- Semiconductor Materials & Components

- Interposer and Fan-out WLP Market

Interposer and Fan-out WLP Market Size, Share, and Growth Forecast for 2025 - 2032

Interposer and Fan-out WLP Market By Packaging Technology (Through-silicon Vias, Interposers, Fan-out Wafer-level Packaging), By Application (Logic, Imaging & Optoelectronics, Memory, MEMS/Sensors, LED, Power Analog & Mixed Signal, RF, Photonics) and Regional Analysis

Interposer and Fan-out WLP Market Outlook (2025 to 2032)

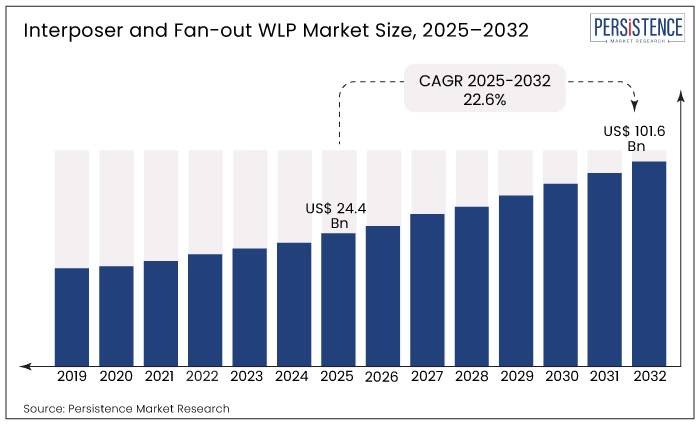

Global interposer and fan-out WLP sales revenue reached US$ 24.4 billion in 2025. Over the projection period (2025 to 2032), global demand for interposer and fan-out WLP is set to rise at 22.6% CAGR. By the end of 2032, the worldwide interposer and fan-out WLP market size is anticipated to reach US$ 101.6 billion.

Adoption of interposers and fan-out WLP is anticipated to remain high in consumer electronics sector. As per Persistence Market Research (PMR), consumer electronics segment is set to progress at 22.6% between 2025 and 2032. It will remain a key revenue-generation segment for interposer and fan-out WLP companies.

Key Market Shaping Factors:

- Growing need for advanced packaging technologies across several sectors like military and consumer electronics is set to drive the global market forward

- Rising trend of miniaturization of electronic devices to act as a catalyst triggering market expansion

- Growing usage of advanced wafer-level packaging technologies in MEMS and sensors to elevate demand

- Increasing usage of wearables and connected compact devices and wearables is projected to boost interposer and fan-out WLP sales revenue

- Rising usage of interposers in advanced electronic systems, especially 2.5D and 3D IC applications will create growth prospects for the market

An electrical interface used to reroute a connection or socket to another one is known as interposer. Consumers primarily use it to spread a connection to a wider pitch. Interposers are widely used in multi die chips or boards.

Fan-out WLP on the other hand is an integrated circuit packaging technology used for making a miniaturized package footprint with higher input/output and enhanced thermal and electrical performance.

FOWLP is an advanced form of standard wafer-level packaging solutions. Consumers prefer it since they provide solutions for various semiconductor devices that need a greater integration level and a higher number of external contacts.

Rapid shift towards heterogeneous integration and system-in-packaging is anticipated to put the interposer and fan-out WLP industry into spotlight.

Growing trend of miniaturization in electronic devices and increasing demand for compact and efficient devices are compelling companies to use advanced packaging platforms or technologies, including fan-out wafer level packaging.

Fan-out wafer level packaging enables manufacturers to cater to rising demand for smaller form factors and improved thermal performance. It allows them to form compact packages with several external inputs/outputs.

Rising applications of interposers and fan-out wafer level packaging in MEMS, LEDs, memory, photonics, and optoelectronics, is forecast to drive the global market forward.

High adoption of FOWLP in consumer electronics sector to manufacture efficient and ultra-thin devices such as laptops, smartphones, and smartwatches will boost market expansion.

Increasing usage of fan-out WLP for placing a large count of contacts in small footprints, and enhancing electrical performance of systems is likely to boost the market.

Companies can use interposer and fan-out wafer level packaging to combine dies and components such as MEMS, passives, filters, and crystals in a relatively small size package.

Rising awareness about the advantages of fan-out WLP such as substrate-less package, greater input/output count, and enhanced RF performance is set to create opportunities for companies.

Robust expansion of military & defense sector coupled with high demand for advanced electronic products in this sector will elevate interposer and fan-out WLP demand.

In 2018 global military spending was around US$ 523 billion which increased to around 2.1 trillion by 2022. This in turn is expected to create high growth prospects for the providers of interposers and FOWLP.

Interposer and fan-out WLP technologies are increasingly being adopted in the military industry due to their ability to provide high levels of integration, faster speeds, and lower power consumption in ruggedized electronic systems. Thus, growing demand for sophisticated military devices will foster market development.

| Attributes | Key Insights |

|---|---|

|

Global Interposer and Fan-out WLP Market Size in 2025 |

US$ 24.4 billion |

|

Projected Interposer and Fan-out WLP Market Value (2032) |

US$ 101.6 billion |

|

Value-based CAGR (2025 to 2032) |

22.6% |

| Historical Market Growth Rate (CAGR 2019 to 2024) |

19.4% |

2019 to 2024 Interposer and Fan-out WLP Sales Outlook Compared to Demand Forecast from 2025 to 2032

Historically, from 2019 to 2024, the value of the interposer and fan-out WLP market increased at around 19.4.% CAGR. Over the next ten years, the market is projected to witness a CAGR of 22.6%, creating an absolute $ opportunity of US$ 101.6 billion by 2032.

Growing usage of interposers and fan-out WLP across diverse sectors is expected to drive the global market forward.

Interposer and fan-out wafer-level packaging (WLP) is increasingly being used in the automotive industry to enable the development of more advanced and sophisticated electronic systems.

The use of interposer and fan-out WLP in automotive applications helps to reduce the size and weight of electronic components while improving performance and reliability. These technologies also help to enable the development of more advanced driver assistance systems (ADAS) and autonomous driving systems, which require high-performance, compact, and low-power electronics.

The use of interposer and fan-out WLP can also help to address the challenges of thermal management and power consumption, which are critical in automotive applications. Therefore, the use of interposer and fan-out WLP is projected to continue to rise in the automotive industry as the demand for more advanced and sophisticated electronic systems continues to increase.

There were around 64 million units of cars sold in the world in 2020 which is projected to increase to around 74 million by 2027. This in turn will create a high demand for interposer and fan-out WLP as they help to improve the performance and reliability of the electronics in the car.

Interposer and fan-out WLP technologies have applications in the military industry, where high-performance and ruggedized electronic systems are needed for mission-critical operations.

Interposer and fan-out WLP technologies are used to create smaller and more power-efficient electronic devices, which are essential for military equipment such as communications systems, radar systems, and navigation systems.

The military industry also requires electronic systems that can withstand harsh environments and extreme temperatures, and interposer and fan-out WLP technologies are designed to meet these requirements.

Which Region is Projected to Offer Lucrative Opportunities for Interposer and Fan-out WLP Providers?

Asia Pacific is expected to offer lucrative opportunities for interposer and fan-out WLP providers. As per the latest report, Asia Pacific interposer and fan-out WLP industry size is likely to expand from US$ 6.8 billion in 2025 to US$ 52.7 billion by 2032.

Increasing military spending and expansion of automotive & consumer electronics sectors are key factors driving Asia Pacific market.

Asia Pacific has significant military spending in the world with around US$ 523 billion in 2019 which increased to around US$ 595 billion by 2024. This is anticipated to create a conducive environment for the growth of the target market.

Interposer and fan-out WLP is used in military applications for the development of advanced military applications such as unmanned aerial vehicles (UAVs), smart munitions, and satellite systems. Rising production and sales of these equipment will elevate interposer and fan-out WLP demand during the assessment period.

Country-wise Insights:

What is the Demand Outlook for the United States Interposer and Fan-out WLP Market?

The United States interposer and fan-out WLP market is forecast to expand at 21.3% CAGR through 2032, in comparison to 24.1% CAGR registered from 2019 to 2024. Total market valuation in the country is likely to reach US$ 12.7 billion by 2032.

Rising usage of interposers and fan-out WLP across thriving military, medical device, and telecommunication sectors is expected to boost the United States market.

The United States spends a substantial amount of money on defense. It is the world's predominant spender on the military. In 2019, the country spent over US$ 638 billion, which is expected to climb to over $977 billion by 2032. This will positively impact interposer and fan-out WLP sales revenue.

Interposer and fan-out WLP are increasingly being adopted in military applications to create smaller and more power-efficient electronic devices, which are essential for military equipment such as communication systems, radar systems, and navigation systems.

Increasing military spending will therefore continue to elevate demand for interposers and fan-out WLP during the assessment period.

Will China Continue to Remain a Highly Lucrative Interposer and Fan-out WLP Market?

According to the latest report by Persistence Market Research (PMR), China will continue to remain the highly lucrative market for interposer and fan-out WLP companies. Demand for interposer and fan-out WLP in China is expected to rise at 24.3% CAGR during the assessment period.

By 2032, China interposed and fan-out WLP market is projected to exceed a valuation of US$ 27.4 billion. It will create an absolute $ growth of US$ 24.3 billion over the next decade.

Booming consumer electronics, automotive, and military & defense sectors along with high usage of advanced packaging technologies in these sectors is driving China market forward.

China is a global leader when it comes to military force. The country spent around US$ 293.3 billion on military in 2019 which is predicted to climb to about US$ 531 billion by 2032.

Large military forces will create high demand for advanced weapons and technologies which can be made by using interposers and fan-out WLP. Hence, expansion of military sector due to increasing military spending will boost China market.

Category-wise Insights:

Which is the Leading Packaging Technology in the Market?

As per Persistence Market Research (PMR), through-silicon vias will remain the popular packaging technology. The target segment exhibited a CAGR of 27.4% from 2019 to 2024 and is expected to thrive at a CAGR of 22.5% through 2032. This is due to rising usage of through-silicon vias in a wide range of applications.

Through silicon vias (TSVs) are a critical component in interposer and fan-out wafer level packaging (FOWLP) technologies, providing high-density and high-speed electrical connections between the various layers of a chip stack.

In interposer technology, TSVs are used to connect the chip to the interposer, while in FOWLP, TSVs are used to connect the chip to the substrate. The use of TSVs in interposer and FOWLP technologies offers several advantages over traditional packaging techniques.

TSVs enable high-density and high-speed electrical connections between the various layers of a chip stack, reducing the overall footprint of the device. Further, TSVs provide a more direct and efficient path for electrical signals, reducing signal loss and improving overall performance.

The use of TSVs is expected to become increasingly prevalent as consumer electronics continue to demand smaller, more powerful devices.

Which is the Predominant End-Use industry of Interposer and Fan-out WLP?

According to the latest report, consumer electronics segment will generate significant revenues in the market. This is due to increasing demand for interposer and fan-out WLP in consumer electronics sector.

The consumer electronics segment grew at a CAGR of 27.0% from 2019 to 2024. For the next ten years (2025 to 2032), it is likely to expand at 22.3% CAGR.

Interposer and fan-out WLP technologies are used in consumer electronics to provide higher levels of integration, faster speeds, and lower power consumption. These technologies enable the creation of smaller and more power-efficient electronic devices, which are essential for consumer electronics such as smartphones, tablets, and wearables.

Interposer and fan-out WLP technologies provide a high-density interconnect solution that allows for the integration of multiple chips onto a single substrate, resulting in smaller form factors and lower power consumption.

The use of interposer and fan-out WLP technologies in consumer electronics enables the development of more advanced features such as augmented reality, artificial intelligence, and high-speed connectivity. These features require advanced chipsets with high levels of integration, which can be achieved through the use of interposer and fan-out WLP technologies.

As consumer electronics demand faster product cycles and frequent updates with smaller sizes, lighter weight, and high performance, interposers and fan-out WLP technologies can accommodate these demands by reducing the size, improving performance, and providing additional functionalities.

Competitive Landscape:

Key players in the market include Samsung Electronics, Toshiba Corp., ASE, Qualcomm Incorporated, Texas Instruments, Taiwan Semiconductor Manufacturing, Amkor Technology, United Microelectronics, STMicroelectronics, Broadcom Ltd., Intel Corporation, and Infineon Technologies AG.

These leading companies are investing heavily in research and development to develop new packaging technologies. They are also adopting strategies such as mergers, partnerships, acquisitions, collaborations, joint ventures, etc. to expand their global footprint.

Recent Developments:

- In June 2022, ASE Inc announced the VIPack, a packaging platform that is designed to enable vertically integrated package solutions. In order to improve clock speed, bandwidth, and power delivery, as well as to shorten the co-design time, product development, and time to market, the VIPack platform offers the capabilities needed.

- In July 2019, Intel announced that it will purchase eASIC. Through this acquisition, Intel is aiming to expand its portfolio to include structured eASIC and therefore service a wider range of clients across the world.

- In February 2018, Advanced Semiconductor Engineering, Inc. and Cadence Design Solutions, Inc. collaborated to provide a System-in-Package (SiP) EDA solution to handle the difficulties in designing and validating Fan-Out Chip-on-Substrate (FOCoS) multi-die packages. This will allow designers to significantly increase throughput while minimizing the number of design iterations, which decreases the time required to create and validate extremely complex SiP packages.

Companies Covered in Interposer and Fan-out WLP Market

- Taiwan Semiconductor Manufacturing

- Samsung Electronics

- Toshiba Corp

- ASE

- Qualcomm Incorporated

- Texas Instruments

- Amkor Technology

- Value (US$ Billion) Microelectronics

- STMicroelectronics

- Broadcom Ltd.

- Intel Corporation

- Infenion Technologies AG

Frequently Asked Questions

The market is expected to reach US$ 101.6 billion by 2032.

The market is forecast to grow at a 22.6% CAGR during the period.

Asia Pacific leads, with expected growth from US$ 6.8B to US$ 52.7B by 2032.

China is projected to reach US$ 27.4 billion by 2032.

Major players include TSMC, Samsung, Intel, ASE, Qualcomm, and Broadcom.