- Industrial Goods & Service

- Artificial Lift Systems Market

Artificial Lift Systems Market Size, Share, and Growth Forecast 2026 - 2033

Artificial Lift Systems Market by Product Type (Rod Lift Systems, Electric Submersible Pumps (ESP), Progressive Cavity Pumps (PCP), Gas Lift Systems, Hydraulic Pump Systems, Plunger Lift Systems, Jet Pumps), by Technology (Conventional Systems, Smart / Digital Systems), Component (Pumps, Motors, Cables, Controllers, Drive Heads, Separators, Gas Lift Valves, Sucker Rods), End-user, and Regional Analysis, 2026 - 2033

Artificial Lift Systems Market Size and Trend Analysis

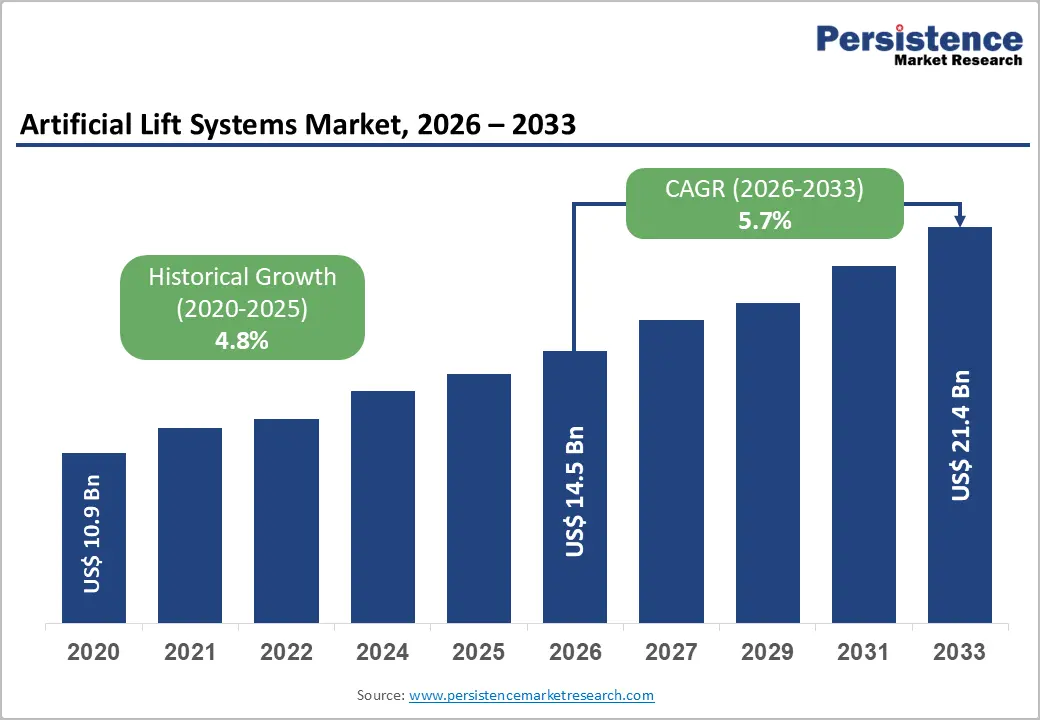

The global Artificial Lift Systems market size is likely to reach US$14.5 billion in 2026 and US$21.4 billion by 2033, growing at a CAGR of 5.7% over the forecast period from 2026 to 2033. Rising global energy demand and the progressive depletion of natural reservoir pressure in mature oil fields are the primary catalysts propelling market expansion.

Key Industry Highlights:

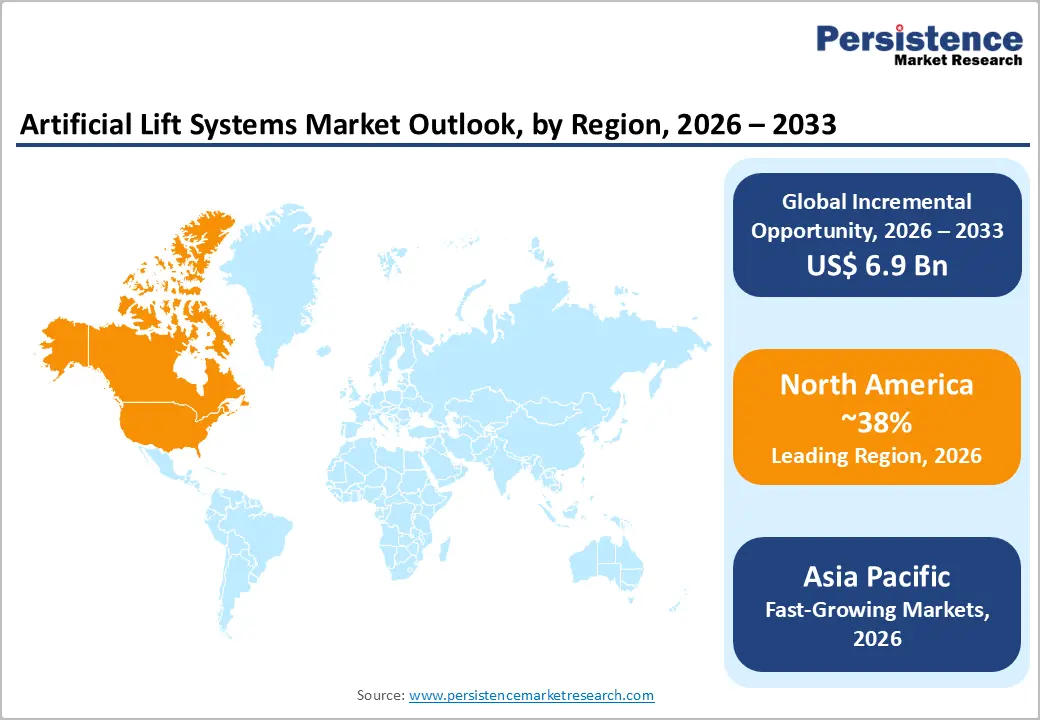

- Leading Region: North America leads the global artificial lift systems market, holding 38% share, driven by prolific shale production in the Permian Basin and Eagle Ford. The U.S. generates approximately 13.2 million barrels per day, supported by widespread artificial lift deployment.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with a rising CAGR of 6.8%, propelled by increasing artificial lift deployments in China's aging Daqing and Shengli oilfields, India's offshore assets managed by ONGC, and expanding unconventional resource programs across Southeast Asia.

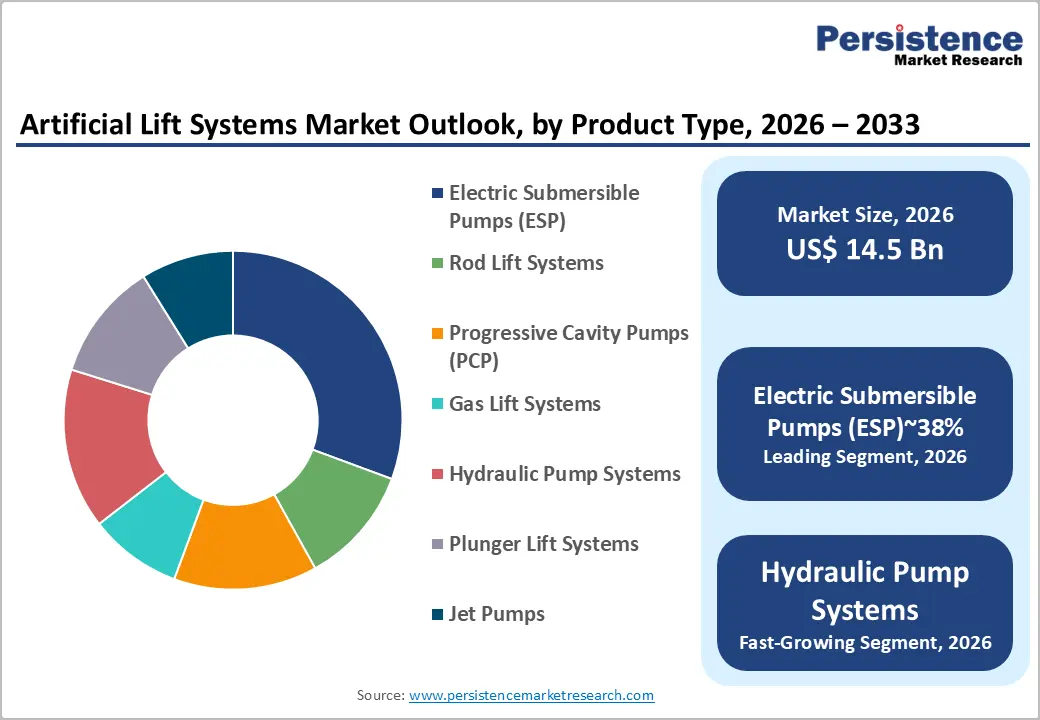

- Dominant Segment: Electric Submersible Pumps (ESPs) dominate the market by product type with approximately 38% revenue share, favored for high-volume offshore and horizontal well applications across deepwater Gulf of Mexico and Middle East operations.

- Fastest Growing Segment: Smart/Digital artificial lift systems represent the fastest-growing technology segment, with adoption accelerating as operators integrate AI analytics and IIoT sensors to reduce non-productive time and optimize production efficiency across major basins.

- Key Market Opportunity: The Middle East and Latin America offer compelling near-term growth potential, backed by ADNOC's 5 million bpd capacity target and Petrobras' US$78 billion capex plan, driving sustained demand for advanced ESP and gas-lift system solutions.

Market Dynamics

Drivers - Rising Production from Mature and Depleted Oil Fields

As global oil reservoirs age, natural reservoir pressure declines, making artificial lift systems essential for sustaining commercial production rates. According to the U.S. Energy Information Administration (EIA), approximately 70% of U.S. oil production in the Permian Basin and other major shale plays relies on Electric Submersible Pumps (ESPs) and rod lift systems.

The IEA projects that global oil demand will remain above 100 million barrels per day through 2030, necessitating sustained investment in production-enhancing technologies. As operators increasingly focus on maximizing the economic life of existing wells rather than embarking on expensive new drilling campaigns, artificial lift adoption is expected to accelerate, creating robust and recurring demand across both established basins and emerging production regions worldwide.

Expansion of Unconventional Resource Development

The rapid growth of unconventional resource extraction, including shale oil, tight gas, and coalbed methane, has significantly amplified demand for specialized artificial lift solutions. The U.S. EIA reported that tight oil production accounted for nearly 65% of total U.S. crude output in 2023, with horizontal wells requiring artificial lift from early stages of production.

In the Permian Basin, more than 95% of producing wells employ some form of artificial lift. Similarly, growing unconventional activity in Argentina's Vaca Muerta shale and Canada's oil sands is driving additional deployments of lift technology. Progressive Cavity Pumps (PCPs) and ESPs have emerged as preferred solutions for high-viscosity and high-sand-cut environments characteristic of unconventional plays worldwide.

Restraints - High Capital and Operational Expenditure

The installation and maintenance of advanced artificial lift systems represent a substantial financial burden, particularly during periods of oil price volatility. ESP installations, for example, can cost between US$150,000 and US$500,000 per well, excluding ongoing maintenance and replacement costs.

When crude oil prices dip below US$50 per barrel, many operators curtail capital expenditure on lift system upgrades, thereby dampening market demand. Additionally, ESP systems face elevated failure rates in extreme downhole environments, with mean times between failures (MTBF) often ranging from 12 to 24 months, adding to the total cost of ownership and creating operational uncertainty for smaller producers.

Skilled Labor Shortage and Technical Complexity

The operation and maintenance of artificial lift systems, particularly smart digital and ESP configurations, require highly skilled engineers with specialized expertise. A study by the Society of Petroleum Engineers (SPE) highlighted that the oil and gas industry faces a critical shortage of experienced artificial lift engineers, partly attributable to workforce attrition during the COVID-19 downturn and a growing generational skills gap. This talent deficit increases dependence on costly third-party service providers and delays system optimization, directly impacting production uptime and operational efficiency for operators globally.

Opportunities - Adoption of Smart and Digital Artificial Lift Systems

The transition toward smart, digitally enabled artificial lift technologies presents a compelling growth opportunity for market participants. Integration of Industrial Internet of Things (IIoT) sensors, real-time monitoring, and artificial intelligence (AI)-driven analytics enables operators to optimize pump performance, predict failures before they occur, and reduce non-productive time substantially. Baker Hughes Company's Leucipa automated field production solution, expanded through 2024, exemplifies growing operator appetite for data-driven lift optimization.

According to the U.S. Department of Energy (DOE), digital oilfield technologies can reduce operational costs by up to 25% and improve production efficiency by up to 20%. As operators seek to extract more value from existing asset bases with fewer resources, the smart artificial lift segment is poised for accelerated adoption, particularly in North America and the Middle East, where digital transformation programs are well-funded and strategically prioritized.

Growing Demand in the Middle East and Latin America

Significant near-term opportunities exist in the Middle East and Latin America, where national oil companies are ramping up output to meet sustained global energy demand. Saudi Aramco's production expansion programs and Abu Dhabi National Oil Company's (ADNOC) 2030 capacity target of 5 million barrels per day are expected to drive substantial investment in artificial lift infrastructure across the region.

In Latin America, Brazil's Petrobras has outlined capital expenditure plans exceeding US$ 78 billion through 2028, with a meaningful portion earmarked for pre-salt and mature field production optimization using advanced lift technologies. These regional investment programs create fertile ground for ESP, gas lift, and smart lift system providers to establish long-term supply agreements and service contracts beyond traditional North American markets.

Category-wise Analysis

By Product Type Insights

Electric Submersible Pumps (ESPs) dominate the artificial lift systems market by product type, accounting for approximately 38% of total market revenue. This leadership is driven by the technology's proven ability to handle high fluid volumes and deep-well applications, making it the preferred choice across both conventional and unconventional oil fields. ESPs are particularly dominant in offshore production environments, where subsea completions demand reliable, high-capacity lift solutions.

According to the American Petroleum Institute (API), ESP deployments have grown steadily across deepwater Gulf of Mexico operations, with operators increasingly favoring variable-speed drive-equipped systems for precise flow rate control. The technology's adaptability to high-temperature, high-pressure downhole conditions and its compatibility with smart monitoring solutions further reinforce its commanding market position and continued demand across global producing regions.

By Technology Insights

Conventional systems currently hold the largest share in the artificial lift systems market by technology, accounting for approximately 62% of total market value. Standard rod pump units, fixed-speed ESPs, and conventional gas lift installations remain dominant due to lower upfront capital costs, well-established maintenance protocols, and widespread availability of replacement parts and skilled technicians. In mature producing regions such as the Middle East and parts of Asia Pacific, conventional lift systems form the backbone of field operations.

However, Smart / digital systems are gaining share rapidly, particularly in North America, where operators are retrofitting existing installations with IIoT-enabled sensors and AI-driven controllers to enhance efficiency without complete system overhauls, reflecting a broader industry trend toward incremental digitalization of upstream assets.

Component Insights

Pumps are the leading component segment in the artificial lift systems market, accounting for approximately 34% of component-level revenue. Pumps are the core functional element across virtually all artificial lift configurations, whether ESPs for deepwater and horizontal wells, Progressive Cavity Pumps for heavy oil and sand-laden production, or reciprocating pumps in rod lift systems.

The demand for high-efficiency, wear-resistant pump designs is intensifying as operators pursue longer run-life intervals in challenging downhole environments characterized by high temperatures, corrosive fluids, and abrasive solids. Manufacturers such as Halliburton Company and Baker Hughes Company have introduced advanced pump metallurgies and protective coating technologies to address these challenges, driving replacement and upgrade cycles within this segment.

End-user Insights

Oil production remains the dominant end-use segment for artificial lift systems, capturing approximately 68% of total market demand. This dominance is rooted in the fundamental role of artificial lift in maintaining commercial production rates from mature and declining oil reservoirs worldwide.

The U.S. EIA has reported that over 80% of currently producing oil wells in the United States operate below their natural flow capacity, making continuous lift support a pervasive operational requirement. In the Middle East and Africa, major producers such as Saudi Aramco and ADNOC are investing heavily in upgrading lift systems to maximize recovery from existing reservoirs. Natural gas production and unconventional resources are growing end-use contributors but remain secondary to the oil production segment in overall demand share.

Regional Insights

North America Artificial Lift Systems Trends

North America leads the global artificial lift systems market, driven primarily by prolific shale oil and gas activity in the United States. The Permian Basin, Eagle Ford, and Bakken formations represent the epicenter of artificial lift demand, where horizontal drilling and multi-stage fracturing necessitate early-stage lift adoption across virtually every new well. The U.S. Energy Information Administration (EIA) reported that U.S. crude oil production reached approximately 13.2 million barrels per day in 2023, with artificial lift systems playing a critical supporting role across this output. Regulatory oversight by the Bureau of Land Management (BLM) and state-level agencies promotes operational standards that favor advanced, efficient lift technologies.

Canada contributes meaningfully to regional market dynamics through oil sands operations in Alberta, where Progressive Cavity Pumps (PCPs) are extensively deployed for heavy oil extraction. The Canada's Oil Sands Innovation Alliance (COSIA) has championed technology development to enhance lift efficiency in high-viscosity, sand-laden applications, further supporting domestic demand for specialized artificial lift solutions. Innovation ecosystems in Houston, Texas, and Calgary continue to host significant R&D investments from major oilfield service companies aimed at advancing smart lift technologies.

Europe Artificial Lift Systems Trends

Europe's artificial lift systems market is shaped predominantly by mature producing regions in the North Sea, where operators in the United Kingdom and Norway continue to invest in life-extension technologies for aging offshore fields. The U.K. North Sea Transition Authority (NSTA) reported that over 60% of producing fields in the UK Continental Shelf (UKCS) have been in production for more than 25 years, creating a sustained aftermarket for lift system upgrades. Germany and the Netherlands contribute through onshore production activities, though at a significantly smaller scale compared to North Sea offshore output.

Regulatory harmonization under the European Union's energy efficiency and emissions reduction directives is encouraging operators to transition to smart artificial lift systems with lower carbon footprints and improved energy efficiency profiles. France and Spain, while not major hydrocarbon producers, host significant engineering and manufacturing hubs that supply the artificial lift component chain, supporting the region's overall industrial footprint in this market.

Asia Pacific Artificial Lift Systems Trends

Asia Pacific represents the fastest-growing regional market for artificial lift systems, underpinned by expanding oil and gas activities across China, India, Indonesia, and Malaysia.

China National Petroleum Corporation (CNPC) and China Petroleum & Chemical Corporation (Sinopec) are scaling up artificial lift deployments in aging onshore oilfields, including Daqing and Shengli, to arrest production declines. China's National Energy Administration data indicates that annual production from the Daqing oilfield has been sustained above 30 million tonnes with artificial lift playing a critical role in maintaining that output level.

India's Oil and Natural Gas Corporation (ONGC) has ramped up investments in lift systems for the Mumbai High and western offshore fields, while Southeast Asian markets, led by Malaysia's Petronas and Indonesia's Pertamina, are deploying ESP and gas-lift technologies to sustain output from mature offshore assets. The region's growing domestic manufacturing capabilities, particularly in China, also provide cost-competitive conventional lift components, enabling broader market penetration in price-sensitive production environments across the ASEAN region.

Competitive Landscape

The global artificial lift systems market exhibits a moderately consolidated structure, with Halliburton Company, Schlumberger Limited (SLB), Baker Hughes Company, and Weatherford International plc commanding significant share through integrated service offerings and extensive global deployment networks. These industry majors compete alongside specialized mid-tier players such as ChampionX Corporation, NOV Inc., and Borets International Limited.

Key competitive differentiators include technological innovation in smart lift solutions, geographic service network depth, supply chain reliability, and total cost of ownership optimization. An emerging trend is the shift toward digital service models, where companies offer performance-based contracts tied directly to production outcomes rather than equipment sales, reflecting a broader industry evolution toward outcome-driven oilfield services.

Key Developments:

- March 2024: Baker Hughes Company expanded its Artificial Lift portfolio with next-generation Variable Speed Drive (VSD) ESPs engineered for ultra-deep and high-temperature applications, specifically targeting deepwater Gulf of Mexico production operations.

- November 2024: Weatherford International plc announced a strategic partnership with a leading IIoT platform provider to integrate AI-driven predictive analytics into its rod lift and ESP monitoring services, enhancing real-time production optimization for operators globally.

- January 2025: Halliburton Company launched an enhanced Progressive Cavity Pump (PCP) system featuring advanced elastomer technology, specifically engineered for high sand-cut and high-temperature unconventional well environments in the Permian Basin.

Companies Covered in Artificial Lift Systems Market

- Halliburton Company

- Schlumberger Limited (SLB)

- Baker Hughes Company

- Weatherford International plc

- NOV Inc.

- ChampionX Corporation

- Borets International Limited

- Dover Corporation

- Lufkin Industries

- Tenaris S.A.

- Novomet

- JJ Tech

- AccessESP

- Alkhorayef Petroleum Company

- Canadian Advanced ESP Inc.

- Flowco Production Solutions

- Apergy

- GE Vernova

Frequently Asked Questions

The global Artificial Lift Systems market is valued at approximately US$ 14.5 Billion in 2026 and is projected to reach US$ 21.4 Billion by 2033, expanding at a CAGR of 5.7% over the forecast period. Historically, the market grew at a CAGR of 4.8% between 2020 and 2025, driven by sustained oil field development activity and rising demand for production-enhancement technologies.

The market is primarily driven by rising production from mature and depleted oil reservoirs where natural pressure is insufficient to sustain commercial flow rates. Accelerating unconventional resource development, especially shale oil in the United States, further amplifies demand. The U.S. Energy Information Administration (EIA) estimates that over 70% of Permian Basin production relies on artificial lift, underscoring its indispensable role in global upstream operations.

Electric Submersible Pumps (ESPs) hold the leading share in the Artificial Lift Systems market by product type, accounting for approximately 38% of total revenue. Their dominance is attributed to superior performance in high-volume, deepwater, and horizontal well applications, including widespread deployment across the Gulf of Mexico and Middle East offshore fields, where they offer reliable lift capacity under demanding downhole conditions.

North America is the leading region in the global Artificial Lift Systems market, driven by the extensive shale oil and gas activity in the United States, particularly in the Permian Basin, Eagle Ford, and Bakken formations. With U.S. crude oil production reaching approximately 13.2 million barrels per day in 2023, the region represents the single largest demand hub for artificial lift technologies globally, supported by a strong innovation ecosystem and favorable regulatory frameworks.

Key growth opportunities lie in the rapid adoption of smart and digital artificial lift systems, integrating IIoT sensors, AI-driven analytics, and real-time monitoring, which can reduce operational costs by up to 25% and boost production efficiency by 20% according to the U.S. Department of Energy (DOE). Additionally, national oil company expansion programs in the Middle East and Latin America, including ADNOC's 5 million bpd capacity target and Petrobras' US$ 78 billion capex plan, offer compelling long-term growth avenues for market participants.

Key market players include Halliburton Company, Schlumberger Limited (SLB), Baker Hughes Company, Weatherford International plc, NOV Inc., ChampionX Corporation, Borets International Limited, Dover Corporation, Lufkin Industries, Tenaris S.A., Novomet, JJ Tech, AccessESP, Alkhorayef Petroleum Company, and Canadian Advanced ESP Inc., among other regional and specialized providers.