- Industrial Goods & Service

- Industrial Degreaser Market

Industrial Degreaser Market Size, Trends, Share, Regional Forecasts 2026 - 2033

Industrial Degreaser Market by Product Type (Light-Duty Degreasers, Medium-Duty Degreasers, Heavy-Duty Degreasers), Grade (Petroleum-Based, Bio-Based, Liquid-Based, Others), Industry (Automotive, Manufacturing/Industrial Machinery, Aviation/Aerospace, Pharmaceutical, Electronics), and Region Analysis for 2026 - 2033

Industrial Degreaser Market Share and Trends Analysis

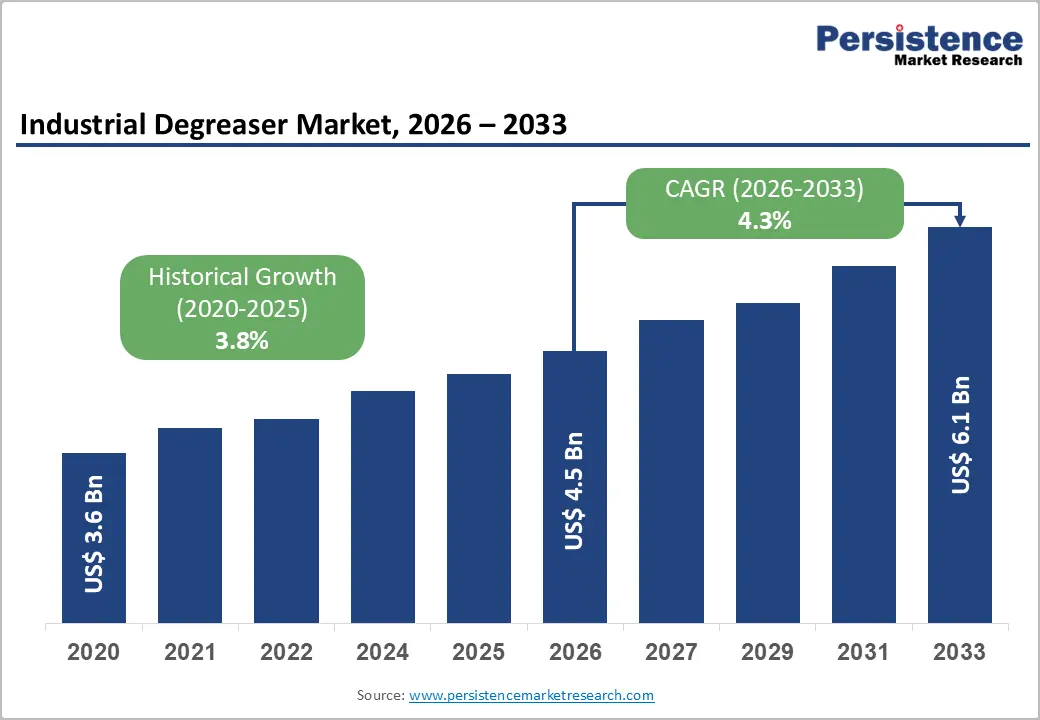

The global Industrial Degreaser Market size is likely at US$ 4.5 billion in 2026 and is projected to reach US$ 6.1 billion by 2033, growing at a CAGR of 4.3% between 2026 and 2033.

Sustained expansion in global automotive production, tightening environmental regulations governing solvent emissions, and accelerating industrial automation are the primary drivers of demand. The progressive shift toward bio-based and water-reducible formulations, driven by regulatory compliance requirements, is structurally reshaping product mix and average selling prices within the Industrial Degreaser Market.

Key Industry Highlights:

- Product Leadership: Heavy-Duty Degreasers lead product type at 36.9% share. Medium-duty degreasers are the fastest-growing at 4.3% CAGR, expanding across electronics and pharmaceutical cleaning applications.

- Dominant Grade: Petroleum-based grade dominates at 41.6% share. Bio-based formulations grow fastest at 6.2% CAGR, driven by EPA, REACH, and USDA Bio-Preferred compliance requirements.

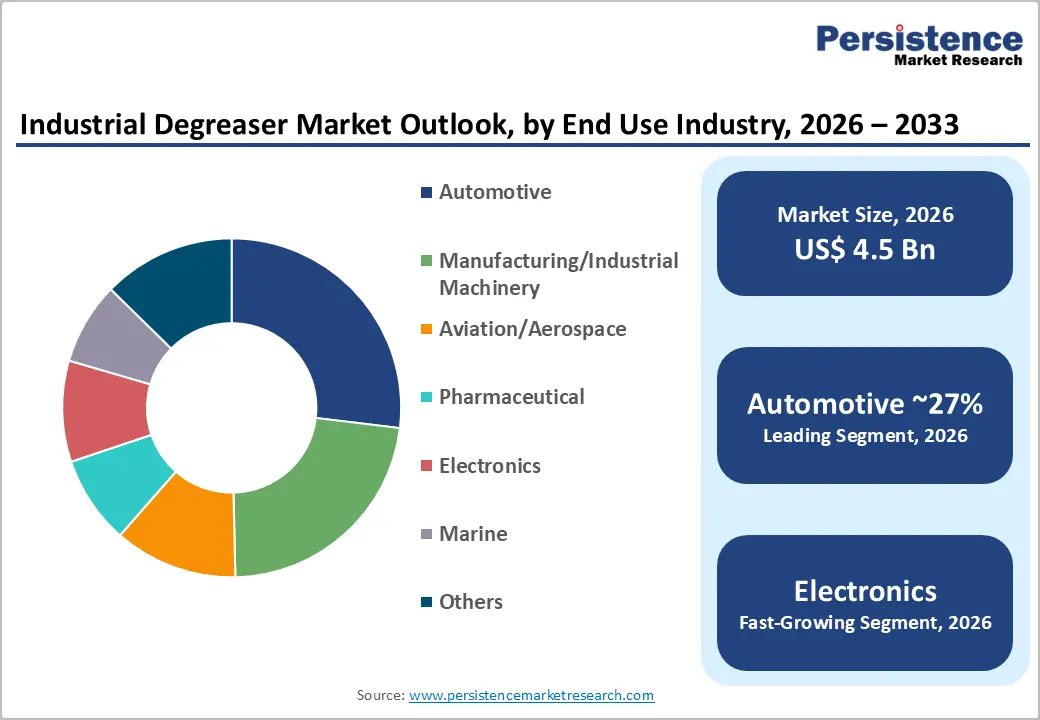

- End-use Market Scenario: Automotive leads with a 26.9% share; Electronics grows fastest at a 5.3% CAGR, supported by the U.S. CHIPS Act and the EU Chips Act semiconductor investment cycles.

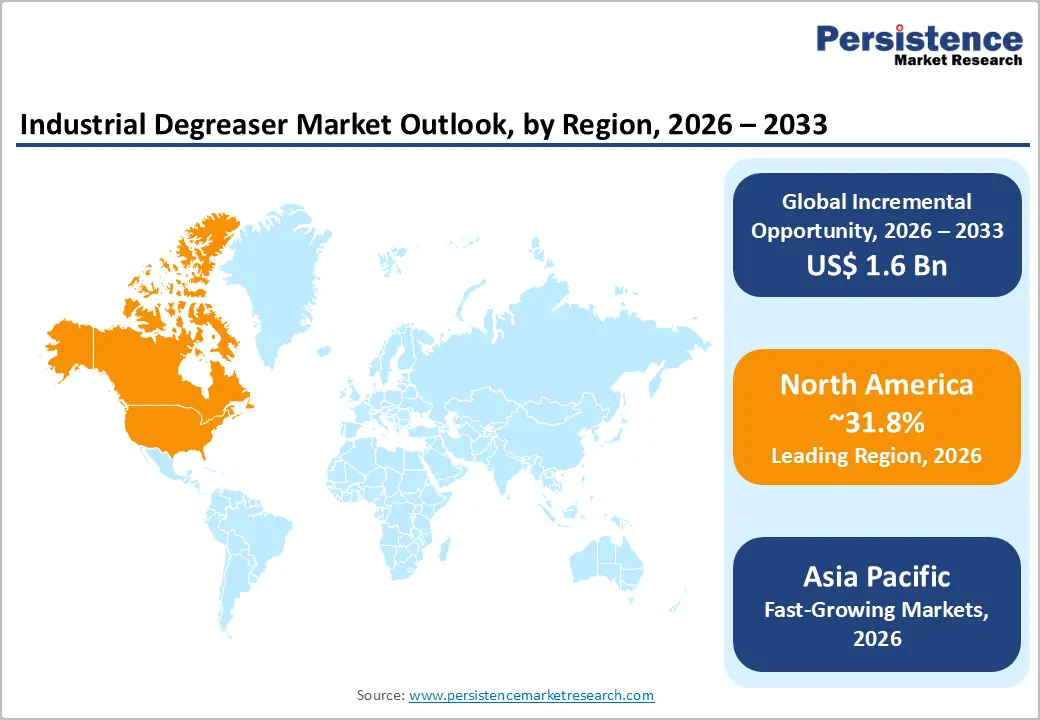

- Regional Leadership: North America dominates with ~31.8% global share; Asia Pacific is fastest-growing at 5.2% CAGR, led by China, India, and expanding ASEAN manufacturing clusters.

- Market Competitiveness: BASF's EV-compatible degreaser launch (2024) and Ecolab's bio-based product series launch (2025) mark critical competitive shifts toward sustainable and application-specific formulations.

| Key Insights | Details |

|---|---|

|

Industrial Degreaser Market Size (2026E) |

US$ 4.5 Bn |

|

Market Value Forecast (2033F) |

US$ 6.1 Bn |

|

Projected Growth CAGR (2026–2033) |

4.3% |

|

Historical Market Growth (2020–2025) |

3.8% |

DRO Analysis

Drivers - Expanding Global Automotive Production and Maintenance Activity

The automotive sector is the single largest end-use driver of industrial degreaser consumption, and its structural expansion directly increases demand for heavy-duty and medium-duty formulations used in engine cleaning, metal surface preparation, and component decontamination. According to the International Organization of Motor Vehicle Manufacturers (OICA), global motor vehicle production exceeded 93 million units in 2023 and continued recovering through 2024 and 2025.

Each production unit requires multiple degreasing steps across engine assembly, transmission manufacture, and body preparation. Additionally, the global installed base of vehicles requiring aftermarket service and preventive maintenance generates continuous, recurring demand for degreasers. This volume-driven demand profile, concentrated in the U.S., Germany, China, Japan, and India, reinforces the Industrial Degreaser Market's stable baseline growth across the forecast period.

Tightening Environmental and Occupational Health Regulations Driving Formulation Upgrades

Regulatory frameworks governing volatile organic compound (VOC) emissions, hazardous solvent use, and workplace chemical exposure are compelling manufacturers across the automotive, aerospace, and electronics sectors to transition from conventional petroleum-solvent degreasers toward bio-based, water-based, and low-VOC alternatives. The U.S. Environmental Protection Agency (EPA) regulations under the Clean Air Act Amendments restrict the use of high-VOC solvent degreasers in commercial and industrial environments.

The EU's REACH regulation imposes strict controls on hazardous substances, including perchloroethylene and trichloroethylene, which have historically been used in industrial cleaning. These regulatory mandates effectively accelerate product replacement cycles, creating sustained revenue opportunities for compliant formulation suppliers while simultaneously constraining the legacy petroleum-based solvent degreaser segment.

Restraints - Regulatory Restrictions on Petroleum-Based and Chlorinated Solvent Degreasers

The dominant petroleum-based degreaser segment faces mounting regulatory headwinds as the U.S. EPA, EU REACH, and equivalent national frameworks progressively restrict or ban high-VOC and halogenated solvents. Transition costs for industrial end-users reformulating cleaning processes, including equipment modification, worker retraining, and validation testing, create adoption friction that can slow compliance uptake. Manufacturers of conventional solvent-based systems face product lifecycle compression risks, with regulatory-driven phase-outs threatening existing revenue streams before next-generation bio-based alternatives achieve competitive cost parity.

Raw Material Price Volatility and Supply Chain Concentration

Industrial degreaser formulations rely on petrochemical derivatives, surfactants, and specialty solvents, all of which are subject to crude oil price volatility and geographic supply concentration risks. Brent crude oil price fluctuations of 30% to 50% over a 12-month cycle directly compress manufacturer margins when cost pass-through to end users is constrained by competitive market pricing. Bio-based feedstock supply chains, essential to the fastest-growing degreaser-grade category, are also subject to agricultural commodity price volatility and seasonal availability constraints, complicating the stability of production costs for eco-formulation producers.

Opportunities - Bio-Based Degreaser Adoption Across Regulated Industrial End-Markets

The Bio-Based grade segment is the fastest-growing formulation category in the Industrial Degreaser Market, with a 6.2% CAGR, driven by institutional procurement policies prioritizing green chemistry, regulatory compliance mandates, and corporate sustainability commitments. The U.S. BioPreferred Program, administered by the USDA, mandates minimum bio-based content thresholds for cleaning products procured by federal agencies, directly stimulating institutional demand.

The European Green Deal and the Circular Economy Action Plan commitments similarly incentivize industrial chemical procurement managers to transition to certified bio-based cleaning systems. Suppliers who obtain recognized eco-certification labels and demonstrate measurable environmental performance credentials can command pricing premiums and secure long-term supply agreements with sustainability-committed industrial buyers.

Emerging Market Manufacturing Infrastructure Development

Rapid industrialization across India, Southeast Asia, and Latin America is creating large incremental demand pools for industrial degreasers as new automotive plants, electronics assembly facilities, and pharmaceutical manufacturing units are commissioned.

India's Production-Linked Incentive scheme is attracting over US$ 26 billion in committed manufacturing investment across 14 key sectors, including electronics, pharmaceuticals, and automotive components, all of which require industrial degreasing solutions for equipment maintenance and production processes. Degreaser suppliers establishing localized distribution partnerships, technical service capabilities, and regionally compliant product registrations in these growth markets can build durable market share positions ahead of mature competitor entrenchment within the industrial degreaser market.

Category-wise Analysis

Product Type Insights

Heavy-duty degreasers lead the product type segmentation with 36.9% of global market share in 2026, reflecting concentrated consumption in the automotive, aerospace, and heavy industrial machinery sectors, where high grease, accumulated oil, and carbon deposits require powerful formulations for effective removal. These degreasers are indispensable for engine overhaul operations, turbine maintenance, and industrial floor cleaning. The segment's commercial leadership is reinforced by the large installed base of heavy industrial equipment globally, requiring routine high-performance cleaning at defined maintenance intervals across primary manufacturing geographies.

Medium-duty degreasers are the fastest-growing segment, with a 4.3% CAGR, driven by broader adoption across mid-scale manufacturing facilities, electronics assembly operations, and pharmaceutical equipment cleaning applications where heavy-duty formulations would be excessive and light-duty products would be insufficient for cleaning efficacy.

Grade Insights

Petroleum-Based degreasers hold the leading grade position with 41.6% of global market share, underpinned by their established cost competitiveness, widespread availability, proven cleaning performance across heavy grease and hydrocarbon contamination profiles, and deep penetration in mature industrial markets. The automotive and heavy machinery sectors continue to deploy petroleum-based formulations as the primary cleaning agent for high-carbon-deposit removal applications, where bio-based alternatives have not yet achieved equivalent solubilization efficacy. Their established distribution infrastructure and long-standing OEM cleaning specification approvals reinforce segment leadership despite intensifying regulatory pressure.

Bio-based degreasers are the fastest-growing grade at 6.2% CAGR, propelled by regulatory compliance mandates under EPA and EU REACH frameworks, USDA BioPreferred Program procurement requirements, and corporate sustainability policies driving institutional procurement shifts toward certified green chemistry solutions.

Industry Insights

Automotive is the dominant Industry segment, commanding 26.9% of the global industrial degreaser market share in 2026, reflecting the sector's extraordinary volume of cleaning applications spanning engine assembly, transmission manufacturing, body fabrication, paint surface preparation, and aftermarket vehicle service and maintenance. OICA data confirms global automotive production exceeded 93 million units in 2023, with each unit passing through multiple degreasing process steps. The automotive sector's simultaneous transition toward electric vehicle platforms is additionally creating new cleaning requirements for battery module assembly and power electronics manufacturing processes.

Electronics is the fastest-growing end-use segment, with a 5.3% CAGR, driven by the global semiconductor investment supercycle, expanding PCB production, and precision component manufacturing requirements that demand residue-free, ESD-compatible cleaning formulations for cleanroom environments.

Regional Market Insights

North America Industrial Degreaser Market Trends

North America holds the dominant global share of approximately 31.8% in the Industrial Degreaser Market, anchored by the U.S.'s large-scale automotive manufacturing base, extensive aerospace and defense maintenance operations, and mature pharmaceutical and electronics manufacturing sectors.

The U.S. EPA's Clean Air Act VOC regulations and OSHA chemical exposure standards are the primary regulatory forces shaping formulation transitions toward low-VOC and water-based systems, compelling end-users to accelerate product specification upgrades. The U.S. aerospace sector, which represents a significant degreaser consumption base due to maintenance, repair, and overhaul (MRO) requirements, is supported by FAA-mandated cleaning standards and Department of Defense procurement specifications.

Canada contributes incremental regional demand through its automotive assembly and mining equipment maintenance sectors. North American innovation leadership in bio-based degreaser chemistry, driven by USDA BioPreferred program incentives, reinforces the region's position as the primary commercialization testbed for next-generation green formulations.

Europe Industrial Degreaser Market Trends

Europe is expected to achieve steady CAGR growth, driven by rigorous EU REACH chemical regulatory compliance requirements, the European Green Deal sustainability framework, and sustained demand from Germany's automotive OEM and Tier 1 supplier ecosystem. Germany remains the regional demand anchor, with its automotive production base, which hosts BMW, Volkswagen, Mercedes-Benz, and their supplier networks, generating consistent, high-volume consumption of both heavy-duty and medium-duty industrial degreaser formulations. The U.K. maintains industrial demand through its aerospace MRO sector, while France and Spain contribute through automotive assembly and industrial machinery manufacturing activities.

EU chemical safety directives are accelerating the phase-out of petroleum-solvent degreasers across member states, creating structured replacement demand for bio-based and low-VOC alternatives. Regulatory harmonization under REACH provides a unified compliance framework that simplifies pan-European product registration for reformulated green degreaser systems.

Asia Pacific Industrial Degreaser Market Insights

Asia Pacific is the fastest-growing regional market at 5.2% CAGR, driven by China's dominant manufacturing ecosystem, India's accelerating industrial base expansion, and ASEAN's growing electronics and automotive production clusters. China leads regional consumption volume through its massive automotive, electronics, and heavy machinery manufacturing sectors, generating the highest absolute degreaser demand across the Asia Pacific.

Japan sustains premium-grade industrial degreaser adoption through its precision automotive component manufacturing and high-technology electronics assembly industries. India's PLI scheme-driven manufacturing investments are creating structural new demand across automotive, pharmaceutical, and electronics degreasing applications.

South Korea's semiconductor and shipbuilding sectors sustain consistent specialized degreaser consumption, while Vietnam, Thailand, and Malaysia are absorbing manufacturing relocation investments that progressively expand regional industrial degreaser demand. Local price competition from domestic Chinese manufacturers keeps average selling prices disciplined across mid-tier product categories.

Competitive Landscape

Market leaders in the Industrial Degreaser Market are advancing bio-based formulation innovation, regulatory compliance positioning, and application-specific product differentiation as dominant competitive strategies. Ecolab and Henkel leverage integrated service models bundling product supply with technical cleaning consultation. Emerging trends include EV-compatible cleaning system development, concentrated product formats reducing logistics costs, and sustainability-certified product portfolios targeting institutional procurement mandates.

Key Developments:

- In 2025, Ecolab Inc. launched a new bio-based industrial degreaser series targeting automotive manufacturing and electronics assembly applications, incorporating plant-derived surfactant technology meeting EPA Safer Choice and EU Ecolabel standards across North American and European industrial markets.

- In 2025, Henkel AG & Co. KGaA expanded its Bonderite industrial cleaning and degreasing product portfolio with low-VOC, water-based formulations for precision electronics and aerospace component cleaning, securing new OEM supply agreements with European Tier 1 automotive and aerospace manufacturers.

Companies Covered in Industrial Degreaser Market

- Ecolab Inc.

- Henkel AG & Co. KGaA

- BASF SE

- 3M Company

- Diversey Holdings Ltd.

- Illinois Tool Works Inc.

- Dow Inc.

- Zep Inc.

- NCH Corporation

- Carroll Company

- Stepan Company

- A.W. Chesterton Company

- Quaker Houghton

- Callington Haven Pty Ltd

- BG Products Inc.

Frequently Asked Questions

The industrial degreaser market size is valued at US$ 4.5 Bn in 2026, projected to reach US$ 6.1 Bn by 2033.

Expanding global automotive production, tightening VOC emission regulations, and industrial automation growth are the primary demand drivers.

The market is projected to grow at a CAGR of 4.32% from 2026 to 2033, accelerating from a 3.8% historical rate.

Bio-based formulation adoption, precision electronics cleaning demand driven by the semiconductor investment cycle, and emerging market manufacturing expansion represent the most actionable growth opportunities.

Leading players include Ecolab, Henkel, BASF, 3M, Diversey, Illinois Tool Works, Dow, Zep, NCH Corporation, Quaker Houghton, Stepan, Callington Haven, A.W. Chesterton, Carroll Company, and BG Products.