- Industrial Goods & Service

- Gravure Printing Machines Market

Gravure Printing Machines Market Size, Share, and Growth Forecast, 2026 - 2033

Gravure Printing Machines Market by Application (Label Manufacturing, Decorative Printing, Others), Substrate Type (Plastic Films, Paper and Paperboard, Others), Printing Speed, and Regional Analysis for 2026 - 2033

Gravure Printing Machines Market Size and Trends Analysis

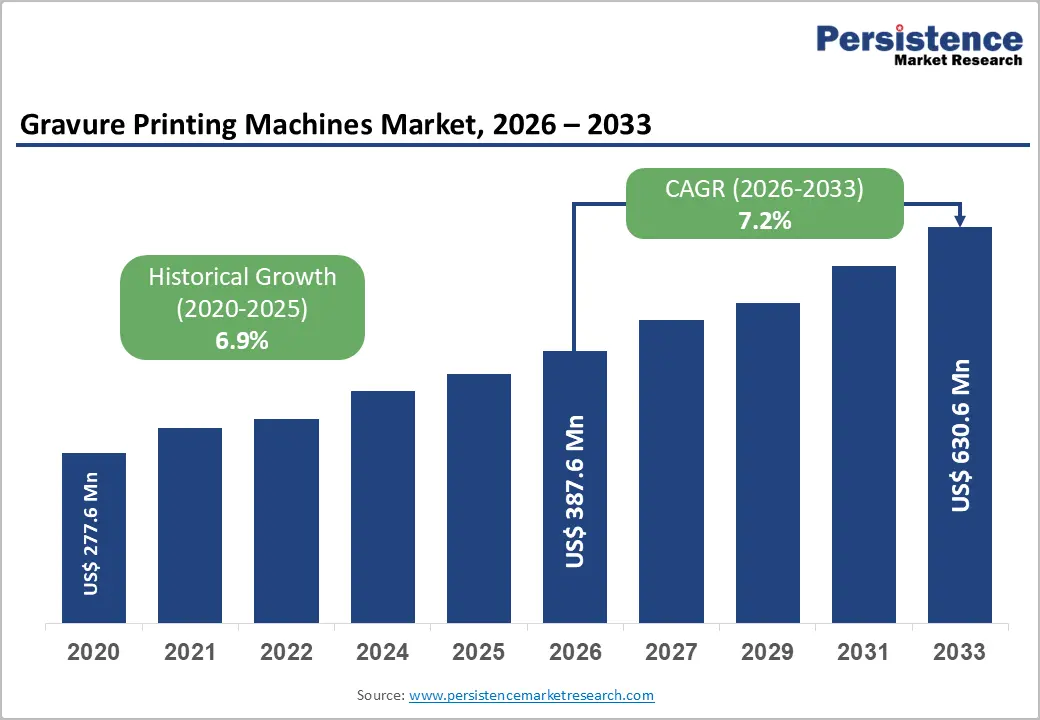

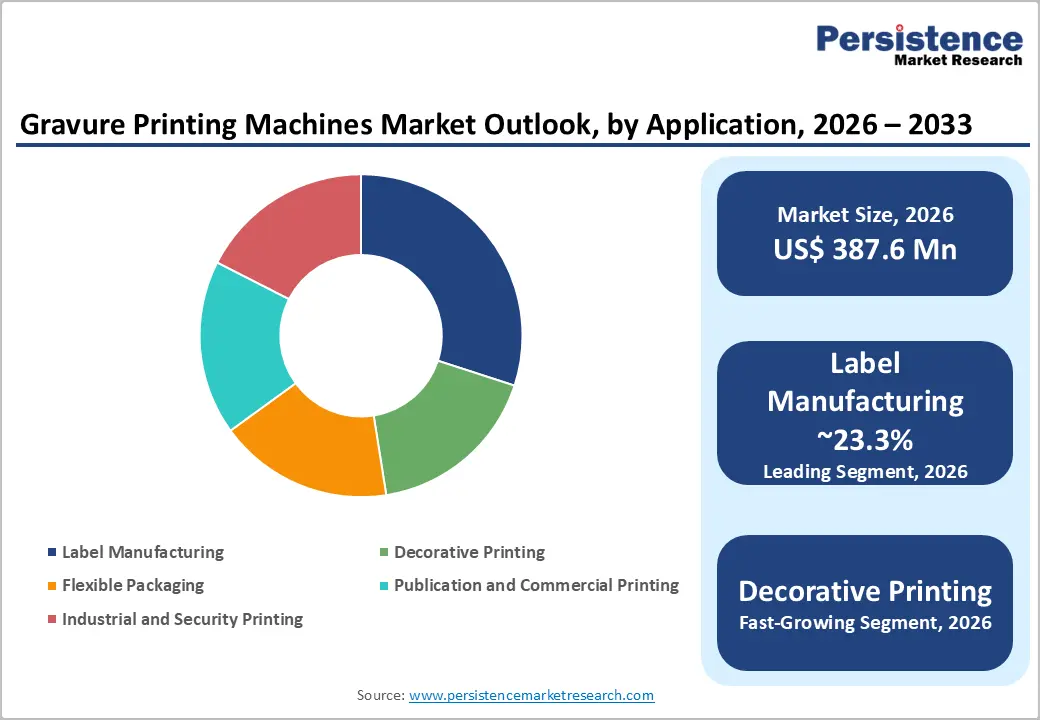

The global gravure printing machines market size is likely to be valued at US$ 387.6 million in 2026 and is expected to reach US$ 630.6 million by 2033, growing at a CAGR of 7.2% between 2026 and 2033, driven by the expanding flexible packaging sector and increasing demand for high-quality decorative printing.

Gravure technology remains a preferred solution for large-scale production due to its consistent print quality, superior color depth, and ability to handle diverse substrates at high speeds. Technological advancements in automation, energy-efficient drying systems, and improved process control are further improving operational efficiency for converters. Although competition from flexographic and digital printing technologies remains a structural challenge, gravure presses continue to maintain strong adoption in long-run industrial applications and premium packaging production.

Key Industry Highlights:

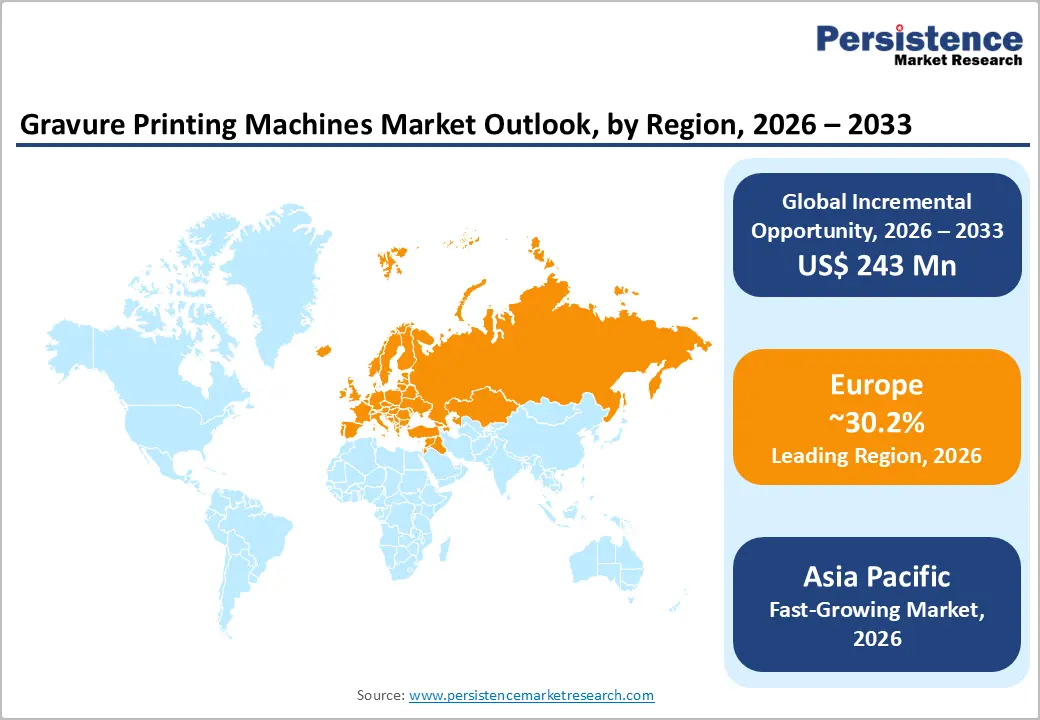

- Leading Region: Europe is projected to dominate the market, accounting for 30.2% of market revenue, benefiting from a strong printing technology heritage, advanced packaging industries in countries such as Germany and Italy, and strict environmental regulations that encourage investment in modern, high-efficiency gravure presses.

- Fastest-growing Region: Asia Pacific is the fastest-growing regional market, supported by expanding manufacturing capacity, rapid urbanization, and increasing consumption of packaged goods across China, India, and Southeast Asia.

- Dominant Application: Label manufacturing remains the largest application segment, anticipated to represent 23.3% of market share, supported by high-volume label production requirements in the food, beverage, and consumer packaged goods industries.

- Leading Substrate Type: Plastic films are anticipated to account for 29.8% of market revenue, driven by widespread adoption of flexible plastic packaging for food preservation, lightweight logistics, and large-scale industrial printing applications.

| Key Insights | Details |

|---|---|

| Gravure Printing Machines Market Size (2026E) | US$387.6 Mn |

| Market Value Forecast (2033F) | US$630.6 Mn |

| Projected Growth (CAGR 2026 to 2033) | 7.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Packaging-Driven Volume Growth and Premiumization

The expansion of global flexible packaging production is a major driver of demand for gravure printing machines. Flexible packaging is widely used across food, beverages, pharmaceuticals, and personal care products due to its lightweight nature, extended shelf life benefits, and strong barrier properties. Gravure printing remains a preferred technology for packaging converters because it offers excellent tonal gradation, consistent ink transfer, and superior image clarity across long production runs. Large consumer goods companies frequently specify gravure printing for packaging with metallic finishes, photographic imagery, and detailed branding elements. As consumer product companies increase investment in premium packaging designs to strengthen brand differentiation, converters require printing systems capable of delivering high resolution and precise color reproduction. Gravure presses are particularly suited for these requirements because engraved cylinders ensure uniform ink transfer throughout extended production runs. As a result, even modest growth in global packaging production volumes generates significant demand for gravure printing equipment, especially among large-scale packaging converters.

Process Automation and Sustainability Improvements

Technological innovation in gravure printing machinery has significantly improved productivity and environmental performance. Modern gravure presses incorporate automated registration systems, intelligent ink circulation units, and advanced drying modules that reduce setup time and material waste. These improvements enable converters to achieve higher production efficiency while maintaining strict quality standards. Energy-efficient drying technologies and solvent recovery systems have also become critical components of new gravure printing machines. Environmental regulations and corporate sustainability goals are encouraging converters to invest in equipment that reduces volatile organic compound emissions and energy consumption. In many cases, reducing waste during production cycles significantly improves the economic return on new gravure press installations. Consequently, many converters are upgrading legacy equipment with modern automated systems to improve operational efficiency and regulatory compliance.

Emergence of Short-Run and High-Value Applications

Historically, gravure printing technology has been optimized for very long production runs. However, recent equipment innovations have enabled gravure presses to handle shorter runs more efficiently through modular cylinder configurations and faster changeover systems. These capabilities allow converters to accommodate more diversified product portfolios without sacrificing print quality. This development has expanded the addressable market for gravure presses. Contract packaging companies that previously relied primarily on flexographic printing are increasingly evaluating gravure systems for specialized decorative packaging and premium label production. As consumer brands introduce more product variations and limited-edition packaging designs, gravure presses capable of shorter production cycles offer a competitive advantage while preserving the quality standards associated with the technology.

Barrier Analysis - High Capital Investment and Long Payback Periods

One of the most significant barriers to the adoption of gravure printing machines is the substantial capital investment required for equipment installation. Gravure printing systems typically require specialized infrastructure, including cylinder engraving equipment, solvent recovery units, and advanced drying systems. These components significantly increase converters' total cost of ownership. For small and medium-scale printing companies, achieving the production volume required to justify the investment can be challenging. The economic viability of gravure presses depends heavily on high utilization rates and long production runs. If printing capacity is underutilized, the payback period for new installations can extend considerably, discouraging investment in certain market segments.

Competition from Flexographic and Digital Printing Technologies

Advancements in flexographic and digital printing technologies have created strong competitive pressure for gravure printing systems. Modern flexographic presses offer improved print resolution, faster setup times, and lower operating costs for medium-volume production. Similarly, digital printing technologies provide exceptional flexibility for short runs, rapid design changes, and personalized packaging. These advantages make flexographic and digital printing more attractive for applications involving frequent design changes or limited production volumes. As a result, gravure printing is increasingly concentrated in large-scale industrial applications where long production runs and high image quality justify the higher capital investment.

Opportunity Analysis - Expansion of Manufacturing Capacity in the Asia Pacific

The Asia Pacific region is emerging as a major growth engine for the market, driven by rapid industrialization and expanding packaging demand. Countries such as China and India have become key manufacturing hubs for consumer goods, resulting in increased demand for high-volume packaging production. Many packaging converters in these markets are expanding capacity to support both domestic consumption and export-oriented production. This trend is creating strong demand for high-speed gravure presses capable of delivering consistent print quality at an industrial scale. Equipment manufacturers that establish regional manufacturing facilities and service networks in the Asia Pacific are well-positioned to benefit from this expansion.

Integration of Functional Coating and Specialty Printing

Another important opportunity lies in integrating gravure printing technology with advanced coating and laminating processes. Gravure presses are increasingly configured with inline modules that apply protective coatings, barrier layers, and specialty finishes. These capabilities enable packaging converters to produce multifunctional packaging materials in a single production line. Such integrated systems reduce processing time and improve production efficiency while creating new value-added services for brand owners. As demand grows for advanced packaging materials with enhanced barrier properties and decorative features, gravure printing machines equipped with multifunctional capabilities are expected to gain wider adoption.

Category-wise Analysis

Application Insights

Label manufacturing represents the largest application segment in the market, anticipated to account for approximately 23.3% of market share in 2026. Gravure printing technology is widely adopted for high-volume label production because it enables precise image reproduction, consistent color, and repeatable print quality across long production runs. These capabilities are critical for consumer packaged goods (CPG) companies that require uniform brand identity and regulatory information across millions of product units, particularly in sectors such as food, beverages, personal care, and household products.

The expansion of organized retail and the growth of packaged food consumption have significantly strengthened demand for high-quality printed labels. Gravure presses allow label manufacturers to operate at high printing speeds while maintaining tight quality control standards, which is essential for global brands that require strict color management and traceability. For example, packaging converters supplying labels for major beverage companies such as The Coca-Cola Company and PepsiCo rely on high-capacity gravure printing systems to maintain consistent branding across multiple regional production facilities. As multinational brands expand distribution networks across emerging economies, the need for scalable label production capabilities continues to reinforce the dominant role of gravure printing machines in this application segment.

Decorative printing represents the fastest-growing application segment in the market. Decorative printing is commonly used in luxury packaging, premium consumer goods packaging, decorative laminates, and high-end retail product presentation, where aesthetic quality plays a key role in consumer purchasing decisions. Rising competition in retail markets has encouraged brands to invest in visually distinctive packaging designs that enhance product differentiation on store shelves. Gravure printing technology is particularly well-suited for decorative applications because it delivers exceptional color depth, metallic effects, fine tonal gradation, and high-resolution image reproduction.

These characteristics make gravure presses attractive for premium packaging categories such as cosmetics, confectionery, and luxury beverages. For instance, cosmetic brands frequently use decorative gravure printing for metallic foil-based packaging and laminated pouches, which require high precision and consistent finish quality. Similarly, manufacturers of decorative laminates for furniture and interior surfaces use gravure printing to produce wood grain textures, marble patterns, and complex surface designs. Companies such as Sappi, a global materials and specialty paper manufacturer, supply coated packaging papers and substrates designed for gravure printing, which are widely used by packaging converters for premium labels, flexible packaging, and decorative packaging applications.

Substrate Type Insights

Plastic films represent the largest substrate category in the market, accounting for approximately 29.8% of global revenue in 2026. Flexible plastic packaging is widely used across the food and beverage industry due to its lightweight structure, durability, barrier properties, and ability to preserve product freshness and shelf life. Materials such as polyethylene (PE), polypropylene (PP), and polyethylene terephthalate (PET) films are commonly used for flexible packaging formats, including pouches, sachets, and wrappers.

Gravure printing technology is particularly effective for plastic film substrates because it provides uniform ink distribution, excellent adhesion, and consistent image quality even on smooth, non-porous surfaces. High-speed gravure presses enable packaging converters to print large volumes of flexible film packaging with minimal variation in color density or registration, making the technology well-suited for industrial-scale production. Global packaging manufacturers such as Amcor and Berry Global rely on gravure printing technology for large-scale production of flexible packaging used for snack foods, frozen foods, and ready-to-eat meals.

Paper and paperboard substrates represent the fastest-growing segment. The increasing shift toward environmentally sustainable and recyclable packaging materials is encouraging many consumer goods companies to adopt paper-based alternatives to conventional plastic packaging. Government policies and sustainability commitments by major consumer brands are accelerating the adoption of paper-based flexible packaging and recyclable carton formats. Organizations such as the European Commission and the U.S. Environmental Protection Agency (EPA) have introduced initiatives promoting recyclable and circular packaging solutions, which are influencing packaging material choices across multiple industries. As a result, packaging converters are investing in printing technologies that support paper substrates without compromising print quality.

Advancements in gravure printing technology have improved its compatibility with paper and paperboard materials. Improved drying systems, precision tension control mechanisms, and water-based ink formulations now enable high-quality printing on paper surfaces while minimizing substrate distortion or damage. For example, several packaging converters producing snack packaging and retail paper bags have adopted gravure printing for high-definition graphics and brand messaging on paper-based packaging formats. As consumer brands increasingly commit to sustainability targets, such as 100% recyclable packaging goals announced by companies including Unilever and Nestlé, the demand for gravure printing machines capable of processing paper and paperboard substrates is expected to grow steadily over the coming years.

Regional Insights

North America Gravure Printing Machines Market Trends-Technology Upgrades Driven by Premium Flexible Packaging Demand and Environmental Compliance

North America represents a technologically advanced market for gravure printing machines, supported by a mature packaging ecosystem and strong demand from consumer goods manufacturers. The U.S. remains the dominant market within the region due to its large consumer packaged goods (CPG) industry, advanced converting infrastructure, and extensive retail distribution networks. Companies operating in food, beverages, pharmaceuticals, and personal care products require high-resolution packaging graphics and consistent large-volume production, which supports continued adoption of gravure printing technology.

Many packaging converters in North America specialize in premium flexible packaging, decorative packaging, and shrink sleeve labels, which require precise image reproduction and stable color consistency. Gravure printing remains a preferred solution for these applications as it provides exceptional tonal range and repeatable output across long production runs. For example, packaging suppliers such as Amcor, Berry Global, and Sonoco Products Company operate large flexible packaging facilities in the U.S. and Canada where gravure printing technology is frequently used for snack packaging, frozen food pouches, and beverage shrink sleeves. These companies supply major consumer brands, including PepsiCo, Procter & Gamble, and The Coca-Cola Company, which require consistent packaging graphics across multiple product lines.

Environmental regulations also play a major role in shaping equipment investment decisions in North America. Agencies such as the U.S. Environmental Protection Agency (EPA) regulate volatile organic compound (VOC) emissions from printing processes, encouraging converters to adopt modern gravure presses equipped with energy-efficient drying systems, solvent recovery units, and improved ink management technologies. Investment activity in North America is therefore largely driven by replacement demand and technological upgrades rather than greenfield expansion.

Converters are replacing legacy presses with machines that support digital process monitoring, automated register control, and inline defect inspection systems. Equipment manufacturers such as Bobst Group SA and Windmöller & Hölscher have expanded their presence in the region by supplying advanced gravure presses designed for high-speed flexible packaging production. These systems allow converters to increase throughput, reduce material waste, and comply with environmental standards, reinforcing North America’s role as a high-technology gravure printing market.

Europe Gravure Printing Machines Market Trends - Innovation-Led Market Supported by Strong Manufacturing Base and Sustainability Regulations

Europe holds the largest share of the global gravure printing machines market, accounting for approximately 30.2% of the market share in 2026. The region has a long history of innovation in printing technology and precision manufacturing, and it is home to several leading gravure equipment manufacturers. European engineering companies have historically played a central role in advancing high-speed printing systems, automated press control technologies, and cylinder engraving techniques.

Countries such as Germany, Italy, Spain, and France maintain well-developed packaging industries that rely heavily on high-performance printing technologies. Germany, in particular, is a major hub for printing equipment manufacturing, with companies such as Windmöller & Hölscher and Koenig & Bauer producing advanced packaging and printing systems used worldwide. Italy also plays a key role through companies such as Uteco Group, which supplies gravure presses for flexible packaging and decorative printing applications.

The European Union’s regulatory framework strongly influences equipment investment across the region. Regulations under initiatives such as the European Green Deal and the Packaging and Packaging Waste Directive encourage companies to adopt printing technologies that support recyclable packaging materials, reduce solvent emissions, and improve energy efficiency. Converters are increasingly investing in next-generation gravure presses with solvent recovery systems and advanced drying technologies. Europe also maintains a strong aftermarket service ecosystem, including cylinder engraving specialists, maintenance providers, and technology integrators. Companies such as Siegwerk Druckfarben, a global ink manufacturer headquartered in Germany, collaborate with packaging converters to develop low-solvent and environmentally optimized ink formulations suitable for gravure printing. This integrated supply chain supports long equipment lifecycles and encourages continued investment in gravure technology across the region.

Asia Pacific Gravure Printing Machines Market Trends - Rapid Market Expansion Driven by Manufacturing Growth and Rising Packaging Consumption

Asia Pacific represents the fastest-growing regional market for gravure printing machines, driven by rapid industrialization, expanding consumer markets, and strong growth in packaged goods consumption. Countries including China, India, Japan, and several Southeast Asian economies have become major production centers for consumer products, creating significant demand for high-volume packaging and labeling solutions. China is the largest market within the region due to its extensive manufacturing base and large domestic consumer market. The country hosts a vast network of packaging converters supplying industries such as food processing, consumer electronics, pharmaceuticals, and e-commerce retail.

Gravure printing machines are widely used because they support long production runs required for mass manufacturing environments. Chinese packaging manufacturers frequently produce flexible packaging for global brands, including Nestlé, Unilever, and Mars, which require high-capacity printing systems capable of maintaining consistent visual quality across large production volumes. India is also emerging as an important growth market due to rapid expansion in the packaged food and personal care sectors.

Local equipment manufacturers are playing an increasingly important role in the Asia Pacific market by offering cost-competitive gravure printing machines tailored to emerging market requirements. Chinese manufacturers such as Shaanxi Beiren Printing Machinery produce gravure presses designed for flexible packaging converters seeking affordable, high-capacity printing systems. These machines often feature simplified designs and lower capital costs, making them attractive to small and mid-sized packaging converters across Southeast Asia. The region is also witnessing rising investment in modern automated printing technologies. Japanese engineering companies such as Toshiba Machine (now Shibaura Machine) and specialized printing equipment suppliers continue to develop advanced industrial printing systems used in the packaging and electronics sectors.

Multinational packaging companies, including Amcor and Huhtamaki, have expanded production facilities across the Asia Pacific to serve regional consumer markets. The combination of rapid manufacturing growth, expanding consumer demand, and increasing investment in packaging infrastructure positions Asia Pacific as the most dynamic growth region for gravure printing machines during the forecast period. As global consumer brands continue to localize production in Asia, demand for high-capacity, high-speed printing equipment is expected to increase steadily.

Competitive Landscape

The global gravure printing machines market demonstrates a moderately concentrated competitive structure. A group of established equipment manufacturers dominates the high-performance segment of the market, offering technologically advanced printing systems for large packaging converters. At the same time, numerous regional manufacturers supply competitively priced equipment designed for emerging markets and small-scale printing companies. This dual structure results in strong competition across both premium and cost-efficient equipment segments.

Leading gravure printing machine manufacturers are focusing on technological innovation, sustainability improvements, and global service network expansion. Product development strategies emphasize automation, higher printing speeds, and improved environmental performance. At the same time, regional manufacturers are strengthening their market positions by offering cost-effective equipment and localized customer support.

Key Industry Developments:

- In December 2025, Bobst Group SA expanded the application of its oneECG extended color gamut technology for gravure printing, enabling converters to produce metallic effects using a standardized ink set. This development helps reduce ink waste, simplify printing workflows, and improve sustainability in flexible packaging production.

- In November 2025, Uteco Group showcased its latest printing and converting technologies at the Plastic & Rubber 2025 exhibition in Jakarta, highlighting advanced equipment and integrated solutions designed to support the growing flexible packaging sector in Asia.

Companies Covered in Gravure Printing Machines Market

- Bobst Group SA

- Windmöller & Hölscher Group

- Koenig & Bauer AG

- Uteco Group

- Shaanxi Beiren Printing Machinery Co., Ltd.

- Comexi Group Industries S.A.U.

- Cerutti Group (Officine Meccaniche Giovanni Cerutti S.p.A.)

- Rotomec S.p.A.

- Guangdong Jinming Machinery Co., Ltd.

- Toshiba Machine Co., Ltd. (Shibaura Machine Co., Ltd.)

- KYMC (Kuen Yuh Machinery Engineering Co., Ltd.)

- Taiyo Kikai Ltd.

- Wenzhou Donghai Printing Machinery Co., Ltd.

- Zhejiang Fangbang Machinery Co., Ltd.

- Shaanxi North Gravure Printing Machinery Co., Ltd.

- Pelican Rotoflex Pvt. Ltd.

- Prakash Web Offset Pvt. Ltd.

- Kohli Industries Pvt. Ltd.

Frequently Asked Questions

The global gravure printing machines market is expected to be valued at approximately US$387.6 million in 2026.

The gravure printing machines market is projected to reach US$630.6 million by 2033.

Key industry trends include rising adoption of automated high-speed presses, increasing demand for sustainable printing solutions with reduced solvent emissions, expansion of flexible packaging production, and integration of digital process control systems to improve production efficiency and print consistency.

Label manufacturing is the leading application segment, accounting for 23.3% of the global market share, supported by strong demand from the food, beverage, personal care, and consumer packaged goods industries.

The gravure printing machines market is expected to grow at a CAGR of 7.2% between 2026 and 2033.

Major companies include Bobst Group SA, Windmöller & Hölscher Group, Koenig & Bauer AG, Uteco Group, and Shaanxi Beiren Printing Machinery Co., Ltd.