- Industrial Goods & Service

- Oil Country Tubular Goods Market

Oil Country Tubular Goods Market Size, Share, and Growth Forecast 2026 - 2033

Oil Country Tubular Goods Market by Product Type (Well Casing, Production Tubing, Drill Pipe, Line Pipe, OCTG Accessories), Manufacturing Process (Seamless, Electric Resistance Welded (ERW), Submerged Arc Welded (SAW)), Material Type (Carbon Steel, Alloy Steel, Stainless Steel, Duplex Steel, Super Duplex Steel), End-User, and Regional Analysis, 2026 - 2033

Oil Country Tubular Goods Market Size and Trend Analysis

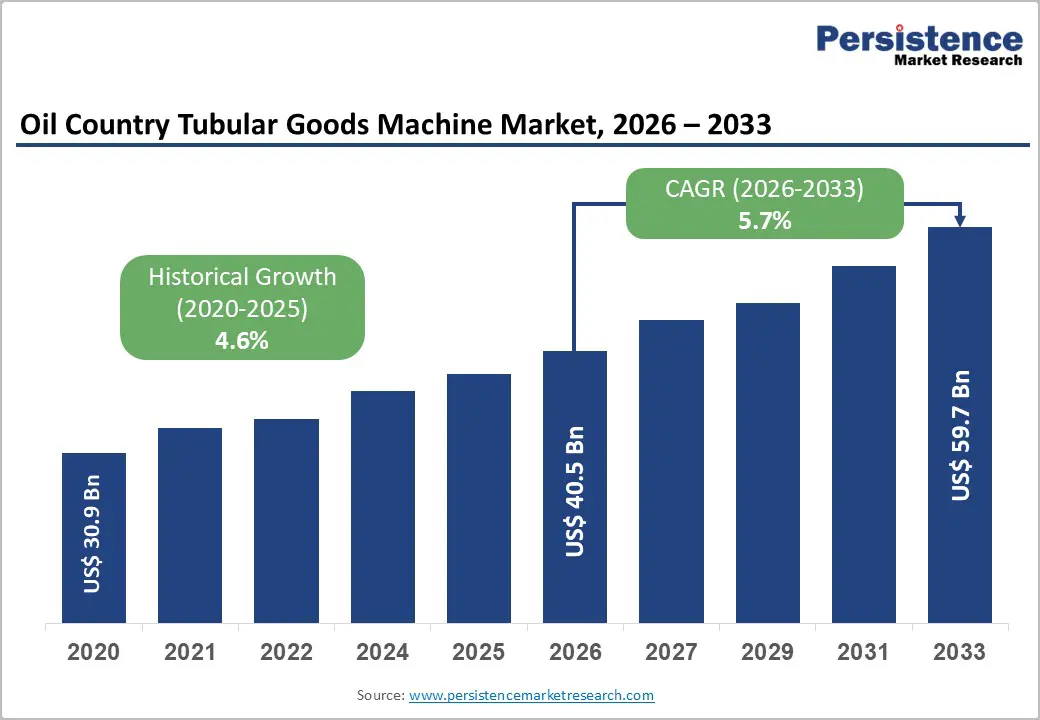

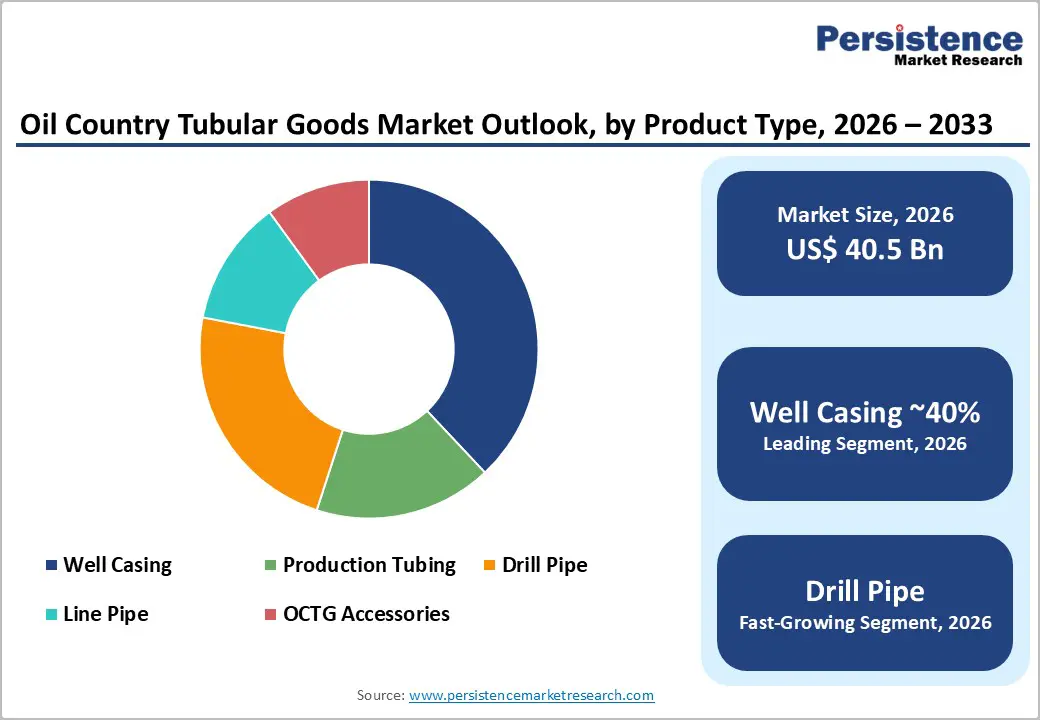

The global oil country tubular goods market size is likely to be valued at US$40.5 billion in 2026 and is expected to reach US$ 59.7 billion by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033.

The OCTG market is expanding at a sustained pace, underpinned by recovering global oil and gas drilling activity, rising deepwater and unconventional resource development, and growing national energy security investments worldwide.

Key Industry Highlights:

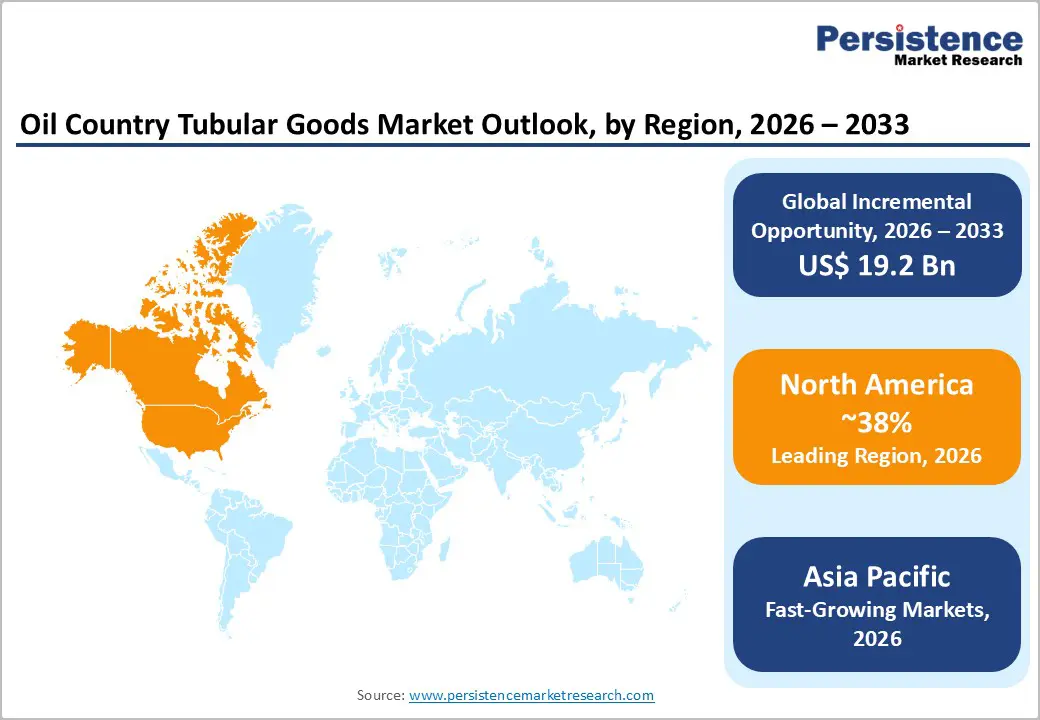

- Leading Region: North America leads the global OCTG market, with a 38% share, driven by the United States' massive shale oil and gas drilling activity in the Permian Basin, Eagle Ford, and other unconventional plays that require high per-well OCTG volumes.

- Fastest Growing Region: Asia Pacific is the fastest-growing OCTG region with a rising CAGR of 6.8%, fueled by China's domestic energy security drilling programs, India's upstream expansion under the HELP policy, and rising offshore activity across ASEAN nations.

- Leading Manufacturing Segment: Seamless OCTG dominates with approximately 55% market share, driven by its superior mechanical performance under high pressure and corrosive well environments, and mandatory specification under API and ISO standards for most critical well applications.

- Fastest Growing Material Type: Duplex and Super Duplex Steel OCTG are the fastest-growing material segments, driven by escalating deepwater, HPHT, and sour-service well environments that demand superior corrosion resistance beyond standard carbon and alloy steel grades.

- Opportunity: Middle East NOC-led multi-year drilling expansion programs, including Saudi Aramco and ADNOC committing over US$ 150 billion in upstream investment, represent the most significant high-volume, high-specification OCTG demand opportunity through 2033.

Market Dynamics

Drivers - Rising Global Upstream Oil & Gas Capital Expenditure

A sustained recovery in global upstream oil and gas investment is the most powerful driver of the OCTG market. After the sharp contraction of 2020, upstream capital expenditure has rebounded decisively, with the International Energy Agency (IEA) reporting that global upstream oil and gas investment recovered to approximately US$ 500 billion in 2023 and continued growth is projected through 2030.

In the United States, the U.S. Energy Information Administration (EIA) reports sustained high rig counts in the Permian Basin and Eagle Ford shale plays. Each new horizontal well drilled in unconventional formations consumes substantially more casing and tubing per foot than conventional wells, creating a multiplier effect on OCTG demand that directly benefits market growth.

Expansion of Deepwater and Ultra-Deepwater Drilling Programs

Deepwater and ultra-deepwater oil exploration is generating premium demand for high-specification OCTG products capable of withstanding extreme pressure, corrosion, and temperature conditions. According to the International Association of Drilling Contractors (IADC), deepwater rig utilization has been trending upward since 2022, with significant new projects sanctioned offshore Brazil, Guyana, West Africa, and the Gulf of Mexico.

Deepwater wells require specialty OCTG grades, including Duplex and Super Duplex Steel tubing, which command significant price premiums over standard carbon steel grades. This structural shift toward technically demanding environments supports both volume growth and value expansion in the OCTG market, particularly benefiting manufacturers with advanced metallurgical capabilities.

Restraints - Volatility in Global Oil Prices and E&P Spending Cycles

The OCTG market remains acutely sensitive to crude oil price volatility, which directly governs exploration and production (E&P) capital allocation. When Brent crude prices fall below the economic threshold for new drilling programs, typically US$ 50-60 per barrel for many operators, rig counts decline rapidly, sharply reducing OCTG procurement.

The U.S. EIA documents multiple such contraction cycles over the past decade. This cyclicality introduces significant revenue unpredictability for OCTG manufacturers and distributors, complicating production planning and inventory management.

Trade Policy Uncertainty and Anti-Dumping Measures

The global OCTG market is significantly shaped by trade policy interventions, particularly in the United States, the world's largest OCTG consumer. The U.S. Department of Commerce has imposed anti-dumping and countervailing duties on OCTG imports from multiple countries, including South Korea, China, and India, disrupting established supply chains. Section 232 steel tariffs further increase material costs for downstream users. These trade barriers create pricing distortions, limit drilling contractors' supply flexibility, and introduce geopolitical risk into long-term procurement strategies across the industry.

Opportunities - Middle East NOC-Led Capacity Expansion Programs

National Oil Companies (NOCs) across the Middle East are executing multi-year drilling and production capacity expansion programs that represent a transformational demand opportunity for OCTG manufacturers. Saudi Aramco has committed to maintaining crude oil production capacity at 12 million barrels per day while simultaneously expanding gas production through its Master Gas System.

Abu Dhabi National Oil Company (ADNOC) has announced over US$ 150 billion in upstream investment through 2027. These programs require enormous volumes of well casing, production tubing, and drill pipe, particularly in premium-connection and corrosion-resistant grades, creating sustained, high-value demand for OCTG suppliers with established NOC relationships and the technical capability to meet exacting specification requirements.

Growth of LNG Infrastructure and Associated Gas Well Development

The global LNG capacity expansion boom is creating significant new demand for OCTG products associated with gas well development and gathering infrastructure. With over 150 million tonnes per annum (MTPA) of new LNG capacity under construction or in advanced planning globally as of 2024.

According to the International Gas Union (IGU), upstream gas well drilling activity is accelerating across Qatar, Australia, the U.S. Gulf Coast, East Africa, and Canada. Gas wells, particularly those targeting high-pressure, high-temperature (HPHT) reservoirs, demand premium OCTG grades, including Alloy Steel and Duplex Steel tubing with premium connections. This creates a sustained, specification-driven revenue opportunity for OCTG manufacturers capable of producing and certifying specialty grades for technically demanding gas applications.

Category-wise Analysis

By Product Type Insights

Well casing is the dominant product type in the OCTG market, accounting for approximately 40% of total revenue. Well casing is required in every wellbore drilled, from surface casing to production casing, making it the highest-volume OCTG product by far. Each well consumes multiple casing strings across different diameters and grade specifications, creating substantial tonnage demand per well.

According to the American Petroleum Institute (API), casing standards cover the broadest range of specifications within OCTG, reflecting its central role in well integrity and pressure containment. The expansion of horizontal drilling in unconventional plays, which uses significantly longer lateral sections of casing, further amplifies per-well consumption and reinforces casing's market-leading position.

By Manufacturing Process Insights

Seamless OCTG products command the largest share of the manufacturing process segment, representing approximately 55% of the market. Seamless tubes are produced without a weld seam, making them significantly stronger under high internal pressure, bending, and torsional loads, critical performance requirements in oil and gas well environments.

The American Petroleum Institute (API) and ISO standards prescribe seamless construction for the majority of high-grade casing and tubing applications, particularly in deepwater, HPHT, and sour service environments. Leading seamless OCTG manufacturers, including Tenaris and Vallourec, have invested heavily in seamless tube manufacturing capacity, reinforcing this segment's market dominance.

By Material Type Insights

Carbon Steel is the dominant material type in the OCTG market, accounting for an estimated 52% of total consumption by volume. Carbon steel OCTG products, spanning standard API grades such as J55, K55, N80, and P110, serve the vast majority of conventional and unconventional well applications where fluid conditions do not require corrosion-resistant alloys.

Their cost-effectiveness, wide availability, and compatibility with standard API threading and connection specifications make carbon steel the default material for the overwhelming majority of global well programs. The World Steel Association confirms that oil country tubular grades remain among the highest-specification carbon steel applications, driving premium pricing relative to commodity steel products.

By End-User Insights

National Oil Companies (NOCs) represent the leading end-user segment in the global OCTG market, accounting for approximately 38% of total consumption. NOCs, including Saudi Aramco, ADNOC, NIOC, Petrobras, and CNPC, control the majority of the world's proven oil and gas reserves and execute the largest drilling programs globally.

According to the IEA, NOCs are responsible for over 50% of global oil production. Their long-term development plans, often spanning decades, provide OCTG manufacturers with predictable, high-volume demand. NOCs also increasingly mandate local content requirements and qualification processes that create barriers to entry and reward established supplier relationships.

Regional Insights

North America Oil Country Tubular Goods Market Trends & Analysis

North America remains the largest OCTG market, driven by high-intensity shale drilling and horizontal well adoption exceeding 85% in the U.S. The Permian Basin dominates activity, while trade protection measures support domestic production. Canada’s oil sands and Mexico’s offshore drilling sustain regional demand growth, with steady replacement and expansion cycles.

- U.S. Oil Country Tubular Goods Market Size

The U.S. OCTG market is estimated at USD 10 billion in 2026, accounting for the majority of North American demand. Strong shale output (over 12 million barrels/day total liquids) and continuous rig activity drive consumption. High-grade seamless pipes and premium connections are increasingly used in deeper, longer horizontal wells.

- Europe Oil Country Tubular Goods Market Trends, Drivers & Insights

Europe’s OCTG market is shaped by energy security priorities and reduced reliance on Russian hydrocarbons. North Sea exploration remains the core demand driver, while EU decarbonization policies create long-term uncertainty. Demand is stable but moderate, supported by offshore drilling, gas storage expansion, and infrastructure upgrades across Western and Eastern Europe.

- Germany Oil Country Tubular Goods Market Size

Germany’s OCTG market is estimated at USD 1.5 billion in 2026, driven mainly by gas storage, pipeline infrastructure, and limited upstream activity. While domestic exploration is modest, industrial demand and energy transition strategies, especially hydrogen-ready infrastructure, support steady consumption of specialized tubular products.

- U.K. Oil Country Tubular Goods Market Size

The U.K. OCTG market is projected at USD 2.5 billion in 2026, supported by continued North Sea exploration and licensing rounds. Offshore investments and well decommissioning activities drive both new demand and replacement cycles, with a strong preference for corrosion-resistant alloys and premium-grade OCTG products.

- France Oil Country Tubular Goods Market Size

France’s OCTG market is relatively smaller, estimated at USD 0.8 billion in 2026. Demand is primarily linked to refining, petrochemical operations, and limited upstream activity. Strategic reserves and energy infrastructure modernization contribute to stable but low-growth consumption of OCTG products.

- Asia Pacific Oil Country Tubular Goods Market Drivers & Analysis

Asia Pacific is the fastest-growing OCTG market, driven by rising energy demand and increased domestic exploration. China and India lead upstream investments, while Southeast Asia expands offshore drilling. Government policies supporting energy independence and deepwater exploration are accelerating demand for both standard and premium OCTG products.

- China Oil Country Tubular Goods Market Size

China’s OCTG market is estimated at USD 11 billion in 2026, supported by large-scale drilling programs led by national oil companies. Increasing focus on unconventional resources and deep wells is driving demand for high-performance tubular goods, while domestic manufacturers dominate supply.

- India Oil Country Tubular Goods Market Size

India’s OCTG market is projected at USD 3.4 billion in 2026, fueled by upstream expansion under HELP policies. Deepwater exploration in the Krishna-Godavari Basin and increased rig activity are key drivers. Domestic manufacturing capabilities are improving, reducing import dependence and supporting long-term growth.

- Japan Oil Country Tubular Goods Market Size

Japan’s OCTG market is estimated at USD 1.3 billion in 2026, characterized by limited upstream activity but strong demand for high-specification tubular products. The country focuses on advanced materials and exports, with demand linked to overseas energy investments and technological leadership in premium OCTG manufacturing.

Competitive Landscape

The global OCTG market is moderately consolidated, with a small number of vertically integrated global manufacturers, led by Tenaris, TMK Group, and Vallourec, commanding disproportionate revenue shares through proprietary premium connection technology, global manufacturing footprints, and NOC qualification advantages.

Key differentiators include metallurgical expertise, premium threading technology, and integrated service capabilities. Emerging business models encompass tubular management services, digital inspection platforms, and supply-chain-as-a-service offerings. Regional manufacturers in China, India, and South Korea compete aggressively on price in standard API-grade segments, intensifying margin pressure on tier-one players in volume markets.

Key Developments:

- January, 2025: Tenaris announced the expansion of its premium connection manufacturing capacity at its Veracruz, Mexico facility, targeting increased supply of high-specification OCTG products to deepwater operators in the Gulf of Mexico and offshore Brazil.

- August, 2024: Vallourec completed the commissioning of its new green steel-based seamless tube production line in Brazil, reducing carbon emissions by approximately 40% per tonne compared to conventional blast furnace-based production.

- March, 2023: TMK Group signed a long-term OCTG supply agreement with a major Middle Eastern NOC for the delivery of premium-grade casing and tubing products, reinforcing its strategic position in the region's expanding upstream market.

Companies Covered in Oil Country Tubular Goods Market

- Tenaris

- TMK Group

- Vallourec

- Nippon Steel Corporation

- United States Steel Corporation

- National Oilwell Varco

- ArcelorMittal

- JFE Steel Corporation

- Sumitomo Corporation

- ILJIN Steel Co., Ltd.

- Sandvik AB

- Jindal SAW Ltd.

- Tianjin Pipe Corporation (TPCO)

- SeAH Steel Corporation

- ChelPipe Group

- Evraz plc

- ISMT Limited

- Northwest Pipe Company

Frequently Asked Questions

The global Oil Country Tubular Goods (OCTG) market is estimated at US$ 40.5 Billion in 2026 and is projected to grow to US$ 59.7 Billion by 2033, at a CAGR of 5.7% during the forecast period. Historically, the market expanded at a CAGR of 4.6% from 2020 to 2025, supported by recovering upstream oil and gas investment following the pandemic-era downturn.

The primary growth drivers are the sustained recovery in global upstream oil and gas capital expenditure, with IEA-tracked investment approaching US$ 500 billion annually, and the expansion of deepwater and unconventional drilling programs. Horizontal drilling in U.S. shale plays, Middle East NOC capacity expansions, and global LNG development are all generating intensified demand for high-specification OCTG products.

Well Casing is the dominant product type, accounting for approximately 40% of total OCTG market revenue. Casing is required in every well drilled across multiple strings and diameters, making it the highest-volume OCTG product. The expansion of horizontal drilling in unconventional plays further amplifies casing consumption per wellbore, cementing this segment's leading market position.

North America, led by the United States, is the world's largest OCTG market. The U.S. shale industry, centered on the Permian Basin, Eagle Ford, and Haynesville plays, drives enormous volumes of casing and tubing demand. Horizontal wells now account for over 85% of new U.S. wells drilled, each consuming far more OCTG than conventional vertical wells.

The most significant opportunities lie in supplying Middle East NOC-led drilling expansion programs, including Saudi Aramco and ADNOC's combined upstream investment exceeding US$ 150 billion, and in developing premium-grade OCTG for deepwater, HPHT, and LNG-associated gas well applications where technical specifications command significant price premiums over commodity grades.

Leading companies in the global OCTG market include Tenaris, TMK Group, Vallourec, Nippon Steel Corporation, United States Steel Corporation, National Oilwell Varco, ArcelorMittal, JFE Steel Corporation, Sumitomo Corporation, ILJIN Steel Co., Ltd., Sandvik AB, Jindal SAW Ltd., Tianjin Pipe Corporation (TPCO), SeAH Steel Corporation, and ChelPipe Group, among others.