- Specialty & Fine Chemicals

- Fluorosurfactants Market

Fluorosurfactants Market Size, Share, and Growth Forecast, 2026 – 2033

Fluorosurfactants Market by Product Type (Non-Ionic, Anionic, Cationic, Amphoteric), Application (Paints & Coatings, Adhesives & Sealants, Caulks, Waxes & Polishes, Polymers, Foamers, Inks, Others), End-User (Construction & Architecture, Automotive, Consumer Goods, Oilfields, Electronics, Others), and Regional Analysis for 2026-2033

Fluorosurfactants Market Share and Trends Analysis

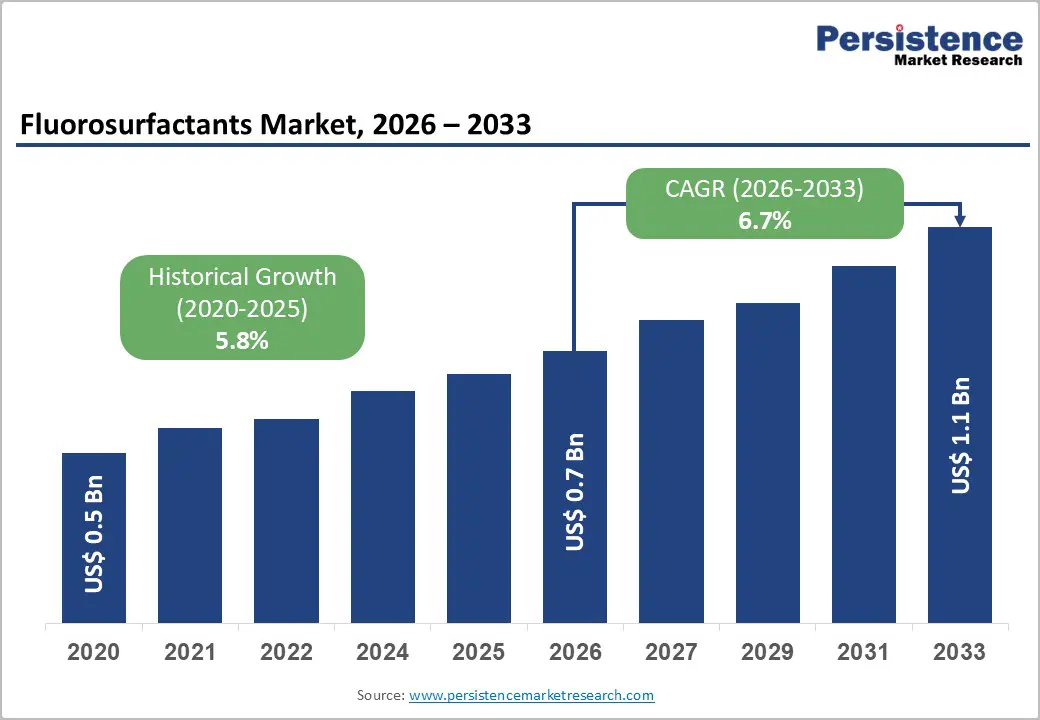

The global fluorosurfactants market size is likely to be valued at US$ 0.7 billion in 2026, and is projected to reach US$ 1.1 billion by 2033, growing at a CAGR of 6.7% during the forecast period 2026−2033. Market expansion is primarily driven by increasing adoption of performance-enhancing surfactants across industrial and consumer applications. Rising demand for coatings, adhesives, and sealants that require superior wetting, spreading, and surface tension control is encouraging manufacturers to integrate fluorosurfactants into formulations.

Technological integration in chemical synthesis and formulation processes is accelerating scalability and production efficiency, enabling cost-effective delivery of high-purity fluorosurfactants. Regulatory alignment with environmental and safety standards ensures consistent market accessibility across regions. End-user industries such as construction, automotive, electronics, and consumer goods are expanding adoption due to material performance benefits, reliability, and longevity. In addition, enhanced awareness of the functional role of fluorosurfactants in industrial performance optimization is influencing procurement decisions, especially in applications requiring specialized surface activity.

Key Industry Highlights

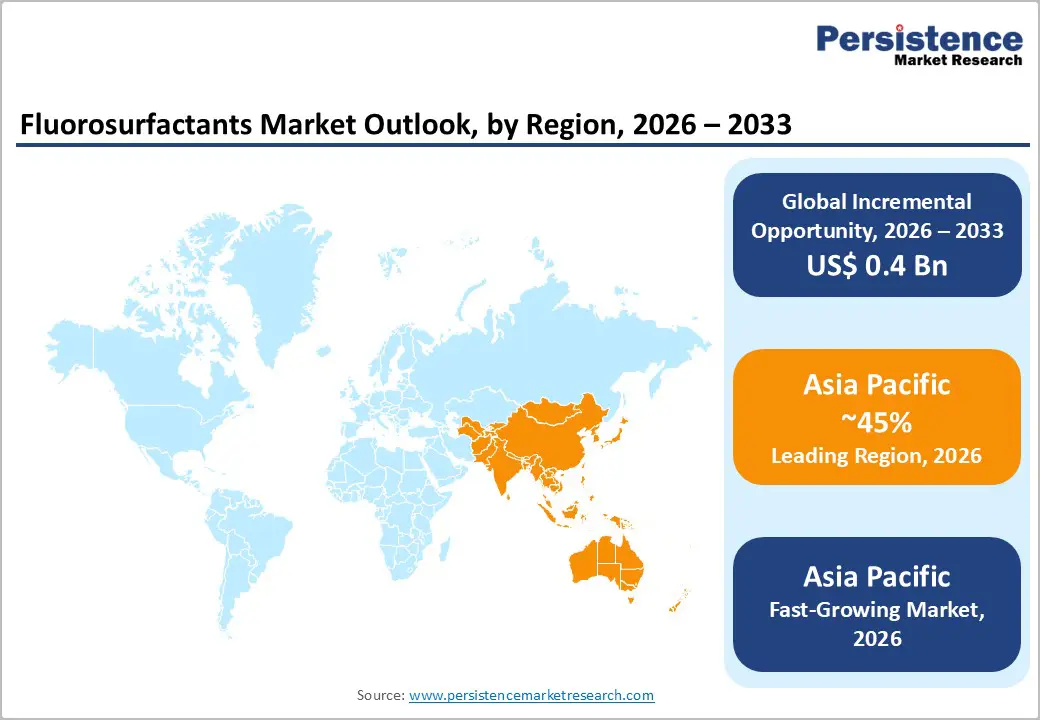

- Dominant Region: Asia Pacific is expected to dominate with a share of nearly 45% in 2026, driven by high-volume manufacturing and strong demand from electronics, automotive, pharmaceuticals, and specialty coatings.

- Fastest-growing Market: Asia Pacific is forecasted to be the fastest-growing 2026-2033 market, stimulated by the wide adoption of environmentally compliant solutions and rising demand for precision coatings.

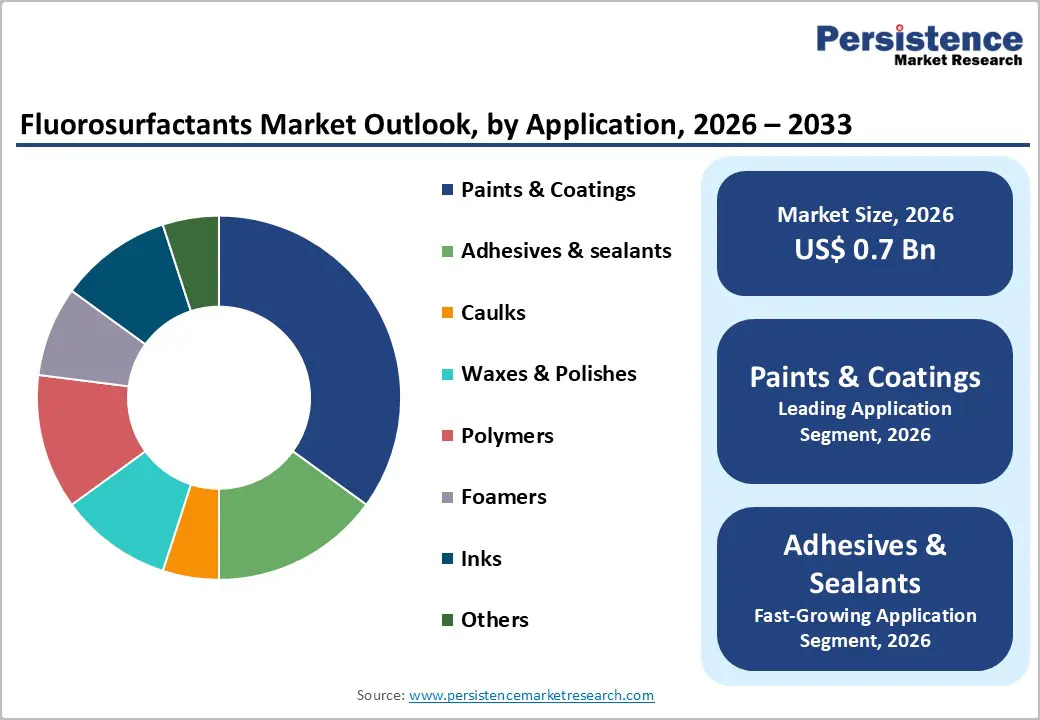

- Leading Application: Paints & coatings are expected to lead with over 35% share in 2026, fueled by the huge demand for functional additives.

- Fastest-growing Application: Adhesives & sealants are projected to be the fastest-growing segment through 2033, driven by automotive, electronics, and construction expansion.

| Global Market Attributes | Key Insights |

|---|---|

| Fluorosurfactants Market Size (2026E) | US$ 0.7 Bn |

| Market Value Forecast (2033F) | US$ 1.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancements in Chemical Formulations

Innovation in chemical formulation transforms efficiency and versatility of fluorosurfactants, enabling their application across highly specialized industrial processes. Advanced molecular design allows precise control over surface activity, wetting, and spreading properties, enhancing product performance in coatings, cleaning agents, and industrial treatments. Tailored formulations improve chemical stability and reduce environmental impact, meeting increasingly stringent regulatory standards. Continuous refinement of synthesis methods and the integration of nanotechnology expand functional capabilities, creating opportunities for high-performance solutions that were previously unattainable with conventional surfactants.

Enhanced formulation techniques reduce production costs and improve scalability, supporting consistent quality across large-volume applications. Research-driven improvements in solubility, thermal tolerance, and compatibility with diverse chemical systems enable wider adoption across multiple sectors. This capability to deliver predictable and reliable performance fosters operational efficiency and strengthens supply chain confidence. The convergence of computational modeling, automated experimentation, and green chemistry principles accelerates development cycles, positioning innovation as a primary driver for adoption and growth.

Industrial Expansion and End-User Demand Growth

Industrial growth drives the procurement of high-performance chemical inputs that enhance the effectiveness of formulations in manufacturing processes. Fluorosurfactants deliver exceptional surface-tension reduction, wetting, spreading and stability under extreme operational conditions, attributes increasingly specified in coatings, adhesives, textiles, cleaning agents and precision electronics production where quality standards are stringent. Government regulation highlights the scale of production and use of the broader chemical class that includes many fluorosurfactants. For example, under the U.S. Toxic Substances Control Act (TSCA) Section-8(a)(7) rule, manufacturers and importers of per-and polyfluoroalkyl substances (PFAS) must report detailed production, use and exposure information to the Environmental Protection Agency (EPA).

End-user sectors such as construction, automotive, aerospace and semiconductors translate final product performance expectations into material specifications that demand reliable surfactant functionality. Fluorosurfactants contribute to product features such as enhanced durability, resistance to environmental stressors and improved process yields, making them integral to formulation strategies where alternative chemistries cannot meet technical demands. Rising output in these downstream sectors correlates with increased demand for formulation ingredients that improve product competitiveness and compliance with quality standards.

Environmental and Health Concerns

Regulatory focus on fluorinated surfactants derives from the inherent properties of PFAS, the chemical class that includes many such surfactants. PFAS are extremely resistant to natural breakdown once released into the environment, often described by agencies as persistent substances that remain for decades to centuries in soil, water and organisms. Their mobility across environmental media results in widespread contamination. For example, in Europe, monitoring shows a large share of rivers, lakes and coastal waters have levels of PFAS above environmental quality standards, indicating pervasive pollution. Groundwater and drinking water are especially vulnerable to PFAS infiltration, demanding advanced and costly treatment to protect public water supplies.

Public health evidence further informs government action. Health authorities recognize that certain PFAS accumulate in living organisms and are associated with adverse outcomes such as reproductive effects, disruptions to endocrine (hormone) systems, and increased cancer risk in humans. Regulatory bodies classify many PFAS as substances of very great concern in chemical management frameworks, with restrictions focused on reducing human and wildlife exposure through environmental pathway,s including water, food and air. Persistent presence of these chemicals in the environment and in biological systems means exposure reduction is a long-term challenge for public health policy.

Regulatory Restrictions and Limited Biodegradability

Government regulation intensifies due to the intrinsic persistence and environmental mobility of PFAS, which include fluorinated surface-active agents. Strong carbon-fluorine bonds render these compounds highly resistant to natural breakdown, leading to accumulation in water, soil, air, and biological systems over extended periods. The U.S. EPA reports ongoing monitoring of PFAS across approximately 10,000 water systems to assess their prevalence and guide risk mitigation efforts, reflecting the scale of environmental presence documented by national authorities. Regulatory frameworks such as the U.S. Toxic Substances Control Act and analogous European Union chemical policies impose stringent controls on production, importation, and permitted applications of persistent fluorinated chemicals to protect public health and environmental quality.

Limited biodegradability of fluorinated surfactants creates long-term environmental liabilities that influence regulatory decisions and corporate risk strategies. Scientific and regulatory bodies classify PFAS as “persistent” because of their minimal natural degradation over time, necessitating engineered solutions for removal and containment. These characteristics constrain use in applications with exposure potential in consumer and industrial settings, as policymakers seek to reduce environmental loading and associated health concerns. Restrictive measures include phased bans on specific uses, mandatory technology upgrades, and enhanced disclosure obligations that can delay product launches and increase capital expenditure.

Opportunity Analysis- Policy Shifts toward Eco-Friendly Alternatives

Regulatory frameworks worldwide are increasingly favoring chemicals with lower environmental impact, driving demand for surfactants that meet stringent sustainability standards. Restrictions on perfluorinated compounds and persistent organic pollutants are prompting manufacturers to reformulate products with biodegradable and less bioaccumulative alternatives. Companies that adopt such eco-conscious chemicals gain a competitive advantage through regulatory compliance, reduced liability, and enhanced brand reputation. Investors are also showing a preference for organizations demonstrating alignment with global sustainability goals, further strengthening the economic rationale for transitioning to environmentally safer formulations.

Growing awareness of ecological preservation among end-use industries fuels demand for safer chemical inputs. Industries such as coatings, textiles, and personal care are seeking solutions that minimize their environmental footprint while maintaining performance characteristics, including reduced surface tension, improved wetting, and enhanced emulsification. This trend opens opportunities for suppliers to innovate high-performance alternatives that satisfy both operational efficiency and environmental responsibility. The adoption of greener chemicals can reduce disposal costs and waste-management challenges, thereby creating operational efficiencies.

Emerging Market Industrialization

Rapid industrialization in emerging economies is driving significant demand for specialty chemical solutions that enhance operational efficiency and product performance. Expanding manufacturing sectors such as automotive, electronics, textiles, and construction require advanced surface-active agents to improve coating uniformity, reduce material waste, and enable high-performance finishes. Rising infrastructure investments and expanding production capacities in these regions drive consistent demand for performance-driven chemical additives, creating a scalable growth opportunity for companies targeting industrial clients.

Urbanization and rising disposable income are driving increased demand for consumer and industrial products with advanced surface properties. Industries such as electronics and personal care are incorporating specialized agents to achieve enhanced durability, aesthetic appeal, and functional performance. Concurrently, regulatory focus on process efficiency and environmental compliance in emerging regions encourages the adoption of chemicals that reduce emissions, improve material efficiency, and support sustainable manufacturing practices.

Category-wise Analysis

Product Type Insights

Non-ionic fluorosurfactants are likely to be the leading product type with approximately 40% revenue market share in 2026, driven by superior chemical stability, compatibility with diverse formulations, and widespread industrial acceptance. Non-ionic variants exhibit reduced reactivity with acidic or basic substrates, making them suitable for coatings, adhesives, and sealants in construction and automotive applications. Industrial manufacturers favor non-ionic surfactants for predictable performance, consistent wetting, and reduced process variability. End-users also prefer these formulations for their long-term stability and lower environmental reactivity, facilitating compliance with regulatory requirements. Continuous innovation in molecular design enables enhanced spreading and surface tension control, reinforcing adoption across high-performance coatings, specialty adhesives, and polymer applications.

Cationic fluorosurfactants are expected to witness the fastest growth between 2026 and 2033, due to expanding applications in antimicrobial coatings, electronics, and specialty adhesives. Cationic variants provide electrostatic interaction benefits, enhancing adhesion and material protection, especially in coatings for medical devices, electronics, and automotive interiors. Growth is further supported by technological convergence with nanomaterials and bioactive formulations, enabling multifunctional surfaces. End-users value cationic surfactants for performance in moisture control, surface sanitization, and anti-fouling properties, which are increasingly required across industrial and consumer applications.

Application Insights

Paints & coatings are poised to lead with a forecasted 35% of the fluorosurfactants market revenue share in 2026, owing to the widespread need for functional additives that improve wetting, spreading, and substrate adhesion. Fluorosurfactants enhance coating uniformity, reduce defects, and improve durability, making them critical for industrial and decorative coatings. Construction and automotive end-users require high-performance paints for protection against weathering, corrosion, and abrasion, reinforcing the adoption of fluorosurfactants. Manufacturers integrate these surfactants to optimize formulation efficiency and ensure regulatory compliance with VOC limits and environmental safety standards.

Adhesives & sealants are anticipated to be the fastest-growing application segment between 2026 and 2033, driven by expansion in automotive, electronics, and construction sectors. Fluorosurfactants improve substrate wetting, bonding consistency, and material longevity, enabling stronger adhesion and reduced defects in high-performance assemblies. Adoption is reinforced by increasing complexity of industrial materials, requiring precise formulation and multifunctional performance. Manufacturers targeting specialty adhesives integrate fluorosurfactants for enhanced process control and product differentiation.

Regional Insights

North America Fluorosurfactants Market Trends

In North America, the demand for fluorosurfactants is expected to be steady throughout the 2026-2033 forecast period, supported by strong industrial diversification, advanced manufacturing technologies, and high-value end-use sectors requiring precise surface functionality. Electronics, aerospace, automotive, and pharmaceuticals drive consumption of high-performance agents that enhance coating uniformity, durability, and functional efficiency. Well-established chemical production infrastructure allows large-scale synthesis of specialty surfactants with consistent quality and purity. Integration of research and development with manufacturing operations accelerates innovation in functional coatings, semiconductor processing, and precision cleaning solutions. Industrial focus on process optimization, waste reduction, and operational efficiency encourages use of agents that improve material utilization and reliability, supporting long-term cost efficiency for manufacturers.

The North America fluorosurfactants market growth is predicted to gather traction as the adoption of environmentally compliant and high-performance chemical solutions across industrial segments increases. Expansion of electronics and pharmaceutical sectors drives demand for surfactants that enhance product functionality while meeting strict safety and regulatory requirements. Investment in continuous production technologies, automated quality control, and process monitoring ensures consistent output and operational resilience. Collaboration between chemical producers and industrial clients enables development of customized formulations, enhancing application-specific performance.

Europe Fluorosurfactants Market Trends

Europe remains a strategically significant market for fluorosurfactants, owing to robust regulatory frameworks, advanced manufacturing capabilities, and high demand from industrial sectors requiring specialized chemical solutions. Strict environmental and safety standards encourage adoption of low-emission, high-purity surfactants in electronics, automotive coatings, pharmaceuticals, and specialty chemicals. Mature industrial infrastructure enables precise formulation and large-scale production, supporting consistent quality while meeting stringent operational requirements. Close collaboration between research institutions and chemical producers accelerates innovation in applications such as water- and oil-repellent coatings, semiconductor processing, and precision cleaning solutions.

High-value sectors, particularly electronics and pharmaceuticals, require surfactants that enhance performance while minimizing environmental impact, creating demand for tailored formulations. Investment in advanced production technologies, including continuous processing and automated quality control, ensures consistent output and supports premium pricing strategies. Expansion of specialty coatings and growing focus on product differentiation and durability reinforce consumption of performance-driven chemical solutions. Collaboration between chemical producers and industrial clients enables customized applications, promoting innovation in surface treatments and functional coatings while maintaining regulatory compliance and operational efficiency.

Asia Pacific Fluorosurfactants Market Trends

Asia Pacific is expected to dominate with an estimated 45% of the fluorosurfactants market share in 2026, reflecting extensive industrial capacity, high-volume chemical manufacturing, and strong integration of research and development with production capabilities. Expansion across electronics, automotive, pharmaceuticals, and specialty coatings sectors is driving demand for performance-oriented surface-active agents that enhance durability and functional efficiency. Concentrated industrial hubs support cost-effective supply chains, enabling competitive pricing while ensuring consistent quality and regulatory compliance. Advanced production technologies and bulk procurement systems further reinforce operational efficiency, positioning the region as a central contributor to global supply and innovation in high-performance fluorosurfactants.

Asia Pacific is also forecasted to be the fastest-growing regional market for fluorosurfactants between 2026 and 2033, stimulated by the rising adoption of environmentally compliant and high-performance chemical solutions. Increasing demand for precision coatings in electronics and automotive industries requires low-surface-energy agents that improve product longevity and functionality. Strategic collaboration between chemical producers and industrial consumers facilitates tailored formulations, enhancing application-specific performance and supporting premium pricing strategies.

Competitive Landscape

The global fluorosurfactants market exhibits a moderately consolidated structure, with leading companies collectively accounting for an estimated 55% of global revenue. Key players, including The Chemours Company, Solvay, 3M, AGC Chemicals Americas, Inc., Arkema, and DAIKIN INDUSTRIES, Ltd., leverage strong production capacities, robust research and development pipelines, and extensive global distribution networks to maintain market influence. These companies focus on the development of high-performance surfactants for applications across electronics, automotive, aerospace, pharmaceuticals, and specialty coatings, enabling them to capture premium segments and maintain competitive advantage. Investments in process optimization, automation, and continuous production technologies support consistent product quality and scalability, while ongoing innovation in environmentally compliant and specialty formulations strengthens market positioning.

The market is primarily served by mid-scale and regional manufacturers that focus on niche and application-specific segments such as specialty adhesives, electronics, antimicrobial coatings, and precision cleaning agents. These players often differentiate through customized formulations, flexible production capabilities, and targeted service offerings that cater to specific industrial requirements. While these companies capture smaller market shares individually, collectively they address specialized demand that complements the scale of leading corporations. The competitive landscape is shaped by technological expertise, regulatory compliance, and capacity to meet diverse performance requirements, which collectively determine market dynamics.

Key Industry Developments

- In October 2025, researchers from the University of Queensland’s Australian Institute for Bioengineering and Nanotechnology (AIBN) published new work on the design and synthesis of fluorosurfactants for microfluidic droplet-based bioapplications, highlighting advanced molecular architectures that enhance droplet stability, responsiveness, and biocompatibility for next-generation biological and chemical assays.

- In August 2025, HT&K’s Anti-Fire Group introduced HT1157, HT1157D, and HT1470 fluorosurfactants as direct drop-in replacements for Chemours’ discontinued Capstone firefighting foam products, allowing formulators to continue production without recertification and maintain performance equivalence.

- In July 2025, AGC launched a new high-performance fluoroelastomer in its AFLAS™ FFKM series, manufactured entirely without surfactants or fluorinated polymerization solvents using proprietary technology, meeting growing demand for cleaner production while maintaining equivalent performance to conventional products.

Companies Covered in Fluorosurfactants Market

- The Chemours Company

- Solvay

- 3M

- AGC Chemicals Americas, Inc.

- Arkema

- DAIKIN INDUSTRIES, Ltd.

- Clariant

- BASF

- Mitsubishi Chemical Group Corporation.

Frequently Asked Questions

The global fluorosurfactants market is projected to reach US$ 0.7 billion in 2026.

Rising demand for specialty coatings, electronics, and industrial applications is driving the market.

The market is poised to witness a CAGR of 6.7% from 2026 to 2033.

Rapid industrialization, increasing demand for high-performance coatings, and adoption of environmentally compliant chemical solutions are presenting key market opportunities.

Some of the key market players include The Chemours Company, Solvay, 3M, AGC Chemicals Americas, Inc., Arkema, and DAIKIN INDUSTRIES, Ltd.