- Specialty & Fine Chemicals

- Forging Lubricants Market

Forging Lubricants Market Size, Share, and Growth Forecast 2025 - 2032

Forging Lubricants Market by Material Type (Steel, Aluminium, Magnesium, Brass, Others), Process Type (Hot Forging, Cold Forging), Product Type (Graphite based, Non-Graphite based), Solvent Type (Water based, Oil based, Soap based), Industry (Automotive, Aerospace, Industrial Machinery, Energy, Others), Regional Analysis, 2025 - 2032

Forging Lubricants Market Size and Trend Analysis

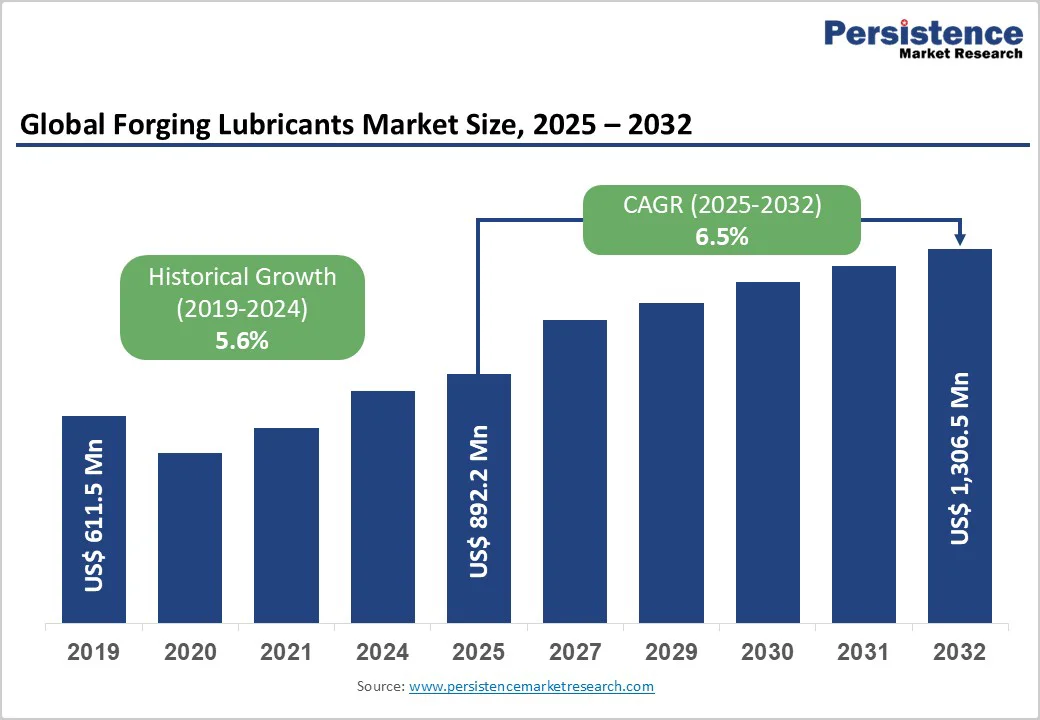

The global forging lubricants market size is likely to value US$ 892.2 million in 2025 and is projected to reach US$ 1,306.5 million, growing at a CAGR of 5.6% between 2025 and 2032.

The market expansion is primarily driven by the growing demand from the automotive and aerospace sectors, where precision metalworking requires advanced lubrication solutions to enhance production efficiency and component quality.

Rising industrialization in emerging economies, particularly in the Asia Pacific combined with technological advancements in lubricant formulations designed for extreme pressure and temperature conditions, continues to strengthen market growth.

Key Industry Highlights:

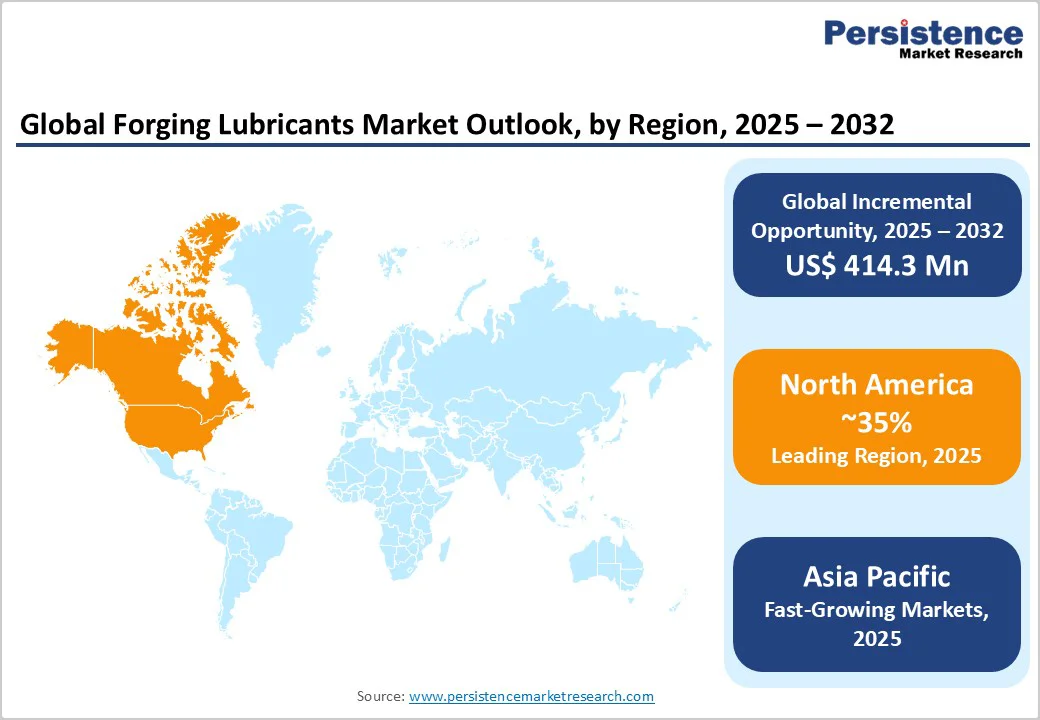

- Leading Region: North America leads the forging lubricants market with around 35% share, driven by a strong automotive and aerospace base, advanced manufacturing infrastructure, and stringent environmental compliance encouraging premium lubricant adoption.

- Fastest Growing Markets: Asia Pacific accounts for roughly 32% share and is the fastest-growing region, propelled by surging automotive output in China and India, expanding aerospace manufacturing, and increased investment in advanced forging technologies.

- Dominant Material Segment: Steel forging lubricants capture about 45% share, supported by widespread use across automotive, industrial machinery, and energy sectors, representing the majority of global forging volume.

- Fastest Growing Process Segment: Cold forging, holding around 38% share, is the fastest-growing process type, driven by automakers’ shift toward EV components and lightweighting initiatives requiring high-performance lubricants.

- Key Opportunity: Electric vehicle component forging presents a major growth avenue, as rising EV production demands specialized lubricants for precision aluminum and magnesium alloy components with tight dimensional tolerances.

| Key Insights | Details |

|---|---|

| Forging Lubricants Market Size (2025E) | US$ 892.2 million |

| Market Value Forecast (2032F) | US$ 1,306.5 million |

| Projected Growth CAGR (2025 - 2032) | 6.5% |

| Historical Market Growth (2019 - 2024) | 5.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Accelerating Automotive Production and Lightweighting Initiatives

The automotive industry’s ongoing push toward lightweighting to enhance fuel efficiency and reduce emissions is significantly driving the demand for advanced forging lubricants. In 2024, global automotive production reached nearly 81 million vehicles, with automakers increasingly using aluminum and magnesium alloys for complex, lighter components. These materials require specialized lubrication to maintain precision, dimensional stability, and surface finish during hot and cold forging operations.

The growing focus on electric vehicles further amplifies lubricant demand, as lightweight structural parts are essential for improving battery performance and range. Manufacturers are integrating forging operations with advanced lubricant technologies that reduce friction, minimize die wear, and extend tool life. This integration has become a key differentiator in automotive manufacturing competitiveness worldwide.

Aerospace and Defense Sector Expansion with High-Performance Requirements

The aerospace sector’s steady expansion is creating lucrative opportunities for forging lubricant suppliers. The industry is projected to produce around 10,000 commercial aircraft over the next decade, generating high demand for precision-forged components such as engine parts, landing gear, and structural elements. These applications require lubricants capable of performing reliably under extreme temperature and pressure conditions.

Strict regulatory standards set by the FAA and EASA necessitate high-performance lubricants that ensure metallurgical consistency, surface integrity, and component traceability. Additionally, the rising defense budgets and the expansion of aerospace manufacturing hubs in the Asia Pacific and the Middle East are fueling further growth. This trend underscores the increasing need for advanced forging lubricants tailored for demanding aerospace and defense applications.

Barrier Analysis - Environmental Regulations and Transition to Sustainable Formulations

Stringent environmental regulations in key regions such as the European Union, North America, and Asia are presenting significant challenges for the forging lubricants market. Policies like the EU’s REACH directive and the U.S. EPA’s restrictions on volatile organic compounds (VOCs) and hazardous substances are compelling manufacturers to reformulate traditional oil-based lubricants. These rules increase compliance costs and complicate formulation processes for lubricant producers striving to meet environmental and performance standards simultaneously.

To adapt, manufacturers are investing in R&D to develop bio-based and water-based alternatives that reduce environmental impact without compromising lubrication quality. However, the transition phase introduces additional economic strain on both suppliers and end users. Upgrading equipment and adjusting production processes for new formulations temporarily slows market adoption, especially in highly regulated markets.

Volatility in Raw Material Prices and Supply Chain Disruptions

The forging lubricants market faces substantial constraints from fluctuating raw material costs and supply chain instability. Petroleum-derived base oils, synthetic additives, and essential minerals form the backbone of lubricant production, making prices highly sensitive to crude oil market volatility. Frequent variations in Brent crude prices directly affect manufacturing expenses, squeezing profit margins and limiting pricing flexibility for lubricant producers.

Global supply chain disruptions exacerbated by transportation bottlenecks, geopolitical tensions, and material shortages have further intensified these challenges. Unstable logistics and cost pressures disrupt production schedules and strain inventory management. In developing economies, where pricing remains a critical purchasing factor, these fluctuations significantly hinder market expansion and profitability for both manufacturers and end users.

Opportunity - Emerging Demand in Electric Vehicle Manufacturing and Advanced Lightweight Materials

The accelerating shift toward electric mobility is opening new avenues for innovation in forging lubricants. With global EV production reaching around 14 million units in 2024, automakers are increasingly relying on forging processes for critical components such as battery housings, motor shafts, and lightweight structural frames. These applications often involve aluminum and magnesium alloys that require advanced lubrication to prevent material adhesion, reduce die wear, and maintain dimensional precision vital for EV performance and safety.

The rapid expansion of EV manufacturing hubs in China, India, and Southeast Asia is driving large-scale investments in forging infrastructure and capacity. This evolution creates lucrative opportunities for lubricant suppliers to develop high-performance, eco-friendly formulations tailored to EV component forging. Such products can command premium pricing by aligning with manufacturers’ sustainability commitments and carbon-reduction targets.

Technological Advancements in Graphite-Based and Nano-Lubricant Formulations

Continuous advancements in lubrication technology are presenting strong opportunities for growth in the forging lubricants market. Nano-structured formulations incorporating graphite and metallic nanoparticles are delivering remarkable improvements in friction reduction, load-bearing capacity, and heat dissipation during high-pressure forging operations. These lubricants enable extended tool life, superior surface finish, and better process stability, particularly under demanding hot- and cold-forging conditions.

Collaborations between research institutions and lubricant producers are accelerating innovation, with multiple nano-lubricant patents filed in 2024. Moreover, advanced graphite-based lubricants are gaining prominence in precision cold-forging applications where consistency and speed are essential. Companies investing in next-generation formulations that demonstrate measurable performance gains stand to capture a competitive edge, offering value through productivity enhancement and reduced maintenance costs.

Category-wise Analysis

Material Type Insights

Steel dominates the forging lubricants market, accounting for nearly 45% of the total share, primarily due to its extensive use in automotive, industrial machinery, and energy applications. Millions of tons of steel components are forged annually for parts such as crankshafts, connecting rods, and transmission components. The segment benefits from mature process technologies, established supply chains, and widespread industrial infrastructure supporting consistent lubricant demand.

Aluminum alloys are the fastest-growing material type as industries increasingly prioritize lightweighting and fuel efficiency. These alloys require advanced lubricants to prevent sticking and ensure a superior surface finish. Brass and other specialty metals make up the remaining share, catering to niche industrial and mechanical applications.

Process Type Analysis

Hot forging dominates the market with approximately 62% share, driven by its use in shaping large, complex, high-strength components across automotive, aerospace, and heavy machinery sectors. Hot forging lubricants must withstand extreme temperatures exceeding 1,000°C, offering oxidation resistance and high thermal stability to maintain tool life and part integrity.

Cold forging is the fastest-growing process type due to its ability to produce precise and high-strength components without secondary machining. It improves efficiency and material utilization, particularly in electric vehicle production, driving demand for advanced cold-forging lubricants that reduce tool wear and ensure smooth surface quality.

Product Type Analysis

Graphite-based lubricants hold the leading position with roughly 58% market share, favored for their superior high-temperature stability, lubrication efficiency, and load-bearing capacity. Their ability to form protective films under extreme pressure makes them indispensable for forging automotive and aerospace components requiring precision and durability.

Non-graphite lubricants are the fastest-growing product type as industries shift toward cleaner manufacturing. These advanced formulations use synthetic base stocks and eco-friendly additives, offering excellent lubrication without graphite residue, making them ideal for cold forging and precision part applications.

Solvent Type Analysis

Oil-based lubricants lead the market with around 53% share, owing to their high viscosity control, thermal stability, and superior performance in traditional hot and warm forging operations. They remain the most preferred option across automotive and heavy industrial sectors where consistent lubrication under extreme conditions is crucial.

Water-based lubricants, represent the fastest-growing segment as manufacturers move toward sustainable and safer alternatives. Technological advancements in emulsification and additive chemistry have significantly enhanced their performance, enabling adoption in various forging applications previously dominated by oil-based products.

Industry Analysis

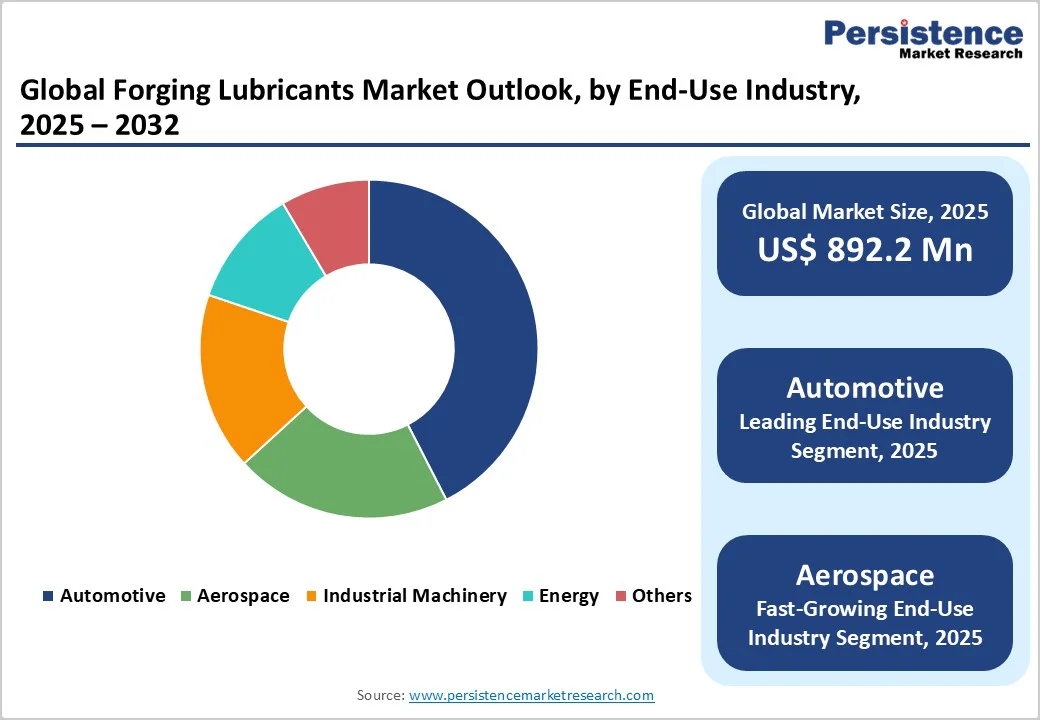

The automotive sector dominates the forging lubricants market, capturing around 48% share due to massive global vehicle production and reliance on forged components for engines, transmissions, and suspension systems. The sector’s demand is driven by lightweighting initiatives and just-in-time production strategies, ensuring continuous lubricant consumption.

The aerospace industry, accounting for nearly 22% of the market, represents the fastest-growing end-use segment. Growth is primarily driven by surging aircraft production, increased investment in defense manufacturing, and the adoption of high-performance alloys that require advanced lubrication during precision forging. Additionally, rising demand for lightweight forged components in next-generation aircraft engines and landing gear systems is accelerating lubricant consumption in this segment.

Regional Insights

North America Forging Lubricants Trends

North America leads the global forging lubricants market with around 35% share, supported by its robust automotive, aerospace, and industrial manufacturing sectors. The U.S. dominates regional demand, with strong production hubs in the Midwest and South advancing EV and lightweight component forging. Strict EPA environmental standards are accelerating the adoption of sustainable, water-based, and bio-based formulations, driving continuous R&D investment from lubricant suppliers to ensure regulatory compliance and high performance.

Aerospace and defense forging operations in the U.S. and Canada sustain demand for premium-grade lubricants offering superior thermal stability and clean residue characteristics. The region’s integration of Industry 4.0 and predictive maintenance technologies enhances lubricant performance monitoring and process optimization, strengthening North America’s leadership position in the global market.

Europe Forging Lubricants Trends

Europe represents a mature, highly regulated market where environmental compliance and Europe holds roughly 25% share of the global forging lubricants market, with Germany, the UK, France, and Spain being key contributors. The region’s mature industrial ecosystem emphasizes sustainability and environmental compliance, driven by EU directives such as REACH and VOC emission limits. These regulations are pushing manufacturers toward bio-based and water-based formulations, spurring strong R&D activity among regional lubricant suppliers.

Germany dominates due to its robust automotive and industrial machinery sectors, while the UK and France drive demand through aerospace forging. European manufacturers prefer high-performance lubricants offering superior efficiency and durability. Additionally, regional emphasis on the circular economy and carbon neutrality goals continues to promote innovation in recycled and renewable lubricant materials.

Asia Pacific Forging Lubricants Trends

Asia Pacific holds approximately 32% of the global market and remains the fastest-growing region, driven by rapid industrialization and large-scale automotive and EV production. China dominates regional demand, supported by strong aerospace expansion and increasing adoption of precision forging technologies for

and magnesium components.

India’s expanding automotive exports, growing forging infrastructure, and modernization of industrial manufacturing are further accelerating lubricant consumption. Japan and South Korea sustain steady demand through high-tech forging industries, while Southeast Asian nations-such as Thailand, Vietnam, and Indonesia-are emerging as new hubs for forging capacity expansion. Competitive labor costs, policy incentives, and industrial investments continue to establish Asia Pacific as the primary growth engine of the global forging lubricants market through 2032.

Competitive Landscape

The forging lubricants market is moderately consolidated, with a mix of global, mid-tier, and regional manufacturers competing across diverse end-use industries. Leading players focus on product innovation, advanced formulation development, and strong distribution networks, while regional suppliers emphasize customized solutions and competitive pricing to address localized market needs.

Competition is intensifying around sustainability and environmental compliance, with rising investments in bio-based and water-based lubricants. Differentiation is achieved through superior thermal stability, reduced environmental footprint, and technical support services. Industry consolidation continues as companies pursue acquisitions and partnerships to expand portfolios and develop integrated, performance-driven lubrication solutions.

Key Market Developments

- In May 2025, FUCHS Petrolub SE announced expansion of its forging lubricant production capacity in Southeast Asia, investing in advanced manufacturing facilities to serve growing automotive and industrial machinery demand in the region, supporting regional market expansion objectives.

- In March 2025, Henkel Corporation launched comprehensive sustainability initiative for forging lubricants portfolio, committing to 30% reduction in VOC emissions by 2027 and transitioning 50% of product line to bio-based formulations meeting environmental regulatory requirements across major markets.

- In September 2024, Klüber Lubrication introduced next-generation nano-structured forging lubricants incorporating graphite particles at microscopic scale, demonstrating 25% reduction in tool wear and 18% improvement in surface finish quality for automotive applications compared to conventional formulations.

Companies Covered in Forging Lubricants Market

- Henkel Corporation

- FUCHS Petrolub SE

- Quaker Houghton

- Chem-Trend L.P.

- CONDAT S.A.

- The Lubrizol Corporation

- ExxonMobil Corporation

- Croda International Plc

- Klüber Lubrication

- Lubriplate Lubricants Company

- TotalEnergies SE

- Idemitsu Kosan Co., Ltd.

- Houghton International Inc.

- Petrofer Chemie H.R. Fischer GmbH + Co. KG

- Chemtool Incorporated

Frequently Asked Questions

The global forging lubricants market was valued at US$ 892.2 million in 2025 and is projected to reach US$ 1,306.5 million by 2032, growing at a CAGR of 5.6%.

Key drivers include automotive lightweighting, aerospace expansion, EV manufacturing growth, and rising demand for sustainable, bio-based lubricants.

Steel forging lubricants command approximately 45% market share as the dominant segment due to extensive application across automotive powertrains, industrial machinery components, and energy sector equipment manufacturing.

North America leads the global forging lubricants market by 35%, supported by its strong automotive and aerospace industries and strict environmental regulations.

Electric vehicle component forging offers the largest opportunity, requiring specialized lubricants for aluminum and magnesium alloys.

Major players include Henkel, FUCHS, Quaker Houghton, Chem-Trend, CONDAT, Lubrizol, ExxonMobil, Klüber, TotalEnergies, and Idemitsu Kosan.