- Industrial Goods & Service

- Autonomous Forklift Market

Autonomous Forklift Market Size, Share, and Growth Forecast 2026 - 2033

Autonomous Forklift Market by Product Type (Pallet Jack / Pallet Truck, Counterbalance Forklift, Reach Truck, Pallet Stacker, Order Picker, Misc.), By Navigation Technology (LiDAR / Laser Guidance, SLAM / Hybrid Navigation, Vision-Based Navigation, Magnetic Guidance), Application (Warehousing & Storage, Manufacturing (In-Plant Material Handling), Logistics & Distribution Centers, E-commerce Fulfillment Centers, Cold Storage), Industry, and Regional Analysis, 2026 - 2033

Autonomous Forklift Market Size and Trend Analysis

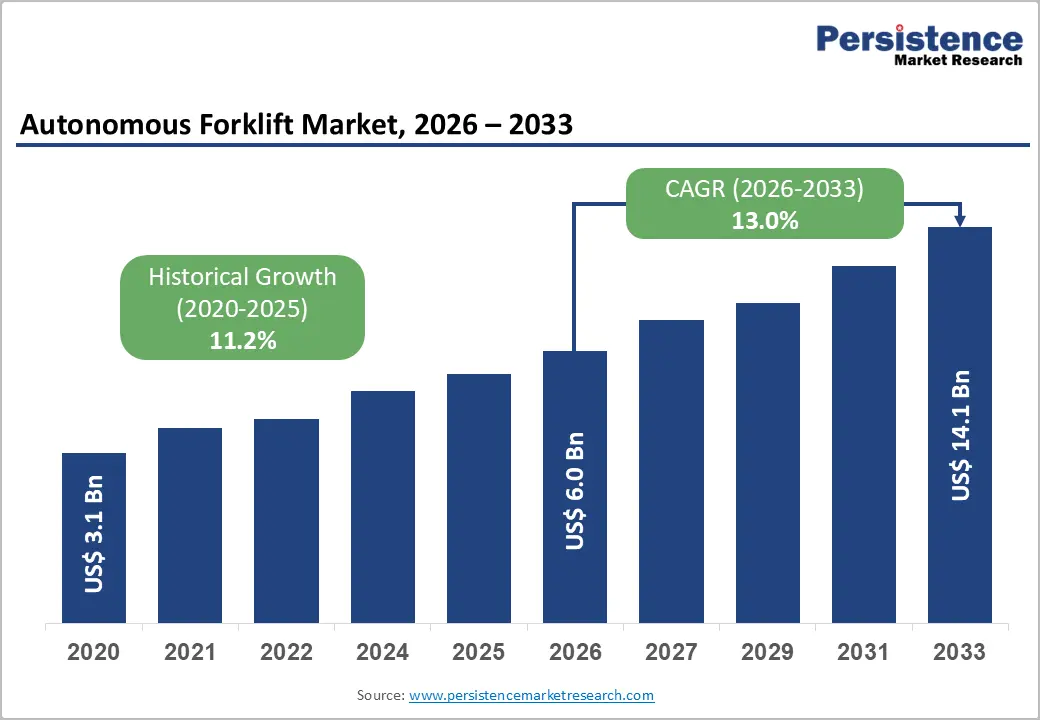

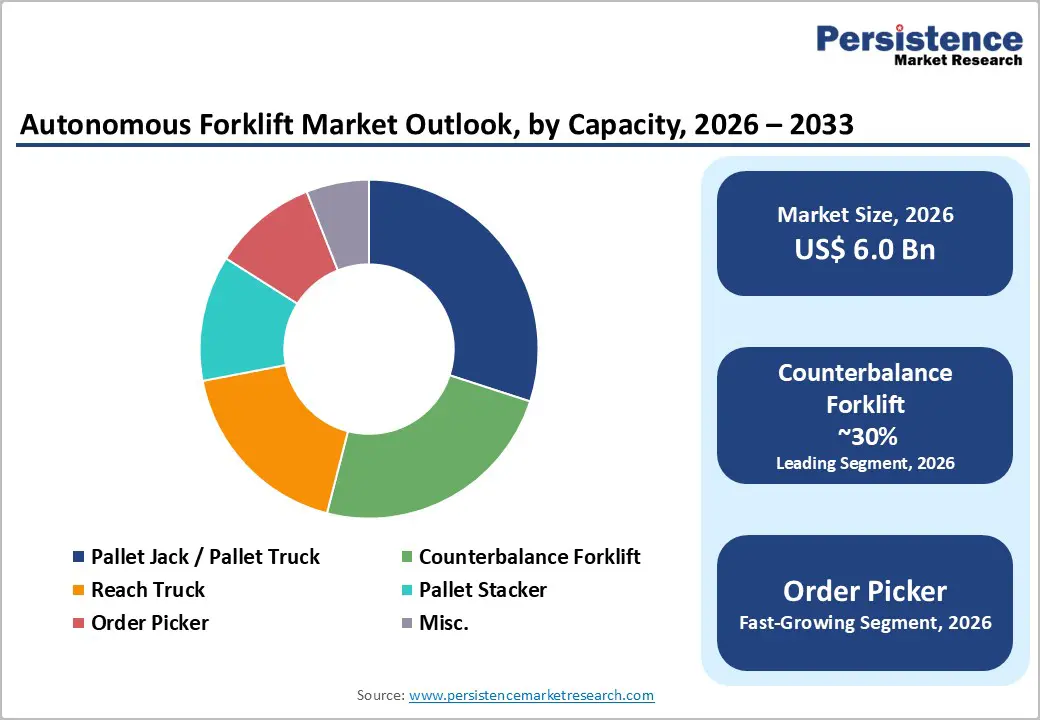

The global autonomous forklift market size is likely to be valued at US$ 6.0 billion in 2026 and is projected to reach US$ 14.1 billion by 2033, growing at a CAGR of 13.0% between 2026 and 2033. The market recorded a historical value of US$ 3.1 Bn in 2020, reflecting an impressive historical CAGR of 11.2%, underscoring a decade-long structural shift toward warehouse and logistics automation.

The primary growth momentum is anchored by accelerating labor shortages in warehousing, rapid e-commerce fulfillment infrastructure buildout, and aggressive Industry 4.0 adoption across manufacturing and logistics sectors globally.

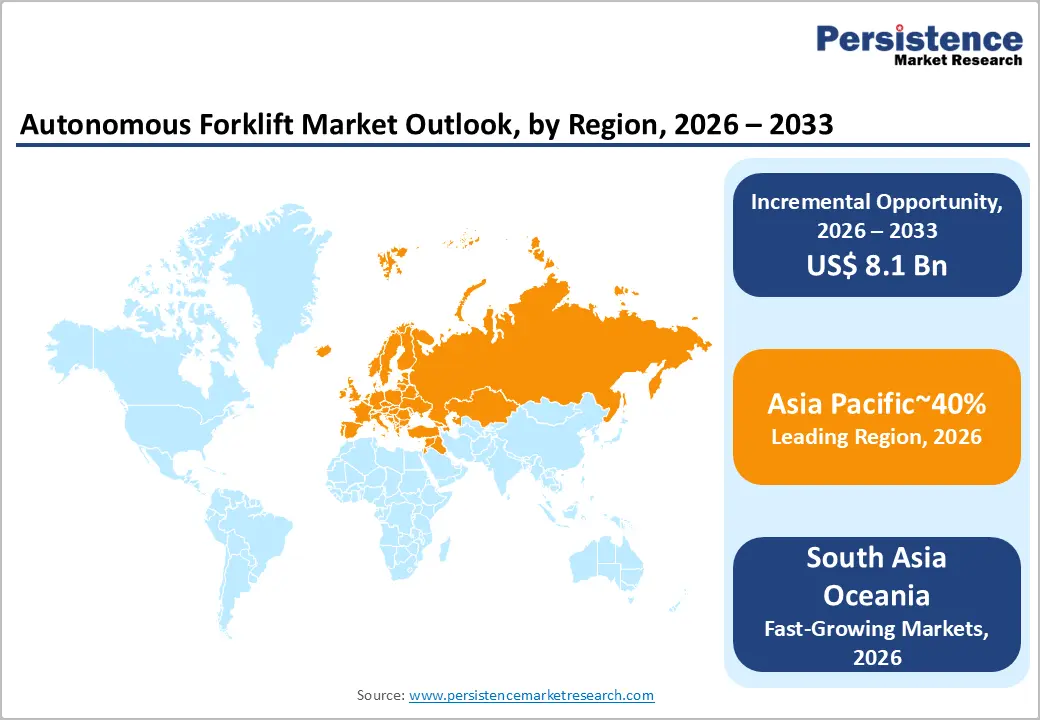

The convergence of AI-powered navigation systems, real-time fleet management software, and declining hardware costs is making autonomous forklifts increasingly viable across both large enterprises and mid-sized operations. Asia Pacific leads regional demand, commanding approximately 40% of global market share, while North America contributes around 32%, collectively representing over 70% of total market revenue.

Key Market Highlights

- Leading Region: Asia Pacific dominates with 40% share, driven by large-scale warehouse automation in China and rapid logistics modernization in India.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, supported by policy-driven logistics upgrades, expanding e-commerce infrastructure, and rising 3PL demand.

- Leading Application: Warehousing & Storage leads with 32% share, driven by standardized environments and large-scale deployment of automated material handling systems.

- Leading Product Type: Counterbalance Forklifts hold 30% share, supported by their versatility across manufacturing and heavy-duty logistics operations.

- Leading Technology: LiDAR / Laser Guidance dominates with 39% share, driven by high accuracy and widespread adoption in industrial environments.

- Key Growth Indicator: Structural labor shortages and rising warehouse workforce deficits are accelerating adoption of autonomous forklifts for cost reduction and 24/7 operations.

- Key Opportunity: Subscription-based and flexible financing models, along with emerging market logistics modernization, are expanding adoption across mid-sized enterprises and greenfield facilities.

Market Dynamics

DRO Analysis - Structural Labor Shortages and Warehouse Workforce Deficit Accelerating Automation Adoption

The persistent global shortage of qualified warehouse and material labor has emerged as one of the most powerful structural forces propelling the Autonomous Forklift Market. Across the United States, Europe, and Asia Pacific, warehousing and logistics operators face chronic staffing gaps that conventional hiring pipelines cannot bridge.

In the United States, food and beverage manufacturing alone employed approximately 1.7 million workers in 2021, representing 15.4% of total manufacturing employment, yet operators continue to report persistent unfilled forklift operator positions due to high attrition and safety compliance requirements. In India, the logistics sector employs over 22 million people and contributes approximately 14.4% to GDP yet faces severe productivity gaps, making automation not a luxury but an operational necessity.

Autonomous forklifts directly address this gap by operating 24/7 without fatigue, eliminating human error, and reducing total labor costs by 30-50% over a 5-year deployment horizon. The structural nature of this workforce deficit, driven by aging demographics in developed economies and skills mismatches in emerging ones, ensures that autonomous forklift adoption will remain a high-priority capital investment across industries ranging from food processing to automotive assembly.

Explosive E-Commerce and B2B Digital Trade Infrastructure Demanding Automated Fulfillment

The structural transformation of global commerce toward digital procurement channels is generating unprecedented demand for automated material handling within fulfillment and distribution infrastructure. The global B2B eCommerce Gross Merchandise Value expanded from US$ 9,837 billion in 2017 to a projected US$ 36,163 billion by 2026, reflecting a 14.5% CAGR, a scale of digital trade volume that simply cannot be processed efficiently with manual forklift operations.

India's industrial and warehousing leasing activity reached a record 39.5 million sq. ft. in 2024, with third-party logistics providers accounting for 41% of total leasing demand and e-commerce firms driving 25% of warehouse leasing in H1 2025 alone, according to CBRE. In parallel, India's e-commerce market, valued at approximately US$ 125 billion in 2024, is projected to reach US$ 345 billion by 2030, requiring proportional expansion in automated storage, retrieval, and transport solutions. The Autonomous Forklift Market directly benefits as fulfillment center operators deploy autonomous pallet jacks, reach trucks, and counterbalance forklifts to meet same-day and next-day delivery commitments at scale, without proportionally scaling headcount.

Industry 4.0 Integration and IoT-Enabled Smart Warehouse Ecosystems

The widespread adoption of Industry 4.0 principles, encompassing IoT connectivity, digital twins, AI-driven decision-making, and real-time data analytics, is fundamentally reshaping warehouse and manufacturing floor operations, creating a fertile environment for the autonomous forklift market.

Based on Eurostat data extracted in July 2025, approximately 70% of EU citizens aged 16 to 74 reported using at least one internet-connected device in 2024, and IoT adoption in large European enterprises stands at 56% versus 26% in small enterprises, with large firms leading in condition-based maintenance (44%) and production process automation (36%). These enterprise IoT deployments create the sensor, connectivity, and data infrastructure that autonomous forklifts require for safe navigation, fleet coordination, and warehouse management system integration.

In December 2024, KION Group advanced simulation-based autonomous forklift training in collaboration with Leibniz University Hanover and IPH Hanover, using imitation learning and real-time data a clear demonstration of how IoT and AI convergence is transitioning autonomous forklifts from rigid, path-fixed systems toward adaptive, intelligence-driven intralogistics solutions that can operate in complex, dynamic environments.

Market Restraints

High Capital Expenditure and Complex Integration Costs

The significant upfront investment required for autonomous forklift deployment, including hardware, navigation infrastructure, software licensing, and facility retrofitting, remains a critical adoption barrier, particularly for small and medium-sized enterprises. Integration with existing Warehouse Management Systems (WMS) and Enterprise Resource Planning (ERP) platforms adds further technical complexity and cost.

Facilities often require physical modifications, such as reflector installations, floor markings, or zone delineation, which extend payback periods beyond 3 to 5 years. This cost barrier disproportionately limits adoption in fragmented logistics markets and developing economies where capital allocation for automation competes with basic infrastructure needs.

Regulatory Uncertainty and Safety Certification Complexity

The absence of harmonized global safety standards for autonomous industrial vehicles creates significant regulatory friction for manufacturers and deployers across multiple jurisdictions. Compliance requirements under frameworks such as ISO 3691-4 (industrial trucks), ANSI/ITSDF B56 standards in North America, and varying EU machinery directives require manufacturers to pursue market-specific certifications, increasing time-to-market and development costs substantially.

In sectors such as pharmaceutical and food processing, where FDA regulations and GMP compliance govern facility operations, integrating autonomous forklifts requires additional validation and documentation, further extending deployment timelines and deterring operators from early adoption.

Opportunities - Subscription and Flexible Financing Models Democratizing Autonomous Forklift Access

The emergence of subscription-based and rental forklift models represents a transformative commercial opportunity that can fundamentally expand the addressable market for the Autonomous Forklift Market beyond large enterprises to mid-sized and regional operators. Traditionally, the high upfront capital requirement for autonomous forklifts has restricted adoption to well-capitalized global logistics and manufacturing companies. New flexible ownership structures are dismantling this barrier.

In December 2024, Jungheinrich launched its "Full Flex Rental" forklift subscription service, incorporating integrated fleet management and maintenance within a flexible, scalable subscription model enabling companies to dynamically expand or contract their autonomous forklift fleets, including automated systems, without committing to large capital outlays. This model aligns with the broader shift toward Opex-based procurement preferences across global enterprises and mirrors the success of Software-as-a-Service models in enterprise technology. As subscription and leasing penetration deepens, it will directly accelerate deployment velocity across warehousing, cold storage, and distribution center segments, particularly in markets like India and Southeast Asia where logistics infrastructure investment is scaling rapidly, supported by record leasing activity.

Emerging Market Logistics Modernization Driving First-Time Autonomous Deployment

Rapidly modernizing logistics ecosystems in India, Southeast Asia, the Middle East, and Latin America represent high-potential greenfield opportunities for the Autonomous Forklift Market, where first-time automated facility deployments avoid the legacy system constraints that slow adoption in mature markets. India's warehousing and logistics sector, valued at US$ 250 billion in 2021 and projected to reach US$ 380 billion by 2025 at a 10 to 12% annual growth rate, is transitioning from fragmented, manual operations toward tech-enabled, institutionally backed logistics parks.

Nearly 70% of Asia Pacific occupiers surveyed by CBRE expressed intent to expand logistics operations in India within two years, with 3PL providers and e-commerce firms leading warehouse leasing demand. India's National Logistics Policy explicitly targets reducing logistics costs from 13 to 14% of GDP to global benchmark levels by 2030, creating strong policy tailwinds for the adoption of automation across the supply chain. Tier-II city logistics expansion into Chandigarh, Hosur, and Jaipur, alongside multi-tenanted warehouse format proliferation, is creating standardized environments well-suited for autonomous forklift integration. Operators deploying autonomous forklifts in these first-time automated facilities gain long-term efficiency advantages without the retrofit and transition costs faced in legacy markets.

Category-wise Analysis

Product Type Insights

The counterbalance forklift segment holds the dominant position commanding nearly 30% of total market revenue. Its leadership stems from its versatility as the most widely used forklift type across manufacturing, distribution, and heavy-duty logistics applications, capable of handling diverse load types, operating both indoors and outdoors, and integrating with LiDAR and SLAM-based navigation systems without significant facility modification.

The segment benefits from strong adoption in automotive manufacturing and heavy industry, where European OEM production expansion and Industry 4.0 adoption are compelling operators to automate in-plant material handling. Companies including Toyota Industries Corporation, KION Group, and Jungheinrich have invested heavily in autonomous counterbalance platforms, reinforcing the segment's commercial maturity and breadth of deployment options.

The Order Picker segment is the fastest-growing forklift type within the Autonomous Forklift Market, driven by the explosive growth of e-commerce fulfillment operations demanding high-throughput, accurate individual item picking at elevation. As fulfillment centers shift from pallet-level to each-level picking to meet direct-to-consumer delivery models, autonomous order pickers equipped with vision-based navigation and AI-powered SKU recognition are becoming mission-critical.

Navigation Technology Insights

LiDAR and Laser Guidance technology hold the dominant position in the Autonomous Forklift Market's navigation segment, accounting for approximately 39% of market share. The technology's leadership is grounded in its proven accuracy with LGV systems recalculating vehicle position 30 to 40 times per second using reflector signals and its decades-long track record in demanding industrial environments. Germany, France, and the Netherlands' automotive, pharmaceutical, and precision manufacturing industries have anchored global LiDAR navigation adoption, where stringent material handling accuracy requirements make laser guidance the technically preferred solution.

SLAM (Simultaneous Localization and Mapping) and Hybrid Navigation represents the fastest-growing navigation technology segment within the Autonomous Forklift Market, driven by its unique ability to operate without pre-installed reflector or magnetic infrastructure enabling rapid deployment in dynamic, changing environments such as e-commerce fulfillment centers, cold storage, and construction material handling. Unlike fixed laser guidance systems, SLAM-based forklifts build and continuously update their own environmental maps, making them resilient to layout changes and suitable for facilities that reconfigure frequently.

Application Insights

Warehousing and Storage commands the largest application share within the Autonomous Forklift Market at approximately 32%, reflecting the segment's foundational role as the primary deployment environment for autonomous forklifts globally. The segment's dominance is driven by the scale and standardization of modern warehouse environments, that offers the structured floor layouts, reflective marker infrastructure, and predictable traffic patterns that maximize the operational efficiency of laser guidance and LiDAR-based navigation systems. India's industrial warehousing leasing reached record levels in 2024 at 39.5 million sq. ft. across eight major cities, underpinning sustained demand for automated intralogistics. Toyota Industries Corporation's June 2025 strategic privatization initiative to accelerate autonomous logistics technology development further signals long-term industry commitment to warehousing automation as the primary revenue anchor

Regional Insights

Asia Pacific Autonomous Forklift Market Trends and Insights

Asia Pacific commands approximately 40% of the global autonomous forklift market, establishing it as the world's dominant regional market, a position anchored by China's industrial-scale warehouse automation ecosystem, India's rapidly modernizing logistics infrastructure, and South Korea's high-technology manufacturing sector.

China's autonomous forklift market was valued at US$ 897.7 Mn in 2025, reflecting the country's role as both the world's largest manufacturer and largest deployer of autonomous intralogistics solutions. China's dominance is reinforced by its position as the leading driver of APAC's B2B eCommerce GMV, which accounts for approximately 80% of global B2B digital trade value by 2026, creating demand for automated warehouse throughput at a scale unmatched globally.

South Korea holds approximately 10% of the Asia Pacific autonomous forklift share, driven by its globally competitive semiconductor, electronics, and precision manufacturing sectors where autonomous forklifts operating under vision-guided and LiDAR-based navigation are essential for meeting the zero-defect material handling standards demanded by advanced fabrication facilities. Japan's contribution is anchored by Toyota Industries Corporation's June 2025 strategic privatization to accelerate autonomous logistics technology and Mitsubishi Logisnext's PLATTER Auto S Type demonstration in August 2025, reflecting Japan's position as a primary technology origination hub for the global market.

North America Autonomous Forklift Market Trends and Insights

North America holds approximately 32% of the Global Autonomous Forklift Market, with the United States autonomous forklift market valued at US$ 1,504.6 Mn in 2025 driven by structural labor shortages in warehousing, aggressive e-commerce fulfillment infrastructure investment, and an advanced enterprise IoT adoption base. U.S. food and beverage manufacturing employing approximately 1.7 million workers and accounting for 16.8% of total U.S. manufacturing sales in 2021, represents a primary demand vertical, where FDA compliance requirements and perishable goods handling mandates make consistent, autonomous material handling operationally essential. The U.S. market benefits from the presence of Seegrid Corporation (Zebra Technologies), Vecna Robotics, OTTO Motors, and Oceaneering International, all of whom maintain significant North American deployment footprints.

Canada's e-commerce market, online retail accounted for 6.1% of total retail sales in Canada as of December 2024, with fashion, hobby, leisure, and electronics driving the highest fulfillment velocity categories that require high-throughput autonomous pallet and order-picking solutions. The region's high enterprise IoT adoption rates, advanced digital infrastructure, and strong eProcurement ecosystem further accelerate the integration of autonomous forklifts into connected warehouse management platforms.

Europe Autonomous Forklift Market Trends and Insights

Europe accounts for approximately 20% of the global autonomous forklift market, characterized by a precision-engineering culture, stringent regulatory environment, and an advanced manufacturing sector that collectively make it a technically demanding but commercially significant regional market.

Germany, France, and the Netherlands are the primary demand anchors, where automotive OEMs, pharmaceutical manufacturers, and advanced logistics operators prioritize laser guidance and LiDAR-based navigation for their 30 to 40 recalculations-per-second accuracies. The EU's accommodation and business services economy employed approximately 10.9 million people in food and beverage services alone in 2022, with the broader manufacturing and distribution ecosystem generating sustained demand for autonomous material handling across cold chain, pharmaceutical, and industrial sectors.

Competitive Landscape

The global autonomous forklift market exhibits a semi-consolidated competitive structure, where a small group of global OEM leaders, Toyota Industries Corporation, KION Group, Jungheinrich, Mitsubishi Logisnext, and Hyster-Yale collectively dominate by revenue and geographic breadth, while a growing cohort of specialized robotics players, including VisionNav Robotics, Vecna Robotics, Balyo SA, AGILOX, and OTTO Motors, compete aggressively on navigation technology differentiation and niche application focus.

The market is neither fully consolidated nor fragmented. The top five OEMs leverage manufacturing scale, global service networks, and integrated hardware-software portfolios, while pure-play robotics firms compete on AI capability, deployment flexibility, and emerging subscription models. Barriers to entry remain high due to certification requirements, navigation technology IP, and customer switching costs.

Key Market Developments

- In March 2026, KION Group demonstrated the deployment of AI-powered autonomous industrial trucks in live warehouse operations at GTC 2026, including a pilot with GXO Logistics in France, leveraging digital twins, NVIDIA-powered AI perception, and real-time fleet orchestration, marking a critical transition from simulation-based development to real-world autonomous forklift operations with enhanced safety through AI-based human detection systems.

- In May 2025, Coca-Cola Bottlers Japan Inc. & Toyota Industries Corporation initiated full-scale deployment of Japan’s first 3D-LiDAR-enabled autonomous four-fork forklift for truck loading and unloading at the Hakushu Plant, achieving human-level precision in pallet handling and enabling end-to-end automation from manufacturing to shipping, marking a significant advancement in real-world adoption of autonomous forklift solutions in logistics operations.

- In July 2024, Kao Corporation & Toyota Industries Corporation: Successfully implemented Japan’s first real-world truck loading operations using automated forklifts at the Toyohashi Plant, enabling fully automated end-to-end warehouse processes from product receiving to truck loading, highlighting a major advancement in autonomous forklift deployment in complex, high-mix logistics environments.

Companies Covered in Autonomous Forklift Market

- Toyota Industries Corporation

- KION Group AG

- Jungheinrich AG

- Mitsubishi Logisnext Co. Ltd

- Hyster-Yale Group Inc.

- Hangcha Group Co. Ltd

- Balyo SA

- Swisslog Holding AG

- AGILOX Services GmbH

- HD Hyundai Construction Equipment

- VisionNav Robotics

- Seegrid Corporation (Zebra Technologies)

- Vecna Robotics

- OTTO Motors (Rockwell Automation)

- Oceaneering International Inc.

Frequently Asked Questions

The global autonomous forklift Market is projected to be valued at US$ 6.0 Bn in 2026.

Counterbalance Forklift leads the forklift type segment at approximately 30% share, supported by broad manufacturing and outdoor logistics deployment; Order Picker is the fastest-growing type driven by e-commerce fulfillment demand.

Warehousing & Storage leads with approximately 32% share, while E-commerce Fulfillment Centers are the fastest-growing segment.

The market is expected to witness a CAGR of 13.0% from 2026 to 2033.

The market is evolving toward AI-driven autonomous navigation and subscription-based business models, enhancing both technological capabilities and market accessibility.

Autonomous Forklift Market growth is driven by structural labor shortages, rapid expansion of e-commerce and digital trade, and increasing adoption of Industry 4.0 technologies enabling smart, automated warehouse operations.

Key opportunities in the Autonomous Forklift Market are driven by the rise of subscription-based and flexible financing models, enabling wider adoption, and rapid logistics modernization in emerging markets, creating strong demand for first-time autonomous forklift deployments.

Key players in the Autonomous Forklift Market include Toyota Industries Corporation, KION Group AG, Jungheinrich AG, Hyster-Yale Materials Handling, Inc., Mitsubishi Logisnext Co., Ltd., Seegrid Corporation, and AGILOX Services GmbH.