- Hardware & Software IT Services

- Hyper-converged Infrastructure Market

Hyper-converged Infrastructure Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Hyper-converged Infrastructure Market by Component Type (Hardware, Software, Service), Deployment Mode (On-Premise Deployment, Cloud-Based Deployment, Hybrid Deployment), Organization Size (Large Enterprises, Small & Medium Enterprises (SMEs)), End-user (Enterprises, Cloud Service Providers, and Colocation Providers) Industry (Banking, Financial Services & Insurance (BFSI), IT & Telecom, Healthcare, Government & Public Sector, Manufacturing) and Regional Analysis for 2026 - 2033

Hyper-converged Infrastructure Market Size and Trends Analysis

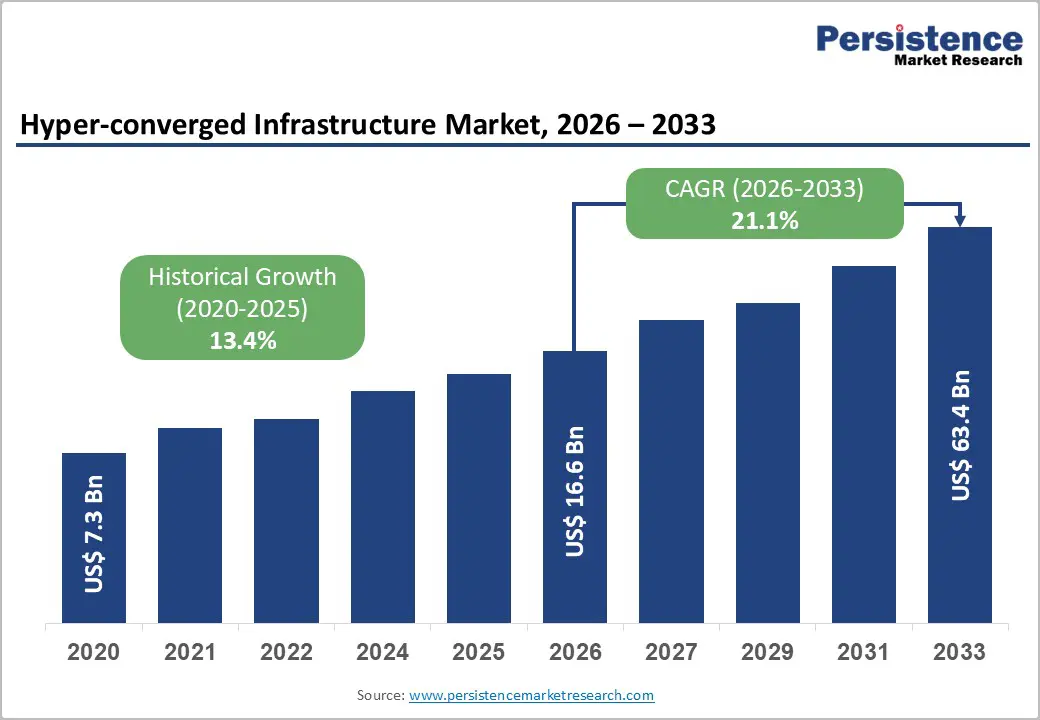

The global hyper-converged infrastructure market size is likely to be valued at US$ 16.6 billion in 2026 and is projected to reach US$ 63.4 billion by 2033, growing at a CAGR of 21.1% between 2026 and 2033.

This accelerated growth trajectory reflects enterprise modernisation imperatives, digital transformation acceleration, and infrastructure consolidation priorities across global markets. The market expansion is fundamentally driven by organisational shifts toward cloud-native architectures, regulatory compliance automation requirements, and total cost of ownership optimisation that consolidated infrastructure platforms deliver. The market is demonstrating strong momentum in Asia-Pacific and among financial services organisations, where infrastructure modernisation directly enables competitive differentiation and regulatory compliance.

Key Industry Highlights:

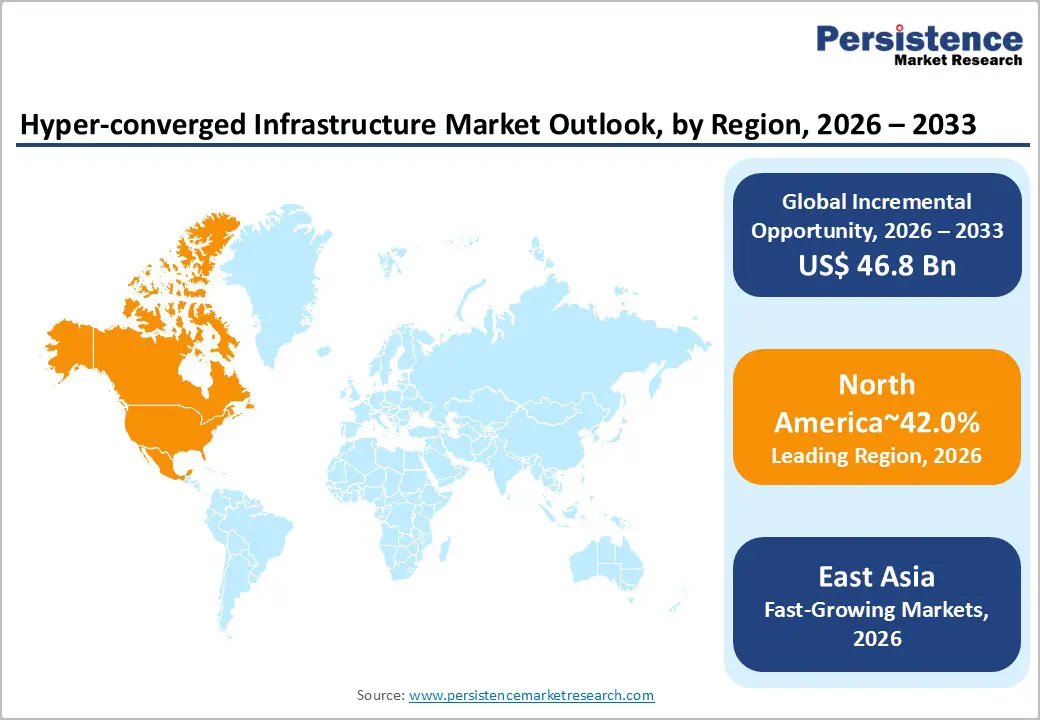

- Regional Leadership: North America dominates the Global Hyper-converged Infrastructure Market with a ~42% share, supported by mature enterprise IT adoption, the presence of hyperscale cloud providers, and strong demand across BFSI, healthcare, and hybrid cloud applications.

- Strong European Presence: Europe accounts for ~27% of market share, driven by GDPR-aligned compliance, financial sector modernization, and enterprise focus on data sovereignty and consolidated IT infrastructure.

- High-Growth East Asia: East Asia holds ~15% share, led by China, Japan, and South Korea, fueled by government-led digital transformation, 5G deployment, edge computing, and AI infrastructure expansion.

- Leading Solution Segment: Hardware leads with ~52% share, reflecting widespread adoption of integrated, pre-configured servers, storage, and networking appliances optimised for HCI performance.

- Fastest-Growing End-user: Enterprises are the fastest-growing end-user category, driven by infrastructure modernisation, containerised application adoption, and multi-site deployment needs.

| Key Insights | Details |

|---|---|

| Hyper-converged Market Infrastructure Size (2026E) | US$ 16.6 Bn |

| Market Value Forecast (2033F) | US$ 63.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 21.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 13.4% |

Market Dynamics

Drivers - Enterprise Infrastructure Consolidation and Operational Efficiency Optimisation

Enterprise organisations globally are pursuing aggressive infrastructure consolidation strategies to reduce operational complexity, minimise capital expenditure, and achieve superior return on infrastructure investment. Traditional three-tier infrastructure separating compute, storage, and networking across multiple vendors and management silos creates operational overhead, increases management personnel requirements, and constrains deployment velocity that increasingly competitive markets demand.

Consolidated infrastructure solutions address these constraints by integrating computers, storage, and networking into unified, software-defined platforms managed through centralised interfaces. The Hyper-converged Infrastructure Market directly benefits from this consolidation imperative, as enterprises recognise that integrated platforms reduce infrastructure operational costs by 30-40% while simultaneously enabling faster application deployment cycles, which are essential for digital competitiveness.

Government and regulatory drivers further accelerate the adoption of consolidation. India's financial services sector, having expanded 50-fold in market capitalisation to reach Rs. 91 lakh crore (US$ 1 trillion) in 2025 from Rs. 1.8 lakh crore in 2005, demonstrates infrastructure modernisation patterns central to sector growth. Banks and financial institutions utilise consolidated HCI platforms to support real-time payments, regulatory reporting, and customer analytics that legacy infrastructure architectures struggle to deliver cost-effectively.

The transition from traditional banking to digital-first financial services requires infrastructure platforms capable of supporting containerised applications, rapid scaling, and integrated security capabilities native to modern hyperconverged solutions. Across global markets, enterprise infrastructure consolidation represents a structural shift that will sustain demand for the Hyper-converged Infrastructure Market over the forecast period, as organisations systematically retire legacy three-tier infrastructure in favour of consolidated platforms.

Regulatory Compliance and Data Security Architecture Evolution

Regulatory frameworks globally have undergone substantial expansion, mandating rigorous data protection, business continuity, disaster recovery, and compliance automation capabilities that have fundamentally altered infrastructure design requirements. The European Union's financial and insurance activities sector generated €0.9 trillion in value added in 2022, employing nearly 5 million people across 867,000 enterprises, with a gross operating rate of 24.0% reflecting financial sector profitability and substantial infrastructure investment capacity. European banking sector assets totalled €43.6 trillion in 2023, with organisational restructuring reducing credit institutions from 5,304 to consolidate operations and implement digitalization-driven efficiency improvements that hyperconverged infrastructure platforms facilitate

Regulatory mandates across geographies, including GDPR (data privacy), PCI-DSS (payment security), HIPAA (healthcare records), SOX (financial reporting), and sector-specific frameworks, have created structural demand for infrastructure solutions providing integrated compliance automation, audit logging, encryption, and business continuity capabilities. Hyperconverged infrastructure addresses these requirements by consolidating compliance functions, disaster recovery mechanisms, and security controls into unified platforms, reducing the organizational burden of manual compliance verification and infrastructure-specific security management.

Organisations implementing HCI-based compliance infrastructure report a 30-40% reduction in audit cycle time, while simultaneously improving their security posture through centralized, auditable infrastructure management. The hyper-converged infrastructure market captures this opportunity by having vendors incorporate compliance automation directly into management interfaces, enabling finance and healthcare organizations to achieve regulatory objectives while reducing infrastructure operational complexity.

Restraint - Capital Investment Requirements and Budget Cycle Constraints

Despite offering superior long-term total cost of ownership, hyperconverged infrastructure solutions require substantial upfront capital investment, which constrains their adoption among cost-conscious organisations with limited capital budgets. Integrated hardware-software systems require simultaneous infrastructure refresh cycles, creating purchasing friction when existing infrastructure has remaining depreciation schedules.

Organisations must justify multi-million-dollar HCI investments against legacy infrastructure with already recorded sunk costs, which creates hesitation to purchase despite demonstrated long-term economic advantages. Migration complexity from three-tier environments introduces project risks, including application compatibility validation, staff retraining requirements, and potential service disruption during transition phases that extend procurement cycles and defer purchasing decisions.

Opportunity - Edge Computing Infrastructure Deployment and Real-Time Processing Acceleration

Edge computing architectures driven by 5G network deployment, Internet of Things sensor proliferation, autonomous systems requirements, and distributed artificial intelligence inferencing have created substantial infrastructure opportunities for hyperconverged solutions optimized for remote, latency-sensitive deployments. Traditional centralized data centers concentrate computing power in limited geographic locations, creating latency, bandwidth, and cost inefficiencies for applications requiring sub-millisecond response times or local data processing. Hyperconverged infrastructure vendors have responded through compact, modular HCI nodes designed for edge deployment featuring simplified management, reduced power consumption, and integrated AI/ML capabilities suited to edge-specific workloads.

India's digital infrastructure transformation creates specific opportunities for edge computing. The nation's telecom sector is positioned as the world's second-largest telecommunications market in 2025, with 1.21 billion subscribers and a tele-density of 86.09% has expanded internet adoption to 979 million users by June 2025. Government initiatives, including BharatNet (rural broadband), PM-WANI (public WiFi), and the draft National Telecom Policy 2025, are accelerating 5G and fiber infrastructure deployment, driving demand for distributed data center infrastructure closer to population centers. These initiatives represent US$ 20-30 billion in infrastructure investment opportunities through 2030, with substantial allocation directed toward edge HCI solutions supporting secure, compliant infrastructure for digital government service delivery, e-commerce platforms, and telecommunications network expansion.

India's telecom sector demonstrates the scale of the edge infrastructure opportunity: sector gross revenue increased from US$ 39.22 billion in FY24 to US$ 43.42 billion in FY25, while broadband subscriptions expanded from 149.75 million in 2016 to 979 million in 2025. This expansion requires a distributed computing infrastructure supporting content delivery, real-time analytics, and edge-based application processing that centralized data centre models cannot efficiently support.

The hyper-converged infrastructure market captures this edge computing opportunity through vendors such as Scale Computing (now acquired by Acumera in July 2025) and DataCore (which acquired StarWind in May 2025), both of which explicitly target distributed and edge deployments with streamlined, scalable HCI solutions tailored to remote operational environments.

BFSI Digital Transformation and Financial Innovation Platform Requirements

Organizations across the Banking, Financial Services & Insurance industry globally are pursuing aggressive digital transformation initiatives to compete with fintech entrants, meet evolving regulatory requirements, and deliver digital-first customer experiences that modern financial services consumers demand. India's BFSI sector exemplifies this urgency: it expanded 50-fold in market capitalisation to reach Rs. 91 lakh crore (US$ 1 trillion) in 2025 from Rs. 1.8 lakh crore in 2005, now contributing 27% to GDP compared to 6% in 2005. Gross non-performing assets declined from 5.8% in FY22 to 2.2% in FY25, indicating stronger financial sector health and enabling continued technological investment.

Financial institutions require infrastructure platforms supporting real-time payment processing, AI-driven fraud detection, customer analytics, and regulatory compliance automation workloads demanding high availability, rapid scaling capability, and integrated security controls that hyperconverged infrastructure provides.

Life insurance AUM reached Rs. 61.6 lakh crore (US$ 693 billion) and mutual fund AUM rose to Rs. 75 lakh crore (US$ 844 billion) by March 2025, reflecting a financial sector shift toward capital markets and investment management requiring modern infrastructure supporting complex analytics and real-time portfolio processing. The Hyper-converged Infrastructure Market captures the BFSI opportunity through industry-specific solutions that incorporate compliance automation, disaster recovery, and high-availability capabilities essential to financial services operations.

Category-wise Analysis

Component Type Insights

Hardware components represent the dominant market category within the Hyper-converged Infrastructure Market, commanding 52% of market value through 2026. This dominance reflects that hardware remains the primary cost component of integrated infrastructure solutions, encompassing servers, storage controllers, networking components, and power/cooling infrastructure integrated into unified systems.

Hyperconverged appliances combine commodity server hardware (leveraging proven processor architectures), solid-state storage (optimising performance), and networking infrastructure into pre-configured, optimised systems that eliminate integration complexity and deployment risk. Organisations purchasing HCI solutions allocate approximately 45-55% of total infrastructure budgets toward hardware acquisition, reflecting both the capital intensity of physical infrastructure and vendor differentiation through optimised hardware configurations.

Hardware component dominance is further reinforced by vendor business models that bundle software licenses with hardware systems, creating integrated product offerings where hardware represents the primary revenue line item. Dell Technologies' VxRail platform, Nutanix's product portfolio, Cisco's HyperFlex, and HPE's SimpliVity solutions all leverage commodity hardware optimised through vendor-proprietary configurations, software integration, and support bundling.

Industry Insights

Enterprises represent the dominant end-user category, accounting for 60% of the hyper-converged infrastructure market through 2026, reflecting substantial infrastructure modernization requirements among large organizations with complex multi-data-center environments and diverse application portfolios. Enterprise organizations, defined as entities with 500+ employees and annual IT budgets exceeding US$ 10 million, possess capital resources, technical expertise, and organizational complexity that justify hyperconverged infrastructure investments. Enterprise purchasing power enables HCI vendors to support large-scale implementations spanning 50-200+ nodes across geographically distributed locations, deployments that smaller organizations cannot execute or justify economically.

Enterprise HCI adoption is concentrated in sectors with the highest digital transformation urgency: financial services, healthcare, telecommunications, and government organizations, where infrastructure modernization directly enables strategic business objectives. IT operations teams pursue HCI to reduce data center operating costs and simplify management; development organizations adopt HCI-hosted Kubernetes and container platforms to accelerate application modernization; security organizations utilize HCI's integrated compliance and disaster recovery capabilities to meet regulatory mandates. Enterprise implementations report a 30-40% reduction in infrastructure capital requirements compared to traditional three-tier deployments while simultaneously reducing annual operating expenses by 20-30% through consolidated management and optimized power consumption.

Banking, Financial Services & Insurance is the fastest-growing vertical in the Hyper-converged Infrastructure Market, reflecting the profound digital transformation underway across financial services globally as fintech competition, regulatory evolution, and customer expectations drive infrastructure modernisation. Financial institutions increasingly recognise that legacy core banking systems and three-tier infrastructure constrain innovation velocity, creating competitive vulnerability to digital-native competitors. Hyperconverged infrastructure enables financial institutions to modernise infrastructure supporting payment systems, fraud detection, real-time analytics, and customer engagement platforms essential for competitive differentiation.

Regional Insights and Trends

North America Hyper Converged Infrastructure Market Trends

North America commands the largest share of the global hyper-converged infrastructure market, representing 42% of global demand through 2026, reflecting the region's mature enterprise IT market, concentrated hyperscale cloud provider presence, and substantial capital availability for infrastructure modernization. North American enterprises have achieved the highest HCI penetration globally due to competitive pressure to modernize legacy infrastructure and support hybrid cloud strategies essential for modern enterprise competitiveness. The region benefits from established technology vendor ecosystems, deep systems integrator competency, and enterprise purchasing sophistication, which accelerate HCI adoption.

Enterprise purchasing sophistication and established vendor relationships enable North American organisations to negotiate HCI pricing aggressively, compressing vendor margins but expanding the total addressable market through volume adoption. Regulatory maturity within North America, with HIPAA, SOX, and PCI-DSS frameworks well-established and compliance best practices widely documented, creates a predictable environment where BFSI and healthcare organisations confidently deploy HCI, knowing regulatory pathways are well-defined.

The presence of hyperscale cloud providers (AWS, Microsoft Azure, Google Cloud) headquartered in North America creates competitive pressure on on-premises HCI vendors to provide seamless hybrid cloud capabilities that drive extensive partnership development. U.S. e-commerce expansion, with seasonally adjusted sales reaching US$ 310.3 billion in Q3 2025 (growing 5.1% year-on-year and accounting for 16.4% of total retail sales), demonstrates sustained digital infrastructure investment requirements supporting rapid application scaling and real-time commerce platforms that HCI efficiently supports.

East Asia Hyper-Converged Infrastructure Market Trends

East Asia represents the fastest-growing region within the hyper-converged infrastructure market, capturing 15% of global demand through 2026 and demonstrating accelerated expansion driven by government-directed digital infrastructure investment, rapidly expanding cloud service provider presence, and urgent enterprise digital transformation across China, Japan, and South Korea. East Asia's prominence reflects the region's role in supporting AI infrastructure expansion, 5G network deployment, and sovereign cloud initiatives prioritizing on-premises and regional infrastructure over US-based cloud providers.

China leads East Asian HCI adoption through government-mandated digital transformation and financial sector modernisation. Banking assets reached RMB 467.3 trillion in Q2 2025, up 7.9% year-on-year, with large commercial banks accounting for 43.7% of total banking assets and inclusive loans to micro and small enterprises rising 12.3% to RMB 36 trillion. This expansion requires distributed infrastructure supporting on-premises compliance, public cloud cost optimisation, and edge computing for real-time processing that hyperconverged infrastructure uniquely facilitates.

Commercial banks maintained strong asset quality with an NPL ratio of 1.49% and a capital adequacy ratio of 15.58%, supporting continued technology investment velocity. Insurance sector assets grew 9.2% to RMB 39.2 trillion, with primary premium income reaching RMB 3.7 trillion, requiring infrastructure to support real-time customer service, policy analytics, and claims processing, which HCI platforms efficiently enable.

Japan and South Korea maintain significant HCI adoption patterns as mature technology markets with established enterprise IT infrastructure. South Korea's leadership in technology sectors, 5G deployment, and digital government initiatives continues to drive HCI adoption, while Japan demonstrates steady infrastructure modernisation, reflecting enterprise emphasis on reliability, security, and integration with existing technology investments. East Asian competitive dynamics remain distinct from those in North America, with Chinese vendors, including Huawei and Lenovo, expanding their HCI offerings to meet regional requirements and compliance frameworks.

Europe Hyper-converged Infrastructure Market Trends

Europe represents the second-largest regional market within the Global Hyper-Converged Infrastructure Market, accounting for 27% of global demand through 2026, reflecting mature enterprise IT markets, strong regulatory frameworks driving infrastructure modernization, and substantial capital availability for digital infrastructure investment. The region demonstrates distinctive characteristics driven by GDPR implementation, strong regulatory compliance requirements, and an enterprise emphasis on data sovereignty and privacy protections, which hyperconverged infrastructure platforms address through consolidated infrastructure that provides explicit control over data residency.

European financial and insurance sector demonstrates substantial infrastructure investment capacity supporting HCI market expansion. The EU financial and insurance activities sector generated €0.9 trillion in value added in 2022, employing nearly 5 million people across 867,000 enterprises, with a gross operating rate of 24.0% and wage-adjusted labor productivity of 236.1%.

Germany, France, Italy, Spain, and Poland together account for over 65% of EU value added and employment, concentrating the HCI market opportunity within large Western European economies. The European banking sector's assets totaled €43.6 trillion in 2023, with loan portfolios of €26.8 trillion and deposit growth of 1.2% to €17.3 trillion, indicating continued financial sector stability and investment capacity in modernizing infrastructure. The banking sector underwent structural transformation, with credit institutions declining 2.9% to 5,304, driven by digitalization and efficiency-focused restructuring, thereby accelerating HCI adoption as banks consolidate branch infrastructure.

Competitive Landscape

The global hyper-converged infrastructure (HCI) market exhibits a moderately consolidated structure, characterised by the strong presence of a few leading players alongside several mid-tier and niche providers. Nutanix, VMware, Dell Technologies, Hewlett Packard Enterprise (HPE), Cisco Systems, and NetApp collectively command a significant share of the market, supported by broad product portfolios, global distribution networks, and deep enterprise relationships. These companies compete primarily on software innovation, integrated hardware-software offerings, and hybrid-cloud compatibility.

Continuous investments in R&D, strategic partnerships, and ecosystem expansion strengthen their competitive positions. At the same time, the presence of regional and specialised vendors prevents the market from becoming fully consolidated. Overall, the competitive landscape reflects a semi-consolidated market with oligopolistic tendencies at the top tier and competitive intensity across the broader vendor base.

Key Industry Developments

- July 31, 2025 - Acumera acquired Scale Computing, a pioneer in HCI and edge virtualisation, creating the largest edge computing-focused software company. The acquisition expanded AI-ready and HCI capabilities, enabling enterprises and MSPs to securely deploy, manage, and scale workloads across distributed locations with low-latency and simplified operations.

- May 25, 2025 - DataCore strengthened its Hyper-converged Infrastructure market leadership with the acquisition of StarWind, expanding HCI capabilities to edge, remote office, and small business environments. The move enables DataCore to deliver streamlined, software-defined HCI solutions across distributed operations, enhancing scalability, operational efficiency, and support for diverse workloads across core, edge, and cloud infrastructures.

Companies Covered in Hyper-converged Infrastructure Market

- Dell Technologies Inc. (Dell EMC)

- Nutanix, Inc.

- Cisco Systems, Inc.

- Hewlett Packard Enterprise Company (HPE)

- Huawei Technologies Co., Ltd.

- NetApp, Inc.

- VMware, Inc.

- Pivot3, Inc.

- Scale Computing, Inc.

- StarWind Software, Inc.

- DataCore Software Corporation

- Maxta, Inc.

- Microsoft Corporation

- HiveIO, Inc.

- Super Micro Computer, Inc.

- Hitachi Vantara LLC

- Diamanti, Inc.

- Lenovo Group Limited

- NEC Corporation

- Riverbed Technology, Inc.

- IBM

- Fujitsu Limited

- Sangfor Technologies Inc.

- StorMagic Ltd.

Frequently Asked Questions

The global Hyper-Converged Infrastructure Market is projected to be valued at US$ 16.6 Bn in 2026.

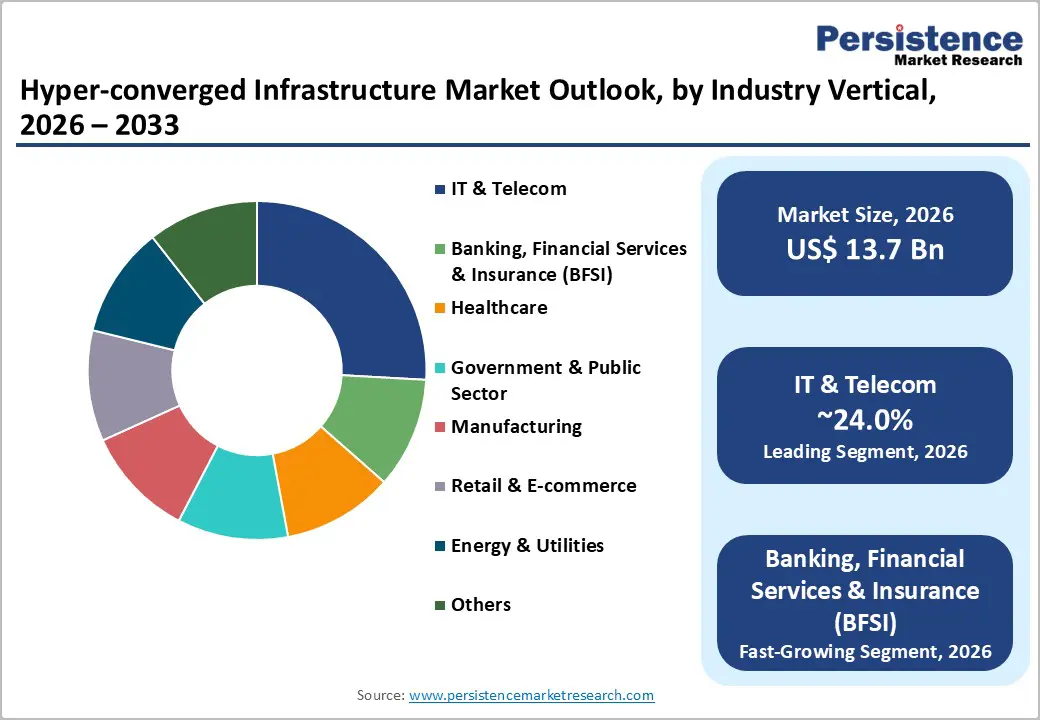

The IT & Telecommunications segment is expected to account for approximately 24.0% of the Global Hyper-converged Infrastructure Market by Use Industry in 2026.

The market is expected to witness a CAGR of 21.1% from 2026 to 2033.

The Hyper-converged Infrastructure Market is driven by enterprise infrastructure consolidation for operational efficiency and cost reduction, coupled with evolving regulatory compliance and data security requirements.

Key market opportunities in the Hyper-converged Infrastructure Market lie in edge computing deployments for low-latency, distributed processing and BFSI digital transformation requiring real-time, scalable, and secure infrastructure.

Key players in the Hyper-converged Infrastructure market include Dell Technologies, Nutanix, VMware, Hewlett Packard Enterprise (HPE), Cisco Systems, and NetApp.