- Biotechnology

- Immunoprotein Diagnostic Testing Market

Immunoprotein Diagnostic Testing Market Size, Share, and Growth Forecast, 2025 - 2032

Immunoprotein Diagnostic Testing Market is segmented by Test Type (C-reactive Protein Diagnostic Test, Complement System Protein Diagnostic Test, Pre-albumin Diagnostic Test, Haptoglobin Diagnostic Test, Immunoglobulin Diagnostic Test, Free Light Chain Diagnostic Test, and Others), Application, Technology, and Regional Analysis for 2025 - 2032

Immunoprotein Diagnostic Testing Market Size and Trends Analysis

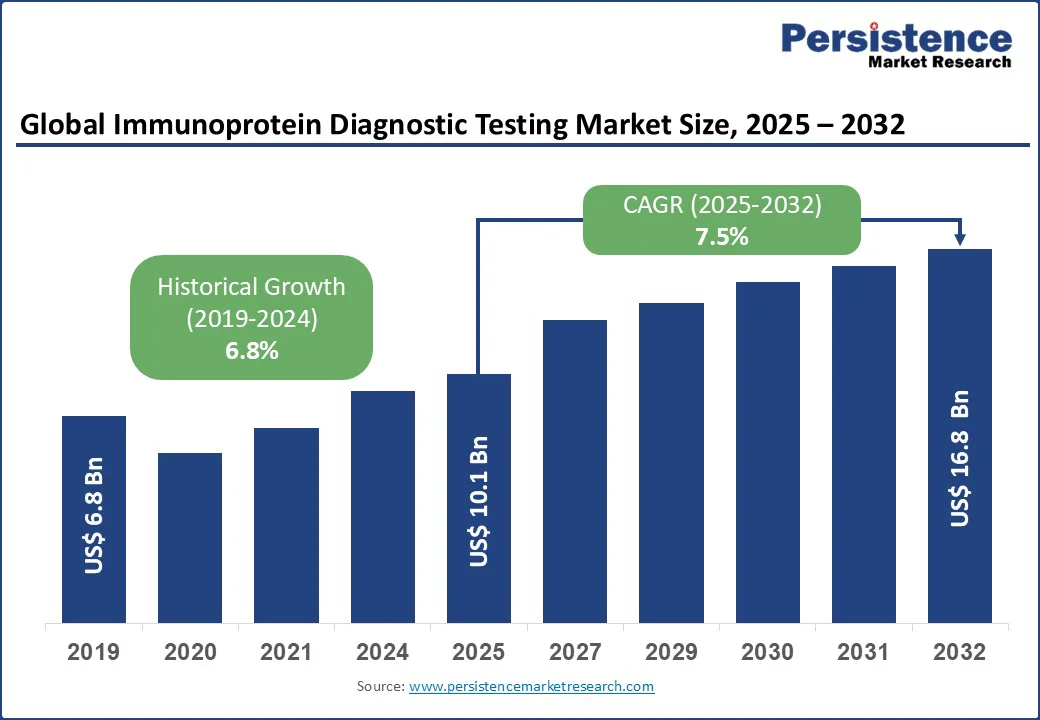

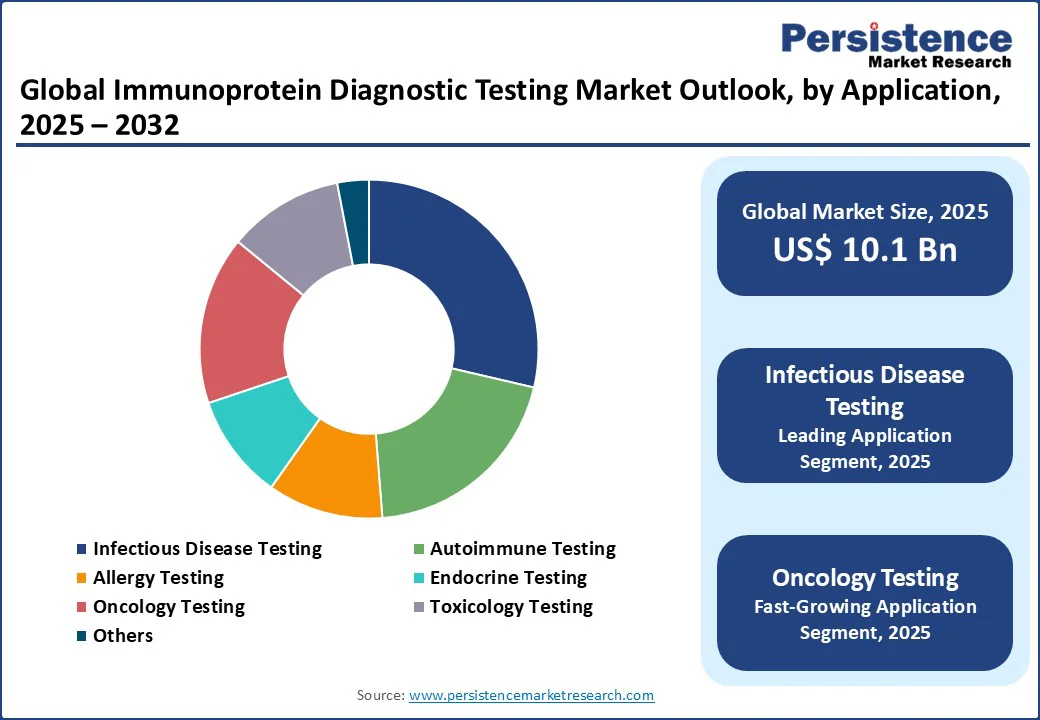

The global immunoprotein diagnostic testing market size is projected to grow from US$10.1 Bn in 2025 to US$16.8 Bn by 2032, registering a CAGR of 7.5% during the forecast period from 2025 to 2032.

The immunoprotein diagnostic testing market has witnessed steady growth, fueled by the rising prevalence of chronic and infectious diseases, coupled with advancements in diagnostic technologies that enhance accuracy and speed. Increasing awareness of preventive healthcare and the growing demand for early, precise diagnostic solutions are further propelling adoption across clinical, research, and point-of-care settings

Key Industry Highlights:

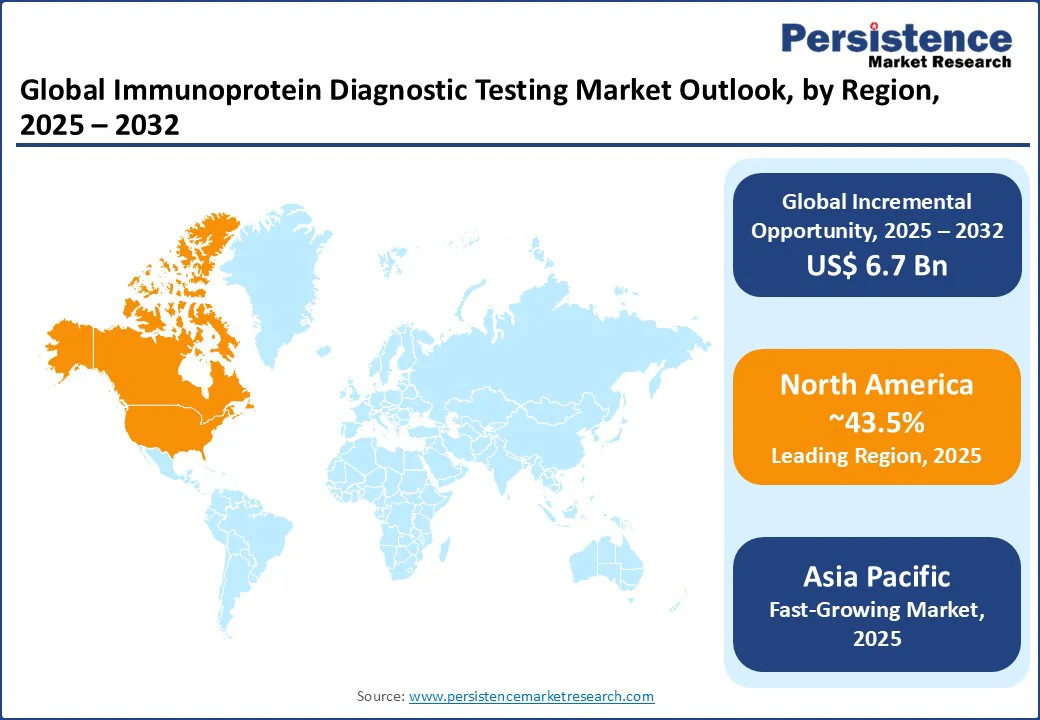

- Leading Region: North America holds a 43.5% market share of the immunoprotein diagnostic testing market in 2025, driven by advanced healthcare infrastructure, high consumer awareness, and strong adoption of innovative diagnostic solutions.

- Fastest-growing Region: Asia Pacific, fueled by rising healthcare investments, growing prevalence of lifestyle diseases, and expanding diagnostic facilities in countries such as China and India.

- Dominant Test Type: Immunoglobulin Diagnostic Tests account for 31.7% of the immunoprotein diagnostic testing market share, driven by their critical role in accurate immune disorder diagnostics.

- Leading Application: Infectious Disease Testing leads with a 28.5% share, reflecting high global demand for pathogen-specific diagnostics.

|

Global Market Attribute |

Key Insights |

|

Immunoprotein Diagnostic Testing Market Size (2025E) |

US$10.1 Bn |

|

Market Value Forecast (2032F) |

US$16.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.8% |

Market Dynamics

Driver - Rising Prevalence of Chronic and Infectious Diseases Pushes Demand

The global rise in chronic and infectious diseases significantly drives the immunoprotein diagnostic testing market. According to the World Health Organization, non-communicable diseases (NCDs) cause 74% of global deaths, with over 41 million annual fatalities from conditions such as cardiovascular diseases, cancer, and diabetes.

Infectious diseases, such as HIV and hepatitis, affect millions globally, with the CDC reporting over one million HIV cases in the U.S. alone. This growing disease burden fuels demand for precise, biomarker-based diagnostics such as immunoglobulin and C-reactive protein (CRP) tests.

Technological advancements in diagnostic platforms, such as automated immunoassays and multiplex testing, enhance market growth. For example, Roche’s cobas® systems deliver high-sensitivity results with multiplexing capabilities, reducing diagnostic turnaround times. Studies indicate that advanced immunoprotein tests reduce misdiagnosis rates significantly compared to traditional methods. The integration of AI-driven analytics and point-of-care (POC) testing further boosts adoption in clinical settings.

Government initiatives and increased healthcare funding also propel market expansion. In India, schemes such as Ayushman Bharat have improved diagnostic access, with thousands of health centers offering testing services. In North America, policies promoting early detection incentivize laboratories to expand immunoprotein test portfolios, with a strong increase in diagnostic lab investments reported recently.

Restraint - High Costs and Regulatory Challenges Restrict Adoption

High costs of immunoprotein diagnostic tests remain a significant barrier, particularly in emerging markets. Premium reagents, such as monoclonal antibodies, and advanced platforms, such as automated ELISA systems, drive up prices.

For instance, a single immunoglobulin test can cost substantially more than conventional diagnostics, limiting accessibility in regions such as rural India and Latin America. Ongoing expenses for sourcing high-quality biomarkers and meeting certification standards further increase costs.

Supply chain challenges for diagnostic reagents also hinder market growth. Volatile prices for biological materials, such as enzymes and antibodies, require specialized logistics. Industry reports note a shortage of qualified suppliers in the Asia Pacific, increasing reliance on costly imports. Stringent regulatory requirements, such as the EU’s MDR and FDA’s premarket approvals, add compliance costs, delaying product launches and restricting adoption in developing regions.

Opportunity - Innovation in Multiplex Assays and Point-of-Care Testing Boosts Consumption

The development of multiplex and high-sensitivity immunoprotein tests offers significant growth opportunities, particularly in precision medicine and rapid diagnostics. Advanced products, such as multiplex assay kits, enable simultaneous detection of multiple biomarkers, which is essential for busy clinical laboratories and remote healthcare facilities where efficiency and accuracy are critical. Rising consumer demand for rapid and reliable diagnostics further fuels adoption, with point-of-care (POC) testing gaining strong traction in urban and semi-urban markets.

The growing emergence of portable and AI-integrated diagnostic platforms, including chemiluminescence-based POC devices, represents another promising growth avenue. These innovations support early detection of complex conditions such as cancer, autoimmune disorders, and infectious diseases, significantly improving patient outcomes. Multiplex assays also provide the advantage of reducing diagnostic errors and streamlining workflow, which is increasingly valued by healthcare providers.

Additionally, the expansion of e-commerce platforms for laboratory supplies is reshaping market dynamics. Companies offering subscription models and digital sales channels improve accessibility, particularly for small and mid-sized laboratories. This shift strengthens market potential by broadening reach, increasing stakeholder engagement, and accelerating the adoption of next-generation immunoprotein diagnostic solutions.

Category-wise Analysis

Test Insights

The immunoprotein diagnostic testing market is segmented into C-reactive protein diagnostic test, complement system protein diagnostic test, pre-albumin diagnostic test, haptoglobin diagnostic test, immunoglobulin diagnostic test, free light chain diagnostic test, and others. Immunoglobulin diagnostic tests dominate and account for approximately 31.7% share in 2025, due to their critical role in diagnosing immune disorders such as rheumatoid arthritis and lupus. Advanced products, such as Abbott’s ARCHITECT immunoglobulin assays, are widely adopted for their precision and reliability.

C-reactive Protein Diagnostic Tests are the fastest-growing segment, driven by increasing demand for inflammation markers in chronic conditions such as cardiovascular diseases. Innovations in high-sensitivity CRP tests, such as Siemens’ Atellica® solutions, enhance diagnostic accuracy, boosting adoption in hospitals and clinics.

Application Insights

The immunoprotein diagnostic testing market is divided into autoimmune testing, infectious disease testing, allergy testing, endocrine testing, oncology testing, toxicology testing, and others. Infectious disease testing leads with a 28.5% share in 2025, driven by high global demand for detecting pathogens such as HIV, hepatitis, and tuberculosis.

Oncology testing is the fastest-growing segment, fueled by rising demand for cancer biomarkers such as free light chains. The success of tumor-marker tests, such as PerkinElmer’s cancer panels, drives adoption in personalized medicine markets.

Technology Insights

The immunoprotein diagnostic testing market is segmented into radioimmunoassay, immunoturbidity assay, immunoprotein electrophoresis, enzyme-linked immunosorbent assay (ELISA), and others. Enzyme-linked Immunosorbent Assay dominates with a 27% share in 2025, driven by its high throughput and accessibility. Automated ELISA platforms, such as those from Tecan Trading AG, are widely used in North America and Europe.

Chemiluminescence assay is the fastest-growing segment, fueled by demand for high-sensitivity diagnostics. These platforms, equipped with automation and multiplexing, cater to rapid testing needs, boosting adoption in clinical laboratories.

Regional Insights

North America Immunoprotein Diagnostic Testing Market Trends

In North America, the U.S. continues to dominate the global immunoprotein diagnostics market, supported by advanced healthcare infrastructure, strong health awareness, and widespread adoption of preventive diagnostic practices. The demand for immunoglobulin and CRP tests is rising steadily, particularly as healthcare systems emphasize early detection and chronic disease management. Leading players such as Thermo Fisher Scientific Inc. and Danaher Corporation are at the forefront, introducing AI-integrated diagnostic platforms designed to deliver faster, more precise results.

Market preferences are also shifting toward multiplex and point-of-care (POC) systems, as these technologies enable rapid, accurate, and cost-effective testing in both clinical and remote settings. Companies such as Bio-Rad Laboratories are leveraging automation to improve reliability and efficiency, meeting the growing demand for advanced solutions.

Furthermore, regulatory frameworks led by the FDA continue to support validated diagnostics, ensuring high safety and performance. Government initiatives encouraging early disease detection have driven notable expansion in diagnostic laboratory capacity, contributing to a highly competitive and innovation-driven market.

Europe Immunoprotein Diagnostic Testing Market Trends

Europe is led by Germany, the U.K., and France, benefiting from robust regulatory frameworks and consumer demand for precise diagnostics. Germany holds the dominant share, with sales driven by brands such as Agilent Technologies and PerkinElmer, capitalizing on demand for immunoglobulin and CRP tests. The EU’s MDR fosters innovation and compliance, supporting advanced assay development.

In the U.K., growth is fueled by the popularity of automated platforms, with products such as Promega’s multiplex assays appealing to precision medicine needs. France sees rising demand for oncology-focused tests, with companies such as Aurora Biomed offering tailored solutions. Policies promoting sustainable diagnostics strengthen market prospects, ensuring long-term growth.

Asia Pacific Immunoprotein Diagnostic Testing Market Trends

Asia Pacific is emerging as the fastest-growing region in the immunoprotein diagnostics market, driven by rising healthcare needs, government initiatives, and increasing awareness of the importance of early disease detection. India plays a pivotal role, where the growing prevalence of lifestyle-related diseases and initiatives such as Ayushman Bharat are expanding access to affordable diagnostic services. This is boosting demand for cost-effective tests, including CRP and immunoglobulin assays, with companies such as Creative Biolabs offering tailored solutions to serve a broad consumer base.

China’s market growth is driven by the rapid expansion of retail healthcare networks and a growing middle-class population with increased healthcare spending power. Leading global players, including Thermo Fisher, are localizing products to meet patient and clinical requirements, further strengthening market adoption.

In Japan, the focus is on precision and oncology-related testing, with advanced solutions from companies such as Charles River Laboratories gaining market traction. Moreover, the rise of e-commerce platforms and digital health services is expanding accessibility, ensuring sustained regional growth.

Competitive Landscape

The global immunoprotein diagnostic testing market is highly competitive, with global and regional players focusing on innovation, affordability, and regulatory compliance. The rise of multiplex and POC diagnostics intensifies competition, as companies meet stringent health standards and consumer demands. Strategic partnerships and regulatory approvals are key differentiators.

Key Developments

- In April 2024, as part of their ViraxImmune T-Cell diagnostic platform, Virax Biolabs unveiled ImmuneSelect, a collection of immune profiling tools. ImmuneSelect is a research tool that assesses T-cell-driven immunity to help identify and characterize symptoms of post-viral syndromes, such as Long COVID.

- In July 2023, one of the leading companies in the diagnostic testing industry, Quest Diagnostics, released its first Alzheimer's disease diagnostic test to the general public. The AD-Detect test for Alzheimer's disease, which is accessible online, measures possible risks related to the disease and examines brain protein.

Companies Covered in Immunoprotein Diagnostic Testing Market

- Agilent Technologies, Inc.

- Danaher Corporation

- Thermo Fisher Scientific Inc.

- PerkinElmer Inc.

- Bio-Rad Laboratories, Inc.

- Aurora Biomed Inc.

- Tecan Trading AG

- Promega Corporation

- Charles River Laboratories

- Creative Biolabs, Others

Frequently Asked Questions

The immunoprotein diagnostic testing market is projected to reach US$10.1 Bn in 2025.

Rising chronic and infectious disease prevalence, technological advancements, and government health initiatives are key drivers.

The immunoprotein diagnostic testing market is poised to witness a CAGR of 7.5% from 2025 to 2032.

Innovation in multiplex assays and point-of-care testing presents significant growth opportunities.

Thermo Fisher Scientific Inc., Danaher Corporation, and Agilent Technologies, Inc. are among the key players.