- Specialty & Fine Chemicals

- Foaming Agents Market

Foaming Agents Market Size, Share, and Growth Forecast 2026 - 2033

Foaming Agents Market By Agent Type (Surfactants, Blowing Agents), By Foam Type (Polyurethane Foam, Polystyrene Foam, Phenolic Foam, Polyethylene Foam, and Others), End-user (Healthcare & Pharmaceuticals, Building & Construction, Food & Beverage, Cosmetics & Personal Care, Automotive, Packaging, Oil & Gas, Mining, and Aerospace & Defense), and by Regional Analysis, 2026 - 2033

Foaming Agents Market Size and Trend Analysis

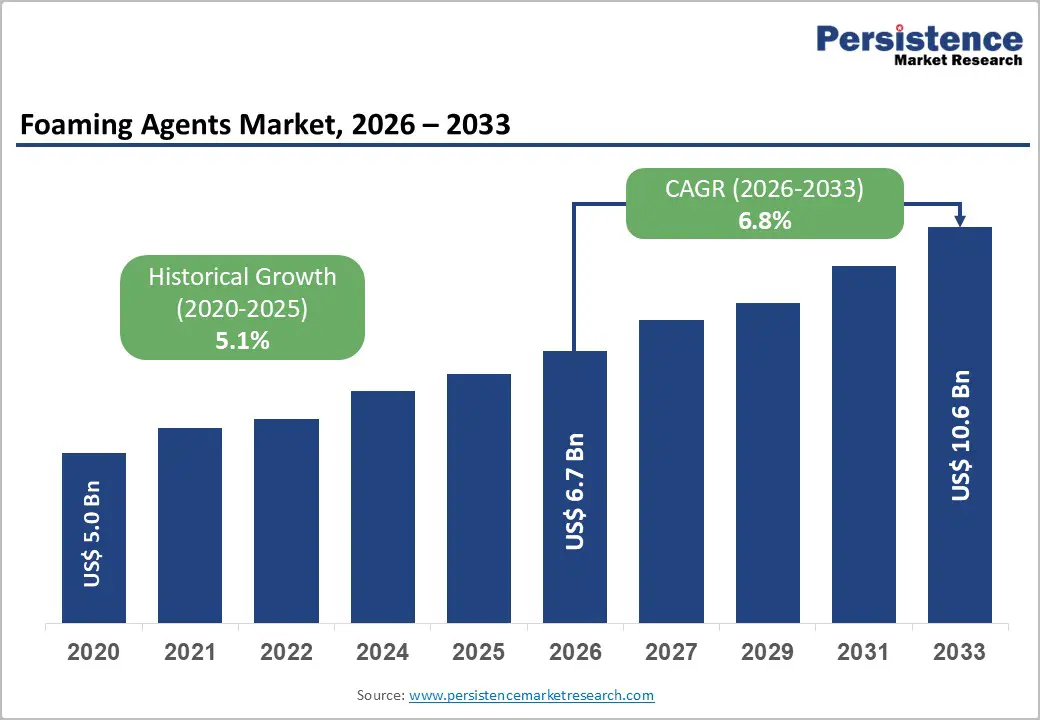

The global foaming agents market is projected to reach US$ 6.7 billion in 2026 and US$ 10.6 billion by 2033, growing at a CAGR of 6.8% from 2026 to 2033.

Robust growth is underpinned by rising demand for high-performance foam materials in building & construction, packaging, automotive, and healthcare applications, where foaming agents are critical to achieving desired density, insulation, cushioning, and weight-reduction properties.

Key Industry Highlights:

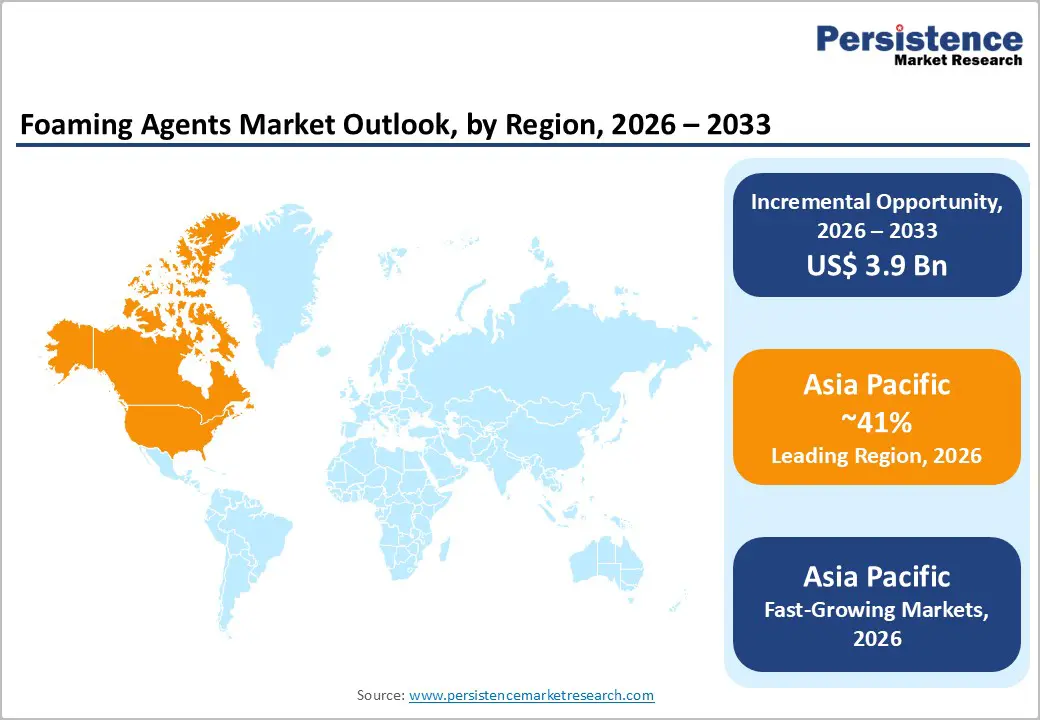

- Leading Region: Asia Pacific is the leading region in foaming agents market, accounting for 41% share with CAGR of 8%, propelled by rapid urbanization, strong construction and automotive output, and leadership in packaging foams for e-commerce and electronics manufacturing across China, India, Japan, and ASEAN.

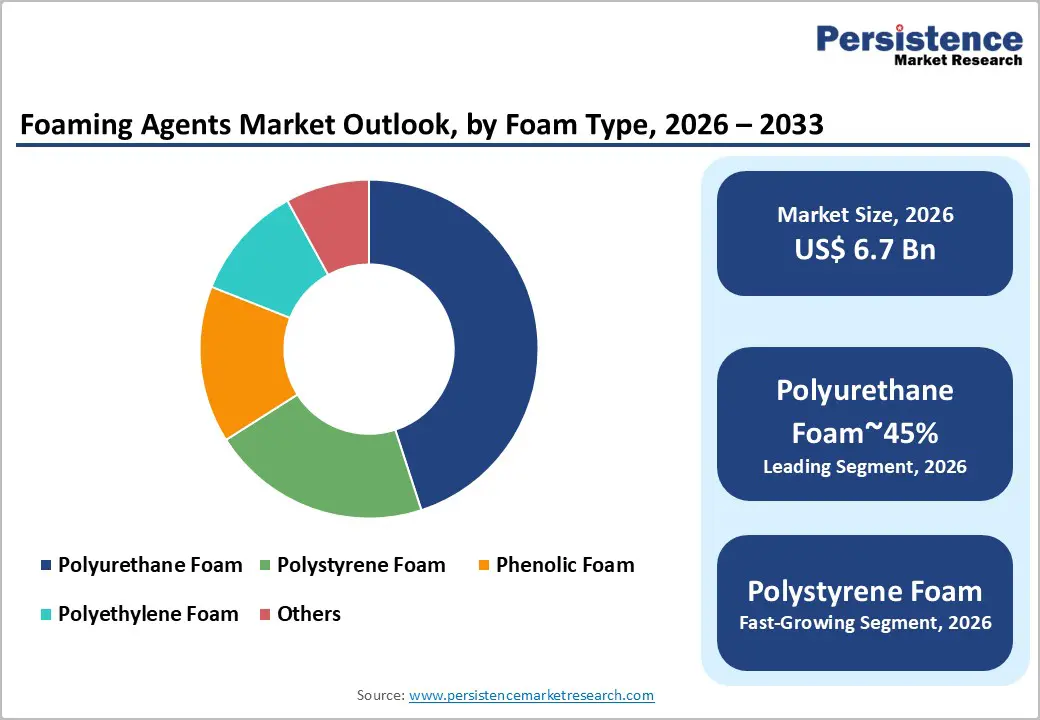

- Leading Form Type: Polyurethane Foam category is the dominant segment, leveraging its broad use in insulation, furniture, automotive, and appliances, and accounting for an estimated 45% share of foaming-agent consumption globally.

- Fastest-Growing End-user Category: By End-user, building & construction is the fastest-growing segment, driven by strict energy-efficiency regulations, retrofit programs, and increased penetration of foam-based insulation and sealants in both developed and emerging markets.

- Key Market Opportunity lies in low-GWP and bio-based foaming agents, as regulators and brand owners push for climate-friendly, circular materials, rewarding innovators that deliver high performance with reduced environmental footprints.

| Key Insights | Details |

|---|---|

| Foaming Agents Market Size (2026E) | US$ 6.7 Billion |

| Market Value Forecast (2033F) | US$ 10.6 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.8% |

| Historical Market Growth (2020 - 2025) | 5.1% |

Market Dynamics

Drivers - Stricter Global Energy-Efficiency Building Codes are Accelerating Demand for High-Performance Insulation Foams and Advanced Foaming Agents

Energy-efficiency regulations across major economies are a key long-term driver for the foaming agents market, as foamed plastics play a critical role in modern insulation solutions. Materials such as rigid polyurethane foam are widely used in roofs, walls, floors, and HVAC systems because they deliver high thermal resistance and effective air sealing. The global building insulation materials market is projected to reach approximately US$ 66.2 billion by 2033, growing at a CAGR of around 4.7%, reflecting strong policy pressure to reduce energy consumption and carbon emissions from buildings.

Spray polyurethane foam and other foamed insulation products depend heavily on physical and chemical blowing agents, along with specialized surfactants, to form closed-cell structures that enhance insulation performance. As building codes become stricter and governments expand large-scale retrofit programs, particularly in North America and Europe, demand for high-performance insulation solutions continues to rise. This directly supports higher consumption of advanced foaming agents designed to meet evolving energy-efficiency and durability standards.

Rapid Growth of E-Commerce and Lightweight Protective Packaging is Driving Sustained Consumption of Foaming Agents Globally

The rapid expansion of global e-commerce and omnichannel retail is significantly increasing the use of protective foamed plastics in packaging applications, thereby supporting steady growth in foaming agent demand. Foamed materials are widely used in secondary and tertiary packaging because they provide cushioning, shock absorption, and thermal protection for products during transportation.

The global packaging foams market is valued at more than US$ 18 billion and is expected to grow at an annual rate of around 6%, driven by strong demand from food, electronics, and pharmaceutical logistics. Asia Pacific accounts for roughly 26% or more of global packaging foam demand, with China, India, and Japan serving as major production and consumption hubs. This regional scale supports high-volume use of surfactant foaming agents and chemical blowing agents across polyurethane, polystyrene, and polyethylene foam manufacturing lines. The ongoing focus on lightweight packaging and logistics efficiency further reinforces long-term demand.

Restraints - Tightening Climate Regulations and HFC Phase-Downs are Reshaping Foaming Agent Formulations and Increasing Compliance Costs

Tightening environmental regulations on ozone-depleting substances and high-global-warming-potential blowing agents are restraining growth in traditional foaming chemistries. International frameworks aligned with the Montreal Protocol and the Kigali Amendment require countries to phase down hydrofluorocarbons commonly used in insulation foams. As a result, manufacturers are increasingly required to shift toward low-GWP alternatives such as hydrofluoroolefins and CO2-based systems.

While these alternatives offer environmental benefits, the transition often involves reformulating foam systems, adjusting processing conditions, and investing in new equipment. These changes can raise production costs and slow adoption, particularly in price-sensitive markets. Smaller manufacturers may face additional challenges due to limited capital and technical resources. As a result, regulatory compliance creates short-term barriers for certain foaming agent portfolios, even though it supports long-term sustainability goals across the industry.

Rising Plastic Waste Concerns and Circular-Economy Regulations are Limiting Demand for Traditional Foamed Plastic Materials

Growing concerns about plastic waste and microplastics are creating regulatory and reputational challenges for the foaming agents value chain. Many foamed plastic products used in packaging and construction are lightweight but bulky, making them difficult and costly to collect, transport, and recycle. Contamination further reduces the economic feasibility of mechanical recycling, particularly for materials such as expanded polystyrene. In response, several cities and regions have introduced restrictions or bans on certain foam products.

At the same time, brand owners and policymakers are committing to circular-economy targets, which encourage the use of recyclable, reusable, or alternative materials. This shift places pressure on suppliers of conventional foaming chemistries unless they can demonstrate improved recyclability, reduced environmental impact, or compatibility with advanced recycling technologies. Without innovation, these sustainability concerns may limit demand growth in specific end-use segments.

Opportunities - Growing Preference for Sustainable, Low-GWP, and Bio-Based Foaming Agents Creates Better Long-Term Opportunities

The global shift toward climate-friendly and sustainable materials presents a strong growth opportunity for next-generation foaming agents. Demand is rising for low-GWP blowing agents and bio-based surfactants that meet both performance and environmental requirements. Global demand for foamed plastic insulation, valued at approximately US$ 27 billion, is expected to grow steadily through 2033 as energy-efficient construction expands. End users increasingly prefer solutions that align with green-building certifications, life-cycle assessments, and corporate net-zero commitments.

Suppliers that successfully commercialize HFO-based blowing agents, CO2-expanded systems, and surfactants derived from renewable feedstocks are well-positioned to gain market share from legacy chemistries. These advanced solutions support compliance with evolving regulations while maintaining insulation efficiency, durability, and processing performance. As sustainability becomes a core purchasing criterion, low-impact foaming technologies are expected to command premium positioning across construction, appliances, and cold-chain infrastructure.

High-Lightweighting and Electrification Trends Boost Demand for Advanced High-Performance Foams in Mobility & Electronics

Lightweighting trends in automotive, aerospace, and electronics are driving demand for advanced foam materials with tailored mechanical, acoustic, and thermal properties. Polyurethane and microcellular foams are increasingly used in vehicle seating, noise and vibration control, battery protection, and impact absorption, particularly in electric vehicles.

Asia Pacific is emerging as a major manufacturing hub for both automotive and electronics production, supporting strong regional demand for high-performance foams. The microcellular polyurethane foam segment is expected to grow rapidly in this region, supported by industrialization and expanding EV output. This creates attractive opportunities for specialized non-ionic and amphoteric surfactant foaming agents that enable fine cell structures, consistent quality, and improved durability. As manufacturers focus on performance optimization and weight reduction, demand for precision foaming chemistries is expected to rise across mobility and electronics applications.

Category-wise Analysis

By Agent Type Insights

Within the agent type category, surfactants are expected to account for around 55% of the global foaming agents market, outpacing blowing agents and other chemistries. This dominance is driven by the versatility of surfactants in controlling foam stability, cell size, and structure across multiple resin systems. Non-ionic and anionic surfactants are widely used in polyurethane, polystyrene, and polyethylene foams for applications ranging from flexible cushioning to rigid insulation.

Compared with traditional gaseous blowing agents, surfactants face fewer climate-related regulatory constraints, supporting more stable demand growth. As manufacturers seek to optimize foam density, surface finish, and processing efficiency, particularly in packaging, furniture, and automotive applications, the need for advanced surfactant formulations continues to increase. These factors collectively reinforce the leadership position of surfactants within the overall foaming agents market.

By Foam Type Insights

By foam type, polyurethane foam is estimated to hold approximately 45% of global foaming agent consumption, maintaining a clear lead over polystyrene, phenolic, and polyethylene foams. Polyurethane foams are used in both flexible and rigid forms across a wide range of applications, including furniture, bedding, automotive interiors, refrigeration, and building insulation. These end-use sectors are among the largest global consumers of foamed plastics. This regional scale further strengthens polyurethane’s market dominance and drives consistent demand for both surfactant and blowing-agent systems. As insulation and comfort requirements continue to rise, polyurethane foam remains central to the consumption of foaming agents worldwide.

By End-user Insights

By end-user category, building & construction is projected to account for approximately 32% of the foaming agents market by 2026. This leadership position is supported by the growing use of foam-based insulation and sealants in residential, commercial, and industrial construction. The global building insulation materials market is expected to reach around US$ 66.2 billion by 2032, with foam products representing a significant share due to their superior thermal efficiency and air-barrier performance.

Governments across North America, Europe, and parts of the Asia-Pacific are strengthening building codes and promoting energy-efficient retrofits, which increase demand for polyurethane spray foam, polystyrene boards, and other foam systems. These applications consume substantial volumes of foaming agents, ensuring that building and construction remains the largest and most stable end-use segment in the market.

Regional Insights

North America Foaming Agents Market Trends

In North America, demand for foaming agents is strongly influenced by advanced building codes and a well-established innovation ecosystem for polyurethane and other foamed plastics. The region leads the global spray polyurethane foam segment, with the United States having the largest installed base of systems and the largest number of contractors. Adoption is supported by regulations such as the International Energy Conservation Code and state-level standards in markets like California and Florida.

These policies promote higher insulation performance, air sealing, and moisture control in both new construction and retrofit projects. As a result, demand continues to grow for advanced blowing agents and surfactant systems that meet performance and compliance requirements. Beyond construction, North America’s large automotive, appliance, and packaging industries further support foaming agent consumption. Strong R&D capabilities position the region as a key market for premium, regulation-compliant foaming solutions.

Europe Foaming Agents Market Trends

In Europe, the foaming agents market is shaped by strict climate and energy-efficiency regulations, particularly under the European Union’s Energy Performance of Buildings Directive. Countries such as Germany, France, Spain, and the U.K. are seeing steady growth in foam insulation usage as they work toward carbon-neutral building stock. The European foam insulation market is valued at around US$ 5.7 billion, highlighting the scale of opportunity for compliant foaming agents.

EU regulations on chemicals and fluorinated gases are accelerating the transition away from high-GWP blowing agents toward HFO-based and CO2-based alternatives. This regulatory environment favors suppliers that can offer fully compliant systems combining optimized blowing agents with tailored surfactant packages. Demand is especially strong in applications such as cold storage, district heating, and prefabricated modular construction across Western and Northern Europe.

Asia Pacific Foaming Agents Market Trends

Asia Pacific is the largest and fastest-growing regional market for foaming agents, supported by rapid urbanization, infrastructure development, and strong manufacturing activity. The region accounts for over 45% of the global polyurethane foam market and dominates packaging foams, holding roughly 26% of global packaging foam demand.

Growth is driven by expanding e-commerce, electronics production, and consumer goods manufacturing across China, Japan, India, and ASEAN countries. Asia Pacific is also emerging as a major hub for microcellular polyurethane foam and other advanced foam technologies used in automotive parts, footwear, and electronics. National energy-efficiency programs, expanding cold-chain logistics, and modern retail formats further support demand for insulation and cushioning foams. These trends collectively strengthen regional demand for advanced foaming agents with improved performance and environmental profiles.

Competitive Landscape

The foaming agents market is moderately consolidated at the global level, with leading chemical producers controlling significant shares in key blowing-agent and surfactant chemistries, alongside a long tail of regional and application-specialist suppliers. Large players emphasize portfolio breadth, regulatory compliance, and technical service, investing in low-GWP blowing agents, tailored surfactant packages for polyurethane and polystyrene foams, and application-specific formulations for spray insulation, packaging, and automotive components.

Increasingly, strategic moves include backward integration into key feedstocks, joint development programs with foam manufacturers and OEMs, and business models centered on solution-selling rather than commodity sales, with digital tools and life-cycle assessments used as differentiators.

Key Market Developments

- In January, 2024: BASF SE announced expanded production capabilities for low-GWP polyurethane foam systems in Asia to support demand in construction and appliance insulation.

- In June 2024, Evonik Industries AG introduced new silicone surfactants tailored for high-performance polyurethane foam used in automotive and bedding, targeting improved cell structure and reduced VOC emissions.

- In September 2023, The Dow Chemical Company reported investments in next-generation HFO-based blowing agents to help customers meet evolving building-energy and climate regulations in North America and Europe.

Companies Covered in Foaming Agents Market

- BASF SE

- The Dow Chemical Company

- Huntsman Corporation

- Evonik Industries AG

- Solvay S.A.

- Arkema Group

- Akzo Nobel N.V.

- Wacker Chemie AG

- Clariant AG

- Lanxess AG

- Chemours Company

- Adeka Corporation

- Shin-Etsu Chemical Co. Ltd.

- SABIC

- Foam Supplies Inc.

- Covestro AG

- Celanese Corporation

- DIC Corporation

Frequently Asked Questions

The global foaming agents market is projected to be worth around US$ 6.7 Billion in 2026 and reach approximately US$ 10.6 Billion by 2033, registering a forecast CAGR of about 6.8%.

The growing use of foam‑based insulation and sealing materials in building & construction, supported by stringent energy‑efficiency regulations and large retrofit programs that require high‑performance polyurethane and related foams, highlights a rise in demand.

By foam type, Polyurethane Foam is the leading segment, accounting for an estimated 45% share of global foaming‑agent consumption due to its extensive use in insulation, furniture, automotive, and appliance applications.

Asia Pacific currently dominates the market, driven by strong construction, automotive, and packaging foam demand in China, India, Japan, and ASEAN, and it also represents the fastest‑growing regional opportunity.

A key opportunity lies in developing low‑GWP, climate‑friendly, and bio‑based foaming agents that meet tightening environmental regulations while delivering high insulation and cushioning performance across construction, appliances, and mobility applications.

Major companies include BASF SE, The Dow Chemical Company, Huntsman Corporation, Evonik Industries AG, Solvay S.A., Arkema Group, Akzo Nobel N.V., Wacker Chemie AG, Clariant AG, Lanxess AG, Chemours Company, Adeka Corporation, Shin-Etsu Chemical Co. Ltd., SABIC, and Foam Supplies Inc., among others.