- Automotive Components & Materials

- Idler Pulley Market

Idler Pulley Market Size, Share, and Growth Forecast, 2026 – 2033

Idler Pulley Market by Product Type (Flat Belt Idler Pulleys, V-Belt Idler Pulleys, Timing Belt Idler Pulleys, Others), Material (Steel, Plastic, Aluminum, Others), Application (Automotive, Industrial Machinery, Agricultural Equipment, Construction Equipment, Others), and Regional Analysis for 2026-2033

Idler Pulley Market Share and Trends Analysis

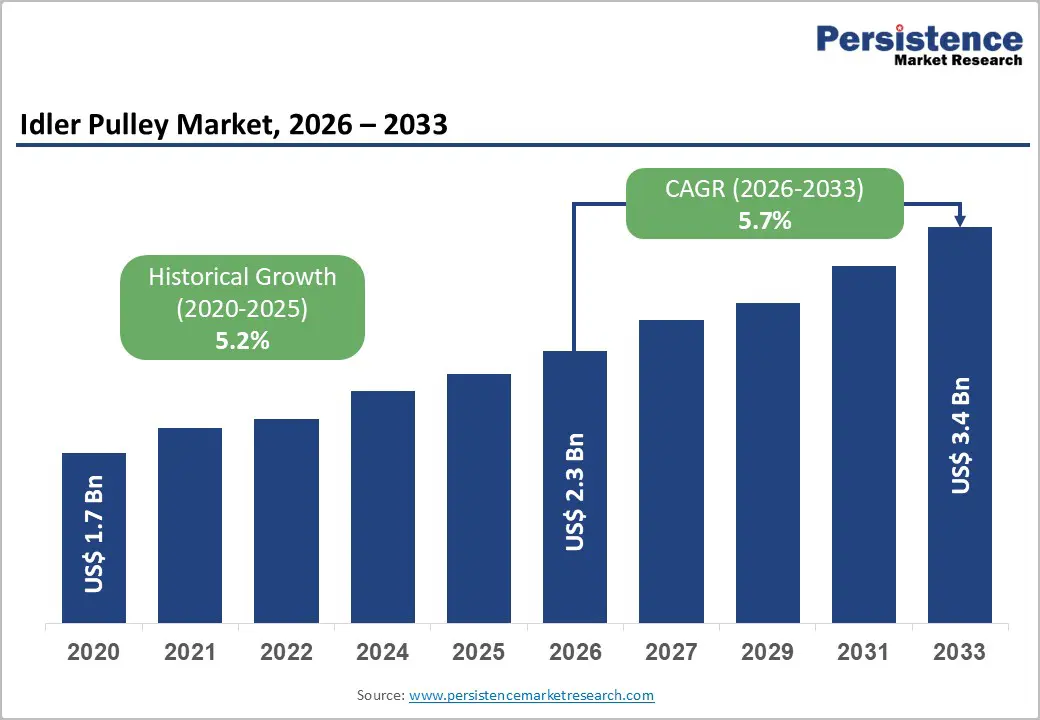

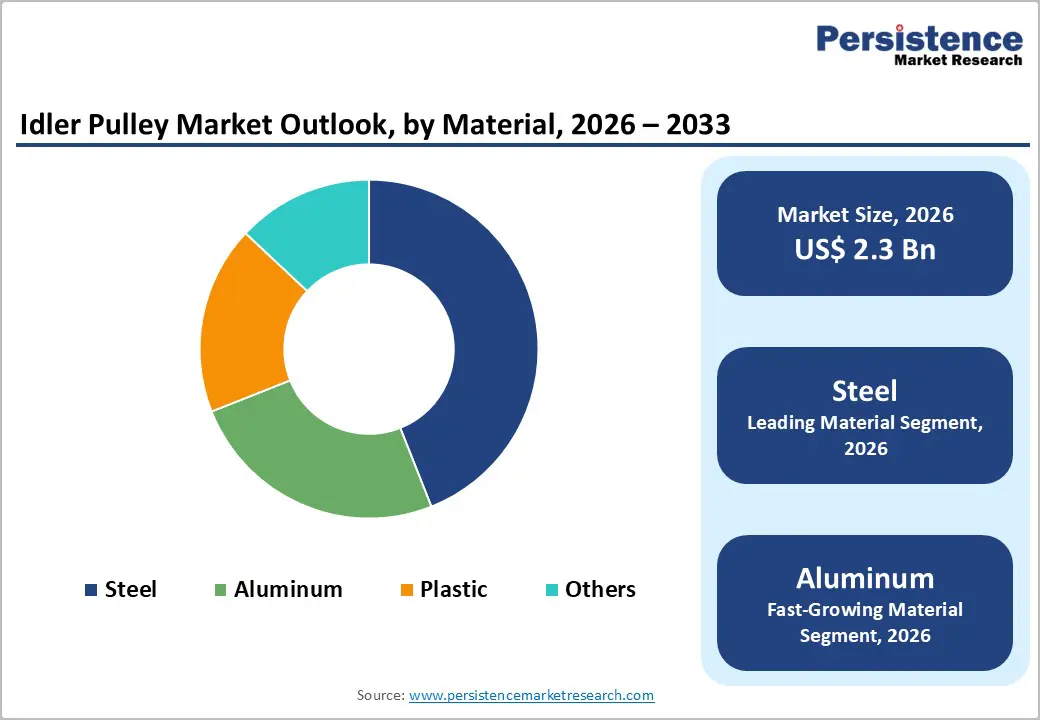

The global idler pulley market size is likely to be valued at US$ 2.3 billion in 2026, and is projected to reach US$ 3.4 billion by 2033, growing at a CAGR of 5.7% during the forecast period 2026−2033.

Sustained demand expansion reflects the critical functional role of idler pulleys in mechanical power transmission systems across automotive, industrial machinery, agricultural equipment, and construction applications. Rising equipment complexity across manufacturing and mobility ecosystems increases the requirement for vibration control, belt alignment, and system efficiency, directly supporting idler pulley integration. Accelerated industrial automation adoption strengthens replacement cycles, as precision-driven operations require consistent belt tension management to reduce downtime and energy losses. Vehicle electrification trends further reinforce market momentum, as electric powertrains and hybrid auxiliary systems depend on optimized belt routing and compact component design to support thermal management and auxiliary functions.

Key Industry Highlights

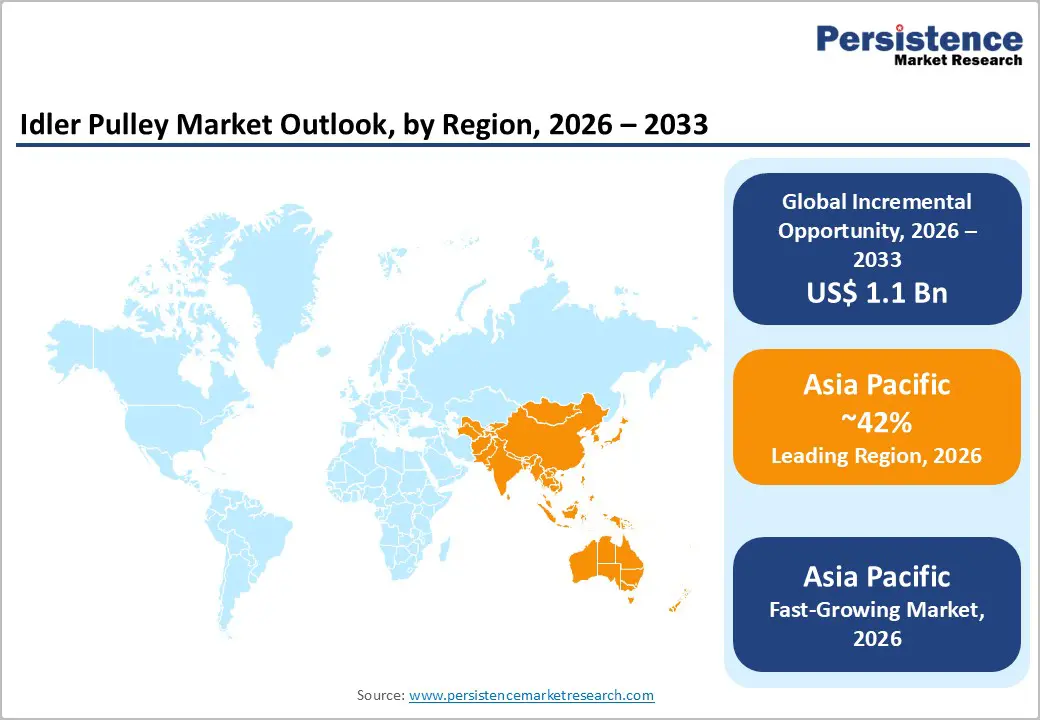

- Dominant Region: Asia Pacific is expected to account for approximately 42% market share in 2026, driven by large-scale manufacturing, localized sourcing, and tiered supplier networks.

- Fastest-growing Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, supported by infrastructure expansion, government initiatives, and equipment modernization.

- Leading Material: Steel idler pulleys are likely to lead with a 44% revenue share in 2026, attributed to their structural strength, thermal stability, and durable fabrication.

- Fastest-growing Material: Aluminum idler pulleys are expected to grow the fastest through 2033, owing to their lightweight design, corrosion resistance, and wear tolerance.

| Key Insights | Details |

|---|---|

| Idler Pulley Market Size (2026E) | US$ 2.3 Bn |

| Market Value Forecast (2033F) | US$ 3.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth in Global Automotive Production and Powertrain Complexity

Rising vehicle output across passenger and commercial segments intensifies demand for durable belt-driven accessory systems that sustain high-volume assembly consistency. Each newly manufactured unit integrates multiple rotational components to stabilize belt tension, manage vibration, and preserve alignment across auxiliary loads such as alternators, air-conditioning compressors, and water pumps. Higher production throughput amplifies the requirement for standardized, cost-efficient, and long-life mechanical elements that reduce warranty exposure and assembly line variability. This linkage between production scale and component demand strengthens procurement volumes for precision-engineered pulleys, particularly in platforms designed for global deployment. According to the International Organization of Motor Vehicle Manufacturers (Organisation Internationale des Constructeurs Automobiles, OICA), global motor vehicle production reached approximately 93 million units in 2023, reinforcing sustained upstream demand for drivetrain and accessory components integrated at factory level.

Powertrain architectures continue to evolve toward higher torque density, compact packaging, and mixed propulsion layouts, placing greater mechanical stress on belt systems. Multi-cylinder downsized engines, turbocharged configurations, start-stop functionality, and hybrid assist units introduce fluctuating load cycles and tighter spatial constraints. These conditions elevate the functional importance of idler pulleys in maintaining belt path stability, noise control, and thermal resilience under dynamic operating profiles. Engineering teams increasingly specify advanced materials, optimized bearing designs, and tighter tolerances to support extended service intervals and compliance with noise, vibration, and harshness benchmarks. Complexity-driven redesign cycles expand content per vehicle and increase replacement frequency across lifecycle phases.

Increasing Competitive Pressure from Integrated Drive System Alternatives

Competitive pressure from integrated drive system alternatives constrains demand as equipment design increasingly prioritizes compact architecture, efficiency, and reduced component count. Integrated solutions such as direct-drive motors, motorized rollers, and enclosed drive modules replace multi-component belt assemblies, removing the functional requirement for idler pulleys used for tensioning, alignment, and vibration control. These alternatives simplify mechanical layouts, lower failure points, and align with lean engineering principles adopted by original equipment manufacturers (OEMs). Design teams favor architectures that minimize assembly time and part inventories, which weakens the strategic relevance of standalone mechanical components. Integrated drives also support tighter tolerances and digital control compatibility, reinforcing adoption in automation-intensive environments where precision and reliability carry higher value than modular replaceability.

This shift alters purchasing behavior across industrial, automotive, and material handling applications, where lifecycle cost optimization guides sourcing decisions. Integrated systems reduce maintenance interventions linked to belt wear, misalignment, and bearing degradation, areas where idler pulleys traditionally play a corrective role. As preventive maintenance budgets face scrutiny, solutions that structurally eliminate maintenance tasks gain preference. Component suppliers focused on conventional pulley systems encounter limited design-win opportunities in new platforms, leading to pricing pressure and margin compression in replacement-driven demand streams. Competitive intensity increases as value migrates from discrete mechanical parts toward system-level solutions delivered by motor and automation specialists.

Material Innovation and High-Performance Component Engineering

Advanced material development and precision-driven component engineering represent a strategic opportunity due to structural shifts in equipment design and operating requirements. Rising power density, compact layouts, and extended duty cycles place sustained stress on conventional metal components, accelerating wear and noise generation. High-performance polymers, engineered composites, and surface-treated alloys deliver improved fatigue resistance, thermal stability, and corrosion control while supporting weight reduction targets. Lower mass improves system efficiency and reduces inertial load on bearings and belts, improving overall drivetrain stability. Precision molding and machining enable tighter tolerances, consistent geometry, and improved balance, aligning with quality expectations of original equipment manufacturers and industrial system integrators.

Engineering innovation further strengthens opportunity through functional integration and lifecycle optimization. Advanced bearing systems, low-friction interfaces, and enhanced sealing architectures extend service intervals and reduce maintenance exposure in demanding environments such as electric mobility platforms, automated logistics, and heavy industrial machinery. Simulation-led design, material testing, and application-specific customization allow suppliers to address noise, vibration, and harshness constraints while meeting sustainability objectives through material efficiency and recyclability. Engineering-led differentiation supports long-term supply agreements, platform-level adoption, and higher switching costs for buyers.

Category-wise Analysis

Product Type Insights

V-belt idler pulleys are poised to lead with a forecasted 38% share in 2026, owing to their widespread deployment across automotive engines, industrial machinery, and agricultural equipment. This leadership is reinforced by long-established usage across internal combustion platforms and belt-driven auxiliary systems where operational familiarity drives procurement confidence. Standardized belt geometries simplify sourcing and enable interchangeability across multiple equipment categories, reducing qualification time for manufacturers. Mature supplier networks support stable pricing, consistent quality, and global availability. Equipment manufacturers favor this segment due to predictable performance, straightforward assembly, and compatibility with legacy mechanical layouts. Strong aftermarket circulation sustains volume momentum, supported by routine maintenance cycles, regular replacement intervals, and continuous incremental design improvements focused on durability, noise control, and operational stability.

Timing belt idler pulleys are anticipated to be the fastest-growing segment between 2026 and 2033, fueled by increasing precision requirements across automotive and automated industrial systems. Growth momentum reflects rising adoption of synchronization-dependent systems where timing accuracy directly influences efficiency and component protection. Advanced powertrain architectures, robotics, and automated production lines require stable belt tracking and controlled tension management. Compact equipment layouts further elevate demand for idlers engineered with tight dimensional tolerances and enhanced material performance. Engineering progress in bearing quality, surface finishes, and thermal resistance enables longer service life under high-speed conditions.

Material Insights

Steel is likely to be the leading segment with a projected 44% of the idler pulley market revenue share in 2026, due to structural strength, thermal stability, and cost efficiency. This dominance reflects long-standing suitability for high-load, high-impact operating environments where mechanical integrity remains a primary selection criterion. Construction, mining, and agricultural equipment demand components capable of sustained operation under vibration, dust exposure, and temperature fluctuation. Steel supports consistent dimensional stability, reducing deformation risk during extended duty cycles. Mature fabrication techniques, including stamping, machining, and heat treatment, enable scalable production with predictable quality. Recycling compatibility aligns with industrial sustainability frameworks and regulatory compliance, while entrenched supplier relationships and material familiarity reinforce procurement confidence among original equipment manufacturers and large fleet operators.

Aluminum idler pulleys are expected to witness the fastest growth between 2026 and 2033, powered by lightweight engineering and corrosion resistance. Adoption accelerates as system designers prioritize mass reduction to improve efficiency, responsiveness, and thermal management. Electrified mobility platforms benefit from lower rotational inertia, supporting energy conservation and extended operating range. Advances in alloy engineering and surface finishing improve wear characteristics and load tolerance, expanding suitability beyond light-duty use. Aluminum enables compact designs and precision machining, supporting integration within space-constrained assemblies.

Application Insights

The automotive segment is slated to hold a dominant position, with an anticipated 41% of the idler puller market share in 2026, driven by consistent vehicle production volumes and auxiliary system complexity. Powertrain architectures, thermal control modules, and accessory drive systems rely on stable belt routing and tension control to maintain operational efficiency. Regulatory pressure linked to emissions and efficiency targets elevates the importance of dependable mechanical subsystems. High model turnover sustains original equipment demand, while extended vehicle lifecycles support steady aftermarket consumption. Stringent supplier qualification frameworks, platform-based sourcing, and multiyear supply agreements reinforce volume continuity. Design standardization across vehicle platforms further supports scale efficiency and predictable replacement cycles, strengthening segment leadership.

Industrial machinery is forecasted to be the fastest-growing end-user segment between 2026 and 2033, boosted by automation, robotics adoption, and predictive maintenance practices. Advanced manufacturing environments demand components that deliver consistent performance under continuous operation and variable load conditions. Expansion of smart factories increases reliance on synchronized motion systems and precision-driven assemblies. Equipment upgrades focused on efficiency, uptime optimization, and digital monitoring accelerate replacement demand. Predictive maintenance strategies identify component wear earlier, shortening service intervals and increasing part turnover.

Regional Insights

North America Idler Pulley Market Trends

North America reflects a demand environment shaped by large-scale equipment utilization, high aftermarket intensity, and strong preference for durability-focused mechanical systems. Automotive production remains anchored by light trucks, sport utility vehicles, and commercial fleets that rely on robust auxiliary drive architectures with extended service intervals. Heavy exposure to construction, mining, oil and gas, and agricultural operations elevates demand for components engineered to withstand high torque, contamination, and temperature variation. Long asset lifecycles and extensive operating hours increase replacement frequency, strengthening aftermarket volumes. Standardization across platforms and fleets supports high-volume procurement, while emphasis on uptime and reliability favors proven designs over rapid specification change.

Growth momentum is driven by structural reinvestment across manufacturing and logistics infrastructure. Reshoring initiatives and capital spending in advanced manufacturing increase deployment of automated equipment and conveyor systems, raising utilization rates of rotating components. Electrification of commercial vehicles and off-highway equipment supports demand for redesigned auxiliary systems optimized for efficiency and noise control. Expansion of e-commerce fulfillment centers and automated warehousing increases demand for continuous-duty mechanical assemblies with predictable maintenance profiles. Predictive maintenance adoption across industrial fleets shortens inspection cycles and accelerates component replacement timing.

Europe Idler Pulley Market Trends

Europe demonstrates a structurally advanced demand profile shaped by engineering intensity, regulatory rigor, and technology-led equipment design. Automotive manufacturing emphasizes precision drivetrains, thermal efficiency, and noise reduction, increasing reliance on high-quality auxiliary components. Strong penetration of premium vehicles, commercial fleets, and rail transport systems sustains steady demand for durable belt-routing solutions. Industrial activity centers on high-value machinery, renewable energy equipment, and advanced manufacturing lines where reliability and lifecycle performance outweigh unit cost considerations. Strict emissions, safety, and material compliance frameworks elevate specification standards, favoring suppliers with validated materials, traceability systems, and advanced testing capabilities. High labor costs incentivize automation, indirectly increasing operating hours and wear rates for rotating components, supporting consistent replacement demand across industrial and mobility applications.

Growth dynamics reflect structural transformation rather than volume expansion alone. Electrification of mobility platforms increases demand for low-noise, high-efficiency auxiliary drive architectures designed for continuous operation. Expansion of wind energy, packaging automation, food processing, and pharmaceutical manufacturing elevates demand for precision-engineered components capable of operating under regulated and hygienic conditions. Circular economy policies encourage material optimization, recyclability, and extended service life, shaping product design priorities. Strong collaboration between original equipment manufacturers, engineering firms, and component suppliers accelerates adoption of advanced materials, digital simulation, and predictive maintenance integration. Export-oriented machinery production further amplifies component demand through embedded supply chains.

Asia Pacific Idler Pulley Market Trends

Asia Pacific is expected to account for approximately 42% of the idler pulley market value in 2026, reflecting deep-rooted manufacturing scale and structural demand concentration across mobility and industrial equipment value chains. High density of automotive assembly plants, agricultural machinery production, and construction equipment manufacturing sustains continuous requirement for belt-driven systems. Localized sourcing of raw materials, bearings, and precision-machined components enables cost control and short production cycles. Strong tier-based supplier integration supports volume consistency and rapid customization aligned with original equipment specifications. High aftermarket circulation driven by extended equipment utilization and predictable maintenance intervals further reinforces volume leadership. Capital investment in capacity expansion across mechanical component manufacturing strengthens throughput capability, positioning this geography as the primary contributor to global consumption.

Asia Pacific is also forecasted to be the fastest-growing regional market for idler pulleys between 2026 and 2033, stimulated by accelerating industrial automation, electric mobility penetration, and infrastructure-led equipment deployment. Expansion of automated manufacturing lines and logistics facilities increases operating hours, elevating replacement frequency for rotating components. Electrified powertrain architectures emphasize low-noise, high-efficiency auxiliary systems, supporting adoption of advanced pulley designs. Government-supported manufacturing programs and export-driven production strategies encourage rapid technology adoption and capacity scaling. Equipment modernization across mining, material handling, and processing industries further drives demand for high-durability components engineered for continuous duty cycles.

Competitive Landscape

The global idler pulley market structure exhibits moderate fragmentation, with leading global suppliers holding approximately 45% combined share. Dominance is primarily driven by engineering expertise, material innovation, and established relationships with original equipment manufacturers. Companies such as Gates Corporation, SKF Group, ContiTech Deutschland GmbH, NTN Corporation, and Dayco Incorporated leverage decades of design experience to deliver high-performance idler pulleys and tensioning systems that meet stringent durability, noise, vibration, and efficiency standards. Product differentiation often arises from proprietary materials, surface treatments, and integrated bearing technologies that enhance component lifespan and operational reliability. Global suppliers also benefit from standardized quality management systems, scale advantages in production, and ability to meet large-volume orders across multiple industrial and automotive platforms. These factors collectively reinforce leadership positions and secure long-term contracts, particularly in regions with high-value mobility and industrial equipment demand.

Regional suppliers maintain relevance through cost efficiency, agility, and aftermarket penetration. Localized production enables faster lead times and adaptability to smaller or niche customer requirements, while aftermarket networks support recurring revenue through maintenance and replacement cycles. Smaller suppliers often focus on specialized material formulations or application-specific designs to compete with global players on performance and value. The combined market structure balances concentration among established global firms with opportunities for agile regional players to capture demand in emerging applications, fleet replacement programs, and price-sensitive segments.

Key Industry Developments

- In January 2026, a neglected Acura Integra GS-R underwent a high-performance K-swap build aiming for a 500 whp target, featuring an upgraded idler pulley to maintain proper belt tension and ensure smooth operation of engine accessories, attracting attention for its ambitious powertrain and motorsport-inspired upgrades.

- In December 2025, an unreleased Teewing Flux eMTB prototype featuring a DJI Avinox motor and an idler pulley to maintain chain tension around its high-pivot suspension teased strong performance potential and value in the electric mountain bike segment.

- In September 2025, the Canyon Sender CFR Team downhill bike was highlighted in a major group test for its high-pivot suspension, 200 mm travel, race-proven performance, and idler pulley system that guides the chain smoothly, reduces slack, and enhances drivetrain stability on challenging terrain.

Companies Covered in Idler Pulley Market

- Gates Corporation

- SKF Group

- ContiTech Deutschland GmbH

- NTN Corporation

- Dayco Incorporated

- Schaeffler Group USA Inc.

- Litens Aftermarket.

- The Timken Company

- NSK Ltd.

Frequently Asked Questions

The global idler pulley market is projected to reach US$ 2.3 billion in 2026.

Rising demand for durable, high-performance belt-driven systems across automotive, industrial, and agricultural equipment is driving the market.

The market is poised to witness a CAGR of 5.7% from 2026 to 2033.

Advancements in material technology and high-performance component engineering present key market opportunities.

Some of the key market players include Gates Corporation, SKF Group, ContiTech Deutschland GmbH, NTN Corporation, and Dayco Incorporated.