- Industrial Goods & Service

- Cutting and Bending Machine Market

Cutting and Bending Machine Market Size, Share, and Growth Forecast 2026 - 2033

Cutting and Bending Machine Market by Machine Type (Cutting Machines, Bending Machines, Combined Cutting & Bending Machines, Straightening Machines, Mesh Cutting & Bending Machines, Stirrup Bending Machines), Automation Level (Manual Machines, Semi-Automatic Machines, Fully Automatic Machines, CNC Machines), Technology, Application, End-user, and Regional Analysis, 2026 - 2033

Cutting and Bending Machine Market Size and Trend Analysis

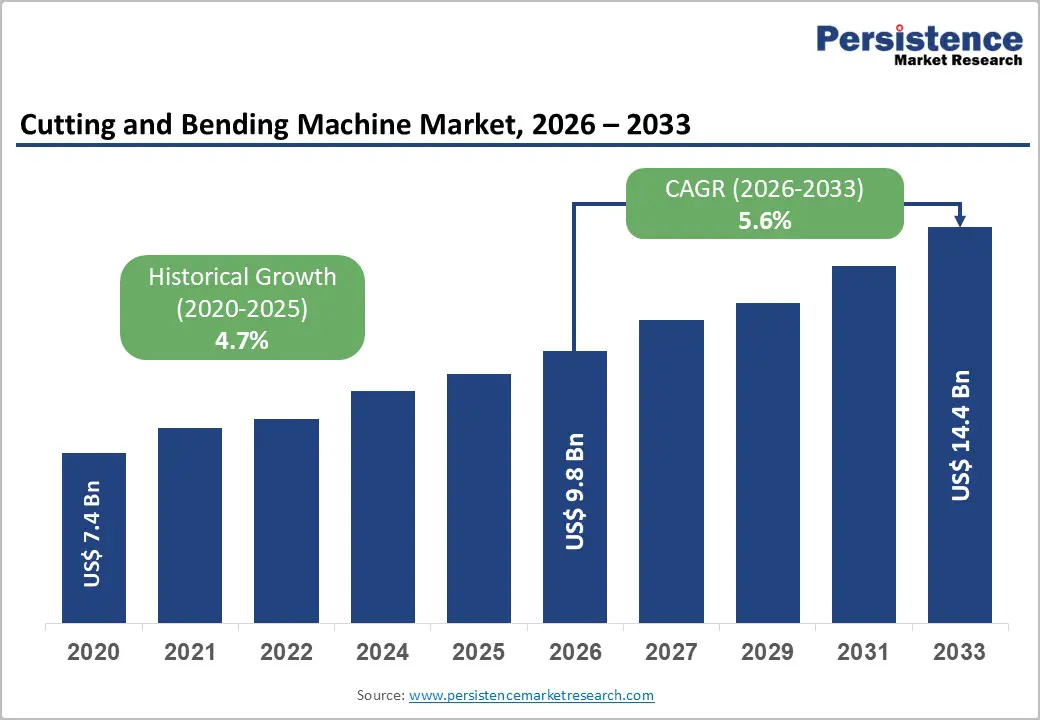

The global cutting and bending machine market size is likely to be valued at US$ 9.8 billion in 2026 and is expected to reach US$ 14.4 billion by 2033, growing at a CAGR of 5.6% during the forecast period from 2026 to 2033.

The market is advancing robustly, driven by surging global infrastructure investment, rapid adoption of CNC and AI-integrated fabrication technologies, and expanding automotive and aerospace manufacturing.

Key Industry Highlights:

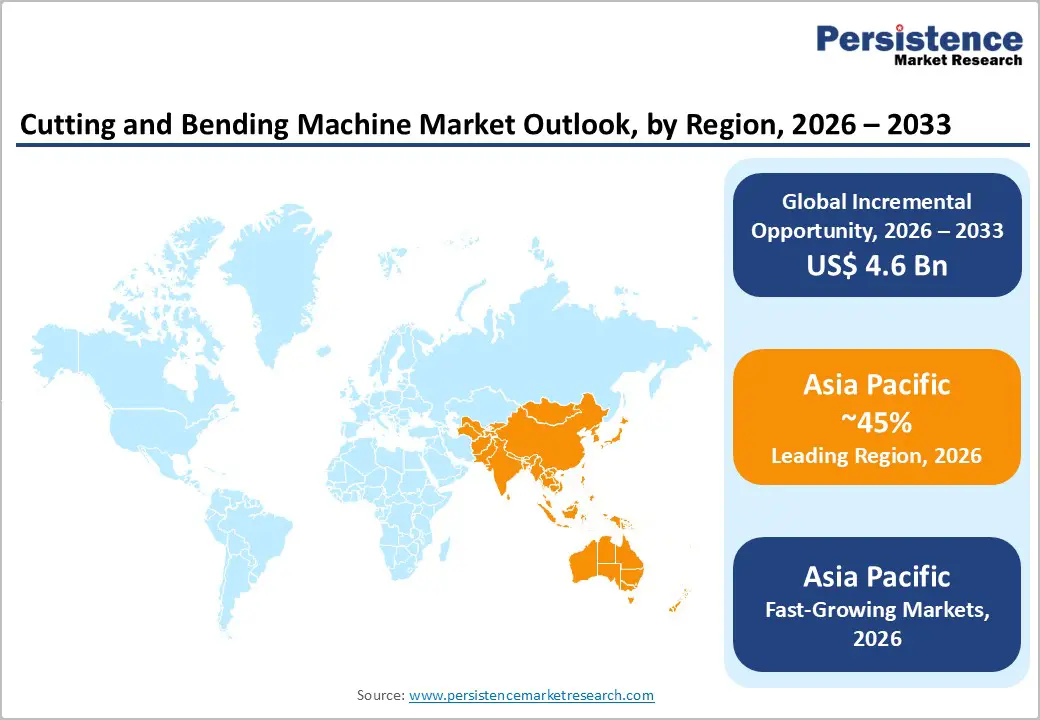

- Leading Region: Asia Pacific dominates the global cutting and bending machine market with over 45% share, driven by China’s massive construction and manufacturing base, India’s infrastructure pipeline, and Japan’s precision-engineering demand.

- Fastest Growing Region: Asia Pacific is also the fastest-growing region, with India and ASEAN nations recording accelerated equipment procurement driven by urbanization, government infrastructure programs, and surging FDI-led manufacturing investments.

- Dominant Segment: CNC Machines lead with approximately 38% market share, as automotive, aerospace, and industrial manufacturers globally prioritize programmable precision, repeatability, and integration with digital manufacturing systems.

- Fastest Growing Segment: AI/Robotics-Integrated Machines are the fastest-growing technology segment, as Industry 4.0 adoption accelerates and manufacturers seek predictive maintenance, adaptive process control, and higher productivity in fabrication operations.

- Key Market Opportunity: The global renewable energy construction wave, wind, solar, and power grid infrastructure, presents a high-value opportunity for OEMs offering specialized heavy-plate cutting and large-radius bending solutions for structural components.

Market Dynamics

Drivers - Global Infrastructure Investment and Construction Activity

Unprecedented global infrastructure spending is the foremost driver of the Cutting and Bending Machine market. Steel-intensive projects, including bridges, highways, metro systems, and commercial real estate, require large volumes of precisely cut and bent rebar, structural sections, and sheet metal components.

The World Bank estimates that developing economies need over US$ 15 trillion in infrastructure investment through 2040 to sustain economic growth. In the United States, the Infrastructure Investment and Jobs Act has committed US$ 1.2 trillion to roads, bridges, rail, and utilities. These projects directly drive procurement of rebar processing machines, stirrup benders, and structural steel cutting systems, sustaining strong demand across the forecast period.

Rising Adoption of CNC and Automation Technologies in Metal Fabrication

The accelerating global transition toward smart manufacturing is a critical growth driver for the market. Manufacturers across automotive, aerospace, and industrial fabrication are replacing conventional machines with CNC-based systems and AI/robotics-integrated machines to achieve higher throughput, reduced material waste, and improved dimensional accuracy.

According to the International Federation of Robotics (IFR), global industrial robot installations exceeded 500,000 units annually as of 2023, signaling broad-based adoption of automation. CNC laser cutting and servo-driven press brakes are gaining rapid traction in sheet metal fabrication, driven by their ability to handle complex geometries with minimal operator intervention, directly expanding the addressable market for advanced cutting and bending equipment manufacturers.

Restraints - High Capital Investment and Long Payback Periods

Fully automatic and CNC-integrated cutting and bending machines carry substantial upfront costs, often ranging from US$ 100,000 to over US$ 1 million per unit for high-end laser cutting centers and large-format press brakes. For small and medium-sized fabricators, who represent a significant share of end-users, such capital requirements present formidable adoption barriers.

The European Commission's SME Barometer consistently highlights access to capital as a primary constraint for manufacturing SMEs. Extended payback periods of 5-10 years further dampen investment appetite, particularly during periods of economic uncertainty, slowing the overall equipment upgrade cycle.

Skilled Workforce Shortage for Advanced Machine Operation

The growing technological complexity of CNC and AI-integrated machines demands a highly skilled operator and maintenance workforce, a resource that is increasingly scarce globally. The Manufacturing Institute in the U.S. estimates that over 2.1 million manufacturing jobs could go unfilled by 2030 due to the skills gap. In developing markets, the lack of trained CNC machine operators limits the penetration of advanced equipment. This workforce constraint acts as a structural brake on market growth, particularly in regions where automated metal fabrication remains nascent.

Opportunities - Expansion of Renewable Energy and Power Infrastructure Projects

The global energy transition is generating massive demand for structural steel and precision metal fabrication, creating a compelling growth opportunity for cutting and bending machine manufacturers. Wind tower manufacturing, solar mounting structures, and power transmission infrastructure all require extensive use of cut and bent metal components produced to tight tolerances.

The International Energy Agency (IEA) projects that annual clean energy investment will exceed US$ 2 trillion globally by 2030. Offshore wind projects in particular demand specialized heavy-plate cutting and large-radius bending capabilities. Machine manufacturers offering tailored solutions for renewable energy component fabrication, including servo-driven bending machines and plasma/laser cutting systems, stand to capture significant new revenue from this rapidly growing end market.

AI Integration and Smart Machine Development for Industry 4.0

The convergence of artificial intelligence, real-time data analytics, and connected manufacturing presents a transformational opportunity for cutting and bending machine OEMs. Smart machines embedded with predictive maintenance algorithms, adaptive process controls, and digital twin capabilities deliver significantly reduced downtime and higher productivity.

According to online sources, manufacturers adopting AI-driven process optimization report productivity gains of 20%. Germany's Platform Industry 4.0 initiative and analogous programs in Japan and South Korea are actively incentivizing smart factory upgrades. OEMs such as TRUMPF Group and Amada Co., Ltd. are already commercializing AI-enhanced laser cutting and press brake systems, signaling a fast-growing market segment that rewards innovation-led suppliers.

Category-wise Analysis

By Machine Type Insights

Among all machine types, cutting machines hold the dominant market position, accounting for approximately 35% of total segment revenue. This leadership reflects cutting operations' fundamental role as the first stage in virtually every metal fabrication workflow. Laser cutting machines, plasma cutters, and waterjet systems have experienced rapid adoption driven by demand for precision, speed, and material versatility.

The Fabricators & Manufacturers Association (FMA) notes that laser cutting adoption among North American fabricators grew by over 40% in the past five years. The expanding sheet metal fabrication and custom fabrication sectors further consolidate the cutting machines segment's market leadership across industrialized and emerging economies alike.

By Automation Level Insights

CNC Machines represent the leading automation level segment, commanding approximately 38% of the market. CNC technology has become the de facto standard in modern metal fabrication, offering programmable precision, repeatability, and the ability to handle complex geometries without operator reconfiguration.

The Association for Manufacturing Technology (AMT) reports that CNC machine tool orders in the U.S. consistently outpace manual and semi-automatic equipment. In automotive and aerospace manufacturing, where tolerances are measured in microns, CNC cutting and bending machines are non-negotiable. Integration of CNC controls with ERP systems for real-time production scheduling is further solidifying this segment's dominance across industrialized markets.

By Technology Insights

CNC-Based Systems dominate the technology landscape with an estimated 42% market share, reflecting decades of investment and standardization in CNC-driven fabrication. CNC technology enables consistent quality across high-volume production runs while reducing reliance on skilled manual labor.

According to the Japan Machine Tool Builders' Association (JMTBA), CNC machine tools account for over 90% of new machine tool shipments in Japan, a benchmark mirrored in Germany and South Korea. While AI/Robotics-Integrated Machines represent the fastest-growing technology segment, CNC-based systems maintain leadership through proven reliability, extensive software ecosystems, and entrenched user familiarity across global manufacturing facilities.

By Application Insights

Rebar processing emerges as the leading application segment, representing approximately 28% of the market. The global construction boom, particularly across Asia Pacific, the Middle East, and Africa, is generating enormous demand for cut-to-length and bent rebar for reinforced concrete structures.

According to the World Steel Association, global steel rebar production has consistently tracked construction investment growth, with output exceeding 300 million tonnes annually. Dedicated rebar processing machines, including stirrup benders, mesh cutting & bending machines, and combined units, are central to modern precast concrete manufacturing and on-site construction, underpinning this segment's sustained leadership.

By End-User Insights

Construction & infrastructure is the dominant end-use sector, accounting for approximately 33% of the cutting and bending machine market. The scale and diversity of construction activity, spanning residential, commercial, and civil infrastructure, creates consistent high-volume demand for rebar cutting, structural steel processing, and sheet metal fabrication equipment.

Government stimulus programs in China, India, the U.S., and across the EU are sustaining elevated steel consumption in construction. The Global Infrastructure Hub (GIH) estimates that global infrastructure investment needs will reach US$ 94 trillion by 2040, providing a long-runway demand environment for machine manufacturers serving the construction sector.

Regional Insights

North America Cutting and Bending Machine Market Trends & Analysis

North America remains a high-value, technology-driven market supported by strong federal investments in infrastructure, clean energy, and advanced manufacturing. Policy frameworks such as the Infrastructure Investment and Jobs Act and Inflation Reduction Act are accelerating demand for precision fabrication equipment. Automation, AI-enabled machining, and reshoring trends continue to push OEM investments, particularly in aerospace, automotive, and heavy construction sectors.

- U.S. Cutting and Bending Machine Market Size

The U.S. dominates the regional market, accounting for approximately USD 3.2 billion in 2026. Growth is driven by strong capital expenditure in metal fabrication, rising adoption of CNC and robotic press brake systems, and increasing domestic manufacturing activity. Demand is particularly robust across automotive, defence, and energy infrastructure applications.

- Europe Cutting and Bending Machine Market Trends, Drivers & Insights

Europe is a mature yet innovation-led market, underpinned by Germany’s engineering leadership and strong intra-EU trade. Regulatory alignment through the EU Machinery Regulation 2023/1230 is enhancing product standardization and market access. Demand is fueled by automotive electrification, aerospace manufacturing, and SME-driven metal fabrication across Southern Europe.

- Germany Cutting and Bending Machine Market Size

Germany leads Europe with an estimated market size of USD 1.6 billion in 2026. Its dominance stems from advanced machine tool manufacturing, strong export orientation, and high adoption of laser cutting and automated bending technologies across industrial sectors.

- U.K. Cutting and Bending Machine Market Size

The U.K. market is projected at around USD 500 million in 2026, supported by aerospace, defense, and infrastructure modernization. Increasing automation in fabrication workshops and government-backed industrial strategies are driving steady equipment upgrades and demand.

- France Cutting and Bending Machine Market Size

France is expected to reach approximately USD 550 million in 2026. Growth is supported by aerospace manufacturing, rail infrastructure projects, and industrial modernization initiatives, alongside rising adoption of precision metal processing technologies.

- Asia Pacific Cutting and Bending Machine Market Drivers & Analysis

Asia Pacific is the largest and fastest-growing regional market, exceeding 45% global share. Rapid industrialization, infrastructure expansion, and strong manufacturing ecosystems drive demand. Government initiatives like China’s 14th Five-Year Plan and India’s National Infrastructure Pipeline are major growth catalysts, alongside increasing adoption of CNC and servo-driven systems.

- China Cutting and Bending Machine Market Size

China dominates globally with an estimated market size of USD 4.2 billion in 2026. Growth is driven by large-scale construction, automotive production, and domestic machine tool manufacturing, supported by strong government backing for advanced equipment adoption.

- India Cutting and Bending Machine Market Size

India’s market is projected at USD 1.5 billion in 2026, fueled by infrastructure expansion, urbanization, and rising steel consumption. Demand for rebar processing and structural fabrication equipment is particularly strong across the construction and energy sectors.

- Japan Cutting and Bending Machine Market Size

Japan’s market is estimated at USD 1.1 billion in 2026. The country focuses on high-precision and technologically advanced systems, with demand driven by the automotive, electronics, and robotics industries, alongside strong exports of advanced cutting and bending machinery.

Competitive Landscape

The global Cutting and Bending Machine market displays a moderately consolidated competitive structure, with multinational OEMs including TRUMPF Group, Amada Co., Ltd., and Bystronic Group controlling significant revenue shares through technology leadership and global distribution. Key differentiators include software integration capabilities, after-sales service networks, and R&D investment in AI and laser source technology.

Emerging business models center on machine-as-a-service (MaaS) offerings, cloud-based remote diagnostics, and digital twin platforms. Regional players, particularly from China and India, are intensifying competition in mid-range segments through aggressive pricing and government-aligned supply strategies.

Key Developments:

- February, 2025: TRUMPF Group unveiled its next-generation TruLaser 5000 series with integrated AI-based process monitoring at EuroBLECH 2025, targeting automotive and aerospace sheet metal customers requiring zero-defect production standards.

- September, 2024: Bystronic Group announced a strategic partnership with a leading robotics integrator to launch fully automated bending cells for high-mix, low-volume production environments, targeting European SME metal fabricators seeking flexible automation.

- March, 2023: TJK Machinery (Tianjin) Co., Ltd. commissioned a new manufacturing facility in Tianjin, China, increasing rebar cutting and bending machine production capacity by 30% to meet surging domestic and export demand.

Companies Covered in Cutting and Bending Machine Market

- Amada Co., Ltd.

- TRUMPF Group

- Bystronic Group

- Prima Industrie S.p.A.

- Salvagnini Group

- HACO Group

- Durmazlar Machinery Inc.

- LVD Group

- Koike Sanso Kogyo Co., Ltd.

- Mazak Corporation

- Mitsubishi Electric Corporation

- Eurobend S.A.

- Schnell S.p.A.

- KRB Machinery

- TJK Machinery (Tianjin) Co., Ltd.

- BLM Group

- Peddinghaus Corporation

- MEP S.p.A.

Frequently Asked Questions

The global Cutting and Bending Machine market is estimated at US$ 9.8 Billion in 2026 and is projected to reach US$ 14.4 Billion by 2033, registering a CAGR of 5.6% during the forecast period. Historically, the market grew at a CAGR of 4.7% from 2020 to 2025, driven by infrastructure expansion and manufacturing automation trends worldwide.

The primary demand drivers are large-scale global infrastructure investment, reinforced by programs such as the U.S. Infrastructure Investment and Jobs Act, and the rapid Industry 4.0-driven adoption of CNC and AI-integrated fabrication technologies. These forces are stimulating both volume demand for rebar and structural steel processing machines and value demand for advanced, high-precision cutting and bending systems.

CNC Machines represent the leading automation level segment with approximately 38% market share. Their dominance stems from widespread adoption in automotive, aerospace, and industrial manufacturing, where programmable precision, repeatability, and integration with digital manufacturing platforms are essential requirements.

Asia Pacific is the largest regional market, accounting for over 45% of global consumption. China leads regional demand through its vast construction and manufacturing ecosystem, followed by India, where the National Infrastructure Pipeline is driving massive steel fabrication equipment procurement, and Japan, which drives demand for high-precision CNC and laser-based systems.

The most significant opportunity is the global renewable energy construction wave, where wind turbine tower manufacturing, solar mounting structure fabrication, and power grid infrastructure demand specialized cutting and bending solutions. The AI-driven smart machine segment, offering predictive maintenance, adaptive process control, and Industry 4.0 connectivity, presents a high-value opportunity for innovation-led OEMs.

Leading companies include Amada Co., Ltd., TRUMPF Group, Bystronic Group, Prima Industrie S.p.A., Salvagnini Group, HACO Group, Durmazlar Machinery Inc., LVD Group, Koike Sanso Kogyo Co., Ltd., Mazak Corporation, Mitsubishi Electric Corporation, Eurobend S.A., Schnell S.p.A., KRB Machinery, and TJK Machinery (Tianjin) Co., Ltd., among others.