- Industrial Goods & Service

- Hollow Metal Doors Market

Hollow Metal Doors Market Size, Share, and Growth Forecast, 2025 - 2032

Hollow Metal Doors Market By Material Type (Cold-Rolled Steel, Galvanized Steel, Others), Product Type (Flush, Paneled, Others), End-user, and Regional Analysis for 2025 - 2032

Hollow Metal Doors Market Size and Trends Analysis

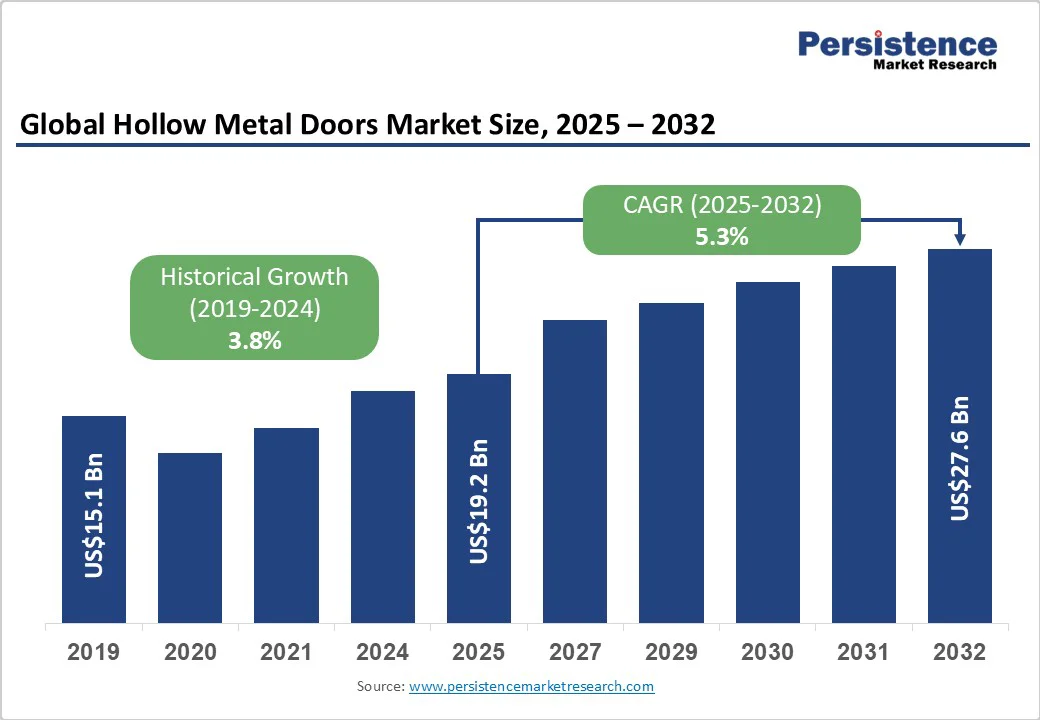

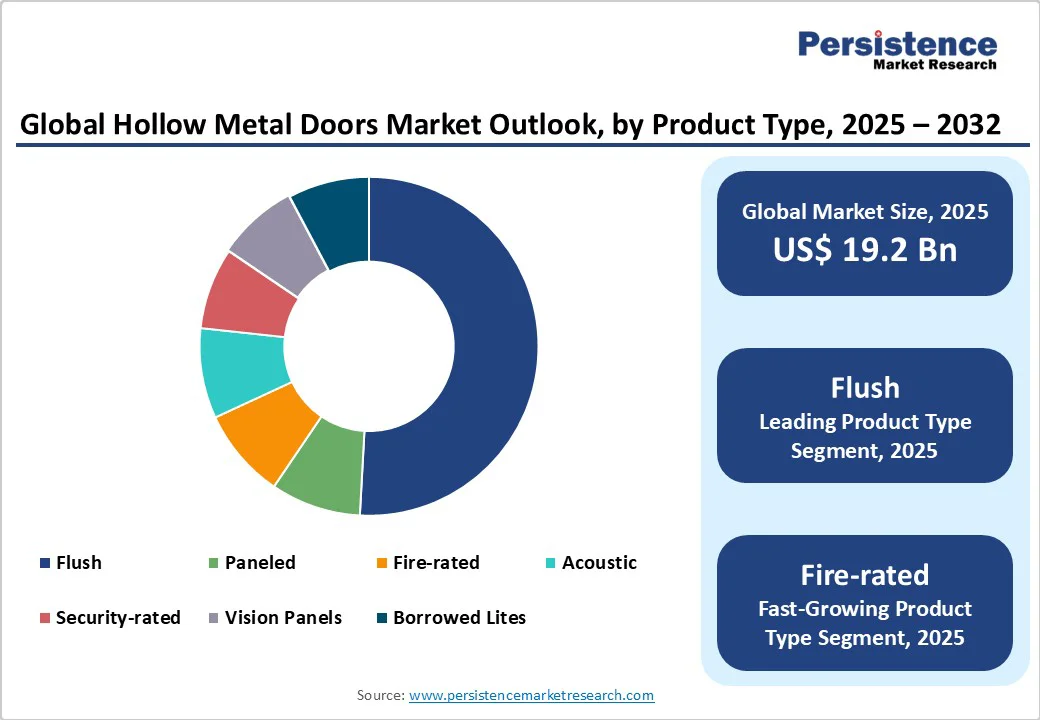

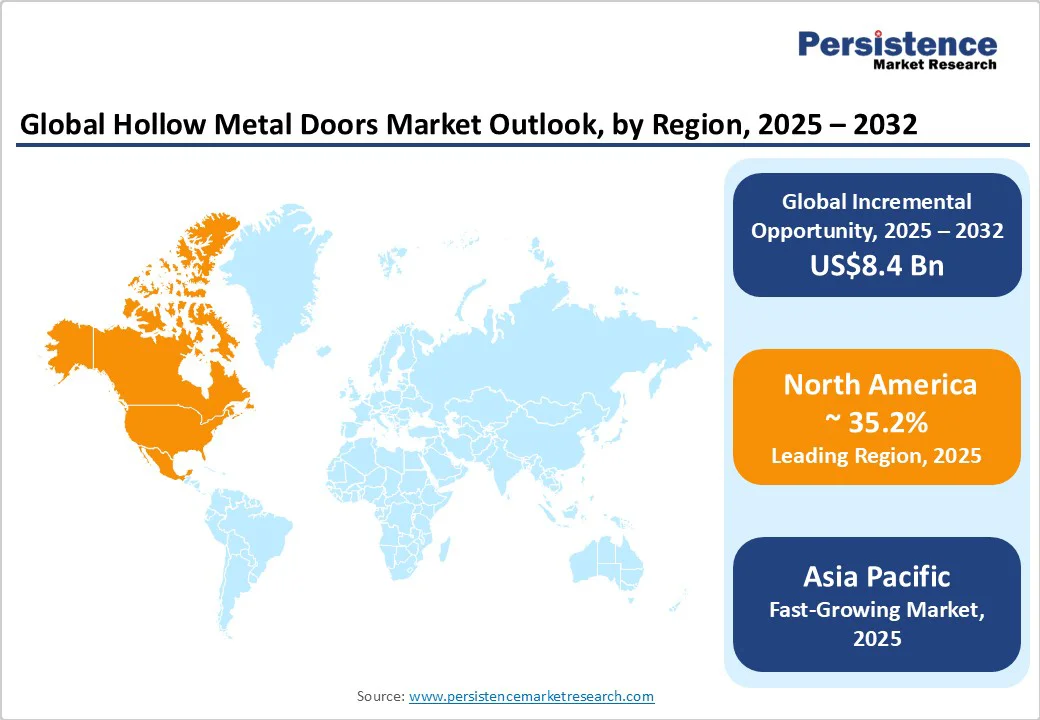

The global hollow metal doors market size is likely to be valued at about US$19.2?Billion in 2025 and is expected to reach around US$27.6 Billion by 2032, growing at a CAGR of approximately 5.3% during the forecast period from 2025 to 2032, driven by sustained commercial construction, regulatory enforcement of fire-rated standards, and modernization of institutional buildings.

The growing replacement cycle for older infrastructure, combined with higher demand for tested and certified fire, acoustic, and security doors, reinforces growth momentum. Emerging manufacturing hubs across Asia and a rising focus on energy-efficient, durable, and standardized door systems further strengthen global market prospects.

Key Industry Highlights

- Leading Region: North America holds 35.2% of the global market share, driven by extensive institutional infrastructure, strict building codes, and frequent renovation cycles.

- Fastest-Growing Region: Asia Pacific, supported by rapid urbanization, industrial investment, and large-scale commercial construction in China, India, and Southeast Asia.

- Investment Plans: Major players such as ASSA ABLOY, Allegion, and CECO are expanding regional manufacturing facilities, modernizing production lines, and investing in automation and smart-access integration to improve delivery and compliance.

- Dominant Material Type: Cold-rolled steel holding 54.7% market share, widely used in commercial and institutional buildings due to strength, fire resistance, and cost efficiency.

- Leading Product Type: Flush hollow metal doors with 58.9% market share, are preferred for versatility, durability, and suitability across offices, educational institutions, and industrial complexes.

| Key Insights | Details |

|---|---|

|

Hollow Metal Doors Market Size (2025E) |

US$19.2 Bn |

|

Market Value Forecast (2032F) |

US$27.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Growth in Construction and Retrofit Activities

Commercial, institutional, and industrial construction is a critical demand driver for hollow metal doors. Rising investments in educational institutions, healthcare facilities, and commercial spaces are expanding the total installed base. Globally, consistent construction expenditure and renovation cycles have sustained a 5-6% annual demand increase for hollow metal doors. Retrofit and code-upgrade programs, particularly in North America and Europe, add recurring replacement opportunities. Public infrastructure modernization and safety compliance measures are expected to contribute significantly to market volume over the next decade.

Enforcement of Building Safety and Fire Regulations

Stringent safety regulations and building code enforcement are increasing the adoption of fire-rated and tested hollow metal door assemblies. National and regional codes now mandate certified fire resistance, acoustic performance, and durability standards. This shift from low-cost substitutes to compliant metal systems has accelerated value growth across both developed and developing regions. In high-occupancy buildings such as hospitals and educational institutions, regulations now specify certified metal assemblies, creating new revenue channels for manufacturers specializing in tested products. The focus on occupant safety and code compliance directly influences procurement priorities for contractors and builders.

Technological Advancements and Manufacturing Automation

Automated production, computer-controlled metal forming, and modular assembly have transformed cost structures within the hollow metal door industry. Manufacturers are increasingly investing in modern fabrication lines to improve throughput, consistency, and customization capability. This technological advancement enables shorter lead times and better quality assurance. The integration of digital tools for design, fabrication, and inventory management also enhances responsiveness to project-specific requirements. Automation not only improves profit margins but also increases scalability in emerging markets where demand for high-volume, low-cost standardized systems is rising.

Barrier Analysis - Raw Material Price Volatility

Steel prices remain one of the most significant cost variables affecting manufacturers. Fluctuations in galvanized and cold-rolled steel prices directly influence production costs and contract profitability. In periods of high steel prices, project bids are often delayed or renegotiated, leading to supply disruptions. This volatility creates uncertainty in procurement planning for both manufacturers and contractors. The cyclical nature of raw material pricing adds risk to long-term contracts, especially in large infrastructure or institutional projects with fixed budgets.

Fragmented Supply and Installation Networks

The market’s downstream layer, comprising regional distributors, local fabricators, and independent installers, is highly fragmented. Inconsistent quality control, varying certification levels, and unequal access to testing infrastructure lead to inefficiencies. Manufacturers are compelled to invest in training, certification, and dealer management to maintain consistent product performance across geographies. This structural fragmentation increases operational costs and limits the scalability of smaller players, reinforcing competitive barriers for new entrants.

Opportunity Analysis - Expansion of Premium Fire-Rated and Acoustic Door Lines

There is a growing shift toward performance-rated doors that meet specific fire, sound, and security standards. These premium doors command higher prices and deliver greater value per installation. With global building safety codes evolving, manufacturers that expand certified product portfolios stand to capture a significant share from mid-market competitors. The premiumization trend offers opportunities worth several billion dollars globally, supported by rising retrofitting budgets and public building safety audits.

Localized Manufacturing and Emerging Market Growth

Rapid urbanization across Asia Pacific, the Middle East, and Africa presents an opportunity for localized manufacturing hubs. Establishing regional assembly and finishing facilities reduces logistics costs and ensures compliance with local building codes. Countries such as India, Indonesia, and Vietnam are experiencing accelerated institutional and industrial construction, driving substantial demand for affordable yet standardized hollow metal door systems. Localized manufacturing not only improves cost competitiveness but also enables quicker delivery and customization for regional market needs.

Integration with Smart Access and Security Systems

The rising adoption of smart building technologies presents new integration possibilities for hollow metal doors. Incorporating access control sensors, electronic locks, and IoT-enabled monitoring solutions enhances security and functionality. Manufacturers that form partnerships with electronic access control companies can differentiate themselves in premium construction projects. This convergence of traditional hardware and smart technologies is expected to redefine product value propositions and expand the long-term addressable market.

Category-wise Analysis

Material Type Insights

Cold-rolled steel is the most widely used material in hollow metal doors, accounting for 54.7% of the market share due to its strength, fire resistance, and cost efficiency. It is extensively deployed in commercial office complexes, educational institutions, and government facilities where building codes demand durable, fire-rated doors. For example, universities in the U.S. often mandate cold-rolled steel doors for high-occupancy areas to meet NFPA 80 fire door standards. Its affordability and proven performance make it the material of choice for large-scale construction and retrofit projects worldwide.

Stainless steel and specialty alloys are experiencing rapid growth, particularly in coastal regions and high-humidity environments. Demand is driven by healthcare facilities, pharmaceutical plants, and cleanrooms, where hygiene, corrosion resistance, and aesthetic appeal are critical. For instance, hospitals in Singapore and luxury hotels in Dubai increasingly specify stainless steel doors for operating theaters and high-end suites due to their durability and sleek design. Specialty alloys also find applications in premium architectural projects that require both visual elegance and superior performance. The CAGR of stainless steel doors surpasses standard cold-rolled steel, reflecting growing adoption in niche and high-value projects.

Product Type Insights

Flush hollow metal doors dominate the market due to their smooth surfaces, versatility, and sturdy construction, with a market share of 58.9%. They are widely installed in office buildings, schools, industrial complexes, and residential high-rises. For example, commercial office towers in New York and Chicago frequently use flush hollow metal doors for interior corridors, providing cost-effective fire and security protection. Their balance of strength, affordability, and low maintenance ensures steady adoption in both new construction and retrofit projects, maintaining a stable market share globally.

Fire-rated hollow metal doors are the fastest-growing product segment, propelled by stricter building safety codes and increased awareness of fire protection standards. They are increasingly specified in hospitals, airports, and high-rise residential complexes to prevent fire propagation and protect occupants. For instance, hospitals in Germany and airports in the Middle East mandate fire-rated doors in corridors, stairwells, and mechanical rooms. Rising retrofitting budgets for older infrastructure and new construction compliance requirements are driving consistent growth in this high-margin category.

End-user Insights

Commercial and institutional buildings represent the largest end-use segment, accounting for approximately 64.2% of the market share. Office complexes, government buildings, educational institutions, and hospitals form the primary demand base. For example, U.S. school districts and municipal offices frequently purchase hollow metal doors as part of long-term safety compliance programs, benefiting from standardized procurement frameworks and recurring service contracts. Regulatory oversight and fire-safety mandates in this sector ensure continued stable demand and significant market revenue.

Industrial and specialized facilities are the fastest-growing end-use segment, driven by the expansion of logistics centers, manufacturing plants, and data centers. These facilities require heavy-duty hollow metal doors capable of withstanding high impact, providing fire protection, and ensuring operational security. For example, e-commerce warehouses in China and large-scale semiconductor fabs in South Korea increasingly adopt high-performance hollow metal doors to secure sensitive areas and support operational safety standards. The rapid growth of industrial infrastructure and specialized facilities in emerging markets is fueling above-average adoption rates in this segment.

Regional Insights

North America Hollow Metal Doors Market Trends - Compliance-Driven Demand and Integrated Manufacturing

North America is the largest and high-value market for hollow metal doors, holding a market share of 35.2%, with the U.S. accounting for the majority of demand. The market is driven by extensive institutional infrastructure, frequent renovation cycles, and stringent fire and safety regulations, particularly those governed by the National Fire Protection Association (NFPA) and local building authorities. Compliance requirements have created a steady demand for certified and tested hollow metal door assemblies, especially in educational institutions, hospitals, and government facilities. Major players such as ASSA ABLOY, Allegion, and CECO maintain extensive distributor and installer networks, offering integrated solutions that combine doors, frames, and hardware.

Technological innovation, including factory automation, modular manufacturing, and integrated access systems, has enabled manufacturers to differentiate products while reducing lead times. Recent developments include Allegion’s 2024 acquisition of Krieger Specialty Products, which enhanced its offerings in fire-rated and sound-rated doors for high-performance applications, and CECO’s modernization of production facilities to support faster delivery and customization. Investments in public building modernization and compliance-driven retrofitting continue to strengthen market growth, while demand for premium, code-compliant products drives revenue expansion.

Europe Hollow Metal Doors Market Trend-Regulatory-Driven Growth with Focus on Sustainability and Performance

Europe’s hollow metal door market is shaped by strict fire safety, acoustic performance regulations, and environmental compliance standards. Germany, the U.K., and France are among the leading markets, supported by both industrial expansion and extensive refurbishment programs. Post-2022 fire safety reviews in the U.K., triggered by building code audits, have significantly increased demand for tested and certified metal door assemblies in commercial and public facilities. Harmonization of construction product standards, including EN and CE certifications, has facilitated cross-border trade for standardized door systems, though high certification costs and complex approval procedures remain barriers for smaller manufacturers.

Key players in the region focus on premium design, energy efficiency, sustainability, and lifecycle performance, catering to evolving green building standards. The adoption of digital manufacturing and automation in door fabrication has enhanced production efficiency, quality consistency, and competitiveness. Recent initiatives include ASSA ABLOY’s expansion of its European production lines with automated assembly technology and Allegion’s launch of modular acoustic and fire-rated door solutions tailored for retrofitting historic buildings, demonstrating the growing focus on performance-oriented and sustainable solutions across the continent.

Asia Pacific Hollow Metal Doors Market Trends - Urbanization-Fueled Expansion and Localization of Production

Asia Pacific is the fastest-growing regional market for hollow metal doors, driven by rapid urbanization, industrial investment, and large-scale commercial construction. China and India dominate regional installations due to booming institutional, industrial, and residential projects. Japan and South Korea maintain strong demand for high-spec, technologically advanced hollow metal doors used in precision facilities, high-rise commercial buildings, and research centers. The region benefits from abundant steel supply, lower labor costs, and expanding localized manufacturing hubs, particularly in Southeast Asia, which reduce logistics costs and allow faster project delivery.

Regulatory frameworks across countries are gradually aligning with international fire and safety standards, enhancing the adoption of certified door systems. Infrastructure mega-projects, such as smart city developments in India and port logistics expansions in Vietnam, are further propelling demand. Recent developments include CECO’s establishment of a manufacturing facility in India to support regional demand for fire-rated and security doors, and ASSA ABLOY’s deployment of modular production lines in China to accelerate delivery of customized solutions for industrial and commercial projects. These trends position Asia Pacific as a high-growth market with increasing opportunities for both standard and premium hollow metal door offerings.

Competitive Landscape

The global hollow metal doors market is moderately consolidated, with a mix of multinational corporations and regional fabricators. Leading manufacturers hold significant market share through brand reputation, distribution reach, and certification capabilities. Major players such as ASSA ABLOY, Allegion, and CECO dominate institutional and commercial projects, while smaller regional companies focus on customized or niche solutions. Competitive advantage is increasingly determined by testing certifications, lead-time reliability, and integrated hardware compatibility.

Leading companies focus on vertical integration, combining door, frame, and hardware production under one umbrella. Strategic priorities include code compliance, smart technology integration, and cost optimization through digital manufacturing. Partnerships, acquisitions, and local assembly ventures remain key to expanding geographic presence and shortening lead times in emerging markets.

Key Industry Highlights

- In December 2024, ASSA ABLOY acquired Premier Steel Doors and Frames, expanding its U.S. manufacturing capacity and enhancing its fire-rated hollow metal door portfolio to improve supply-chain resilience and distribution efficiency.

- In March 2025, Masonite International launched a new line of fire-rated and acoustic doors in North America, targeting retrofitting projects and high-occupancy commercial buildings with advanced compliance and safety certifications.

Companies Covered in Hollow Metal Doors Market

- ASSA ABLOY

- Allegion

- CECO Door

- Masonite International

- JELD-WEN

- Hörmann Group

- Corflex

- Steelcraft

- Ceco Door Products

- Northwest Door

- Metl-Span

- Doorguard Industries

- AMICO

- International Door Corporation

- Graham Architectural Products

- Pemko Manufacturing

- Overly Door Company

- DORMAKABA

- Nabco Entrances

- Pella Corporation

Frequently Asked Questions

The hollow metal doors market size in 2025 is estimated at US$19.2 Billion.

The hollow metal doors market is projected to reach approximately US$27.6 Billion by 2032.

Key trends include the rising adoption of fire-rated and acoustic doors, integration with smart access and security systems, growth of localized manufacturing in emerging markets, and increasing focus on energy-efficient, durable, and code-compliant door systems.

By material type, cold-rolled steel doors hold the largest market share. By product type, flush hollow metal doors dominate, and by end-use sector, commercial and institutional buildings remain the largest segment.

The hollow metal doors market is expected to grow at a CAGR of 5.3% between 2025 and 2032.

Major players in the hollow metal doors market include ASSA ABLOY, Allegion, CECO Door, Masonite International, and JELD-WEN.