- Medical Devices

- Hysteroscopy Instruments Market

Hysteroscopy Instruments Market Size, Share, and Growth Forecast 2026 - 2033

Hysteroscopy Instruments Market by Product Type (Hysteroscopes, Resectoscopes, Handheld Instruments, Hysterosheaths), by Application (Diagnostic Hysteroscopy, Operative Hysteroscopy – Polypectomy, Myomectomy, Endometrial Ablation, Adhesiolysis, Others), Usability (Reusable Instruments, Disposable), by End User (Hospitals, Ambulatory Surgery Centers, Specialty Gynecology Clinics, Fertility Centers and IVF Clinics, Academic & Research Institutes), and Regional Analysis, 20262033

Hysteroscopy Instruments Market Size and Trend Analysis

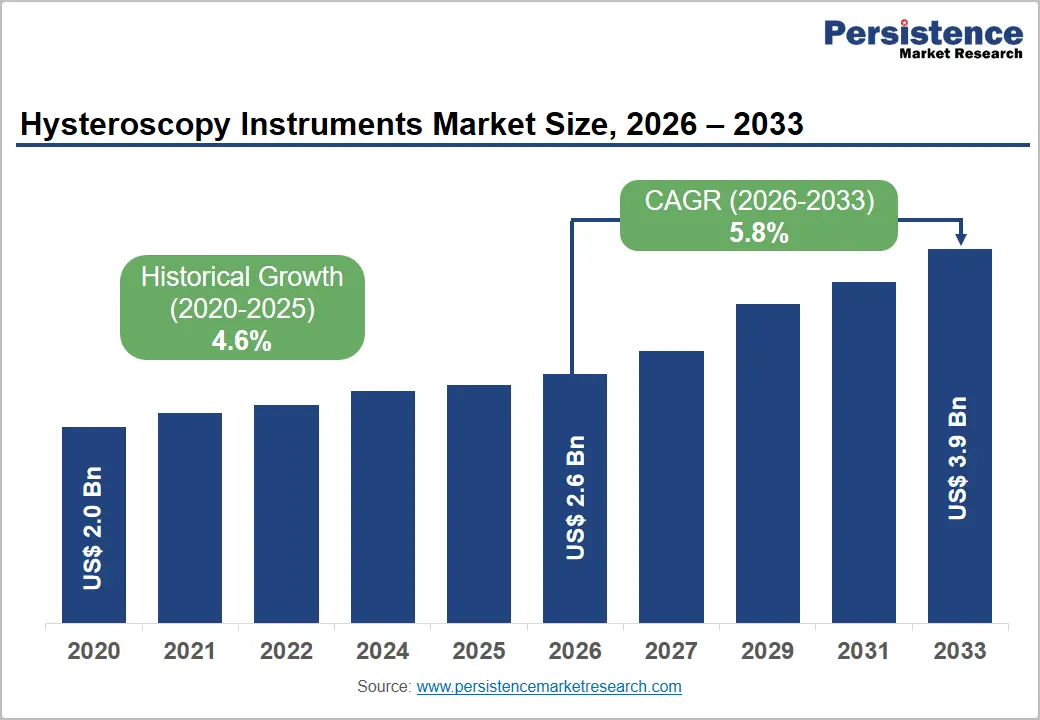

The global hysteroscopy instruments market size is expected to be valued at US$ 2.6 billion in 2026 and projected to reach US$ 3.9 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033. The growing global prevalence of uterine abnormalities including fibroids, endometrial polyps, and intrauterine adhesions along with the increasing adoption of hysteroscopy as the gold-standard minimally invasive diagnostic and operative modality for intrauterine pathology.

The American College of Obstetricians and Gynecologists (ACOG) endorses hysteroscopy as the first-line investigative procedure for abnormal uterine bleeding (AUB) a condition affecting approximately one-third of women of reproductive age globally. Simultaneously, the proliferation of single-use hysteroscope systems, office-based miniaturized platforms, and expanding fertility center networks are broadening hysteroscopy utilization beyond hospital operating rooms into ambulatory and specialist clinic settings worldwide.

Key Market Highlights

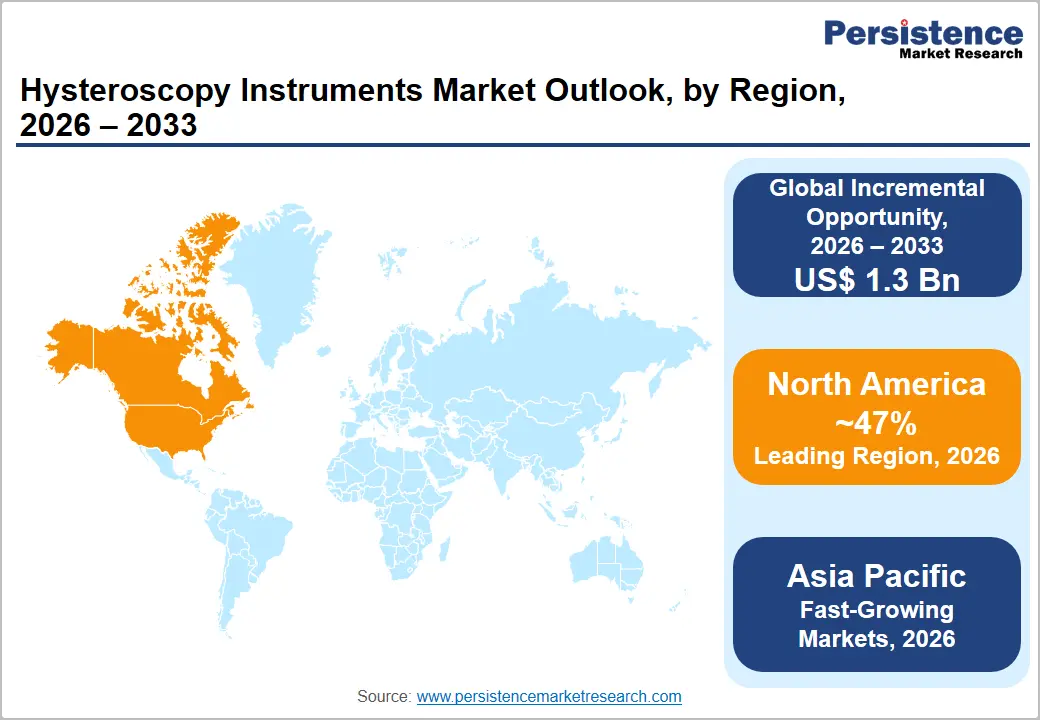

- Leading Region – North America: North America commands approximately 47% of the global hysteroscopy instruments market in 2025, anchored by ACOG-endorsed first-line hysteroscopy protocols for AUB, CMS procedure reimbursement, hospital infection control driving single-use adoption, and commercial leadership of KARL STORZ, Hologic, and CooperSurgical.

- Fastest Growing Region – Asia Pacific: Asia Pacific is the fast-growing market, propelled by China's IVF sector expansion and NHC women's health investment, India's proliferating fertility clinic networks (Nova IVF, Cloudnine), and growing private women's hospital adoption of HD hysteroscopy systems across Southeast Asia and South Korea.

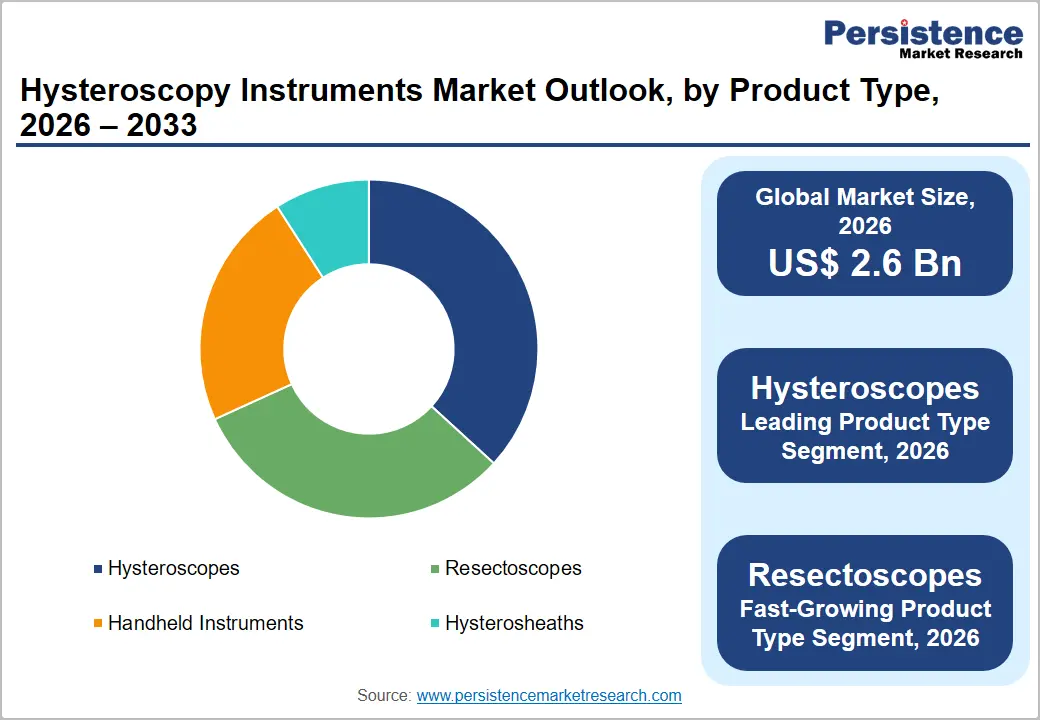

- Dominant Segment – Hysteroscopes: Hysteroscopes hold approximately 37% product type market share in 2025 indispensable in all hysteroscopy procedures with HD and 4K optical systems from KARL STORZ, Richard Wolf, and Olympus commanding premium pricing across hospital OR and ASC settings globally.

- Fastest Growing Segment – Resectoscopes: Resectoscopes are the fastest-growing product type, driven by growing operative hysteroscopy volumes for fibroid and polyp removal endorsed by AAGL as the preferred surgical approach for submucosal fibroids and expanding bipolar energy resectoscope adoption in hospital and ASC settings worldwide.

- Key Opportunity – Single-Use Hysteroscopes and Fertility Center Growth: Single-use disposable hysteroscopes backed by FDA infection control concerns and ESGE guidance and the WHO's estimate of 1 in 6 people globally experiencing infertility (driving 1M+ annual IVF cycles in Europe) represent the highest-growth commercial opportunity frontiers for manufacturers through 2033.

Market Dynamics

Drivers - Rising Global Burden of Uterine Disorders Generating Structured Hysteroscopy Demand

The growing prevalence of uterine pathology is the foundational demand driver for hysteroscopy instruments. Uterine fibroids particularly submucosal variants treated hysteroscopically are estimated to affect approximately 70% of women by age 50 per research published in the American Journal of Obstetrics and Gynecology. Abnormal uterine bleeding (AUB), the leading clinical indication for hysteroscopy referral, affects over 30% of women of reproductive age according to the British Society for Gynaecological Endoscopy (BSGE).

ACOG clinical guidelines mandate hysteroscopy for the investigation of AUB, evaluation of recurrent pregnancy loss, and assessment of intrauterine pathology in infertility workup, creating a large, protocol-driven procedure volume that sustains consistent instrument demand across hospitals, clinics, and fertility centers globally.

Transition to Office and Outpatient Hysteroscopy Expanding Instrument Utilization

The accelerating shift from hospital operating rooms to office-based and ambulatory hysteroscopy settings is significantly expanding the addressable instrument market. Advances in small-caliber hysteroscopes (2.9–3.5 mm outer diameter) and the vaginoscopic 'no-touch' technique, eliminating cervical dilation and anesthesia have enabled same-day office hysteroscopy for diagnostic evaluation and many operative procedures. The European Society of Gynaecological Endoscopy (ESGE) clinical guidelines explicitly recommend office hysteroscopy as the preferred setting for most indications due to equivalent efficacy, lower costs, and superior patient experience. This transition drives demand for purpose-built office hysteroscopy platforms from KARL STORZ, Richard Wolf, and CooperSurgical, increasing the instrument install base in ASC and specialty clinic settings worldwide.

Restraints - High Capital Cost of Reusable Instrument Systems and Reprocessing Complexity

Premium reusable hysteroscopy systems including HD video hysteroscopes and integrated energy resectoscope setups carry capital costs ranging from US$ 20,000 to over US$ 80,000 per configuration, creating adoption barriers for smaller gynecology clinics and budget-constrained hospital departments. Beyond capital outlay, compliance with FDA and EU MDR reprocessing and sterilization validation requirements adds substantial ongoing operational complexity. Endoscope channel cleaning failures have been documented in FDA medical device reports as infection risk events, increasing liability concerns for hospital sterile processing departments and slowing adoption in cost-sensitive healthcare markets.

Training Requirements and Risk of Procedural Complications Limiting Rapid Adoption

Hysteroscopy requires specialized procedural training to achieve competency in safe uterine cavity navigation, fluid management, and energy device use during operative procedures. A systematic review published in Gynecological Surgery estimates uterine perforation rates of 0.8–1.6 per 1,000 procedures. Risks of fluid overload from distension media and cervical trauma further require trained personnel and appropriate facility infrastructure. These safety requirements restrict rapid procedure adoption among general OB/GYN practitioners, moderating market expansion in lower-resource settings and regions with limited specialist training capacity.

Opportunities - Single-Use Disposable Hysteroscopes: Addressing Reprocessing Risk and Expanding Office Adoption

Single-use disposable hysteroscopes represent the most commercially transformative growth opportunity in the hysteroscopy instruments market, driven by growing institutional concern over reprocessing-associated infection risk and the operational simplicity of zero-reprocessing workflows. The FDA medical device adverse event database has documented multiple infection events linked to inadequately cleaned reusable endoscopes, prompting hospital infection control policies favoring disposable alternatives in high-throughput settings. Hologic's Omni Hysteroscope and Boston Scientific's single-use hysteroscopy system have successfully commercialized this segment. The ESGE acknowledges single-use hysteroscopes as a viable clinical alternative. For ASCs, office practices, and fertility centers seeking operational simplicity with no capital investment required, disposable hysteroscopes offer compelling economics representing a growing share of new system purchases globally.

Fertility Centers and IVF Clinics: A High-Growth End-User Segment Powered by the Infertility Epidemic

Fertility centers and IVF clinics represent the fastest-growing end-user category for hysteroscopy instruments, as pre-IVF hysteroscopy for uterine cavity assessment has become a routine clinical protocol at leading reproductive medicine centers globally. The WHO estimates approximately 17.5% of the adult population or 1 in 6 people experience infertility. The European Society of Human Reproduction and Embryology (ESHRE) reports that intrauterine abnormalities are found in up to 50% of infertile women undergoing IVF evaluation abnormalities correctable only via hysteroscopy. With over 1 million ART cycles performed annually in Europe alone (ESHRE), and IVF adoption accelerating in Asia Pacific and Latin America, the fertility center end-user segment offers premium-priced, sustained instrument demand through 2033.

Category-wise Analysis

Product Type Insights

Hysteroscopes represent the leading product type in the hysteroscopy instruments market projected to reach 37% of global revenues in 2026. As the essential, indispensable optical component of every hysteroscopy procedure, the hysteroscope is the primary revenue anchor of the instruments market. Available in rigid, flexible, and single-use configurations spanning calibers from 2.0 mm to 9 mm from miniaturized office systems to full HD/4K operative platforms, hysteroscopes serve the widest range of clinical indications across all settings. Leading manufacturers KARL STORZ SE & Co. KG, Richard Wolf GmbH, and Olympus Corporation dominate the high-definition rigid hysteroscope segment, while Hologic and CooperSurgical lead the emerging single-use hysteroscope product category.

Application Insights

Operative hysteroscopy is the leading application segment, accounting for approximately 62% of revenues in 2025. While diagnostic hysteroscopy drives procedure volume, operative hysteroscopy generates significantly higher per-procedure instrument value through the additional use of resectoscopes, energy hand instruments, morcellators, and specialized accessories required for therapeutic procedures. Hysteroscopic polypectomy and myomectomy are the most frequently performed operative hysteroscopy procedures globally. The American Association of Gynecologic Laparoscopists (AAGL) endorses hysteroscopic myomectomy as the preferred first-line surgical approach for submucosal fibroids a guideline that drives institutional instrument investment. Endometrial ablation procedures using dedicated resectoscope and energy systems represent an additional high-value operative segment supported by strong reimbursement in North America and Europe.

End-user Insights

Hospitals remain the dominant end-user segment in the hysteroscopy instruments market, accounting for approximately 52% of revenues in 2025. Hospital-based gynecology departments and OR suites perform the majority of complex operative hysteroscopy procedures, including resectoscopic myomectomy, endometrial ablation for heavy menstrual bleeding, and adhesiolysis for Asherman's syndrome that require general or regional anesthesia, advanced fluid management, and energy systems unavailable in office settings. Government-funded health systems, particularly NHS England and European national health services drive substantial institutional hysteroscopy instrument procurement through centralized tendering, sustaining consistent revenue for leading instrument manufacturers. The American Hospital Association (AHA) reports over 6,000 registered hospitals in the United States, the majority equipped with dedicated gynecology surgical suites.

Regional Insights

North America Hysteroscopy Instruments Market Trends and Insights

North America accounted for an estimated 45.8% of the global hysteroscopy instruments market in 2026, maintaining its leading position due to favorable reimbursement policies, high procedural volumes, strong adoption of minimally invasive gynecologic techniques, and widespread availability of advanced healthcare infrastructure. Increasing utilization of office-based hysteroscopy and growing demand for disposable hysteroscopy systems are supporting market expansion across hospitals and ambulatory surgery centers. Rising infertility treatment volumes and continued investments in women's health services further contribute to regional growth.

U.S. Hysteroscopy Instruments Market Trends and Insights

The U.S. accounted for approximately 87.2% of the North American hysteroscopy instruments market in 2026. Strong adoption is supported by established reimbursement pathways, high prevalence of uterine fibroids and abnormal uterine bleeding, and increasing use of office-based gynecologic procedures. Healthcare providers continue to invest in advanced hysteroscopy platforms that improve diagnostic accuracy and procedural efficiency. The expansion of fertility treatment centers and ambulatory surgery facilities is creating additional demand for hysteroscopy systems and accessories. In October 2024, Inovus Medical introduced five new modules for its HystAR Hysteroscopy Simulator, enhancing physician training through advanced digital wet-lab functionality and expanding procedural simulation capabilities for hysteroscopic education programs.

Canada Hysteroscopy Instruments Market Trends and Insights

Canada represented nearly 12.8% of the regional market in 2026. Growth is supported by favorable provincial healthcare coverage for hysteroscopic procedures, increasing adoption of minimally invasive gynecologic interventions, and modernization of hospital-based women's healthcare services. Expanding fertility treatment programs and growing awareness regarding early diagnosis of intrauterine abnormalities are contributing to procedural volume growth. Healthcare facilities across Ontario, British Columbia, and Quebec continue to invest in advanced endoscopic equipment to improve patient outcomes and reduce surgical intervention rates. Increasing focus on outpatient gynecologic care is also supporting demand for compact and cost-efficient hysteroscopy systems.

Europe Hysteroscopy Instruments Market Trends and Insights

Europe captured approximately 29.4% of global hysteroscopy instruments revenue in 2026. The region benefits from strong adoption of outpatient hysteroscopy, favorable reimbursement structures, advanced healthcare systems, and established regulatory oversight under EU MDR 2017/745. Growing emphasis on early diagnosis and minimally invasive treatment of intrauterine disorders continues to support demand for both diagnostic and operative hysteroscopy instruments.

Germany Hysteroscopy Instruments Market Trends and Insights

Germany held approximately 25.3% of the European hysteroscopy instruments market in 2026. The country remains a major center for endoscopic innovation, supported by globally recognized manufacturers such as KARL STORZ and Richard Wolf. High procedural volumes, strong hospital infrastructure, and broad physician expertise in minimally invasive gynecology contribute to sustained demand. Healthcare providers continue adopting advanced imaging systems, fluid management technologies, and operative hysteroscopy platforms to improve procedural outcomes. Ongoing product development and replacement cycles across university hospitals and specialty clinics are expected to maintain Germany’s leadership position within the European market.

UK Hysteroscopy Instruments Market Trends and Insights

The UK accounted for approximately 17.5% of the European market in 2026. The NHS outpatient “See and Treat” model continues to increase utilization of hysteroscopy by enabling diagnosis and treatment during a single patient visit. Rising focus on reducing surgical waiting lists and improving women's health services is driving procurement of advanced hysteroscopy systems. Hospitals are increasingly adopting portable and single-use technologies to improve workflow efficiency. In May 2024, Meditrina received CE Mark and UKCA approval for its Aveta Hysteroscopy System, enabling broader commercialization across the UK and supporting access to innovative hysteroscopy technologies that meet stringent regulatory and clinical performance standards.

Asia Pacific Hysteroscopy Instruments Market Trends and Insights

Asia Pacific accounted for approximately 21.6% of the global hysteroscopy instruments market in 2026 and remains the fastest-growing regional market. Rapid expansion of fertility services, increasing awareness of minimally invasive gynecologic procedures, and rising healthcare expenditure are major growth drivers. Governments across the region are investing heavily in women's health infrastructure, while private hospitals and fertility clinics continue expanding their procedural capabilities. Growing demand for advanced visualization systems and office-based hysteroscopy is expected to support the development of regional CAGR.

China Hysteroscopy Instruments Market Trends and Insights

China is likely to represent approximately 42.5% of the Asia Pacific in 2026. Market growth is fueled by government initiatives supporting reproductive health, the expansion of fertility treatment services, and continued modernization of hospital infrastructure. Large tertiary hospitals are increasingly upgrading to HD and digital hysteroscopy systems to improve diagnostic precision and procedural efficiency. The growth of reproductive medicine centers and rising adoption of minimally invasive gynecologic procedures are further strengthening demand. Domestic manufacturing capabilities are also expanding, improving accessibility to advanced hysteroscopy technologies throughout the country.

India Hysteroscopy Instruments Market Trends and Insights

India is likely to account for approximately 20.7% of the Asia Pacific market in 2026 and is among the fastest-growing countries in the region. Increasing infertility treatment demand, expansion of private fertility networks, and improving access to minimally invasive gynecologic care are supporting market growth. Organizations such as Nova IVF Fertility and Cloudnine Hospitals continue expanding their footprint, increasing the adoption of diagnostic and operative hysteroscopy systems. Investments in tier-2 and tier-3 city healthcare infrastructure, coupled with growing physician training initiatives, are accelerating procedural adoption. Rising awareness of early diagnosis and treatment of uterine disorders is expected to further stimulate demand for hysteroscopy instruments over the forecast period.

Competitive Landscape

The hysteroscopy instruments market is moderately consolidated, with KARL STORZ SE & Co. KG, Olympus Corporation, Richard Wolf GmbH, and Medtronic plc collectively accounting for over 50% of global revenues. Key competitive differentiators include optical image quality (HD and 4K), comprehensive system ecosystem integration, energy platform compatibility, and global service networks. Specialty challengers Hologic, CooperSurgical, and Boston Scientific are aggressively capturing the single-use and office hysteroscopy segments. Emerging business models include subscription-based single-use supply programs and AI-integrated digital documentation platforms. Strategic M&A is actively reshaping the women's health surgical instrument landscape.

Key Developments:

- In August 2024, Minerva Surgical announced the immediate and exclusive distribution of a new disposable hysteroscope. It was displayed at the Annual Clinical & Scientific Meeting of American College of Obstetricians and Gynecologists in San Francisco. The firm aims to rebrand the new disposable hysteroscope as HERizon and improve the standards of efficiency in gynecological care.

- In May 2024, Meditrina bagged the FDA 510(k) clearance for its Gen 2 bipolar RF hysteroscopy system. The novel system includes bipolar radiofrequency technology and a new bipolar RF device called the Aveta Glo. This represents a key innovation in minimally invasive gynecologic procedures.

Companies Covered in Hysteroscopy Instruments Market

- KARL STORZ SE & Co. KG

- Medtronic plc

- Richard Wolf GmbH

- CooperSurgical, Inc.

- Hologic, Inc.

- Stryker Corporation

- Boston Scientific Corporation

- Medicon eG

- B. Braun Melsungen AG

- Erbe Elektromedizin GmbH

- EMOS Technology GmbH

- Johnson & Johnson Services, Inc.

- Smith & Nephew plc

- XION GmbH

- Olympus Corporation

- Others

Frequently Asked Questions

The global hysteroscopy instruments market is projected to be valued at US$ 2.6 billion in 2026, driven by ACOG-mandated hysteroscopy protocols for AUB evaluation, fibroids affecting approximately 70% of women by age 50 (American Journal of Obstetrics and Gynecology), growing IVF-related pre-transfer hysteroscopy adoption, and rapid commercialization of single-use hysteroscope platforms by Hologic, Boston Scientific, and CooperSurgical.

Rising prevalence of abnormal uterine bleeding and uterine fibroids, increasing IVF procedures, growing adoption of minimally invasive gynecologic surgeries, and expanding office-based hysteroscopy are the primary demand drivers in the hysteroscopy instruments market.

North America leads with approximately 47% market share in 2025, dominated by the United States with ACOG-endorsed hysteroscopy guidelines for AUB and infertility evaluation, CMS reimbursement under CPT codes 58558–58561, a rapidly growing fertility center network driving pre-IVF hysteroscopy, and commercial leadership of KARL STORZ, Hologic, CooperSurgical, and Boston Scientific in hysteroscopy instrument innovation.

Key market opportunities include expansion of single-use hysteroscopy systems, integration of AI-assisted imaging technologies, increasing penetration in emerging fertility centers, and rising adoption of outpatient hysteroscopic procedures in developing healthcare markets.

The leading companies include KARL STORZ SE & Co. KG (HOPKINS II, TERESA systems), Olympus Corporation, Richard Wolf GmbH, Medtronic plc, Hologic, Inc. (Omni single-use), CooperSurgical, Inc. (Ceragem), Boston Scientific Corporation, Stryker Corporation, Erbe Elektromedizin GmbH, and XION GmbH, collectively spanning premium reusable optical platforms to innovative single-use hysteroscopy systems for office and fertility center settings.