- Industrial Goods & Service

- Air Insulated Switchgear Market

Air Insulated Switchgear Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Air Insulated Switchgear Market by Voltage Level (Low Voltage, Medium Voltage, High Voltage), Installation Type (Indoor AIS, Outdoor AIS), Application (Transmission & Utilities, Industrial, Commercial, Residential), and Regional Analysis for 2026 - 2033

Air Insulated Switchgear Market Trends & Analysis

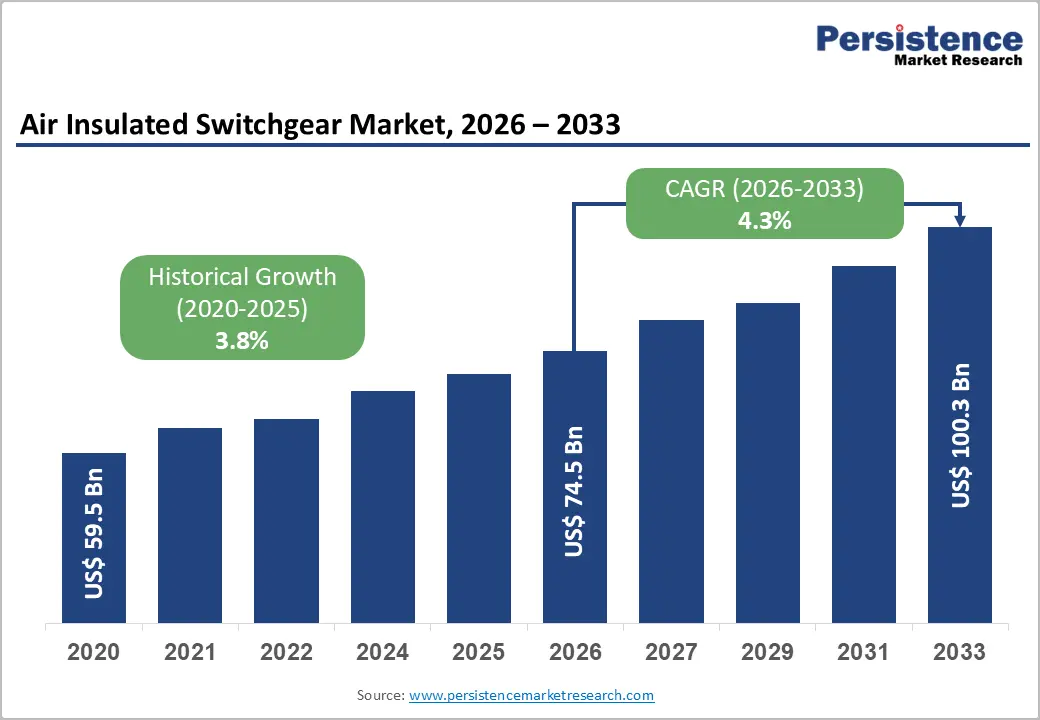

The global air insulated switchgear market size is anticipated at US$ 74.5 billion in 2026 and is projected to reach US$ 100.3 billion by 2033, growing at a CAGR of 4.3% between 2026 and 2033. This growth reflects deepening demand across power transmission, industrial electrification, and grid modernization programs, with AIS serving as the foundational switching and protection technology across 60%+ of global electrical substation infrastructure.

Expanding electricity grid infrastructure investment, renewable energy integration mandates requiring substation upgrades, and growing urbanization driving commercial and residential switchgear deployment are the primary growth catalysts. Smart grid programs across Asia Pacific, Europe, and North America are accelerating AIS replacement cycles toward digitally integrated protection systems. Infrastructure investment commitments under national energy transition policies are sustaining long-cycle AIS procurement demand through 2033.

Key Industry Highlights:

- Leading Voltage Segment: Low Voltage AIS leads at 45.6% share; Medium Voltage grows fastest at 4.8% CAGR, driven by renewable grid interconnection, industrial electrification, and smart distribution network upgrade programs globally.

- Top Application Segment: Transmission & Utilities leads application at 57.5% share; Industrial is poised to achieve a 6.4% CAGR, driven by manufacturing electrification, data center power infrastructure, and EV charging substation construction.

- Installation Type Leadership: Indoor AIS leads installation type at 60.4% share; Outdoor AIS grows fastest at 5.4% CAGR, driven by utility transmission substation construction and rural electrification programs across Asia and Africa.

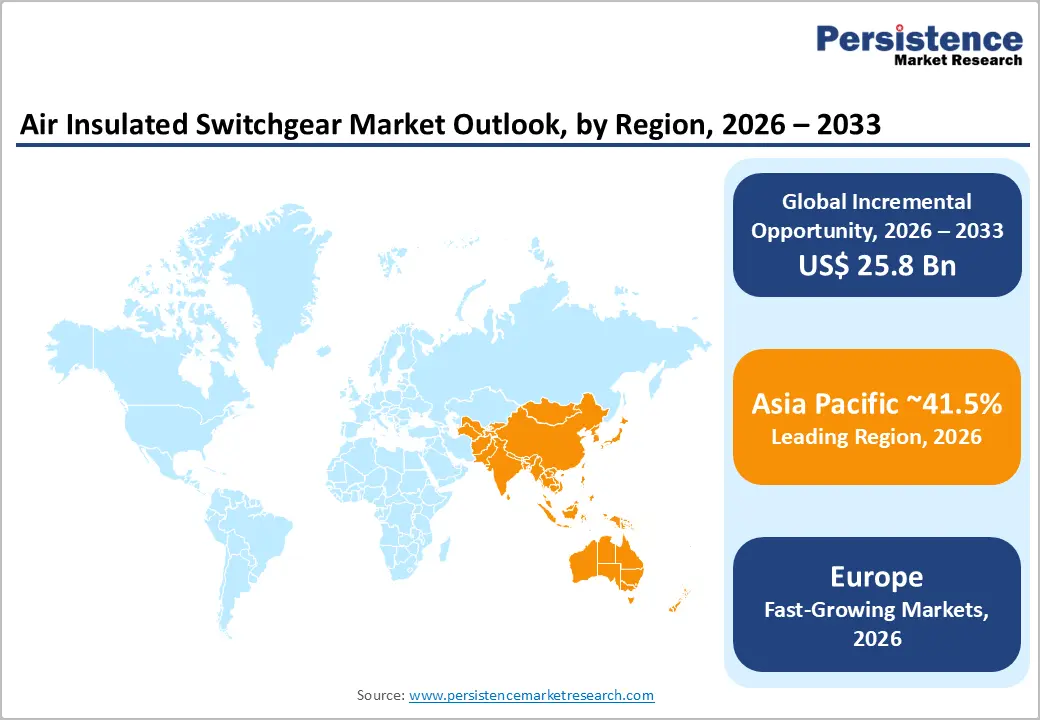

- Regional Performance: Asia Pacific dominates at 41.5% share, with China at US$ 13.5 Bn and India at US$ 7.1 Bn; North America holds a prominent 28.5% share with the U.S. at US$ 17.5 Bn.

- Strategic Developments: Hitachi Energy's European HV AIS framework agreement (April 2024) and Schneider Electric's Vietnam smart MV AIS deployment (August 2024) reflect intensifying smart substation investment across global utility markets.

Market Dynamics Analysis

Drivers - Global Electricity Grid Modernization and Power Infrastructure Investment Programs

Aging electrical grid infrastructure, particularly transmission and distribution substations operating beyond their 30-40-year design life across North America, Europe, and Asia, is generating large-scale AIS replacement and upgrade procurement demand. The U.S. Department of Energy's Grid Modernization Initiative has committed over US$ 30 billion in transmission infrastructure investment under the Infrastructure Investment and Jobs Act (2021), with switchgear system upgrades identified as a priority modernization component across aging substations. ENTSO-E (European Network of Transmission System Operators for Electricity) estimates that over €100 billion in European grid investment will be required through 2030 under the EU's REPowerEU and Green Deal frameworks.

Asia Pacific national utilities, including China State Grid Corporation, India's Power Grid Corporation, and ASEAN national power authorities, are executing large-scale substation construction and AIS procurement programs to extend high-voltage transmission networks into underserved industrial zones and growing urban centers. India's National Electricity Plan 2023 - 2032, approved by the Ministry of Power, targets 458 GW of total installed generation capacity by 2032, requiring proportional substation expansion across all voltage levels, which directly drives AIS procurement volume at industrial and utility scales. These coordinated national grid investment programs represent the most structurally durable demand driver for the AIS market through 2033.

Renewable Energy Capacity Expansion Requiring Substation and AIS Integration

The accelerating global transition toward wind and solar power generation is creating extensive new substation construction and AIS procurement requirements, as each renewable generation facility requires dedicated switchgear systems to connect variable-output generation to stable transmission and distribution grids. The International Energy Agency's Electricity 2024 report found that global renewable power capacity additions in 2023 reached 295 GW, the highest annual figure on record, and that each utility-scale wind or solar facility requires medium- and high-voltage AIS installations for grid connection, protection, and fault isolation.

The European Union's REPowerEU Plan targets 600 GW of wind and solar capacity by 2030, requiring an estimated 4,500-6,000 new or upgraded substations across the EU grid network, each incorporating AIS systems as the primary switching and protection infrastructure. The U.S. IRA's US$ 369 billion clean energy investment package is directly funding the installation of AIS interconnection substation equipment across 48 states. India's 500 GW renewable target by 2030 mandates extensive new MV and HV substation construction across wind-rich and solar-rich states, collectively making renewable energy the fastest-growing AIS demand vector alongside conventional grid modernization procurement through 2033.

Restraints - Long Project Approval and Permitting Timelines Constraining AIS Deployment Velocity

Large-scale transmission substation projects incorporating high-voltage AIS systems face environmental impact assessment requirements, land acquisition procedures, and grid interconnection approval processes that routinely extend project timelines by 3-7 years across the U.S. (FERC interconnection queue), EU (national grid operator approval procedures), and India (CEA clearance requirements). The U.S. FERC reported over 2,000 GW of generation capacity awaiting grid interconnection approval as of 2024, a backlog that delays associated substation AIS procurement and installation despite confirmed investment commitments, creating execution timeline gaps that constrain near-term market revenue realization.

Competition from Gas Insulated Switchgear (GIS) in Space-Constrained Urban Applications

Gas Insulated Switchgear (GIS) systems, occupying 70-80% less floor area than equivalent-voltage AIS configurations, present direct competitive substitution pressure in urban substation applications where land scarcity and indoor installation constraints make AIS's larger physical footprint a structural disadvantage. IEC 62271-203 standardization advances have progressively reduced GIS cost premiums over AIS for medium and high voltage applications, particularly in densely populated Asian metropolitan markets where urban substation space limitations are acute. This competitive dynamic is progressively narrowing the AIS addressable market in premium urban deployment segments where GIS spatial advantages outweigh AIS's lower per-unit capital cost.

Opportunities - Smart AIS Integration with Digital Substation and IEC 61850 Communication Standards

The global transition toward digital substations, adopting IEC 61850 communication-standard-based protection, control, and monitoring architectures, is creating a significant market opportunity for next-generation smart AIS systems that embed digital sensors, IoT connectivity, and advanced protection relay interfaces directly within the switchgear assembly. ABB, Siemens, and Schneider Electric are actively commercializing digitally integrated AIS platforms that replace conventional copper-wired protection and control systems with fiber-optic process bus communication architectures, reducing substation wiring complexity by 30-40% while enabling remote condition monitoring and predictive maintenance capability.

The global digital substation market is projected to grow at 8.5% CAGR through 2030 (IEC Technical Committee estimates), with smart AIS systems positioned as the primary hardware component enabling digital substation architecture at medium and high voltage levels. For AIS manufacturers investing in IEC 61850-compliant smart AIS platforms, the addressable premium product market within the broader AIS install base is estimated at US$ 8-12 Bn by 2030, representing a high-value differentiation opportunity that rewards technology-integrated platform providers capable of combining mechanical switchgear expertise with digital communication and software competencies.

Emerging Market Grid Electrification and Industrial Zone Expansion in Asia and Africa

Southeast Asia, South Asia, and Sub-Saharan Africa represent structurally underserved AIS markets where electrification rates remain below 70% in several nations, and industrial zone development is driving large-scale MV and HV substation construction programs that require cost-competitive AIS procurement at scale. The African Development Bank's New Deal on Energy for Africa targets universal electricity access by 2030, requiring an estimated US$ 55 billion in generation and transmission infrastructure investment across 54 member nations, each incorporating AIS systems as foundational switching infrastructure for new substation construction.

India's PM Gati Shakti National Master Plan and ASEAN's Trans-ASEAN Electricity Grid initiative are each mobilizing multi-billion-dollar grid investment programs requiring MV and HV AIS procurement at a national scale. Vietnam, Indonesia, the Philippines, and Bangladesh, among the world's fastest-growing power-demand markets, are implementing national electrification programs that require both new greenfield substation AIS installations and distribution network AIS upgrades. For AIS manufacturers with cost-competitive manufacturing platforms in India and China, these emerging market expansion programs represent a US$ 5-8 Bn incremental addressable opportunity within the 2026 - 2033 forecast window.

Category-wise Analysis

Voltage Level Insights

Low Voltage (LV) AIS leads the voltage level segment with a 45.6% share in 2026. LV AIS systems, operating at voltages below 1 kV, serve the highest-volume application base encompassing commercial buildings, residential complexes, light industrial facilities, and data centers, where standardized compact switchgear panels are procured in large quantities across construction and infrastructure projects globally. LV AIS benefits from the shortest project specification-to-delivery cycle, the widest distribution network coverage, and the highest replacement cycle frequency among all voltage levels.

MV AIS serves utility distribution and industrial applications at higher per-unit values, while HV AIS serves transmission-level utility applications at lower volumes. LV dominance is expected to persist, given the ongoing urbanization and the commercial construction pipeline, which are sustaining high-volume procurement through 2033.

Medium Voltage (MV) AIS is the fastest-growing voltage segment, with a 4.8% CAGR through 2033. Renewable energy grid interconnection at the distribution level, industrial electrification programs, and smart grid MV network upgrades are collectively driving accelerating MV AIS procurement across utility, industrial, and commercial applications globally.

Installation Type Insights

Indoor AIS leads the installation type segment with a 60.4% market share in 2026. Indoor AIS systems dominate by virtue of their applicability across the broadest range of commercial, industrial, and utility applications, where controlled environmental conditions, equipment protection requirements, and safety standards mandate indoor enclosure configurations. Industrial facilities, commercial buildings, data centers, hospitals, and urban utility substations all specify indoor AIS as the standard installation configuration.

Outdoor AIS serves transmission substations and rural utility applications where space availability and infrastructure economics favor open-air installation. Indoor AIS's leadership is reinforced by ongoing commercial construction and industrial facility investment, driving enclosed switchgear procurement at scale. Dominance is expected to be maintained through 2033 given the volume weight of commercial and industrial demand.

Outdoor AIS is the fastest-growing installation type, with a 5.4% CAGR through 2033. Transmission grid expansion, rural electrification substation construction, and utility-scale renewable energy generation interconnection substations, all requiring open-air AIS configurations, are driving accelerating outdoor AIS procurement across Asia Pacific, Middle East, and Africa markets.

Application Analysis

Transmission & utilities leads the application segment with a 57.5% market share in 2026. Utility transmission and distribution networks represent the highest-value and most volume-intensive AIS application, encompassing HV transmission substations, MV distribution substations, and generation facility interconnection switchyards across national power grid infrastructures globally. Grid expansion mandates, aging infrastructure replacement, and renewable energy integration substation construction sustain Transmission & utilities as the structurally dominant AIS procurement source.

Industrial applications serve process industries at a meaningful but lower share, while commercial and residential segments contribute significant LV AIS volume. The Transmission & Utilities segment's structural leadership is anchored by multi-decade national grid investment programs, ensuring a dominant share through 2033.

Industrial is the fastest-growing application segment, with a 6.4% CAGR through 2033. Manufacturing sector electrification, data center power infrastructure expansion, EV charging hub substation construction, and heavy industrial facility AIS upgrades for automation are collectively driving the Industrial segment AIS procurement at above-market growth rates through 2033.

Regional Market Insights

North America Air Insulated Switchgear Market Trends

North America holds a prominent 28.5% share of the global Air Insulated Switchgear Market in 2025, driven by the U.S. grid modernization investment pipeline, IRA-funded renewable transmission substation construction, and industrial facility AIS upgrade programs across manufacturing and data center sectors. FERC Order 2023's interconnection reform mandate and the DOE's US$ 30+ Bn grid investment commitment under the Infrastructure Investment and Jobs Act are translating into concrete substation AIS procurement across all voltage levels.

U.S Air Insulated Switchgear Market:

The U.S. market is estimated at US$ 17.5 Bn in 2026, sustained by IRA clean energy transmission mandates, aging substation AIS replacement programs, and hyperscale data center power infrastructure investment requiring MV and HV AIS configurations. Canada contributes oil sands, mining, and rural electrification AIS demand through provincial utility grid expansion. ABB, Eaton, Siemens, and GE Vernova anchor the regional competitive landscape with deep utility framework relationships.

Europe Air Insulated Switchgear Market Size

Europe holds a prominent share, growing at 4.0% CAGR through 2033, with Germany's AIS market estimated at US$ 3.9 Bn, anchored by the continent's industrial manufacturing base, EU Green Deal-driven renewable energy substation investment, and grid interconnection infrastructure expansion across member states.

Germany Air Insulated Switchgear Market Trends

Germany hosts the continent's most intensive industrial AIS demand, driven by automotive, chemical, and manufacturing sector electrification, alongside Siemens, Schneider Electric, and ABB's European manufacturing and R&D operations, sustaining technology leadership. EU Regulation (EU) 2019/943 on the internal electricity market mandates transmission grid investment across all member states proportional to renewable capacity expansion, directly driving MV and HV AIS substation procurement. The U.K. sustains offshore wind substation AIS investment, France drives nuclear generation facility AIS upgrade programs, and Spain contributes to solar transmission AIS demand. Europe's growth is anchored by REPowerEU investments in renewable substation infrastructure, EU Smart Grid Directive compliance mandates, and industrial decarbonization programs requiring grid-connected substation AIS upgrades.

Asia Pacific Air Insulated Switchgear Market Size

Asia Pacific commands the leading regional position at 41.5% share in 2025, driven by China's dominant power infrastructure investment, India's grid expansion programs, and ASEAN's accelerating national electrification initiatives requiring large-scale AIS procurement across all voltage levels.

China & India Air Insulated Switchgear Market Size

China's AIS market is estimated at US$ 13.5 Bn in 2026, sustained by China State Grid Corporation's massive annual substation construction program, the Belt and Road Initiative's cross-border power infrastructure projects, and the nation's 1,200 GW renewable capacity target by 2030. India's market at US$ 7.1 Bn is growing rapidly under the Power Grid Corporation's Green Energy Corridor transmission network program and the Rs. 3.03 trillion National Infrastructure Pipeline power sector investment.

Japan contributes to high-specification AIS demand through national utility grid resilience programs. ASEAN's industrial zones and electrification expansion are driving significant volume growth. Asia Pacific's manufacturing scale, with Hitachi, Mitsubishi, and domestic Chinese AIS manufacturers, provides cost and proximity advantages in the supply chain, sustaining regional competitive leadership through 2033.

Competitive Landscape

The global air insulated switchgear market is moderately consolidated, with the top 10 players accounting for approximately 60-65% of global revenue, led by ABB, Siemens, Schneider Electric, Eaton, and GE Vernova, who differentiate through comprehensive voltage range portfolios, digital substation integration capability, and utility-grade project engineering services. Energy-as-a-Service and AIS lifecycle management subscription models are emerging as differentiated commercial propositions.

Technology investment in IEC 61850-compliant smart AIS platforms, geographic expansion into Asia Pacific and Africa emerging grid markets, and strategic utility framework agreements sustaining long-cycle procurement contracts define the dominant strategic themes shaping the global AIS competitive landscape through 2033.

Key Developments:

- In March 2025, ABB Ltd. expanded its smart AIS digital substation portfolio with IEC 61850 process bus-integrated medium voltage switchgear, targeting utility grid modernization programs in Europe and North America requiring digitally enabled protection, control, and remote monitoring architectures at substation scale.

- In November 2024, Siemens AG announced investment in a new AIS manufacturing facility in India, supporting domestic grid expansion procurement under the Green Energy Corridor program and PM Gati Shakti infrastructure initiative, with committed production capacity targeting MV and HV AIS system volumes for Indian utility customers.

Companies Covered in Air Insulated Switchgear Market

- ABB Ltd.

- Siemens AG

- Schneider Electric SE

- Eaton Corporation PLC

- GE Vernova (Grid Solutions)

- Hitachi Energy Ltd.

- Mitsubishi Electric Corporation

- Larsen & Toubro Limited

- Toshiba Energy Systems & Solutions

- Lucy Electric

- CHINT Group Co. Ltd.

- CG Power and Industrial Solutions

- HYOSUNG Heavy Industries

- Fuji Electric Co. Ltd.

- Legrand SA

Frequently Asked Questions

The air insulated switchgear market is valued at US$ 74.5 Bn in 2026, projected to reach US$ 100.3 Bn by 2033.

Electricity grid modernization investment, renewable energy substation construction, and urbanization-driven commercial and industrial switchgear procurement are the primary structural growth drivers.

The air insulated switchgear market is projected to grow at a CAGR of 4.3% from 2026 to 2033.

Smart IEC 61850-integrated AIS platforms for digital substation programs and emerging market grid electrification infrastructure investment represent the most strategically actionable near-term growth opportunities.

ABB, Siemens, Schneider Electric, Eaton, GE Vernova, Hitachi Energy, Mitsubishi Electric, Larsen & Toubro, Toshiba, and CHINT Group are the leading global participants.