- Medical Devices

- Genomic Urine Testing Market

Genomic Urine Testing Market Size, Share, and Growth Forecast for 2026-2033

Genomic Urine Testing Market by Application (Oncology, Infectious Diseases, Genetic & Hereditary Disorders, Transplant Monitoring, Pharmacogenomics, Prenatal & Reproductive Health, Technology (NGS, PCR-based Technologies, Microarrays, Nanopore Sequencing, Bioinformatics Platforms), End-User (Hospitals & Clinics, Diagnostic & Reference Laboratories, Pharmaceutical & Biotech Companies, Point-of-Care Providers, Direct-to-Consumer Providers), and Regional Analysis for 2026-2033

Genomic Urine Testing Market Share and Trends Analysis

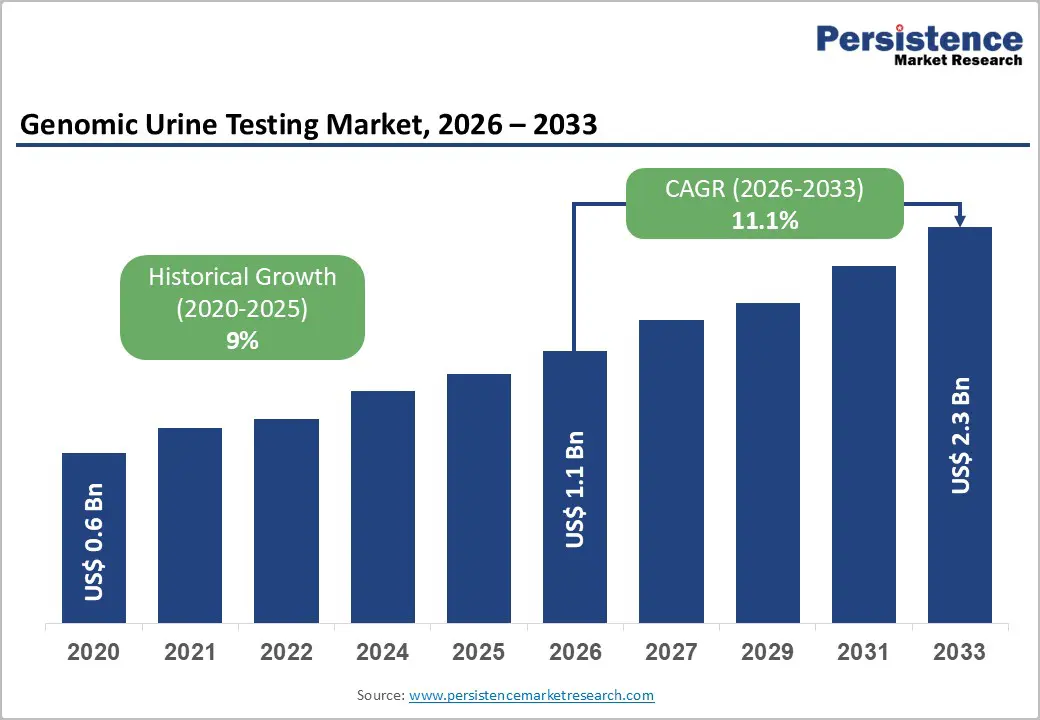

The global genomic urine testing market size is likely to be valued at US$ 1.1 billion in 2026, and is projected to reach US$ 2.3 billion by 2033, growing at a CAGR of 11.1% during the forecast period 2026–2033.

This growth is primarily driven by the rising global burden of cancer and chronic diseases, which compels healthcare systems to prioritize early detection and continuous disease monitoring. Clinicians increasingly adopt liquid biopsy diagnostics because urine-based genomic tests provide a non-invasive, repeatable, and patient-friendly alternative to tissue biopsy. Rapid advancements in next-generation sequencing (NGS) platforms enhance analytical sensitivity, reduce turnaround times, and lower per-sample sequencing costs, enabling broader clinical deployment. Simultaneously, integration of advanced bioinformatics analytics improves mutation interpretation and risk stratification. Regulatory validation of molecular assays and expanding reimbursement coverage across developed economies further strengthen commercialization pathways and accelerate clinical uptake.

Key Industry Highlights

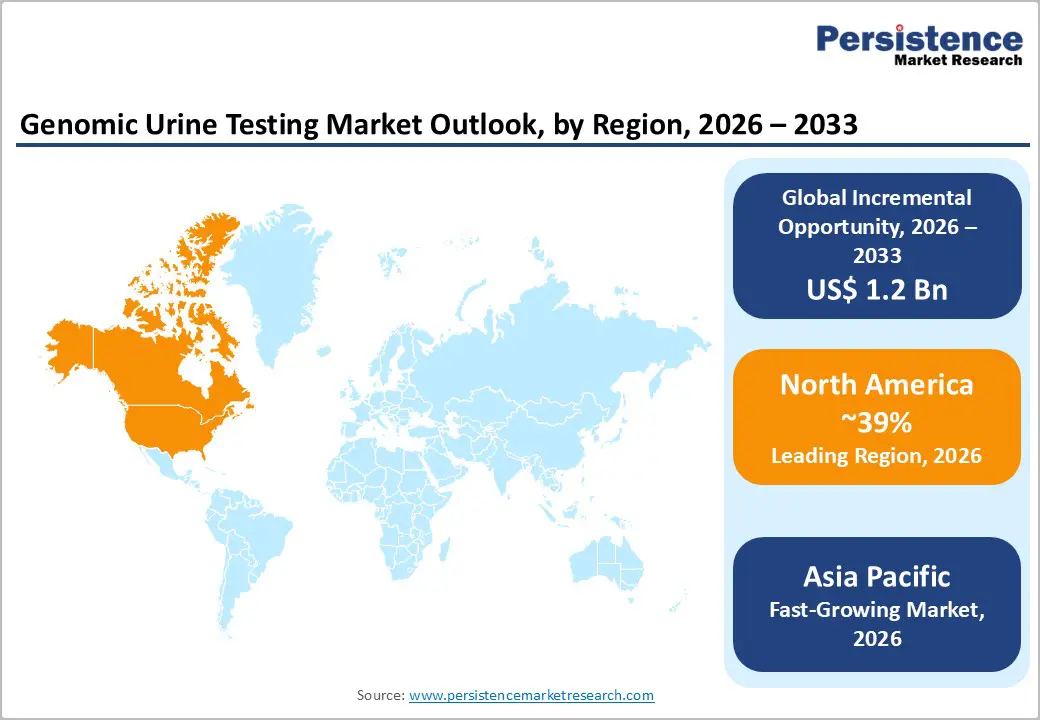

- Regional Leadership: North America is poised to lead with an estimated 39% share in 2026, while Asia Pacific is projected to register the fastest growth at 12.8% CAGR through 2033, driven by heavy genomic research investments.

- Dominant Applications: Oncology is set to command around 39% revenue share in 2026, while transplant monitoring is likely to grow the fastest through 2033, driven by rising cancer prevalence worldwide.

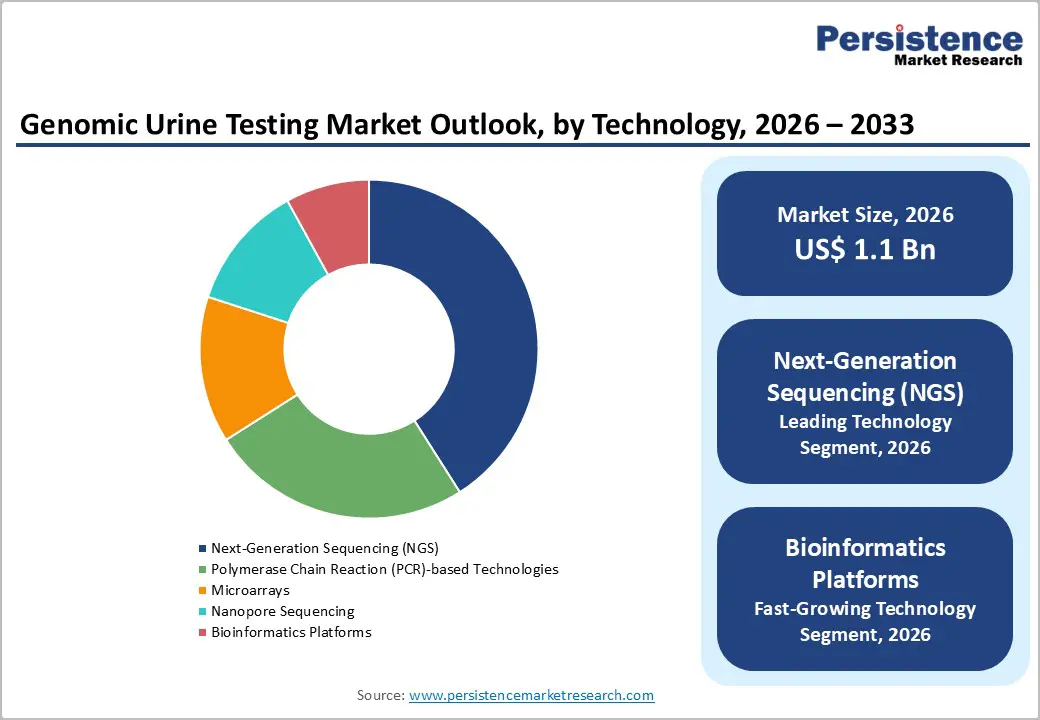

- Leading Technologies: NGS is projected to hold approximately 41% revenue share in 2026, while bioinformatics platforms are expected to expand the fastest at 13.1% CAGR during 2026–2033, supported by AI-driven genomic data interpretation.

- Dominant End-Users: Diagnostic and reference laboratories are anticipated to account for nearly 47% revenue share in 2026, while point-of-care providers are forecast to grow the fastest through 2033, reflecting decentralization of molecular diagnostics.

- Competitive Environment: Competitive dynamics increasingly center on NGS capacity expansion, AI-enabled bioinformatics collaborations, and strategic geographic expansion initiatives.

- Core Growth Drivers: Market expansion continues to be anchored in rising precision medicine adoption, broader regulatory validation of molecular assays, and supportive reimbursement policies across developed healthcare systems.

| Key Insights | Details |

|---|---|

|

Genomic Urine Testing Market Size (2026E) |

US$ 1.1 Bn |

|

Market Value Forecast (2033F) |

US$ 2.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

11.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

10.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Escalating Global Disease Burden and Accelerating Adoption of Non-Invasive Genomic Diagnostics

According to the World Health Organization (WHO), cancer accounts for nearly 10 million deaths annually, and global incidence is projected to increase by over 47% by 2040. This rapid rise in cancer prevalence continues to intensify clinical demand for early detection and ongoing surveillance solutions across both developed and emerging healthcare systems. Liquid biopsy and genomic assays, including urine-based approaches, provide minimally invasive alternatives to tissue biopsies, reducing procedural risk and enabling more frequent monitoring across care pathways. Healthcare providers increasingly prioritize screening tools that improve patient compliance while supporting longitudinal disease management strategies.

In October 2025, a strategic collaboration between A.D.A.M. Innovations and SOPHiA GENETICS was launched to expand AI-enabled liquid biopsy genomic testing and companion diagnostics in Japan, marking a tangible industry shift toward broader clinical adoption of data-driven oncology tools. This partnership, announced at the European Society for Medical Oncology Congress, underscores global efforts to bring advanced molecular diagnostics into routine cancer care by reducing turnaround times and enhancing personalized treatment strategies. The initiative also reflects increasing international investment in precision oncology infrastructure and cross-border technology integration.

Technological Advancements and Regulatory Alignment Strengthening Commercial Viability

Technological progress in NGS and polymerase chain reaction (PCR)-based assays has dramatically lowered sequencing costs over the last decade, expanding clinical accessibility and enabling complex genomic profiling in routine diagnostics. Innovations in bioinformatics and AI-driven mutation analysis significantly enhance test sensitivity and specificity, supporting broader applications in oncology, infectious disease screening, transplant rejection monitoring, and precision therapy matching. These capabilities allow laboratories to scale operations efficiently while delivering higher diagnostic accuracy and faster clinical decision support.

In late 2025, Foundation Medicine achieved a milestone with 100 approved companion diagnostic indications using NGS platforms across the United States and Japan, demonstrating a maturation of regulatory acceptance for high-complexity genomic tests. Such approvals reinforce confidence in genomic diagnostics and accelerate implementation in precision oncology programs worldwide. Additionally, these advancements align with public health initiatives that emphasize non-invasive testing and precision medicine as core elements of modern clinical practice, strengthening long-term commercialization prospects.

High Testing Costs and Reimbursement Variability Limiting Broader Adoption

Despite cost reductions in sequencing, comprehensive multi-gene urine assays remain expensive. Advanced molecular panels may exceed several hundred dollars per test, creating affordability challenges in low- and middle-income countries. Reimbursement policies vary significantly across regions, limiting adoption in emerging markets and smaller hospital systems. Private insurers and public payers often require extensive clinical utility evidence before approving coverage, delaying revenue realization for providers. These financial constraints continue to restrict penetration beyond specialized oncology and tertiary care settings. The pricing gap between advanced molecular diagnostics and conventional screening tools further widens accessibility disparities across healthcare systems.

In the United States, evolving payer policies have underscored these reimbursement challenges. Blue Cross and Blue Shield of North Carolina updated its molecular testing reimbursement guidelines, specifying detailed coding and documentation requirements that, if unmet, can result in claim denials or delayed payments. Meanwhile, Johns Hopkins Health Plans implemented new reimbursement policies effective March 2025 that restrict payment for investigational or unproven molecular tests and require rigorous medical necessity documentation before coverage. These payer actions illustrate real-world administrative hurdles that independent and hospital laboratories face when seeking reimbursement for advanced genomic assays under existing frameworks.

Regulatory and Data Governance Complexity Extending Commercial Timelines

Urine-based genomic biomarkers require extensive clinical validation to demonstrate analytical sensitivity, specificity, and clinical utility. Regulatory pathways under U.S. Food and Drug Administration (FDA) and European Union (EU) In Vitro Diagnostic Regulation (IVDR) frameworks involve rigorous documentation, extending time-to-market. In 2026, the U.S. Food and Drug Administration published updated draft guidance on frameworks for individualized and genomic therapies, reinforcing stringent evidentiary requirements for molecular diagnostic approvals and underscoring the data intensity necessary for clearance. Companies must conduct multi-center studies and demonstrate reproducibility before commercialization, increasing development costs and prolonging regulatory lifecycles.

Data privacy regulations such as the General Data Protection Regulation (GDPR) in Europe create compliance burdens for genomic data storage and transfer, increasing operational costs for diagnostic companies. In 2025, several European data protection authorities intensified enforcement actions related to sensitive health and biometric data processing, signaling heightened scrutiny on genetic information privacy and governance. Furthermore, in 2026 the U.S. Office of Inspector General (OIG) rolled out new compliance guidance that introduces potential daily civil monetary penalties for incorrect laboratory billing or reporting under Medicare, especially for high-cost molecular assays. These developments emphasize that regulatory and data governance complexity, from clinical validation to billing compliance, elevates entry barriers and slows innovation scaling within the genomic urine testing market.

Expansion in Strengthening Asia Pacific Healthcare Systems

Healthcare expenditure in Asia Pacific continues to grow, particularly in China and India, where national screening programs are expanding. According to the World Bank, healthcare spending as a percentage of GDP has steadily increased across major ASEAN economies. Governments across the region are strengthening diagnostic infrastructure to support early disease detection and population health management. Rising middle-class populations and improving insurance penetration further enhance access to advanced medical technologies. These structural improvements create favorable conditions for broader deployment of genomic urine testing solutions.

This opportunity is reinforced by government-led precision medicine initiatives across Asia-Pacific. Singapore expanded its National Precision Medicine Programme Phase III, aiming to integrate genomic insights into routine preventive and diagnostic care for hundreds of thousands of residents, a move that reflects political commitment to precision diagnostics and research capacity building. Additionally, states such as Telangana and Kerala in India are actively positioning themselves as life sciences and medical devices hubs, attracting investment, fostering innovation ecosystems, and encouraging manufacturing partnerships that can support regional genomic testing infrastructure. These developments significantly enlarge the addressable market for genomic urine assays and allied diagnostics.

AI Integration and Preventive Genomics to Unlock New Revenue Channels

The convergence of genomic testing with AI-powered bioinformatics analytics enhances predictive accuracy for oncology and transplant rejection monitoring. Cloud-based analytics platforms reduce computational barriers for smaller laboratories and enable scalable data interpretation. Strategic collaborations between sequencing companies and software developers support automated mutation detection and risk stratification. This integration increases clinical utility and differentiates premium offerings in a competitive market landscape. As clinical datasets expand, machine learning algorithms continue to refine diagnostic precision and outcome-prediction models.

Real-world adoption of AI-enabled genomic and liquid biopsy solutions in 2025–2026 highlights this trend. At the European Society for Medical Oncology (ESMO) Asia Congress 2025, leading clinicians and researchers showcased AI-driven liquid biopsy and multi-omics approaches that span early tumor detection to treatment response monitoring, underlining growing clinical confidence in AI-integrated diagnostics across the region. In India, genomic testing demand is surging beyond major metropolitan centers, driven by broader preventive care adoption and proactive consumer engagement with molecular health insights. These shifts, supported by broader healthcare policy and technology adoption, create fertile ground for expanding urine-based molecular testing into both clinical and preventive health segments.

Category-wise Analysis

Application Insights

Oncology is expected to capture nearly 39% of the genomic urine testing market revenue share in 2026, driven by strong policy and clinical backing for liquid biopsy adoption. Government-supported frameworks and updated guidelines from the National Comprehensive Cancer Network (NCCN) now recommend comprehensive genomic profiling, including circulating tumor DNA testing, when tissue biopsy is not feasible, expanding molecular diagnostics in advanced cancer care. This shift reinforces non-invasive testing across oncology pathways and strengthens personalized treatment alignment.

In 2025, the NHS England launched a nationwide liquid biopsy program using ctDNA panels for lung and breast cancer management. The initiative enables faster therapy decisions and reduces invasive procedures for thousands of patients annually.

Transplant monitoring is projected to be the fastest growing application segment, projected to expand at around 12.4% CAGR through 2033, driven by rising demand for non-invasive graft surveillance. Urine-based genomic assays detecting donor-derived DNA are reducing dependence on surgical biopsies and enabling earlier rejection detection. Clinical research advancements in 2025 highlighted the reliability of cell-free DNA biomarkers for real-time graft health assessment, accelerating hospital adoption.

Expanding transplant volumes globally and the push for precision post-operative care further support uptake. Integration of molecular monitoring into standardized transplant protocols is strengthening reimbursement pathways. These factors collectively position transplant diagnostics as a high-growth opportunity within genomic urine testing.

Technology Insights

NGS is likely to remain the dominant technology platform, estimated to hold 41% of the genomic urine testing market share in 2026, due to its high-throughput capability and multiplex gene panel flexibility. Declining sequencing costs and improved turnaround times are enhancing accessibility across oncology and complex disease applications. Clinical guidance from the National Comprehensive Cancer Network continues to reference comprehensive genomic profiling, reinforcing NGS integration into routine workflows.

Healthcare systems are increasingly reimbursing broad molecular panels, validating clinical and economic value. Centralized laboratories favor NGS for its scalability and depth of genomic insight. Its established infrastructure and regulatory acceptance sustain its technology leadership

Bioinformatics platforms are projected to grow at an estimated 13.1% CAGR through 2033, fueled by the surge in genomic data requiring advanced interpretation tools. AI-enabled mutation analysis, automated reporting, and cloud-based integration are transforming raw sequencing output into clinically actionable insights. Laboratories are investing in scalable analytics ecosystems to manage increasing testing volumes and complex variant classification.

In 2025, leading clinical lab networks expanded digital pathology and genomics data platforms to streamline molecular reporting, reflecting rising demand for integrated solutions. These platforms reduce turnaround time while improving diagnostic accuracy and compliance. Their expanding role in precision medicine workflows drives rapid segment growth.

Regional Insights

North America Genomic Urine Testing Market Trends

North America is projected to account for about 39% of the genomic urine testing market value in 2026, maintaining its leadership due to advanced molecular diagnostics infrastructure and structured reimbursement systems. The United States remains the core growth engine, supported by regulatory oversight from the FDA, which continues to expand approvals for oncology-related molecular assays. In March 2026, the FDA cleared additional next-generation sequencing–based companion diagnostic panels for solid tumor profiling, reinforcing confidence in regulated genomic testing pathways. High cancer prevalence and expanding precision medicine initiatives further strengthen demand. Integration of genomic assays into hospital oncology networks continues at scale.

The Centers for Medicare & Medicaid Services (CMS) updated reimbursement frameworks to broaden coverage for certain molecular diagnostic tests under Medicare, supporting accessibility for eligible oncology patients. Major U.S. cancer centers also expanded clinical trial programs utilizing liquid biopsy monitoring for therapy response assessment. These system-level developments demonstrate institutional commitment to precision diagnostics. Strong academic–industry collaboration and continuous funding from federal health agencies further accelerate biomarker validation. These regulatory clarity and reimbursement support solidify North America’s dominant position.

Europe Genomic Urine Testing Market Trends

Europe continues to represent a significant revenue base, led by the Germany, United Kingdom, France, and Spain. Full enforcement of the IVDR under the European Commission (EC) in 2025 has intensified compliance requirements for molecular diagnostics manufacturers. This regulatory shift strengthens diagnostic reliability and patient safety while raising entry standards. Public healthcare systems continue to support oncology screening initiatives incorporating genomic technologies. Academic research institutions across the region remain active in biomarker discovery programs.

In 2026, the NHS England expanded access to molecular profiling services through additional Genomic Laboratory Hubs, increasing regional capacity for precision oncology testing. Simultaneously, Germany’s Federal Joint Committee (G-BA) evaluated reimbursement pathways for expanded molecular diagnostics in oncology care, reflecting institutional review of clinical value. These developments illustrate how policy-driven frameworks are shaping commercialization pace. While reimbursement heterogeneity persists across member states, standardized quality control under IVDR improves long-term scalability. Europe’s emphasis on safety, validation, and public funding ensures steady market progression.

Asia Pacific Genomic Urine Testing Market Trends

The market for genomic urine testing Asia Pacific is projected to grow at an approximate 2026-2033 CAGR of 12.8% through 2033, making it the fastest expanding region. Growth is spearheaded by China, Japan, and India, where governments are prioritizing genomic medicine within national healthcare modernization strategies. In 2025, China’s National Health Commission (NHC) reinforced its precision medicine framework by supporting hospital-level genomic testing capabilities in major urban centers. Japan continued reimbursement support for certain next-generation sequencing oncology panels under its national insurance system, sustaining clinical uptake. Rising cancer incidence and aging demographics further amplify testing demand.

India’s Department of Biotechnology expanded funding for genomics-driven cancer research collaborations across public institutes, promoting domestic diagnostic innovation in 2026. Regional governments are also investing in digital health integration to strengthen laboratory networks and data interoperability. Local manufacturing partnerships are increasing to reduce import dependency and improve affordability. Expanding private hospital chains across Southeast Asia are incorporating advanced molecular diagnostics into tertiary care offerings. Regulatory streamlining efforts in key markets are enhancing approval efficiency. These coordinated policy and infrastructure developments position Asia Pacific as the primary engine of long-term market growth.

North America is projected to account for about 39% of the genomic urine testing market value in 2026, maintaining its leadership due to advanced molecular diagnostics infrastructure and structured reimbursement systems. The United States remains the core growth engine, supported by regulatory oversight from the FDA, which continues to expand approvals for oncology-related molecular assays. In March 2026, the FDA cleared additional next-generation sequencing–based companion diagnostic panels for solid tumor profiling, reinforcing confidence in regulated genomic testing pathways. High cancer prevalence and expanding precision medicine initiatives further strengthen demand. Integration of genomic assays into hospital oncology networks continues at scale.

The Centers for Medicare & Medicaid Services (CMS) updated reimbursement frameworks to broaden coverage for certain molecular diagnostic tests under Medicare, supporting accessibility for eligible oncology patients. Major U.S. cancer centers also expanded clinical trial programs utilizing liquid biopsy monitoring for therapy response assessment. These system-level developments demonstrate institutional commitment to precision diagnostics. Strong academic–industry collaboration and continuous funding from federal health agencies further accelerate biomarker validation. These regulatory clarity and reimbursement support solidify North America’s dominant position.

Europe Genomic Urine Testing Market Trends

Europe continues to represent a significant revenue base, led by the Germany, United Kingdom, France, and Spain. Full enforcement of the IVDR under the European Commission (EC) in 2025 has intensified compliance requirements for molecular diagnostics manufacturers. This regulatory shift strengthens diagnostic reliability and patient safety while raising entry standards. Public healthcare systems continue to support oncology screening initiatives incorporating genomic technologies. Academic research institutions across the region remain active in biomarker discovery programs.

In 2026, the NHS England expanded access to molecular profiling services through additional Genomic Laboratory Hubs, increasing regional capacity for precision oncology testing. Simultaneously, Germany’s Federal Joint Committee (G-BA) evaluated reimbursement pathways for expanded molecular diagnostics in oncology care, reflecting institutional review of clinical value. These developments illustrate how policy-driven frameworks are shaping commercialization pace. While reimbursement heterogeneity persists across member states, standardized quality control under IVDR improves long-term scalability. Europe’s emphasis on safety, validation, and public funding ensures steady market progression.

Asia Pacific Genomic Urine Testing Market Trends

The market for genomic urine testing Asia Pacific is projected to grow at an approximate 2026-2033 CAGR of 12.8% through 2033, making it the fastest expanding region. Growth is spearheaded by China, Japan, and India, where governments are prioritizing genomic medicine within national healthcare modernization strategies. In 2025, China’s National Health Commission (NHC) reinforced its precision medicine framework by supporting hospital-level genomic testing capabilities in major urban centers. Japan continued reimbursement support for certain next-generation sequencing oncology panels under its national insurance system, sustaining clinical uptake. Rising cancer incidence and aging demographics further amplify testing demand.

India’s Department of Biotechnology expanded funding for genomics-driven cancer research collaborations across public institutes, promoting domestic diagnostic innovation in 2026. Regional governments are also investing in digital health integration to strengthen laboratory networks and data interoperability. Local manufacturing partnerships are increasing to reduce import dependency and improve affordability. Expanding private hospital chains across Southeast Asia are incorporating advanced molecular diagnostics into tertiary care offerings. Regulatory streamlining efforts in key markets are enhancing approval efficiency. These coordinated policy and infrastructure developments position Asia Pacific as the primary engine of long-term market growth.

Competitive Landscape

The global genomic urine testing market structure is moderately consolidated, with top players such as Roche, Qiagen, Guardant Health, and Illumina controlling over 50% of market revenue in 2026. These companies leverage established clinical networks, regulatory expertise, and integrated NGS–bioinformatics platforms. Significant R&D investments drive innovations in multi-gene urinary biomarker assays and AI-based variant interpretation. Strategic collaborations with hospitals and reference laboratories enhance adoption and market penetration. Their focus on advanced diagnostics and precision medicine maintains a strong leadership position.

Regional and niche competitors, including Bio-Rad Laboratories, Natera, and Freenome, target specialized applications such as transplant monitoring and point-of-care testing. Regulatory compliance, clinical validation, and reimbursement complexity remain barriers for new entrants. Cloud-based bioinformatics and AI platforms allow software-centric players to enter without heavy lab infrastructure. Market consolidation is expected through acquisitions and strategic alliances. Partnerships between sequencing and analytics firms continue to enhance scalability and precision.

Key Industry Developments

- In February 2026, doctors and scientists at Newcastle Hospitals and Newcastle University developed a genetic test called the Newcastle MSI-Plus assay to detect cancers linked to Lynch syndrome, a hereditary cancer condition. The test analyzes DNA signals from a simple urine sample to identify early-stage urinary tract cancers before symptoms appear.

- In September 2025, researchers at Johns Hopkins Medicine developed a non-invasive urine-based biomarker test to detect prostate cancer using specific RNA markers found in urine samples. The assay demonstrated high diagnostic performance, identifying prostate cancer in about 91% of cases while improving accuracy compared with traditional screening methods.

- In August 2025, Codex Genetics partnered with Pacific Edge to introduce the Cxbladder suite of genomic urine tests for bladder cancer diagnosis across hospitals and clinics in Hong Kong. The non-invasive tests, including Cxbladder Detect, Monitor, and Triage, analyze genetic biomarkers to support early detection, risk stratification, and patient monitorin

Companies Covered in Genomic Urine Testing Market

- Illumina, Inc.

- Roche Diagnostics

- Thermo Fisher Scientific

- QIAGEN N.V.

- Bio-Rad Laboratories

- Agilent Technologies

- Natera, Inc.

- Guardant Health

- Exact Sciences

- ArcherDx

- Pacific Biosciences

- Oxford Nanopore Technologies

- Myriad Genetics

Frequently Asked Questions

The global genomic urine testing market is projected to reach US$ 1.1 billion in 2026.

Escalating cancer prevalence worldwide, liquid biopsy adoption, and NGS platform advancements are driving the market.

The market is poised to witness a CAGR of 11.1% from 2026 to 2033.

Healthcare technology strengthening in Asia Pacific, AI-bioinformatics integration, and direct-to-consumer testing are opening major opportunities.

Roche, Qiagen, Guardant Health, Illumina, Bio-Rad Laboratories, and Nater are a few among the leading players in the market.