- Beverages

- Kombucha Market

Kombucha Market Size, Share, and Growth Forecast, 2026 – 2033

Kombucha Market by Product Type (Hard, Conventional), Nature (Flavor, Unflavored), Sales Channel (Supermarkets/Hypermarkets, Specialist Stores, Convenience Stores, Online Retail, Others), and Regional Analysis for 2026 – 2033

Kombucha Market Size and Trends Analysis

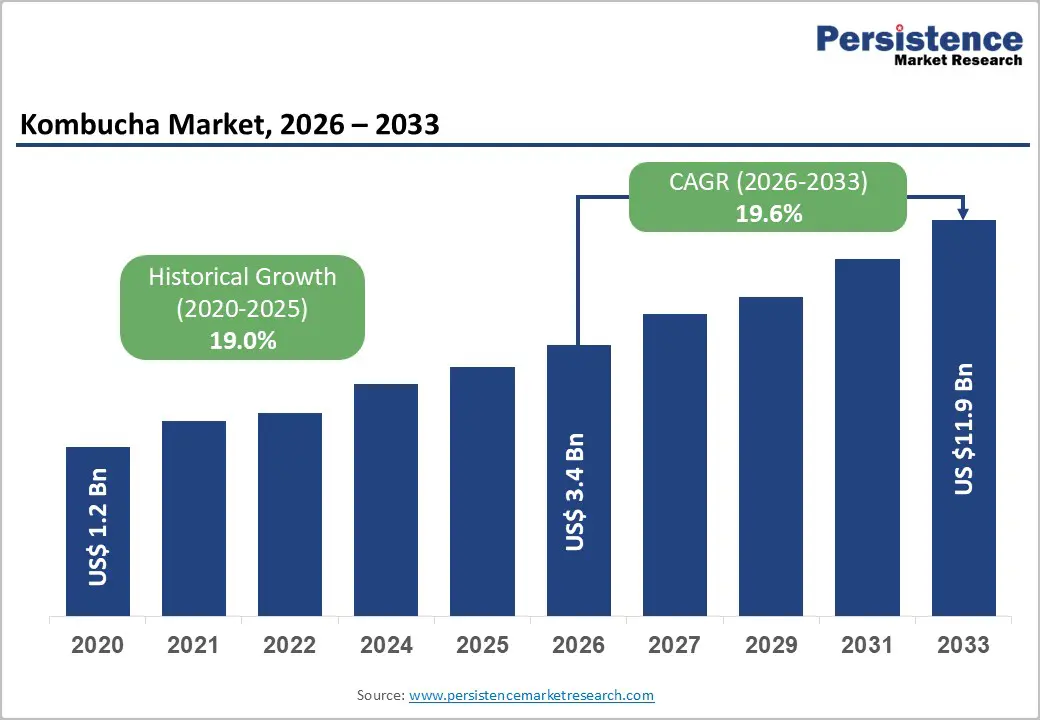

The global kombucha market size is likely to be valued at US$3.4 billion in 2026, and is expected to reach US$11.9 billion by 2033, growing at a CAGR of 19.6% during the forecast period from 2026 to 2033, driven by the increasing prevalence of health-conscious consumer behavior, rising demand for functional beverages with probiotic and low-sugar profiles, and growing mainstream acceptance of fermented drinks as everyday refreshment alternatives.

Growing demand for flavored and hard kombucha variants, especially through online retail and specialist stores, is accelerating adoption across sales channels. Advances in low-alcohol hard kombucha and clean-label unflavored formulations are further boosting uptake by offering better taste and regulatory compliance. Increasing recognition of kombucha as a critical gut-health and immunity-supporting beverage in emerging wellness markets remains a major driver of market growth.

Key Industry Highlights:

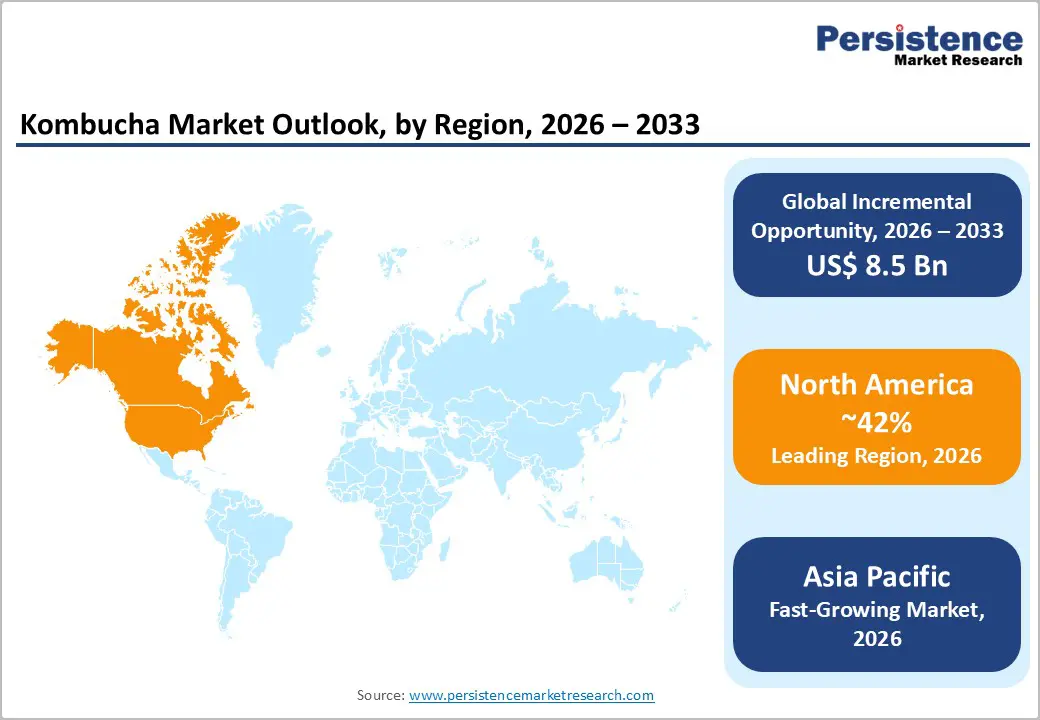

- Leading Region: North America, anticipated to account for a 42% market share in 2026, driven by high per-capita consumption, strong clean-label trends, and premium demand in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rising middle-class health awareness, rapid expansion of modern retail, and growing investments in local kombucha brands in China and India.

- Dominant Product Type: Conventional, to hold approximately 78% of the market share, as it remains the core volume driver in mass retail.

- Leading Nature: Flavor accounts for over 68% of the market revenue, due to superior taste appeal and variety-seeking behavior.

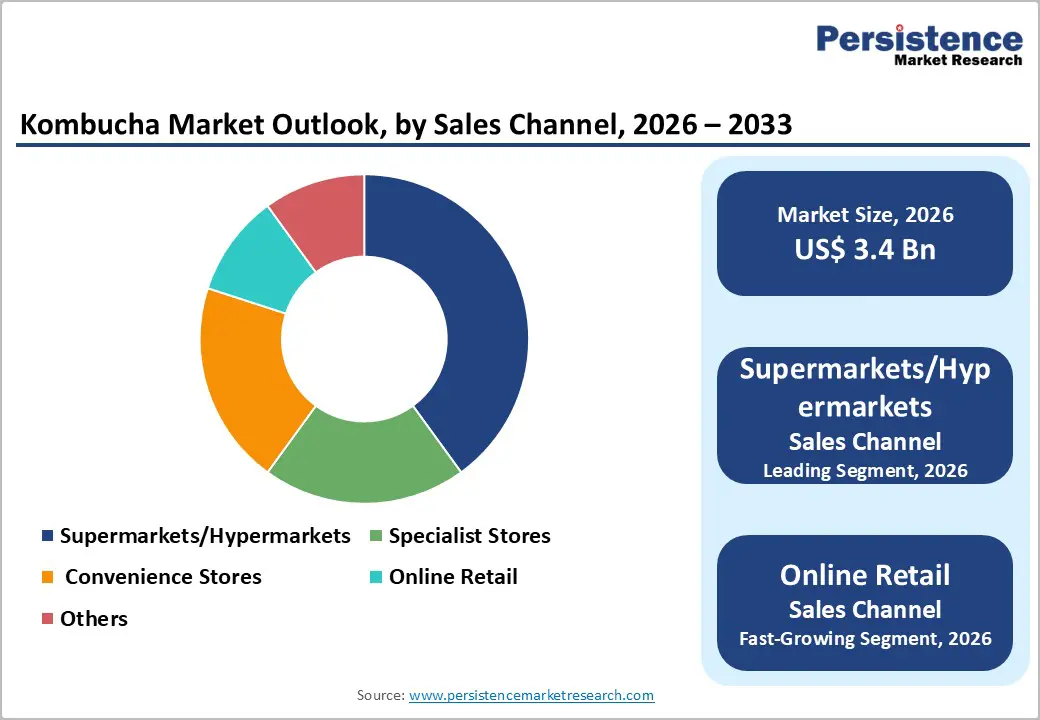

- Leading Sales Channel: Supermarkets/Hypermarkets, contributing nearly 40% of the market revenue, due to broad physical availability and impulse purchases.

| Key Insights | Details |

|---|---|

| Kombucha Market Size (2026E) | US$3.4 Bn |

| Market Value Forecast (2033F) | US$11.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 19.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 19.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Health-Conscious Consumer Behavior and Functional Probiotic Beverages

The rising awareness of health and wellness among consumers has significantly reshaped dietary preferences, leading to a growing demand for functional beverages, particularly those containing probiotics. Modern consumers are increasingly seeking products that not only satisfy thirst but also provide tangible health benefits, such as improved digestive health, enhanced immunity, and overall gut balance. This shift is driven by greater access to information on nutrition, the influence of social media, and a broader cultural focus on preventive health measures.

Probiotic beverages, which contain live beneficial microorganisms, have emerged as a popular choice in this context. They appeal to consumers looking for natural, non-pharmaceutical ways to support gut health. Ingredients such as yogurt cultures, kefir, kombucha, and fortified plant-based alternatives are being incorporated to meet diverse dietary needs, including vegan and lactose-intolerant populations.

Flavor innovation, low sugar content, and clean-label formulations are making these beverages more attractive to mainstream consumers. Manufacturers are responding by expanding product portfolios, emphasizing transparency in labeling, and investing in marketing strategies that highlight scientifically backed health claims.

Regulatory Scrutiny on Alcohol Content and Shelf-Life Challenges

The functional beverage market, particularly probiotic drinks, faces increasing regulatory scrutiny, especially regarding alcohol content and shelf-life stability. Many probiotic beverages, such as kombucha, naturally produce small amounts of alcohol during fermentation. Even minimal alcohol levels can trigger strict regulations in different countries, affecting labeling, distribution, and sales.

Manufacturers must ensure that products comply with local laws governing permissible alcohol percentages, often requiring rigorous testing, documentation, and periodic audits. Failure to meet these requirements can result in fines, recalls, or restrictions on market access.

Shelf-life challenges add another layer of complexity. Probiotics are live microorganisms that can be highly sensitive to temperature, pH, and storage conditions. Maintaining microbial viability over the product’s intended shelf life is crucial to ensure health benefits and regulatory compliance.

Extended shelf-life demands careful formulation, optimized packaging, and cold-chain management, increasing production and logistical costs. Preservatives, if used, must meet food safety standards without compromising the functional integrity of the beverage.

Expansion in Hard Kombucha Expansion and Functional Ingredient Fortification

The kombucha market is witnessing significant opportunities through the expansion of hard kombucha and the fortification of functional ingredients. Hard kombucha, which contains low levels of alcohol, is attracting consumers who seek a healthier alternative to traditional alcoholic beverages.

It combines the probiotic and health benefits of traditional kombucha with the social and recreational appeal of alcoholic drinks, appealing particularly to millennials and health-conscious adults. As lifestyle trends increasingly favor moderation and functional wellness, hard kombucha presents a unique niche that blends enjoyment with perceived health benefits.

Fortifying kombucha with functional ingredients is driving product differentiation and value addition. Ingredients such as adaptogens, herbal extracts, vitamins, antioxidants, and electrolytes enhance both the health appeal and taste profile of the beverage. This allows brands to target specific consumer needs, from stress reduction and energy boosting to digestive support and immunity enhancement.

Functional fortification also supports premium pricing strategies, as consumers are willing to pay more for beverages with added health benefits. Manufacturers are leveraging these trends by developing innovative formulations, experimenting with diverse flavor profiles, and optimizing fermentation processes to ensure product quality and consistency.

Category-wise Analysis

Product Type Insights

The conventional segment is anticipated to lead the market, holding 78% of the share in 2026. Its strong position is driven by established consumer familiarity, wide availability, and trusted flavor profiles that appeal to mainstream audiences. Traditional formulations, with their natural fermentation and probiotic benefits, remain the preferred choice for health-conscious consumers seeking gut health support without the alcohol content found in hard variants.

Conventional kombucha benefits from extensive distribution across retail, cafes, and online platforms, making it highly accessible. GT’s Living Foods is widely recognized as one of the top conventional kombucha brands globally. It was founded by GT Dave and has grown from small-batch brewing to producing over one million bottles per year, with an estimated ~40% share of the U.S. kombucha market owing to its strong brand recognition and wide retail distribution across grocery stores and supermarkets.

The hard segment is likely to be the fastest-growing product type, due to its unique combination of health benefits and recreational appeal. Unlike conventional kombucha, hard varieties contain low levels of alcohol, attracting consumers who seek a healthier alternative to traditional alcoholic beverages without compromising on social enjoyment. This trend is especially pronounced among millennials and Gen Z, who value moderation, wellness, and functional nutrition.

Brands are innovating with bold flavors, premium ingredients, and convenient packaging, which fuels trial and repeat purchases. San Diego-based Hard Kombucha brand JuneShine unveils its latest, highly anticipated innovation, JuneShine100: a better-for-you alcoholic beverage with only 100 calories and 1 gram of sugar per can. JuneShine100 offers the same benefits and taste of JuneShine’s original flavors, it is gluten-free and made with real fruit, at a lower alcohol content of 4.2% ABV, and is organic and contains probiotics and antioxidants.

Nature Insights

The flavor segment is expected to lead the market, with over 68% of the share in 2026. This dominance is driven by consumers’ preference for superior taste, which enhances the overall drinking experience and encourages repeat purchases. A wide variety of flavor options, including fruit blends, herbal infusions, and exotic combinations, caters to variety-seeking behavior, keeping consumers engaged and curious.

Global demand for fruit-based beverages supports the growth of flavored kombucha, as fruit not only improves palatability but also adds perceived health benefits. Health-Ade Kombucha has become one of the best-selling kombucha brands globally, largely due to its flavorful fruit-forward variants such as Lemon Ginger, Pink Lady Apple, Pomegranate, and Citrus-Infused flavors, which attract consumers beyond traditional kombucha drinkers by balancing taste with health benefits.

The unflavored segment is likely to be the fastest-growing nature segment, as it appeals to consumers seeking pure, minimally processed beverages. Its simplicity highlights the authentic fermentation process and probiotic benefits without added flavors, sugars, or artificial ingredients, aligning with the growing demand for transparency and health-focused products.

Health-conscious individuals and wellness enthusiasts prefer unflavored variants for versatility, using them in smoothies, mocktails, or daily routines. Toyo Kombucha Original Kombucha 330ml and Plain Kombucha are examples of unflavored kombucha products offered without added fruit or exotic flavors, highlighting consumer interest in pure, minimally processed kombucha. These products focus on traditional fermentation with simple ingredients such as tea, live cultures, and sugar, with no added flavors, appealing to drinkers who prioritize clean-label and gut-health benefits.

Sales Channel Insights

Supermarkets/hypermarkets are expected to dominate the market, contributing nearly 40% of revenue in 2026. Their extensive reach, high foot traffic, and organized retail environment make them ideal channels for both established and emerging brands to showcase products. Consumers value the convenience of one-stop shopping, allowing them to explore multiple flavors and brands in a single visit.

Supermarkets and hypermarkets often run promotional campaigns, sampling programs, and loyalty incentives, which encourage trial and repeat purchases. Health-Ade is widely stocked in supermarket and hypermarket chains across the U.S. Health-Ade kombucha is available in thousands of mainstream retail outlets such as Whole Foods Market, Safeway/Albertsons, Kroger, Publix, and Target, helping the brand reach a broad consumer base through organized retail channels.

These partnerships illustrate how supermarkets drive visibility, accessibility, and sales for kombucha products by placing them in high-traffic refrigerated beverage aisles alongside other popular drinks.

Online retail represents the fastest-growing sales channel, due to increasing consumer preference for convenience, home delivery, and contactless shopping. E-commerce platforms allow consumers to explore a wider variety of brands, flavors, and package sizes than traditional retail, catering to trial and repeat purchases.

Subscription models and direct-to-consumer websites further enhance accessibility, enabling regular delivery of fresh, refrigerated kombucha. The channel also supports targeted marketing, personalized promotions, and consumer reviews, which influence purchasing decisions.

Remedy Kombucha, an Australian kombucha brand, has developed online subscription and direct-to-consumer delivery models, allowing customers to receive kombucha periodically at home rather than buying in stores. The company offers multipack subscriptions that can be delivered weekly, fortnightly, or monthly, which has boosted its online sales and consumer loyalty as demand for convenient e-commerce purchases grows.

Regional Insights

North America Kombucha Market Trends

North America is projected to dominate the market, capturing the 42% revenue in 2026, supported by the region’s high per-capita functional beverage consumption, strong clean-label trends, and high public awareness of gut-health benefits.

Distribution systems in the U.S. and Canada provide extensive support for kombucha programs, ensuring wide accessibility across flavored conventional, hard variants, and supplements populations. Increasing demand for hard, convenient, and easy-to-find forms is further accelerating adoption, as these formats improve social acceptability and reduce barriers associated with traditional soft drinks.

Innovation in kombucha technology, including stable hard fermentation, improved flavor delivery, and targeted functional enhancement, is attracting significant investments from both public and private sectors. Government initiatives and FDA campaigns continue to promote use against digestive risks, sugar concerns, and emerging wellness threats, creating sustained market demand. The growing focus on hard grades and specialty uses, particularly for evening consumption and others, is expanding the target applications for kombucha.

Europe Kombucha Market Trends

Europe is increasing awareness of probiotic benefits, strong regulatory systems, and government-led health & wellness programs. Countries such as Germany, the U.K., France, and the Netherlands have well-established retail frameworks that support routine kombucha consumption and encourage adoption of innovative beverage delivery methods, including kombucha. These functional formulations are particularly appealing for flavored populations, regulation-conscious consumers, and hard variant users, improving acceptance and coverage rates.

Technological advancements in kombucha development, such as enhanced fermentation, application-targeted delivery, and improved hard grades, are further boosting market potential. European authorities are increasingly supporting research and trials for kombucha against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, low-alcohol options is aligned with the region’s focus on preventive digestive health and reducing sugary drinks. Public awareness campaigns and promotion drives are expanding reach in both urban and rural areas, while brands are investing in flavors and novel variants to increase appeal.

Asia Pacific Kombucha Market Trends

Asia Pacific is likely to be the fastest-growing market for kombucha in 2026, driven by rising health awareness, increasing government initiatives, and expanding application programs across the region.

Countries such as China, India, Japan, and South Korea are actively promoting kombucha campaigns to address wellness growth and emerging functional beverage needs. Kombucha is particularly attractive in these regions due to its scalable administration, ease of adoption, and suitability for large-scale retail drives in both urban and rural populations.

Technological advancements are supporting the development of stable, effective, and easy-to-enjoy kombucha, which can withstand challenging climatic conditions and minimize flavor dependence. These innovations are critical for reaching domestic consumers and improving overall category coverage. Growing demand for flavored, conventional, and hard applications is contributing to market expansion.

Public-private partnerships, increased beverage expenditure, and rising investments in kombucha research and brewing capacity are further accelerating growth. The convenience of kombucha delivery, combined with improved taste and reduced risk of rejection, positions it as a preferred choice.

Competitive Landscape

The global kombucha market features competition between established fermented beverage pioneers and emerging premium & hard-focused brands. In North America and Europe, GT’s Living Foods and Health-Ade lead through strong brand equity, distribution networks, and retail partnerships, bolstered by innovative flavored and low-sugar programs.

In Asia Pacific, local brewers advance with localized flavors, enhancing accessibility. Hard kombucha delivery boosts adult appeal, cuts sugar risks, and enables mass integrations across channels. Strategic partnerships, collaborations, and acquisitions merge expertise, expand flavor portfolios, and speed market penetration. Functional formulations solve health perception issues, aiding penetration in mainstream wellness areas.

Key Industry Developments:

- In June 2025, Aldi stores introduced a range of new kombucha drinks from The Juice Company. The new offerings came in three fruity flavors: Passionfruit, Ginger & Lemon, and Wild Berry. These beverages, known for their health benefits, highlight live cultures that support a healthy gut. Consumer interest in gut health grew, reflected by a 26% increase in related Google searches in the UK over the past year, underscoring the rising demand for functional and wellness-oriented drinks in the supermarket sector.

- In May 2025, Boochcraft launched in Pennsylvania through a new partnership with Sarene Craft Beer Distributors, marking a key milestone in the brand’s East Coast expansion. This move significantly boosted the momentum of the hard kombucha category.

Companies Covered in Kombucha Market

- Kombucha Wonder Drink

- Makana Beverages LLC

- Kosmic Kombucha

- Live Soda LLC

- Reed’s Inc.

- Hudson River Foods

- KeVita LLC

- Carpe Diem

- NessAlla Kombucha

- Humm Kombucha LLC

- GT’s Living Foods

- Mojo Beverages

- Buchi Kombucha

Frequently Asked Questions

The global kombucha market is projected to reach US$3.4 billion in 2026.

Health-conscious consumer behavior and demand for functional probiotic beverages are key drivers.

The kombucha market is poised to witness a CAGR of 19.6% from 2026 to 2033.

Hard kombucha expansion and functional ingredient fortification are the key opportunities.

GT’s Living Foods, Health-Ade, Humm Kombucha LLC, Kevita LLC, and Buchi Kombucha are the key players.