasing power, standardized clinical protocols, and consistent demand for reliable diagnostic equipment.

Region-wise Insights

North America Lensometer Market Trends

North America is expected to dominate the global lensometer market, with a 47.3% share in 2026, led primarily by the United States. The region benefits from a well-established eye care ecosystem, high awareness of vision health, and widespread access to optometry and ophthalmology services. The high prevalence of refractive disorders, the aging population, and the extensive use of corrective eyewear continue to drive demand for accurate lens measurement tools.

Strong presence of leading manufacturers and distributors ensures rapid availability of advanced and conventional lensometer models across hospitals, clinics, and optical retail chains. Favorable reimbursement structures, regular vision screening programs, and emphasis on preventive eye care further support market growth. Additionally, early adoption of technological advancements and frequent equipment replacement cycles sustain demand. High purchasing power and preference for precision diagnostic tools are expected to maintain North America’s leadership position throughout the forecast period.

Europe Lensometer Market Trends

The Europe lensometer market is expected to grow steadily, supported by strong ophthalmic care standards and increasing demand for vision correction services across countries such as Germany, the U.K., France, Italy, and Spain. The region benefits from robust healthcare infrastructure, strict regulatory compliance, and high trust in clinically validated ophthalmic equipment. The rising aging population and increasing incidence of age-related vision disorders are driving routine eye examinations and corrective lens usage.

Hospitals and optical chains across Europe continue to invest in reliable diagnostic tools to maintain accuracy and efficiency. Additionally, the expansion of private eye clinics and optical franchises is strengthening demand for both manual and automated lensometers. Preference for durable, high-quality equipment and growing focus on preventive eye care further support market stability. As access to vision care improves and screening programs expand, Europe is expected to maintain consistent long-term growth.

Asia Pacific Lensometer Market Trends

The Asia Pacific lensometer market is expected to register a relatively higher CAGR of around 7.2% between 2026 and 2033, driven by expanding healthcare infrastructure, rising awareness of eye health, and growing demand for corrective eyewear. Countries such as China, India, Japan, South Korea, and Australia are witnessing an increasing prevalence of refractive errors due to digital screen exposure, urban lifestyles, and aging populations. Rapid expansion of optical retail chains and private eye clinics is significantly increasing demand for lensometers. Improving affordability and the availability of cost-effective manual devices, along with rising penetration of automated systems, are enhancing market accessibility.

Government initiatives to improve vision screening and school eye health programs further contribute to growth. Additionally, local manufacturing and the entry of global players are strengthening regional supply. With rising disposable income and healthcare access, the Asia Pacific is expected to emerge as the fastest-growing regional market.

Market Competitive Landscape

The global lensometer market is highly competitive, with strong participation from companies such as Topcon Corporation, Nidek Co., Ltd., Reichert Technologies, Marco Ophthalmic, Inc., and Keeler Ltd. These players leverage extensive global distribution networks, strong brand equity, and broad ophthalmic and optometry-focused product portfolios to address the growing demand for accurate and efficient lens measurement and verification solutions.

Their offerings emphasize high measurement precision, automation and digital integration, ease of operation, workflow efficiency, and compatibility with a wide range of ophthalmic lenses, including single-vision, bifocal, and progressive lenses. Continuous technological innovation, compliance with regulatory and optical standards, product reliability, and adherence to international quality and manufacturing norms remain critical to sustaining competitive positioning in the global lensometer market.

Key Industry Developments:

- In November 2025, Visionix USA will introduce the VX 40 Couture at Vision Expo West (September 18-21, Las Vegas), a next-generation automated lensmeter designed for fast and accurate lens verification. The system delivers one-touch operation, completes full lens analysis in about 30 seconds, measures key optical parameters, provides real-time 1:1 visualization, and generates instant compliance reports to support quality assurance and reduce remakes.

- In April 2025, the LM-100 auto lensometer received a software upgrade featuring a refreshed user interface, with the measurement screen transitioning from light blue to a deeper blue for improved visibility. The alignment markers were also enhanced, changing from pale blue to bright fluorescent green, resulting in a clearer, more intuitive, and user-friendly measurement experience.

Companies Covered in Lensometer Market

- Topcon Corporation

- Nidek Co., Ltd.

- Reichert Technologies

- Marco Ophthalmic, Inc.

- Keeler Ltd.

- Oculus Optikgeräte GmbH

- Huvitz Co., Ltd.

- Takagi Seiko Co., Ltd.

- Visionix

- Righton Limited

- Luneau Technology

- Ningbo FLO Optical

- Others

Frequently Asked Questions

The global lensometer market is projected to be valued at US$ 310.6 Mn in 2026.

The global lensometer market is driven by the rising prevalence of vision impairments and refractive errors worldwide, growing aging populations increasing demand for accurate lens prescription measurements, and technological advancements transitioning from manual to automated digital devices that enhance precision and workflow efficiency.

The global lensometer market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Key market opportunities include expansion into emerging markets with developing eye-care infrastructure and integration of lensometers with tele-ophthalmology and portable diagnostic solutions to broaden accessibility and remote care capabilities.

Topcon Corporation, Nidek Co., Ltd., Reichert Technologies, Marco Ophthalmic, Inc., and Keeler Ltd. are some of the key players in the lensometer market.