- Biotechnology

- Immunosuppressant TDM Assay Kits Market

Immunosuppressant TDM Assay Kits Market Size, Share, Trends, and Growth Forecast, 2025 - 2032

Immunosuppressant TDM Assay Kits Market By Product Type (Assay Kits, Reagents, Control Materials, Software for Data Analysis), Application (Transplantation Medicine, Autoimmune Disease Management, Cancer Therapy, Organ Preservation), Distribution Channel, and Regional Analysis for 2025 - 2032

Immunosuppressant TDM Assay Kits Market Size and Trends Analysis

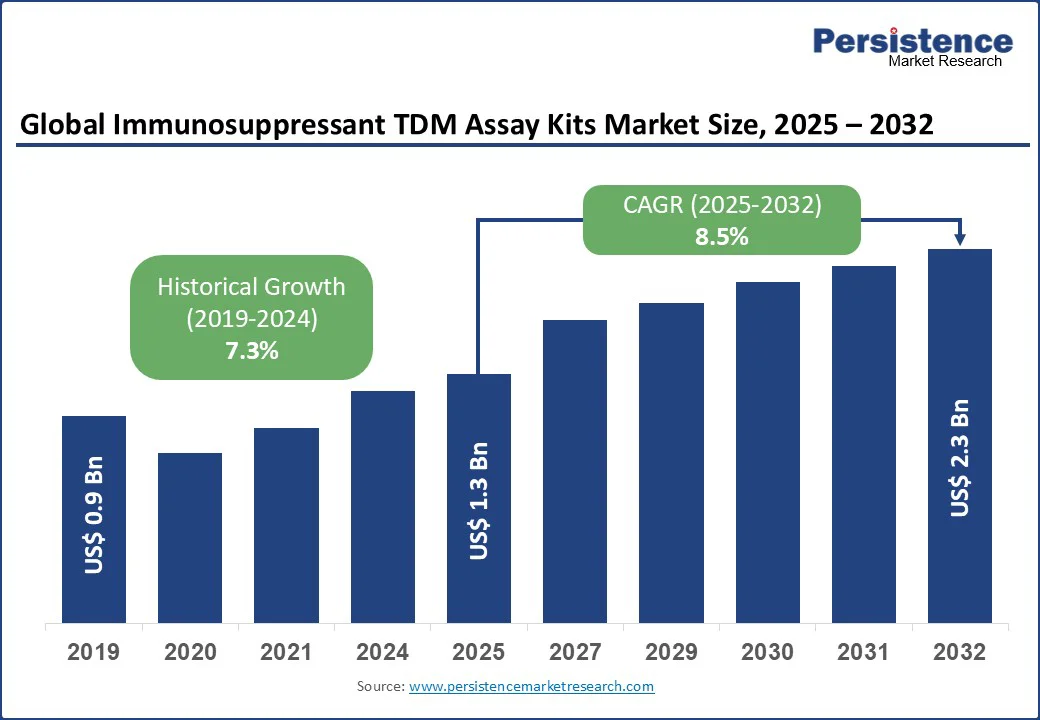

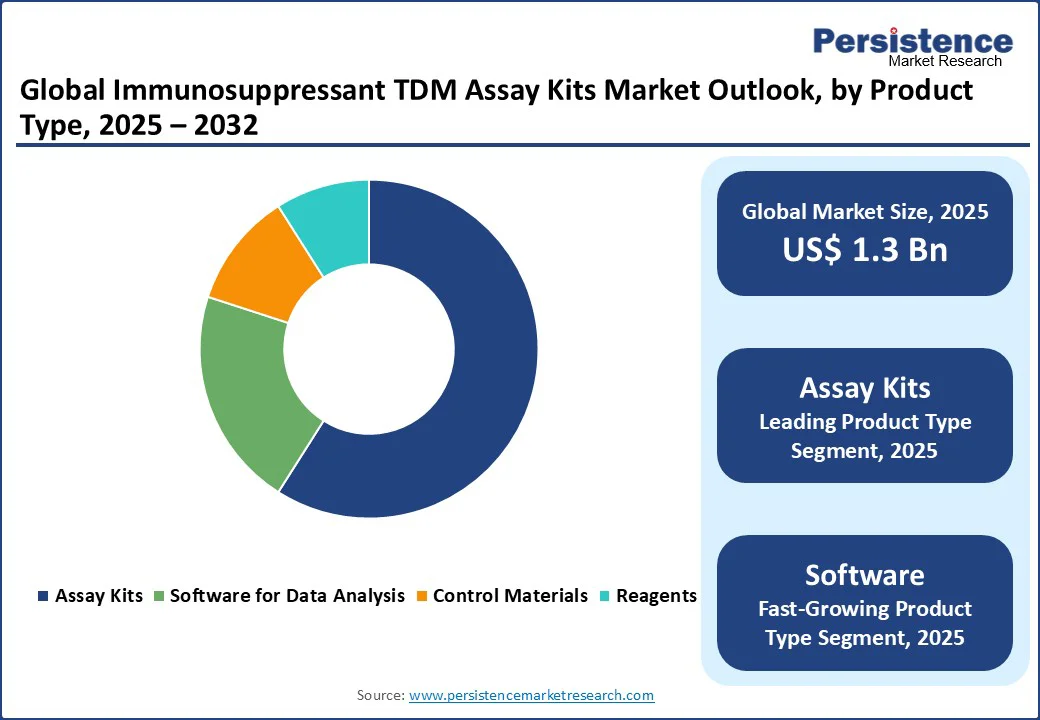

The global Immunosuppressant TDM Assay Kits Market size is expected to be valued at US$1.3 Bn in 2025 and is expected to reach US$2.3 Bn by 2032, growing at a CAGR of 8.5% during the forecast period from 2025 to 2032.

The immunosuppressant TDM assay kits industry has experienced significant growth, driven by the increasing need for precise therapeutic drug monitoring in transplant patients, the rising prevalence of autoimmune diseases across populations, and advancements in assay technologies for accurate dosing.

Key Industry Highlights:

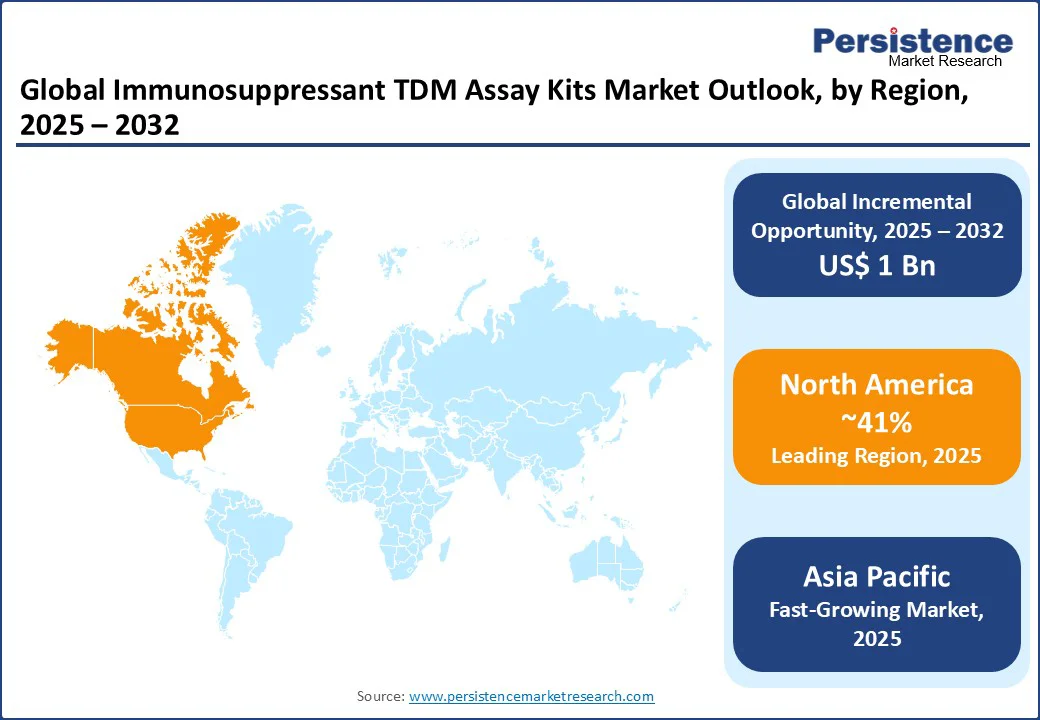

- Leading Region: North America, holding a 41% market share in 2025, driven by the presence of major healthcare hubs in the U.S., high adoption of advanced diagnostic technologies, and strong demand for transplant monitoring and autoimmune applications.

- Fastest-growing Region: Asia Pacific is emerging as the fastest-growing market, fueled by rapid healthcare program developments, increasing government investments in diagnostic infrastructure, and growing demand for autoimmune management and transplantation kits in countries such as China and India.

- Dominant Product Type: Assay Kits, commanding nearly 59% market share, due to their cost-effectiveness, rapid deployment, and widespread adoption in monitoring for various applications.

- Leading Application: Transplantation Medicine, accounting for over 49% of market revenue, driven by the need for efficient drug level monitoring and patient outcomes in expanding transplant networks.

|

Global Market Attribute |

Key Insights |

|

Immunosuppressant TDM Assay Kits Market Size (2025E) |

US$1.3 Bn |

|

Market Value Forecast (2032F) |

US$2.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.3% |

The demand for reliable kits in complex medical operations, particularly in transplantation medicine, autoimmune disease management, and cancer therapy sectors, has significantly boosted market expansion.

Market Dynamics

Driver - Increasing Deployment of Organ Transplantations

The rising number of organ transplantations worldwide has become a primary driver for the adoption of immunosuppressant TDM assay kits. These kits are essential in transplantation medicine to ensure optimal dosing of critical drugs such as tacrolimus and cyclosporine, minimizing rejection risks while reducing toxicity. Beyond transplantation, TDM kits are also increasingly used in autoimmune disease management, oncology, and organ preservation, reflecting their versatility in modern healthcare.

Growing global transplant programs, supported by the World Health Organization (WHO) and national transplant registries, have significantly expanded demand for precise and cost-effective monitoring tools. Hospitals, clinics, and diagnostic companies are adopting advanced TDM kits equipped with miniaturized assay technologies, enabling faster results and more efficient patient management. The need for reliable subsystems, including reagents, controls, and analytical software, further strengthens the sector.

For instance, according to the U.S. Department of Health & Human Services’ Health Resources and Services Administration (HRSA), more than 45,000 organ transplants were performed in the United States in 2023, the highest ever recorded, highlighting the growing reliance on immunosuppressant TDM monitoring to improve post-transplant outcomes.

As healthcare systems worldwide scale up high-volume transplant procedures and complex therapies, immunosuppressant TDM assay kits are expected to remain a cornerstone for improving patient outcomes and supporting long-term treatment success.

Restraint - Development and Regulatory Costs are High

The high costs associated with developing and regulating immunosuppressant TDM assay kits continue to hamper market growth. Designing and validating these kits requires advanced technology, specialized reagents, and extensive clinical testing to ensure performance and safety, resulting in significant financial investment. This challenge is particularly acute for small and medium enterprises (SMEs) and new entrants.

Moreover, compliance with stringent regulations imposed by bodies such as the U.S. Food and Drug Administration (FDA), the European Medicines Agency (EMA), and the International Organization for Standardization (ISO) further escalates development expenses. Lengthy approval timelines, validation requirements, and design modifications to meet compliance standards frequently cause project delays and cost overruns.

Integration with laboratory systems and patient data adds another layer of expense. For instance, several diagnostic developers have reported cost escalations and delayed product rollouts due to FDA and EMA compliance hurdles, underscoring how regulatory complexity raises financial strain. While large pharmaceutical corporations can absorb these costs, smaller players often struggle, limiting innovation and slowing market expansion.

Opportunity - Advancements in Modular and AI-Integrated Assay Technologies

Advancements in modular and AI-integrated immunosuppressant TDM assay technologies present a significant growth opportunity for the domain. Modular designs allow diagnostic manufacturers to build flexible and scalable assay kits that can be customized for diverse applications, ranging from transplantation medicine and autoimmune management to cancer therapy and organ preservation. This reduces both development time and overall costs, making kits more accessible for commercial operators, research institutions, and emerging diagnostic startups.

Additionally, modularity supports easier upgrades and component replacements, extending kit usability and improving return on investment. For instance, a leading player has adopted modular assay architectures to accelerate the deployment of its TDM solutions for global patient monitoring, reducing costs and ensuring faster scalability.

The integration of artificial intelligence (AI) into assay kits further enhances performance by enabling autonomous analysis, predictive dosing, and efficient data management. AI-driven systems can optimize drug monitoring, interpretation, and reporting in real time, reducing dependency on manual processes and ensuring higher accuracy.

For instance, EMA has been exploring AI-integrated assay technologies for TDM kits to adapt parameters in labs, thereby improving operational efficiency autonomously. As healthcare accelerates and demand for cost-effective, intelligent, and scalable diagnostic platforms increases, modular and AI-integrated assay technologies are expected to open new avenues for innovation and long-term market growth.

Category-wise Analysis

Product Type Insights

Assay kits dominate, expected to account for approximately 59% of the share in 2025. Its dominance stems from its cost-effectiveness, rapid development cycles, and ease of integration with monitoring systems for applications such as transplantation and autoimmune management.

Assay kits, such as those offered by Waters and Thermo Fisher Scientific, enable real-time updates, system scalability, and seamless collaboration across labs, making them a preferred choice for industries such as commercial diagnostics and research. Their modular designs also reduce upfront costs, driving adoption among startups and SMEs.

The software for data analysis segment is the fastest-growing, driven by industries with high-performance requirements, such as advanced autoimmune tracking and cancer therapy. Software solutions offer greater data capacity and customization, appealing to large enterprises with complex needs.

The growing focus on precision medicine and high-accuracy monitoring, such as the FDA’s initiatives, is accelerating the adoption of software in regions such as North America and Europe, with significant growth potential in high-stakes applications.

Application Insights

Transplantation medicine leads the immunosuppressant TDM assay kits market, holding a 49% share in 2025. The segment’s dominance is driven by the need for efficient drug monitoring and patient safety in expanding transplant networks, particularly in hospital and clinic settings. Assay kits streamline the integration of monitoring protocols, reduce errors, and improve operational efficiency, making them critical for providers such as Abbott and Zivak Technologies USA.

The Autoimmune Disease Management segment is the fastest-growing, fueled by the rapid growth of chronic disease tracking and the need for real-time patient monitoring. The rise in autoimmune platforms and the increasing demand for precise dosing have spurred the adoption of TDM kits in this sector. The Asia Pacific region, with its booming autoimmune needs, is driving rapid adoption in this segment.

Distribution Channel Insights

Direct sales accounts for the largest market share, accounting for approximately 49% of revenue in 2025. Direct Sales allows vendors such as Thermo Fisher Scientific and Waters to maintain close relationships with customers, offer tailored kits, and provide dedicated support. This channel is particularly dominant in applications with complex requirements, such as transplantation medicine and autoimmune management, where customized solutions are critical.

The online retail channel is the fastest-growing, driven by the increasing adoption of digital platforms and the rise of e-commerce for diagnostic supplies. These platforms offer seamless access to TDM kits, enabling faster procurement and integration with other healthcare services. The growing popularity of online sales among hospitals and clinics is accelerating the adoption of kits through this channel, particularly in North America and the Asia Pacific.

Regional Insights

North America Immunosuppressant TDM Assay Kits Market Trends

North America is projected to account for nearly 41% of the global immunosuppressant TDM assay kits market, reflecting its leadership in healthcare innovation and technology adoption. The region’s dominance is primarily driven by the presence of major healthcare hubs in the United States, which host leading companies such as Abbott, Thermo Fisher Scientific, and Waters. These firms play a pivotal role in developing advanced TDM kits that support critical applications in transplantation medicine, autoimmune disease management, cancer therapy, and organ preservation.

The region’s strong adoption of cutting-edge diagnostic technologies is further fueled by robust government investments, particularly through the FDA, the U.S. Department of Health and Human Services, and the Centers for Medicare & Medicaid Services, which continue to prioritize precision medicine, patient safety, and chronic disease monitoring. Additionally, the rising demand for point-of-care tracking, particularly for immunosuppressant drugs, has accelerated the development of cost-effective and modular TDM kits.

With a combination of healthcare-driven demand, commercial diagnostic initiatives, and private investments in biotech startups, North America continues to set global standards in reliability, performance, and innovation, making it a frontrunner in shaping the future trajectory of the immunosuppressant TDM assay kits market.

Europe Immunosuppressant TDM Assay Kits Market Trends

Europe captures a substantial share of the immunosuppressant TDM assay kits market, supported by its well-established healthcare infrastructure and strong regulatory framework. The region benefits from the presence of leading pharmaceutical and diagnostic companies, alongside collaborative research networks that accelerate the development and deployment of advanced therapeutic monitoring solutions. Countries such as Germany, France, Italy, and the U.K. are at the forefront of adoption, owing to their high transplant volumes and growing emphasis on precision medicine.

The European Medicines Agency (EMA) plays a pivotal role in shaping the industry by providing regulatory guidance on the integration of advanced and AI-enabled diagnostics, ensuring both safety and efficacy. Additionally, the region’s rising prevalence of autoimmune disorders and increasing reliance on personalized dosing strategies drive demand for efficient TDM kits. Academic hospitals and research institutions across Europe are further expanding the clinical use of modular and automated assays, enhancing both accuracy and operational efficiency.

Combined with favorable healthcare policies and growing investments in laboratory automation, Europe is positioned as a critical growth contributor to the immunosuppressant TDM assay kits market through 2032.

Asia Pacific Immunosuppressant TDM Assay Kits Market Trends

Asia Pacific is positioned as the fastest-growing market for immunosuppressant TDM assay kits, supported by rapid advancements in healthcare programs and rising government investments in diagnostic infrastructure. Countries such as China, India, and Japan are leading the region’s expansion, with China accelerating its diagnostic programs for transplantation, autoimmune management, and cancer therapy, while India’s healthcare bodies continue to launch cost-effective monitoring solutions with global recognition. Japan, through its regulatory agencies, is focusing on precision medicine missions and next-generation diagnostic technologies.

The increasing need for high-accuracy TDM kits to support chronic disease management, patient outcomes, hospital planning, and disease monitoring is driving demand for compact, efficient, and modular assay solutions. Similarly, the surge in autoimmune and transplant monitoring to expand healthcare networks across underserved regions is boosting commercial adoption. Private players and emerging diagnostic startups are also contributing by leveraging advanced TDM technologies to deliver affordable solutions.

With supportive government policies, advancements in AI-enabled assay kits, and expanding commercial applications, the Asia Pacific is expected to dominate future diagnostic deployment, creating substantial opportunities for kit vendors.

Competitive Landscape

Intense competition, regional strengths, and a mix of global and niche players characterize the global Immunosuppressant TDM Assay Kits Market. In developed regions such as North America and Europe, large firms such as Abbott, Thermo Fisher Scientific, and Waters dominate through scale, advanced R&D capabilities, and established partnerships with healthcare agencies.

In the Asia Pacific, rapid healthcare developments and increasing demand for advanced kits are attracting significant investments from both international players, such as Zivak Technologies USA and Recipe Chemicals, and regional vendors.

Companies are focusing on product innovation, modular designs, and strategic alliances to gain a competitive edge. The development of AI-powered and miniaturized TDM kits has emerged as a key differentiator, enabling faster adoption in transplantation medicine, autoimmune management, and cancer therapy sectors. Strategic collaborations, acquisitions, and digital-first approaches for supply chain and marketing are further intensifying the competitive landscape.

The industry exhibits a dual nature, with global leaders such as Thermo Fisher Scientific, Abbott, Roche Diagnostics, and Waters consolidating the top tier through advanced technologies, strong distribution networks, and regulatory expertise. In contrast, the lower tier remains fragmented among numerous regional and niche players that focus on cost-sensitive segments and locally tailored solutions.

Key Developments

- In April 2020, Thermo Fisher introduced a CE/IVD-marked immunosuppressant panel for its Cascadion SM Clinical Analyzer, enabling simultaneous measurement of cyclosporine A, everolimus, sirolimus, and tacrolimus from a single whole-blood sample using LC-MS/MS technology.

- In July 2024, Waters was recognized as one of the leading players in the global immunosuppressant TDM assay kits market, according to recent competitive landscape reports. However, no specific product launches or technological updates have been publicly reported.

Companies Covered in Immunosuppressant TDM Assay Kits Market

- Waters

- Abbott

- Aurora Borealis Control BV

- Recipe Chemicals

- Thermo Fisher Scientific

- Zivak Technologies USA

- Others

Frequently Asked Questions

The global Immunosuppressant TDM Assay Kits Market is projected to reach US$ 1.3 Bn in 2025.

The increasing deployment of organ transplantations is a key driver.

The immunosuppressant TDM assay kits market is poised to witness a CAGR of 8.5% from 2025 to 2032.

Advancements in modular and AI-integrated assay technologies are a key opportunity.

Waters, Abbott, Aurora Borealis Control BV, Recipe Chemicals, Thermo Fisher Scientific, and Zivak Technologies USA are key players.