- Metals & Minerals

- Hastelloy Market

Hastelloy Market Size, Share, and Growth Forecast, 2026 - 2033

Hastelloy Market by Product Type (Hastelloy C-276, Hastelloy C-22, Hastelloy C-2000, Hastelloy C-4, Hastelloy B-2, Hastelloy B-3, Hastelloy G-30), End-user (Chemical Processing, Oil & Gas, Aerospace & Defense, Others), and Regional Analysis for 2026 – 2033

Hastelloy Market Size and Trends Analysis

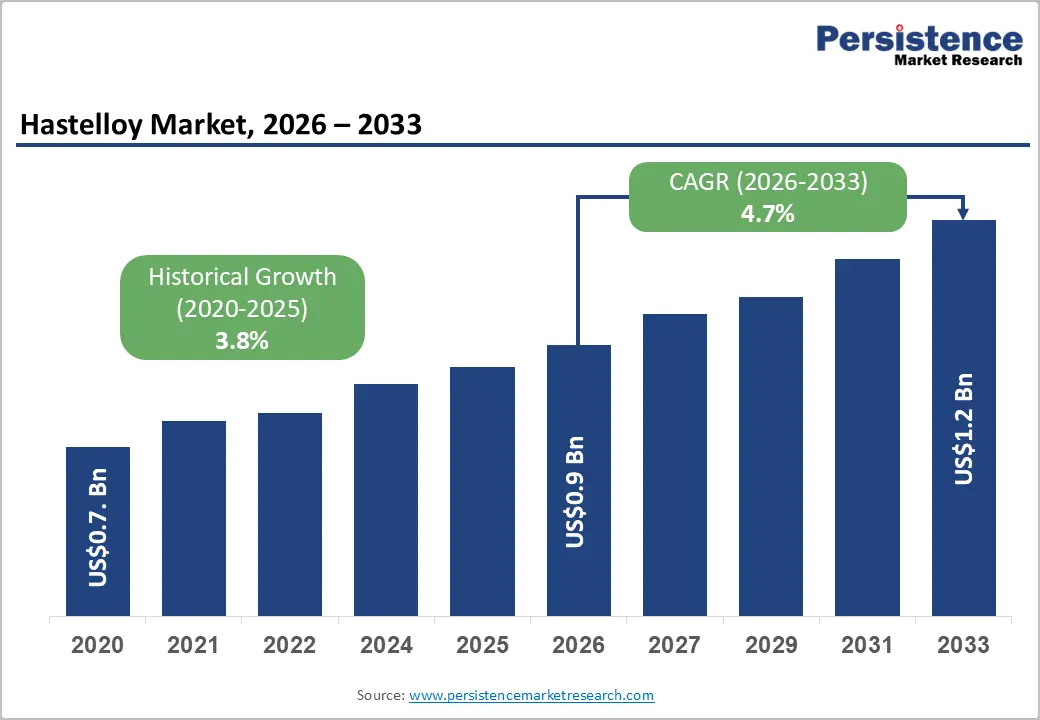

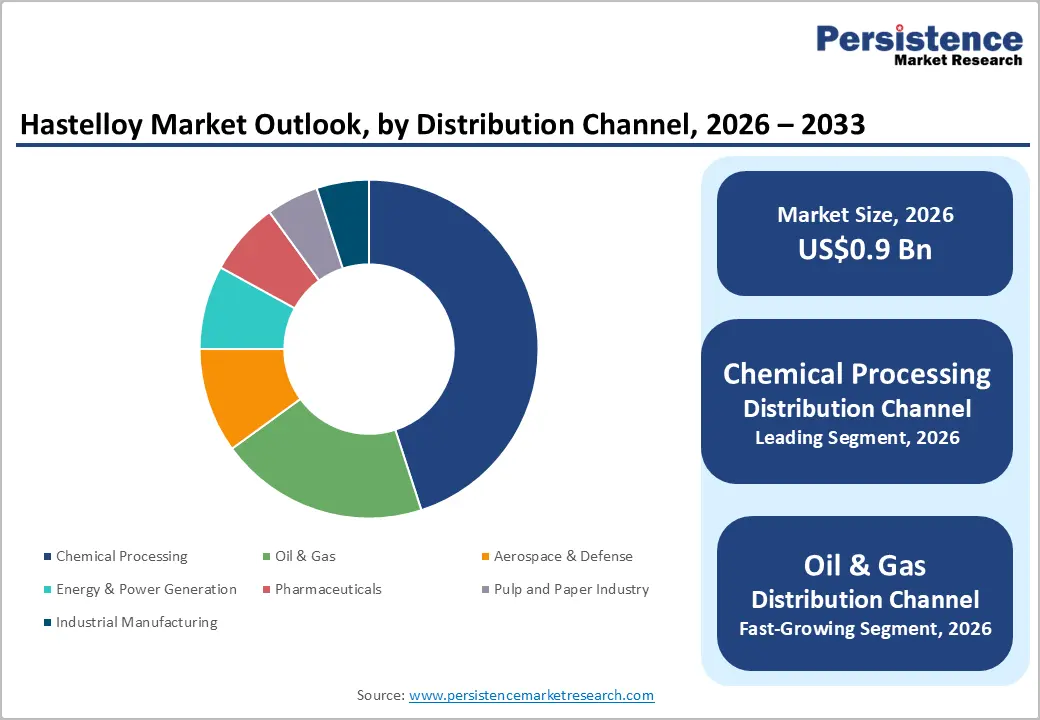

The global hastelloy market size is likely to be valued at US$0.9 billion in 2026, and is expected to reach US$1.2 billion by 2033, growing at a CAGR of 4.7% during the forecast period from 2026 to 2033, driven by the increasing prevalence of demand for high-performance corrosion-resistant alloys in aggressive chemical environments, rising investments in oil & gas exploration, and growing adoption in aerospace & defense for extreme temperature and pressure applications.

Growing demand for Hastelloy C-276 and Hastelloy C-22, especially in chemical processing and oil & gas industries, is accelerating adoption across manufacturers. Increasing recognition of Hastelloy as critical for equipment durability, reduced maintenance, and operational safety in emerging chemical, energy, and pharmaceutical markets remains a major driver of market growth.

Key Industry Highlights:

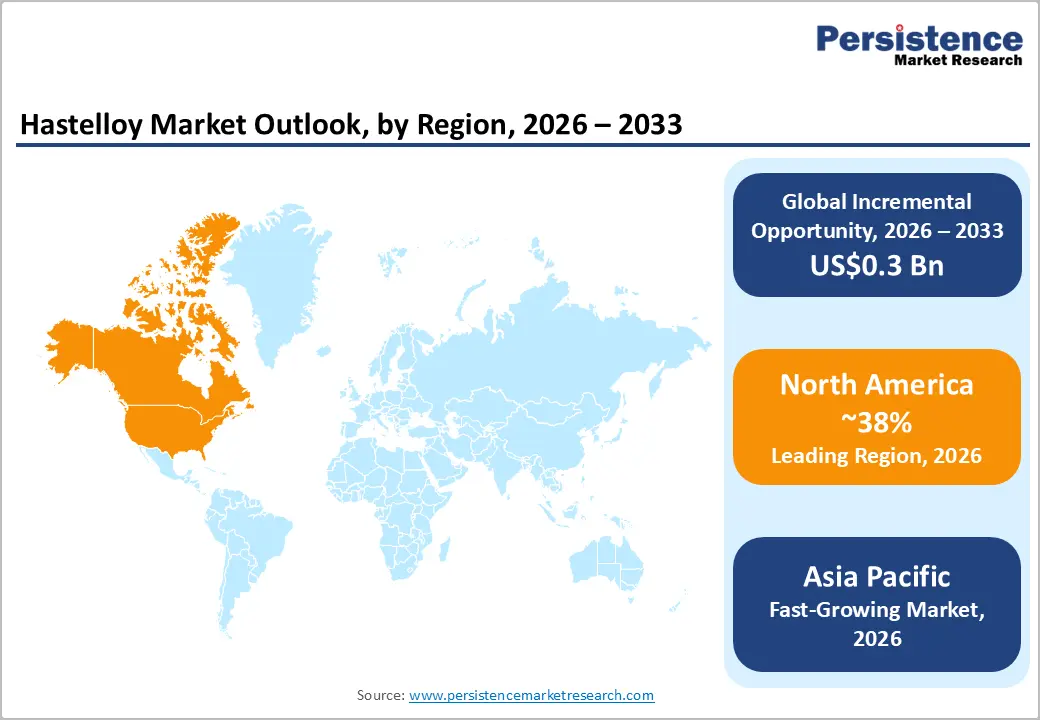

- Leading Region: North America, anticipated to account for a 38% market share in 2026, driven by advanced chemical processing, strong oil & gas sector, and premium demand in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rapid industrialization, expanding chemical manufacturing, and growing energy infrastructure in China and India.

- Dominant Product Type: Hastelloy C-276, to hold approximately 42% of the market share, as it remains the most versatile corrosion-resistant grade.

- Leading End-user: Chemical processing, contributing nearly 45% of the market revenue, due to the highest volume usage in harsh environments.

| Key Insights | Details |

|---|---|

|

Hastelloy Market Size (2026E) |

US$0.9 Bn |

|

Market Value Forecast (2033F) |

US$1.2 Bn |

|

Projected Growth CAGR (2026-2033) |

4.7% |

|

Historical Market Growth (2020-2025) |

3.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Developing Chemical Processing and Oil & Gas Sectors

Global demand for corrosion-resistant alloys such as Hastelloy is strongly influenced by growth in the chemical processing and oil & gas industries. U.S. government energy infrastructure data indicates that the U.S. hosts more than 9,500 chemical plants and over 2,000 oil and gas processing facilities. These facilities require highly durable materials for pumps, pipelines, reactors, and heat exchangers that can withstand corrosive substances as well as high-pressure and temperature conditions. Ongoing expansion in these industries, supported by developments in natural gas pipelines and refinery capacity to meet domestic and export energy demand, highlights sustained investment in processing infrastructure.

Hastelloy, with its high nickel-molybdenum-chromium composition, provides strong resistance to sulfuric and hydrochloric acids and to chloride stress corrosion cracking. Owing to these properties, industries that handle aggressive chemicals increasingly specify Hastelloy for critical components where reliability and failure prevention are essential. In the oil and gas sector, continued refining and midstream infrastructure development tracked through refinery capacity and throughput data from the U.S. Energy Information Administration further supports demand for advanced alloys. Sour service environments containing sulfur compounds can quickly degrade conventional steels, making high-performance alloys more suitable.

Increasing Aerospace & Defense Applications

Expansion in aerospace and defense applications is a major factor driving demand for Hastelloy, as advanced materials are essential for high-performance aircraft and defense systems. Nickel-based alloys, including certain Hastelloy grades such as Hastelloy X and C-276, are commonly used in high-temperature components such as jet engine combustion chambers, turbine parts, exhaust systems, and structural hardware that must endure extreme heat and corrosive operating environments typical in aerospace applications. Technical sources, including NASA, emphasize the long-established role of nickel-based superalloys of which Hastelloy is a part in gas turbine engines and aerospace propulsion systems, where they provide excellent stability at elevated temperatures along with strong resistance to oxidation, both critical for reliable and efficient flight.

The aerospace industry also enforces strict material standards, such as NASA-STD-6016B, which require materials used in spacecraft and aircraft hardware to meet rigorous reliability and durability criteria under extreme conditions. In defense applications, superalloys are equally important for use in military aircraft engines, missile systems, and other platforms where high strength and thermal resistance directly influence operational performance. Hastelloy’s capability to maintain mechanical integrity under extreme temperatures and corrosive environments makes it well-suited for critical defense components, including propulsion and exhaust systems that undergo rapid temperature fluctuations and severe corrosive stresses.

Barrier Analysis – Complex Fabrication and Welding Requirements

Complex fabrication and welding requirements act as a restraint for the Hastelloy market due to the technical precision and specialized capabilities needed to process these nickel-based alloys. Hastelloy grades exhibit high strength and strong work-hardening behavior, which increases tool wear, machining time, and energy consumption during cutting, forming, and shaping operations. Fabrication often requires controlled environments, strict temperature management, and tailored forming techniques to avoid distortion or microstructural damage, raising production complexity for manufacturers and fabricators.

Welding Hastelloy demands skilled operators, qualified procedures, and advanced processes such as gas tungsten arc welding with controlled heat input to prevent hot cracking, porosity, and loss of corrosion resistance in the heat-affected zone. Post-weld cleaning and inspection are critical to maintain performance in aggressive chemical and high-temperature service.

Long Lead Times and Supply Chain Complexity

Long lead times and supply chain complexity restrain the Hastelloy market by creating procurement risk, project delays, and higher working capital requirements for end users. Hastelloy production relies on multi-stage melting, alloying, hot working, and precision finishing processes that require tightly controlled conditions and specialized equipment. Capacity is concentrated among a limited number of qualified producers and processors, which narrows sourcing options and extends delivery timelines for plates, pipes, forgings, and custom components.

Supply chains span multiple regions for critical inputs such as nickel, molybdenum, and chromium, adding exposure to logistics disruptions, export controls, and shipping constraints. Custom specifications for thickness, tolerances, and certifications further lengthen manufacturing cycles and inspection timelines. These factors complicate project planning for chemical processing, oil & gas, and aerospace users, forcing buffer inventories or schedule flexibility, which raises total ownership cost and discourages time-critical deployments of Hastelloy components.

Opportunity Analysis – Innovations in Hastelloy C-22 and C-2000 for Aggressive Environments

Growth in advanced grades such as Hastelloy C-22 and C-2000 presents a strong opportunity for the Hastelloy market by meeting increasingly demanding requirements in aggressive chemical and high-stress environments. Hastelloy C-22 exhibits very high resistance to pitting, crevice corrosion, and stress-corrosion cracking, significantly outperforming many conventional alloys in tests involving chloride-rich and oxidizing chemical exposures. In chloride-induced corrosion testing, C-22 showed critical pitting temperatures above 302°F and critical crevice temperatures above 150°F, demonstrating superior durability in environments that would rapidly degrade common stainless steels.

Hastelloy C-2000 broadens this performance envelope with even better resistance against both oxidizing and reducing chemicals, aided by its copper-enriched alloy chemistry that enhances sulfuric acid resistance across a wide temperature range. C-2000 maintains excellent resistance to chloride-induced pitting and crevice attack with critical thresholds near 293°F for pitting and 176°F for crevice corrosion, matching or exceeding many competing superalloys in rigorous ASTM corrosion tests.

Expansion of LNG, Hydrogen, and Sour Gas Infrastructure

Expansion of LNG, hydrogen, and sour gas infrastructure represents a strong opportunity for the Hastelloy market as these systems operate under severe corrosion, pressure, and temperature conditions that challenge conventional alloys. LNG value chains rely on cryogenic pipelines, heat exchangers, valves, and compressors that face thermal cycling and exposure to corrosive contaminants, while hydrogen processing and transport introduce risks such as hydrogen embrittlement and accelerated corrosion in standard steels. Hastelloy’s nickel-based chemistry offers high resistance to chloride attack, sulfide stress cracking, and localized corrosion, supporting long service life in liquefaction, regasification, and gas treatment units where reliability directly affects uptime and safety performance.

Sour gas facilities contain hydrogen sulfide and acidic compounds that rapidly degrade carbon steel and many stainless steels, increasing leak and failure risks. Hastelloy grades maintain mechanical integrity and corrosion resistance in high-H?S environments, supporting acid gas removal units, amine systems, and sulfur recovery processes. Large-scale build-out of LNG terminals, hydrogen production and distribution assets, and sour gas processing plants raises demand for premium alloys in critical components such as reactors, piping, heat exchangers, and pressure vessels, where failure consequences are high and lifecycle cost efficiency favors durable materials.

Category-wise Analysis

Product Type Insights

Hastelloy C-276 is anticipated to dominate the market, accounting for 42% of the market share in 2026. Its dominance is driven by its broad corrosion resistance and proven performance across multiple high-risk industrial environments. The alloy performs reliably in both oxidizing and reducing media, making it suitable for chemical reactors, heat exchangers, flue gas desulfurization units, and sour gas processing equipment. Its resistance to pitting, crevice corrosion, and stress corrosion cracking supports long service life under fluctuating process conditions. Flue gas desulfurization (FGD) piping and scrubber components are often fabricated from Hastelloy C-276 due to its exceptional resistance to sulfuric acid and chloride attack encountered in desulfurization environments.

Hastelloy C-22 represents the fastest-growing product type, fueled by rising deployment in highly aggressive chemical and pollution control environments that demand superior corrosion resistance. The alloy offers exceptional protection against pitting, crevice corrosion, and stress corrosion cracking across mixed oxidizing and reducing media, which expands its suitability for multipurpose chemical reactors, scrubbers, heat exchangers, and acid handling systems. Its high chromium and molybdenum content supports durability under fluctuating process conditions, reducing unplanned downtime and maintenance cycles. Haynes International, Inc. in flue gas desulfurization (FGD) scrubbers and hazardous waste treatment systems where extreme corrosion resistance is required. Field evaluations cited by the company show Hastelloy C-22 components outperforming 316 stainless steel by at least 6× in corrosion resistance tests under acidic off-gas conditions in industrial incinerators, indicating significantly extended service life and reliability in aggressive environments.

End-user Insights

Chemical processing is expected to dominate the market, contributing nearly 45% of revenue in 2026, propelled by the sector’s constant exposure to highly corrosive acids, chlorides, and mixed chemical streams that degrade conventional metals. Equipment such as reactors, heat exchangers, columns, valves, and piping must operate under fluctuating temperatures and pressures while maintaining purity and safety standards. Hastelloy’s resistance to pitting, crevice corrosion, and stress corrosion cracking supports long service life in sulfuric acid, hydrochloric acid, and chloride-rich media. The sector’s constant exposure to highly corrosive acids, chlorides, and mixed chemical streams that degrade conventional metals. Equipment such as reactors, heat exchangers, columns, valves, and piping must operate under fluctuating temperatures and pressures while maintaining purity and safety standards. Hastelloy’s resistance to pitting, crevice corrosion, and stress corrosion cracking supports long service life in sulfuric acid, hydrochloric acid, and chloride-rich media.

Oil & gas represents the fastest-growing end-user, supported by harsher operating conditions in new field developments and processing assets. Projects increasingly target sour gas reservoirs, high-pressure high-temperature wells, and offshore environments where hydrogen sulfide, chlorides, and acidic condensates accelerate corrosion of conventional alloys. Hastelloy grades deliver strong resistance to pitting, crevice corrosion, and sulfide stress cracking, which supports reliability in separators, heat exchangers, valves, and piping. Midstream and downstream assets also face mixed chemical streams and temperature cycling that drive material upgrades. Saudi Arabian Oil Co. (Saudi Aramco), which has implemented Hastelloy C-276 in critical safety and high-pressure, high-temperature (HPHT) oilfield equipment. Aramco uses C-276 alloy components in wellhead systems, safety valves, and downhole tools where chlorides and hydrogen sulfide can cause severe corrosion and sulfide stress cracking in conventional materials.

Regional Insights

North America Hastelloy Market Trends

North America is projected to dominate, accounting for nearly 38% of the share in 2026, supported by strong demand from the region’s advanced industrial base. The U.S. and Canada host many chemical processing plants, oil & gas refineries, and petrochemical facilities, all of which require highly corrosion-resistant alloys for equipment exposed to aggressive chemicals and high-temperature environments. Hastelloy is widely used in reactors, heat exchangers, pipelines, and pressure vessels where conventional stainless steels may fail due to corrosion or stress cracking.

The region also benefits from a well-established aerospace and defense industry, where high-performance nickel-based alloys are required for jet engine components, exhaust systems, and turbine hardware operating under extreme heat and pressure. North America continues to invest heavily in energy infrastructure, including natural gas processing, LNG export terminals, and refinery upgrades. These projects increase the need for durable materials capable of withstanding sour gas environments and corrosive process fluids.

Europe Hastelloy Market Trends

Europe is stimulated by strong demand from chemical processing, energy, aerospace, and environmental technology sectors. The region has a well-established chemical industry, particularly in countries such as Germany, France, and Italy, where manufacturers require corrosion-resistant alloys for reactors, heat exchangers, valves, and piping systems that operate in aggressive chemical environments. Hastelloy is widely selected in these applications due to its strong resistance to acids, chlorides, and high-temperature corrosion.

The growing focus on clean energy and industrial decarbonization across the region also supports demand for advanced nickel-based alloys. Europe’s expansion of hydrogen production facilities, waste-to-energy plants, and carbon-capture infrastructure requires materials capable of withstanding high temperatures and corrosive gases, making Hastelloy suitable for critical components in these systems. Europe’s aerospace sector further supports the market, with major aircraft manufacturing and engine production activities in the region. High-performance alloys such as Hastelloy are used in engine exhaust systems and high-temperature components where durability and oxidation resistance are essential.

Asia Pacific Hastelloy Market Trends

Asia Pacific is likely to be the fastest-growing market for hastelloy in 2026, supported by rapid industrialization, expanding chemical manufacturing, and increasing investments in energy infrastructure across the region. Countries such as China, India, Japan, and South Korea are significantly expanding their chemical processing, petrochemical, and refining capacities, which require corrosion-resistant materials for reactors, pipelines, heat exchangers, and pressure vessels. Hastelloy alloys are widely preferred in these applications owing to their ability to withstand aggressive chemicals, high temperatures, and chloride-rich environments.

Strong growth in the region’s oil & gas and LNG infrastructure is another major factor driving demand. Several countries are investing in refinery upgrades, gas processing facilities, and cross-border pipeline projects to support rising energy consumption and export capacity. These operations often involve sour gas and corrosive compounds, where advanced nickel-based alloys such as Hastelloy provide longer service life compared to conventional stainless steels. The region’s expanding aerospace, power generation, and semiconductor manufacturing industries also contribute to market growth. High-temperature components in turbine systems and advanced industrial equipment require materials with excellent oxidation and thermal resistance.

Competitive Landscape

The global Hastelloy market is characterized by competition between well-established specialty alloy manufacturers and emerging regional producers. In North America and Europe, companies such as Haynes International and Howmet Aerospace maintain leadership through robust R&D investments, extensive distribution networks, and deep industrial partnerships, enabling the development of advanced alloys such as Hastelloy C-276 and C-22. These programs emphasize enhanced corrosion resistance, longer service life, and reliability under high-temperature, high-pressure, and chemically aggressive environments, meeting stringent requirements in chemical processing, power generation, and aerospace applications.

In Asia Pacific, local manufacturers are leveraging cost-competitive solutions to increase accessibility, allowing wider adoption of Hastelloy alloys across industrial plants. The use of C-276 reduces maintenance risks and supports mass integration into critical equipment, while C-22 formulations address mixed-acid environments, enabling growth in the pharmaceutical and specialty chemical segments. Strategic partnerships, collaborations, and acquisitions are further accelerating technological advancements, expanding product portfolios, and shortening commercialization cycles, strengthening market presence globally.

Key Industry Developments:

- In August 2025, Haynes International, acquired by Acerinox and a leading developer and manufacturer of advanced high-performance alloys, announced the development of HASTELLOY® WR-66™ alloy. The company delivered the new alloy to the wear and corrosion market, continuing its tradition of innovation.

- In April 2023, Aggreko, the world’s leading provider of mobile modular power, temperature control, and energy solutions, announced the launch of two new rental heat exchanger fleets: the Large Node Heat Exchanger and the Hastelloy-C Crossflow Heat Exchanger. The company made the equipment readily available to customers in petrochemical and refinery operations, offering the industry’s largest heat exchanger and the only exchanger constructed from Hastelloy.

Companies Covered in Hastelloy Market

- Howmet Aerospace

- CRS Holdings, LLC

- Doncasters Group

- HAYNES INTERNATIONAL

- Hitachi, Ltd.

- Mattco Forge

- Nippon Yakin Kogyo Co., Ltd.

- Titanium Metals Corporation

- Chicago Metal Fabricators

Frequently Asked Questions

The global Hastelloy market is projected to reach US$0.9 billion in 2026.

Expansion in chemical manufacturing, LNG, hydrogen, aerospace, and defense applications increases demand for durable alloys that reduce maintenance downtime and ensure operational reliability.

The Hastelloy market is poised to witness a CAGR of 4.7% from 2026 to 2033.

New grades such as Hastelloy C-22, C-2000, and WR-66 open applications in highly corrosive and mixed-acid environments, including pharmaceuticals, pollution control, and hydrogen infrastructure.

Haynes International, Howmet Aerospace, CRS Holdings, LLC, Doncasters Group, and Nippon Yakin Kogyo Co., Ltd. are the key players.