- Pharmaceuticals

- Inhalation CDMO Market

Inhalation CDMO Market Size, Share, and Growth Forecast, 2026 - 2033

Inhalation CDMO Market by Product Type (API, API Substrate, Others), Company Size (Large, Medium, Small), Scale of Operation (Preclinical, Clinical, Commercial), and Regional Analysis for 2026 - 2033

Inhalation CDMO Market Size and Trends Analysis

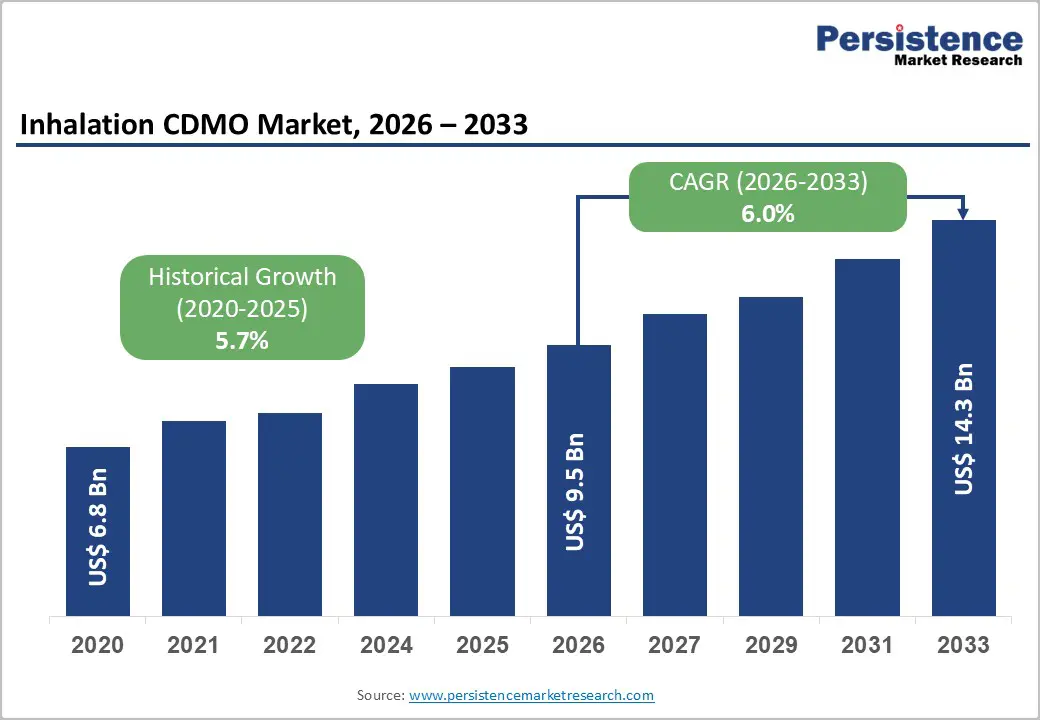

The global inhalation CDMO market size is likely to be valued at US$9.5 billion in 2026, and is expected to reach US$14.3 billion by 2033, growing at a CAGR of 6.0% during the forecast period from 2026 to 2033, driven by the increasing prevalence of respiratory diseases, rising outsourcing of complex inhalation drug-device combination products, and advancements in dry powder inhaler (DPIs) and metered dose inhaler (MDIs) formulation platforms.

Growing demand for end-to-end inhalation CDMO services, particularly for large-molecule biologics and small-molecule APIs for asthma/COPD therapies, is accelerating adoption across scales of operation. Advances in soft mist inhaler technology and particle engineering are further boosting uptake by improving lung deposition and patient compliance. The increasing recognition of inhalation CDMOs as critical to the accelerated development and commercial supply of next-generation inhaled therapies in emerging respiratory and systemic markets remains a major driver of market growth.

Key Industry Highlights:

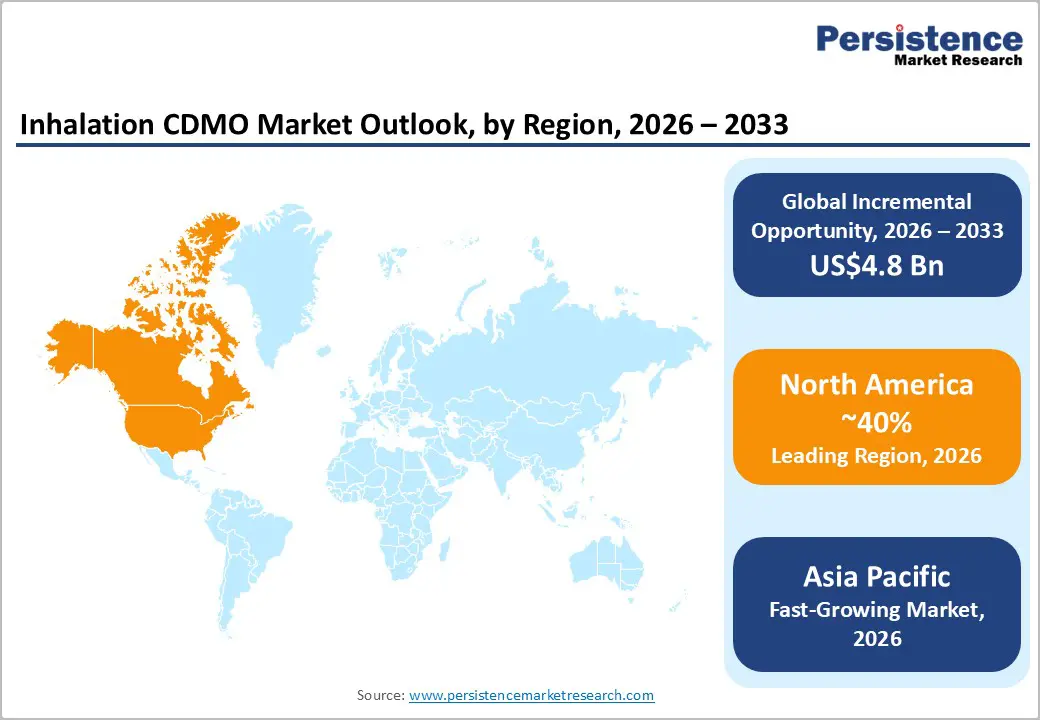

- Leading Region: North America, anticipated to account for a 40% market share in 2026, driven by high R&D spending, strong regulatory expertise, and premium demand in the United States.

- Fastest-growing Region: Asia Pacific, fueled by cost-competitive manufacturing, rising respiratory disease burden, and growing investments in inhalation CDMO capacity in India and China.

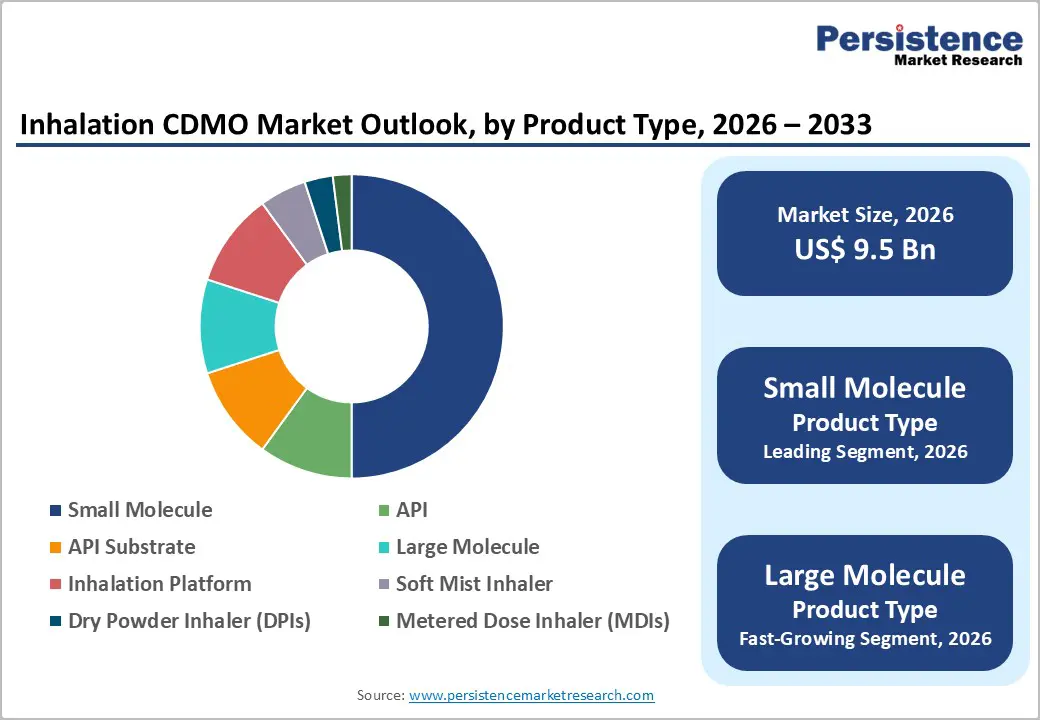

- Dominant Product Type: Small molecule, to hold approximately 55% of the market share, as it dominates the current inhaled drug pipeline.

- Leading Scale of Operation: Commercial, to account for over 50% of the market revenue in 2026, due to the ongoing supply of marketed asthma/COPD products.

- Leading Company Size: Large, to contribute nearly 60% of the market revenue in 2026, due to end-to-end capabilities and global regulatory track record.

| Key Insights | Details |

|---|---|

|

Inhalation CDMO Market Size (2026E) |

US$9.5 Bn |

|

Market Value Forecast (2033F) |

US$14.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Respiratory Diseases and Outsourced Inhalation Development

The rising demand for respiratory disease treatments is closely linked with the growing reliance on outsourced inhalation development, driven by both clinical complexity and economic realities. Respiratory conditions such as asthma, chronic obstructive pulmonary disease (COPD), pulmonary fibrosis, and respiratory infections are becoming more prevalent due to urbanization, air pollution, smoking habits, occupational exposure, and aging populations. These diseases often require targeted drug delivery directly to the lungs, making inhalation the preferred route for faster onset of action and reduced systemic side effects.

Developing inhalation therapies is technically demanding. It involves specialized formulation expertise, device compatibility testing, aerodynamic particle size optimization, and strict regulatory compliance. Many pharmaceutical and biotechnology companies lack in-house capabilities for these highly specific processes. Outsourcing inhalation development to contract development and manufacturing organizations (CDMOs) has become an attractive strategy. Outsourced partners provide advanced infrastructure, experienced scientific teams, and established regulatory know-how, enabling sponsors to reduce development timelines and control costs.

High Technical Complexity and Regulatory Hurdles

High technical complexity and regulatory hurdles remain significant challenges in inhalation drug development and related outsourcing services. Inhalation therapies are fundamentally different from conventional oral or injectable products because the drug must be delivered as an aerosol with precise control over particle size, airflow behavior, and lung deposition. Even minor changes in formulation, excipients, or manufacturing conditions can affect aerosol performance, dose uniformity, and therapeutic outcomes. This level of sensitivity requires advanced formulation techniques, specialized testing methods, and close integration between the drug and its delivery device, thereby increasing development complexity.

Regulatory expectations add another layer of complexity. Inhalation products are regulated as combination therapies, meaning both the drug and the device must meet rigorous safety, quality, and performance standards. Developers are required to generate extensive in vitro, preclinical, and clinical data to demonstrate consistency, reproducibility, and patient safety. Regulatory agencies also demand detailed characterization of aerosol properties and robust comparability studies, particularly for generic or reformulated products.

Expansion of Generic and Value-Added Inhalation Products

The expansion of generic and value-added inhalation products is becoming a key growth driver within the respiratory therapeutics landscape. As patents on several widely used inhalers expire, pharmaceutical companies are actively pursuing generic alternatives to address cost pressures in healthcare systems and improve patient access to essential respiratory treatments. Unlike conventional generics, inhalation products are technically complex, requiring precise replication of aerosol performance, dose delivery, and device functionality. This complexity has created a strong demand for specialized development capabilities.

Beyond standard generics, companies are increasingly focusing on value-added inhalation products that offer clinical or user-experience improvements. These may include enhanced delivery devices, improved dose consistency, reduced dosing frequency, or combination therapies that simplify treatment regimens. Such innovations allow manufacturers to differentiate their products while leveraging established active ingredients, thereby reducing development risk relative to entirely new drugs. Regulatory authorities often require comprehensive comparability and performance data for both generic and value-added inhalers, making development resource-intensive.

Category-wise Analysis

Product Type Insights

The small-molecule segment is expected to lead the market, accounting for approximately 55% of the market in 2026, owing to its well-established role in respiratory therapy and demonstrated suitability for inhalation delivery. These molecules are easier to formulate into stable aerosols, offer predictable lung deposition, and demonstrate reliable pharmacokinetic profiles. Their relatively lower manufacturing costs and scalable production further support widespread adoption.

Many frontline respiratory treatments for asthma and COPD rely on small molecules that are well-known and widely used by physicians. One such treatment is Serevent (salmeterol), developed and marketed by GlaxoSmithKline (GSK). Salmeterol is a long-acting β2-adrenergic agonist, commonly used in inhalers, that helps manage asthma and chronic obstructive pulmonary disease (COPD) by relaxing airway smooth muscle, thereby facilitating airflow.

The large-molecule segment is projected to be the fastest-growing product category in respiratory therapy, as innovation extends beyond traditional bronchodilators. Biologics, peptides, and protein-based therapies are being explored to treat severe asthma, rare pulmonary disorders, and inflammatory pathways that small molecules cannot effectively address. Advances in formulation science and inhalation devices now enable the delivery of these delicate molecules to the lungs with greater stability and accuracy.

One example is Pulmozyme® (dornase alfa), a biologic inhaled therapy developed by Genentech/Roche. Pulmozyme is a recombinant human DNase I protein used in the treatment of cystic fibrosis to reduce mucus viscosity in the lungs, improving airway clearance and lung function. Unlike conventional small-molecule bronchodilators, this protein-based large molecule targets the physical properties of mucus, providing therapeutic benefits that small molecules cannot achieve for certain lung conditions.

Company Size Insights

The large segment is expected to dominate the market, accounting for nearly 60% of revenue in 2026, owing to its strong differentiation and limited competition. Development complexity, advanced manufacturing requirements, and specialized delivery systems create high entry barriers, allowing innovators to maintain stronger pricing power and longer product lifecycles. Many large-molecule therapies are positioned as specialty or breakthrough treatments, often supported by robust clinical evidence and targeted patient populations.

Tyvaso DPI contains treprostinil, a prostacyclin analogue delivered via dry-powder inhaler for the treatment of pulmonary arterial hypertension (PAH) and pulmonary hypertension associated with interstitial lung disease (PH-ILD). In 2024, Tyvaso generated about US$1.62 billion in revenue, showing strong commercial performance for a biologic/large-molecule inhaled therapy and illustrating how advanced inhaled biologics can command high sales in specialized respiratory markets.

The medium company size segment is likely to be the fastest-growing, owing to its balance of agility and capability. Unlike large players, they can adapt quickly to new technologies, customer needs, and regulatory changes, while still possessing sufficient resources to invest in specialized infrastructure and skilled talent.

These companies often focus on niche therapeutic areas or tailored services, allowing them to differentiate without the complexity of large organizational structures. Galecto Biotech is a biotechnology firm developing inhaled therapies for severe lung diseases, including idiopathic pulmonary fibrosis (IPF). Galecto’s lead product candidate, GB0139, is an inhaled inhibitor targeting galectin-3, a protein involved in lung fibrosis, addressing a high unmet need in respiratory treatment.

Scale of Operation Insights

The commercial segment is expected to lead the market, accounting for 55% of the market in 2026, driven by the transition of inhalation therapies from development to large-scale commercialization. As more inhaled products receive regulatory approval, demand for commercial manufacturing, packaging, and lifecycle management services increases.

Pharmaceutical companies increasingly rely on external partners to support consistent, high-volume production while meeting strict quality and compliance standards. Catalent, Inc. is a major contract development and manufacturing organization that provides commercial-scale manufacturing for inhalation products, including dry powder inhalers (DPIs) and metered-dose inhalers (MDIs). Catalent’s inhalation services span formulation through large-volume commercial manufacturing, filling, packaging, and quality testing, enabling pharmaceutical companies to bring finished inhaled therapies to market efficiently and at scale.

The clinical segment is likely to be the fastest-growing area of operation, driven by the rapid expansion of early- and mid-stage inhalation therapies. Pharmaceutical and biotech companies are increasingly outsourcing preclinical and clinical manufacturing to specialized CDMOs to ensure a reliable, high-quality supply for trials, without the need to invest in in-house infrastructure. Clinical-scale operations offer greater flexibility, allowing companies to adapt batch sizes, formulations, and device integration as protocols evolve.

The rising investment in novel inhaled therapies, including biologics and complex small molecules, is fueling demand for specialized clinical production. One example is Phillips Medisize, a contract manufacturer that provides clinical-trial production and supply for inhalation therapies, including dry powder inhalers (DPIs), metered-dose inhalers (pMDIs), and nebulizer systems. Phillips Medisize’s facilities can produce GMP-compliant batches for clinical studies, ranging from early development to pilot-scale manufacturing, ensuring a consistent supply of investigational inhaled drug products for sponsors conducting human trials.

Regional Insights

North America Inhalation CDMO Market Trends

North America is projected to lead the market, accounting for nearly 40% of the share in 2026, driven by the region’s world-leading respiratory drug pipeline, strong regulatory expertise, and high public investments in inhaled biologics research. Development systems in the U.S. and Canada provide extensive support for inhalation programs, ensuring broad accessibility of inhalation CDMO services across small-molecule, large-molecule, DPI, and MDI populations. Increasing demand for end-to-end, convenient, and scalable forms is further accelerating adoption, as these formats improve time-to-clinic and reduce barriers associated with device integration.

Innovation in inhalation CDMO technology, including stable large-molecule formulations, improved soft-mist delivery, and targeted combination-product enhancement, is attracting significant investment from both the public and private sectors. Government initiatives and NIH campaigns continue to promote use to address respiratory risks, development costs, and emerging biologic threats, thereby creating sustained market demand. The growing focus on clinical grades and specialty indications, particularly for rare pulmonary diseases and other indications, is expanding the target applications for inhalation CDMO.

Europe Inhalation CDMO Market Trends

Europe is propelled by increasing awareness of the benefits of inhalation delivery, robust regulatory systems, and government-led respiratory health programs. Countries such as Germany, Switzerland, France, and the U.K. have well-established CDMO frameworks that support routine inhalation development and encourage the adoption of innovative service delivery methods, including inhalation CDMO. These specialized formulations are particularly appealing to small-molecule populations, regulation-conscious sponsors, and large-molecule users, thereby improving time-to-market and coverage rates.

Technological advancements in inhalation CDMO development, such as enhanced device-formulation integration, application-targeted delivery, and improved DPI/MDI grades, are further boosting the market potential. European authorities are increasingly supporting research and trials for inhalation services against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, patient-centric options is aligned with the region’s focus on preventive respiratory care and reducing systemic exposure. Public awareness campaigns and promotion drives are expanding reach in both urban and rural areas, while CDMOs are investing in analytics and novel variants to increase efficacy.

Asia Pacific Inhalation CDMO Market Trends

Asia-Pacific is likely to be the fastest-growing region, driven by rising respiratory awareness, expanding government initiatives, and expanding application programs across the region. Countries such as India, China, Japan, and South Korea are actively promoting CDMO campaigns to address domestic generic growth and emerging inhaled biologic needs. Inhalation CDMO services are particularly attractive in these regions due to their cost-competitive administration, ease of scaling, and suitability for large-scale respiratory drug drives in both urban and rural populations.

Technological advancements are enabling the development of stable, effective, and easy-to-deploy inhalation CDMO services that can withstand challenging regulatory conditions and minimize development dependence. These innovations are critical for reaching domestic sponsors and improving overall pipeline coverage. The growing demand for small-molecule, large-molecule, DPI, and MDI applications is contributing to market expansion. Public-private partnerships, increased respiratory expenditure, and rising investments in CDMO research and manufacturing capacity are further accelerating growth. The convenience of CDMO delivery, combined with improved quality and reduced risk of failure, positions inhalation CDMO as a preferred choice.

Competitive Landscape

The global inhalation CDMO market features competition between established respiratory specialists and diversified contract manufacturers expanding inhalation capabilities. In North America and Europe, Lonza and Catalent lead through strong R&D, distribution networks, and regulatory ties, bolstered by innovative DPI/MDI and large molecule programs. In Asia Pacific, Lupin and Piramal Pharma Limited advance with cost-competitive solutions, enhancing accessibility. End-to-end delivery boosts speed-to-market, cuts development risks, and enables mass integrations across sponsors. Strategic partnerships, collaborations, and acquisitions merge expertise, expand device portfolios, and speed commercialization. Large molecule formulations solve biologic issues, aiding penetration in next-generation inhaled therapies.

Key Industry Developments

- In June 2025, Phillips Medisize, a Molex company, launched TheraVolt™ Medical Connectors. The first medical connector under the Phillips Medisize brand, TheraVolt is designed to enhance device integration, reliability, and performance, providing solutions for handling both signals and high-voltage lines.

- In January 2025, Molex, the parent company of Phillips Medisize, announced that the previously announced acquisition of Vectura Group Ltd. (Vectura) from Vectura Fertin Pharma Inc., a subsidiary of Philip Morris International Inc., had been completed through an affiliate. Phillips Medisize, a leader in the design and manufacturing of innovative products for the pharmaceutical drug delivery, in vitro diagnostic, and medtech markets, was further strengthened by the acquisition.

Companies Covered in Inhalation CDMO Market

- Recipharm AB

- AptarGroup Inc.

- Hovione

- Vectura Group Ltd.

- Nemera

- Kindeva

- H&T Presspart

- Sanner GmbH

- Stevanato Group

- Medspray

- ICONOVO AB

- Lonza

- Gerresheimer AG

- Catalent

- Thermo Fisher Scientific Inc.

- Lubrizol Life Science

- Enteris BioPharma

- Cambrex Corporation

- INKE

- Piramal Pharma Limited

- Lupin

Frequently Asked Questions

The global inhalation CDMO market is projected to reach US$9.5 billion in 2026.

Rising respiratory disease prevalence and outsourcing of complex inhalation drug-device products are the key drivers.

The inhalation CDMO market is poised to witness a CAGR of 6.0% from 2026 to 2033.

Large molecule inhalation programs and soft mist inhaler platforms are key opportunities.

Lonza, Catalent, Recipharm AB, Hovione, and Vectura Group Ltd are the key players.