- Clothing, Footwear, & Accessories

- Handbag Market

Handbag Market Size, Share, and Growth Forecast, 2026 - 2033

Handbag Market by Product Type (Tote Bag, Satchel, Others), Material (Leather, Fabric, Others), Price Range, and Regional Analysis for 2026 - 2033

Handbag Market Size and Trends Analysis

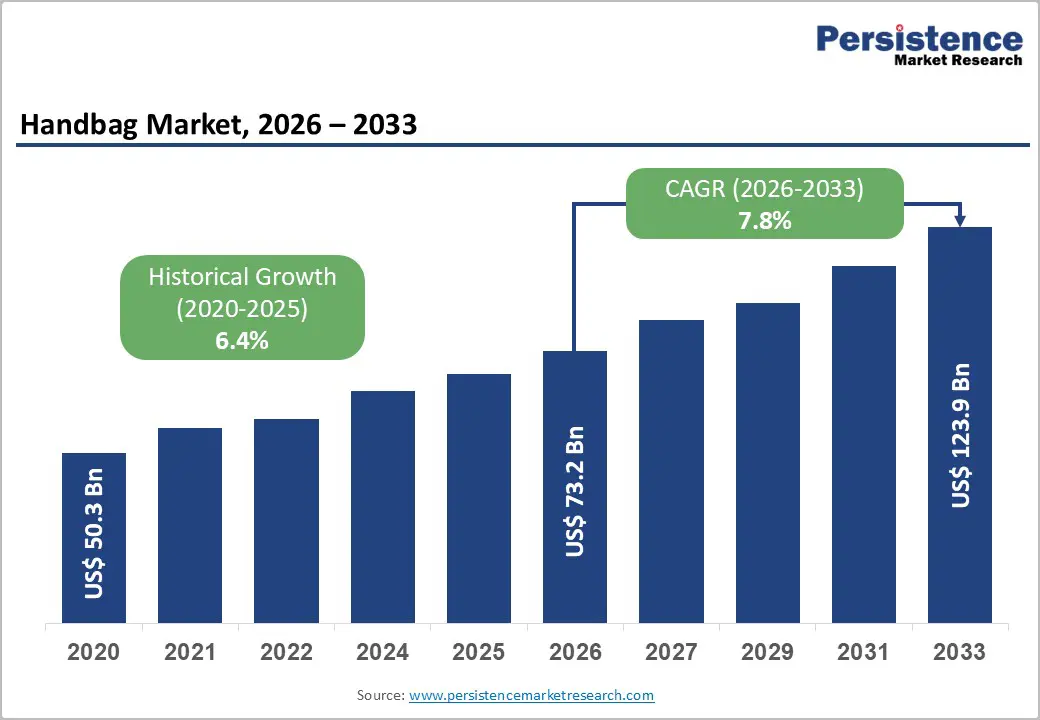

The global handbag market size is likely to be valued at US$73.2 billion in 2026 and is expected to reach US$123.9 billion by 2033, growing at a CAGR of 7.8% between 2026 and 2033, driven by premiumization trends, rising disposable incomes in emerging economies, and expanding digital commerce infrastructure. Sustainability-led material innovation and digital-first brand engagement are reshaping product portfolios and distribution economics. Companies that align assortment agility with verified sustainability credentials and integrated online-offline strategies are positioned to capture disproportionate value.

Key Industry Highlights:

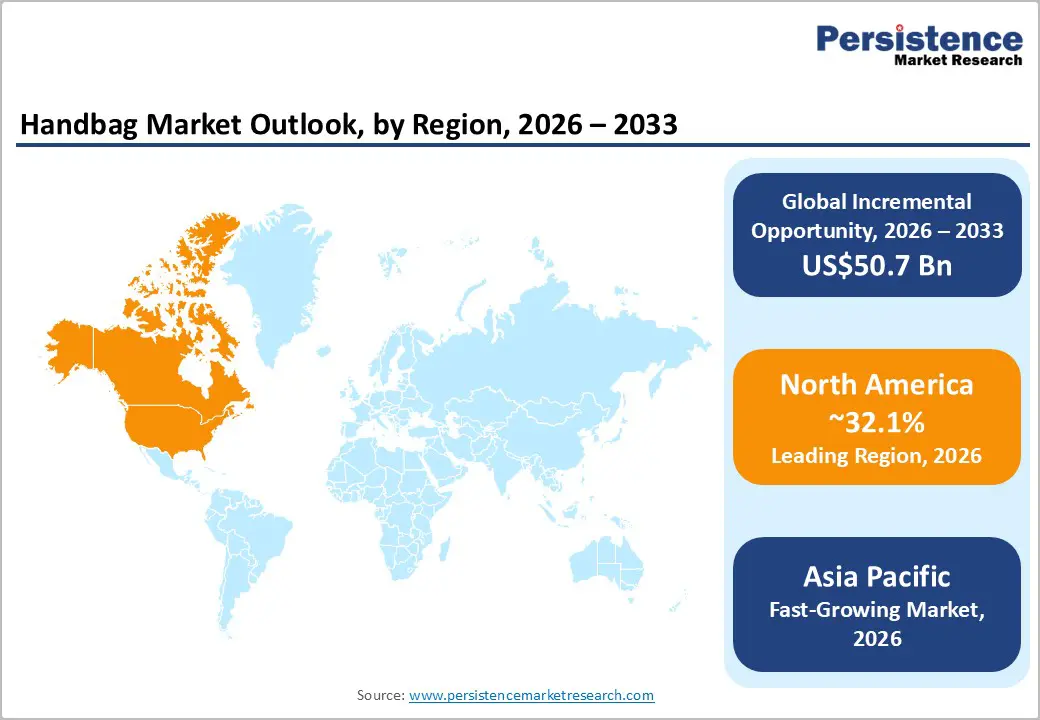

- Leading Region: North America is projected to lead the market with approximately 32.1% of market share, supported by strong disposable income levels, omnichannel retail integration, and a well-established premium and resale ecosystem.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by rising urbanization, expanding middle-class populations, and accelerating digital commerce adoption across China, Japan, and India.

- Investment Plans: Companies are prioritizing investments in nearshoring supply chains, resale authentication platforms, digital commerce infrastructure, and sustainable sourcing initiatives to strengthen margin control and regulatory compliance.

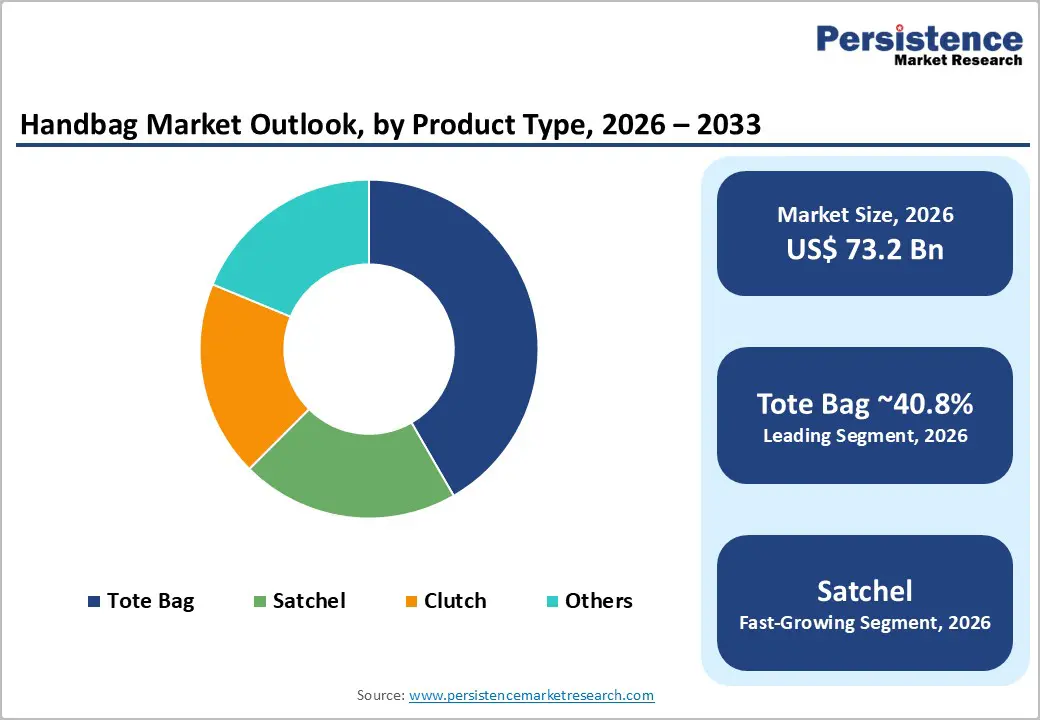

- Dominant Product Type: Tote bags are anticipated to dominate the product-type segment with 40.8% market share due to their versatility, large carrying capacity, and cross-tier appeal.

- Leading Material: Leather is estimated to remain the leading material segment with over 41.4% market share, reflecting its premium positioning, durability, and strong revenue contribution in North America and Europe.

| Key Insights | Details |

|---|---|

| Handbag Market Size (2026E) | US$73.2 Bn |

| Market Value Forecast (2033F) | US$123.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Premiumization and Willingness to Pay

Across developed markets, consumers are allocating a higher share of discretionary spending toward branded fashion accessories that combine craftsmanship, heritage, and aspirational value. Premiumization drives higher ASPs, supporting revenue expansion even in moderate volume-growth environments. Luxury and upper-premium handbags often function as “investment purchases,” with iconic designs retaining resale value and reinforcing brand equity. This dynamic reduces price sensitivity and extends product life cycles compared to mass-market alternatives. Vertically integrated players benefit from improved gross margins due to control over sourcing, production, and distribution. The broader impact is structural uplift in revenue per unit, strengthening profitability for established brands while creating barriers to entry for undifferentiated competitors.

E-commerce and Direct-to-Consumer (DTC) Distribution

Digital commerce continues to reshape the handbag ecosystem by reducing dependence on wholesale intermediaries and enabling direct consumer engagement. E-commerce platforms, brand-owned websites, and social-commerce integrations support shorter product development cycles and faster trend response. Enhanced visual merchandising, virtual try-on tools, influencer partnerships, and personalized marketing increase conversion rates and customer retention. Omnichannel consumers typically demonstrate higher lifetime value due to seamless purchasing and return experiences. Cross-border digital marketplaces further expand accessible demand, particularly between Asia Pacific and Western markets. Integrated inventory visibility, data analytics, and demand forecasting tools contribute to measurable improvements in sell-through rates and margin optimization.

Sustainability and Material Innovation

Sustainability considerations are increasingly influencing purchasing decisions, especially among younger demographics. Demand for traceable, low-impact materials, including certified leather, recycled textiles, and bio-based alternatives, has accelerated product innovation. Regulatory pressure on supply-chain transparency and environmental compliance raises costs for non-compliant manufacturers but creates premium opportunities for certified sustainable collections. Brands that demonstrate lifecycle impact reductions and responsible sourcing practices gain competitive differentiation and preferential retail placement. Investment in material science and circular design initiatives, such as repair programs and resale integration, enhances brand credibility while expanding revenue streams. Sustainability has evolved from a reputational consideration to a strategic growth lever.

Barrier Analysis - Raw Material and Manufacturing Cost Volatility

Leather, hardware components, and specialized trims remain exposed to commodity price fluctuations and currency volatility. Cost swings in leather inputs, estimated in some industry cycles at 8-12%, can significantly compress margins for mid-market producers lacking vertical integration. Trade policy shifts and tariff adjustments introduce additional uncertainty, particularly for brands sourcing from Asia. Supply-chain disruptions, logistics bottlenecks, and rising labor costs in key manufacturing hubs add further operational risk. Companies without diversified sourcing strategies or pricing flexibility face margin erosion in competitive price segments.

Brand Saturation and Fast-Fashion Competition

The proliferation of trend-driven brands and fast-fashion players intensifies competition, particularly in mid-market and entry-level categories. Rapid design cycles increase SKU proliferation and working capital requirements, raising inventory management complexity. Unsold seasonal inventory often leads to heavy discounting, which can reduce annual gross margins by several percentage points and weaken brand positioning. Lower barriers to entry in digital retail amplify competition from emerging labels. Sustained differentiation through craftsmanship, storytelling, and supply-chain efficiency remains essential to defend pricing power.

Opportunity Analysis - Emerging Markets and Expanding Middle Class

Growing discretionary income across Asia, India, and Southeast Asia provides a multi-year growth runway. Rising middle-class populations and increased urbanization support aspirational purchases in both accessible luxury and premium tiers. Localized product assortments, culturally tailored marketing strategies, and region-specific price architecture improve conversion rates and shorten breakeven timelines. Strategic partnerships with regional distributors and e-commerce platforms enhance market penetration. Brands that align digital engagement with local payment ecosystems and fulfillment networks can accelerate scalable growth.

Product and Channel Innovation

Modular and multifunctional bag designs address evolving lifestyle needs, including hybrid work and travel demands. Digital-physical integrations, such as augmented reality visualization, authenticated resale platforms, and NFT-linked ownership, open complementary revenue channels. Limited-edition drops and capsule collaborations drive scarcity-based demand, enhancing perceived exclusivity. Repair, refurbishment, and certified resale services extend product life cycles while generating incremental margin. Early adopters of authentication technologies and circular-economy initiatives can strengthen consumer trust and unlock long-term customer lifetime value.

Category-wise Analysis

Product Type Insights

Tote bags are anticipated to account for 40.8% of the market share in 2026, reinforcing their dominant position. Their large carrying capacity, structural simplicity, and cross-functional appeal support widespread adoption across professional, travel, retail, and daily-use contexts. The tote silhouette adapts effectively across materials and price tiers, ranging from canvas utility designs to premium leather offerings from brands such as Louis Vuitton and Michael Kors. Retailers consistently report stable sell-through rates for totes across seasons, positioning them as revenue stabilizers within broader assortments. In North America and Europe, tote models often function as entry-level luxury purchases, strengthening customer acquisition funnels and encouraging repeat buying. Corporate gifting, promotional branding, and sustainability-driven reusable shopping initiatives further reinforce demand, particularly for canvas and structured hybrid totes. Their scalability in production and merchandising versatility ensures continued leadership in both volume and value terms.

Satchels are projected to be the fastest-growing product category. Structured silhouettes, defined compartments, and compact yet practical sizing align well with urban commuting and hybrid work lifestyles. Fashion-forward brands, including Coach and Kate Spade New York, frequently introduce limited-edition satchel collections to capitalize on influencer marketing and digital campaigns. Convertible strap functionality enhances versatility, allowing satchels to transition between handheld and crossbody formats, which increases consumer willingness to pay within the US$100-US$300 range. Capsule collaborations and social media-driven product drops create demand surges, particularly among Gen Z and millennial buyers. Mid-sized satchels strike a balance between formal structure and everyday practicality, making them suitable for office, travel, and social settings. This adaptability positions satchels for sustained above-average growth relative to larger tote formats.

Material Insights

Leather remains the leading material category with 41.4% of market share and is anticipated to maintain this dominance through the forecast period due to its association with durability, craftsmanship, and premium positioning. Luxury conglomerates such as LVMH and Kering continue investing in vertically integrated supply chains and certified tanneries to ensure traceability and compliance with environmental standards. Premium leather bags command higher average selling prices (ASPs) and longer replacement cycles, supporting strong gross margins. In mature markets, including North America and Europe, leather dominates total revenue contribution due to established luxury consumption patterns and gifting traditions. Innovations in vegetable tanning, chrome-free processing, and biodegradable treatments are further strengthening leather’s long-term value proposition while addressing regulatory and sustainability pressures.

Fabric materials, including recycled polyester, organic cotton, and bio-based blends, represent the fastest-growing segment within the material category. Rising sustainability awareness and comparatively lower production costs accelerate adoption, particularly across mid-market and fast-fashion brands such as Zara and H&M. Fabric allows rapid prototyping, lightweight construction, and localized manufacturing, reducing lead times and inventory risks. Growth is reinforced by corporate commitments to reduce Scope 3 emissions and expand circular production practices, including take-back and recycling programs. Consumers increasingly value durability-to-weight ratios and washable convenience, making fabric-based handbags attractive for travel, student use, and everyday casual settings. As environmental impact becomes a core purchasing criterion, fabric collections are expected to steadily gain incremental share from traditional leather categories.

Regional Insights

North America Handbag Market Trends - Omnichannel Retail Strength and Resale-Driven Premium Value Retention

North America is expected to account for approximately 32.1% of market share in 2026, led overwhelmingly by the U.S., and remains the most profitable region in value terms. High disposable income, strong brand consciousness, and a mature department store and specialty retail ecosystem underpin sustained demand. Urban fashion centers such as New York and Los Angeles drive premium handbag sales through flagship stores and experiential retail formats operated by brands including Coach and Michael Kors. The expansion of direct-to-consumer (DTC) platforms by Tapestry, Inc. has strengthened margin control and customer data analytics, supporting higher repeat purchase rates. Omnichannel retail integration remains a defining structural advantage. Major retailers such as Nordstrom continue investing in inventory visibility systems and same-day fulfillment, improving conversion and retention metrics. At the same time, resale platforms like The RealReal have expanded authentication centers in the U.S., reinforcing price transparency and liquidity in secondary markets. This resale maturity enhances primary market confidence, particularly for premium leather handbags that retain value.

Regulatory emphasis on consumer protection, labeling compliance, and evolving tariff frameworks influences sourcing strategies. U.S.-China trade tensions have prompted selective nearshoring to Mexico and Central America for fabric-based products, reducing lead times and exposure to import duties. Investment momentum increasingly targets accessible-luxury positioning, resale authentication infrastructure, and logistics automation. These structural shifts reinforce North America’s leadership in both value realization and innovation adoption.

Europe Handbag Market Trends - Heritage Luxury Manufacturing and Regulatory-Led Sustainability Transformation

Europe represents a substantial share of global value due to its concentration of heritage luxury houses, vertically integrated manufacturing clusters, and high per-capita discretionary spending. France, Germany, the U.K., Italy, and Spain collectively shape regional demand across luxury and premium tiers. Flagship maisons such as Louis Vuitton and Gucci continue expanding artisanal production facilities in France and Italy, reinforcing “Made in Europe” positioning and supporting regional employment. European Union regulatory frameworks increasingly prioritize environmental compliance, supply-chain traceability, and circular economy targets. Groups like Kering have advanced material traceability programs and biodiversity commitments, strengthening brand differentiation while absorbing higher short-term compliance costs. The EU’s evolving eco-design and product passport initiatives are pushing brands to enhance transparency in leather sourcing and lifecycle disclosures. While these measures elevate operational expenses, they also elevate perceived product integrity and long-term brand equity.

Tourism-driven retail remains structurally important in fashion capitals such as Paris and Milan, where luxury boutiques benefit from cross-border spending. The reopening and modernization of landmark department stores, including Selfridges, have revitalized experiential retail formats that combine physical craftsmanship storytelling with digital engagement. Investment continues in atelier modernization, artisanal training programs, and advanced e-commerce integration. Europe’s blend of heritage production and regulatory leadership positions it as both a value anchor and a sustainability benchmark for the global market.

Asia Pacific Handbag Market Trends-Digital Commerce Acceleration and Mainland China-Led Luxury Consumption Growth

Asia Pacific is the fastest-growing regional market, driven by rapid urbanization, expanding middle-class income cohorts, and strong digital commerce adoption. China remains the largest regional contributor by value, supported by domestic luxury consumption growth and the localization strategies of global brands such as Prada and Chanel, which have expanded boutique networks and digital storefronts on major Chinese e-commerce ecosystems. Post-pandemic repatriation of luxury spending has structurally increased mainland China’s share of regional sales.

Japan maintains one of the highest per-capita luxury spending rates globally and a highly developed resale culture, with platforms such as Mercari supporting active secondary trading of premium handbags. This liquidity reinforces long-term value perception, particularly for leather goods. In India, rising digital payment penetration and premium mall expansion in cities like Mumbai and Bengaluru are accelerating mid-market and premium adoption, benefiting brands including H&M and regional franchise operators.

Asia’s manufacturing ecosystem offers scale and cost efficiencies, especially for non-leather and mid-market fabric categories. Countries such as China and Vietnam remain integral production hubs for global supply chains. Regulatory diversity across markets requires adaptive compliance strategies, particularly in labeling, import licensing, and sustainability reporting. Brands are investing heavily in localized influencer marketing, livestream commerce, and regional fulfillment hubs, which are compressing delivery timelines and improving customer engagement. These structural investments underpin Asia Pacific’s position as the primary volume-growth engine over the forecast horizon.

Competitive Landscape

The global handbag market exhibits value concentration in the luxury tier, while unit demand remains fragmented across mid-market and entry-level segments. Major luxury conglomerates command a significant value share due to elevated ASPs and global brand equity. Meanwhile, digital-native and regional brands compete on speed-to-market and price accessibility. Consolidation opportunities persist, particularly within accessible-luxury and DTC platforms.

Leading companies prioritize exclusivity-driven product drops, vertical integration, omnichannel expansion, and sustainability certification. Emerging brands emphasize social commerce, influencer partnerships, and agile supply chains. Authentication technology and resale integration increasingly serve as competitive differentiators.

Key Industry Developments:

- In April 2025, Prada Group completed the acquisition of Versace. In a strategic move to expand its luxury portfolio and market influence, Prada finalized a US$1.375 billion acquisition of Versace, integrating the brand into its Italian manufacturing and design ecosystem to strengthen competitive positioning globally in handbags and broader fashion.

- In September 2025, Alo Yoga expanded into luxury handbags. Alo launched a high-end handbag line priced between US$1,200 and US$3,600, with pieces crafted in Florence, Italy, and showcased in global cities such as New York, London, and Aspen.

Companies Covered in Handbag Market

- Louis Vuitton

- Gucci

- Chanel

- Hermès

- Prada

- Dior

- Coach

- Michael Kors

- Kate Spade New York

- Burberry

- Fendi

- Bottega Veneta

- Saint Laurent

- Balenciaga

- Tory Burch

- Longchamp

- Celine

- Valentino

Frequently Asked Questions

The global handbag market size is projected to reach US$73.2 billion in 2026.

The handbag market is forecast to attain a value of US$123.9 billion by 2033, reflecting steady expansion over the assessment period.

Key trends include rising demand for versatile and functional product designs, increasing penetration of digital and omnichannel retail models, growing emphasis on sustainable materials such as recycled fabrics, and the expansion of resale and circular economy platforms. Brands are also investing in localized manufacturing and supply chain diversification to manage cost volatility and regulatory compliance.

The tote segment leads the product category with 40.8% market share, driven by its practicality, scalability across price tiers, and strong adoption across professional and everyday use cases.

The handbag market is projected to grow at a CAGR of 7.8% between 2026 and 2033.

Major players with strong brand portfolios and global presence include Louis Vuitton, Gucci, Coach, Michael Kors, and Chanel.