- Medical Devices

- Fluidic Devices Market

Fluidic Devices Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Global Fluidic Devices Market by Product (Microchips, Flow & Pressure Sensors, Flow & Pressure Controllers, Microfluidic Valves, Micropumps, Microfluidic-based-Devices and Others), by Application (Disease Diagnostics, Pharma & Life Science Research & Manufacturing, and Others ), by End User (Hospitals, Diagnostic Centers, Pharmaceutical & Biotechnology Companies, and Academic & Research Institutes), and Regional Analysis from 2026 to 2033

Fluidic Devices Market Share and Trend Analysis

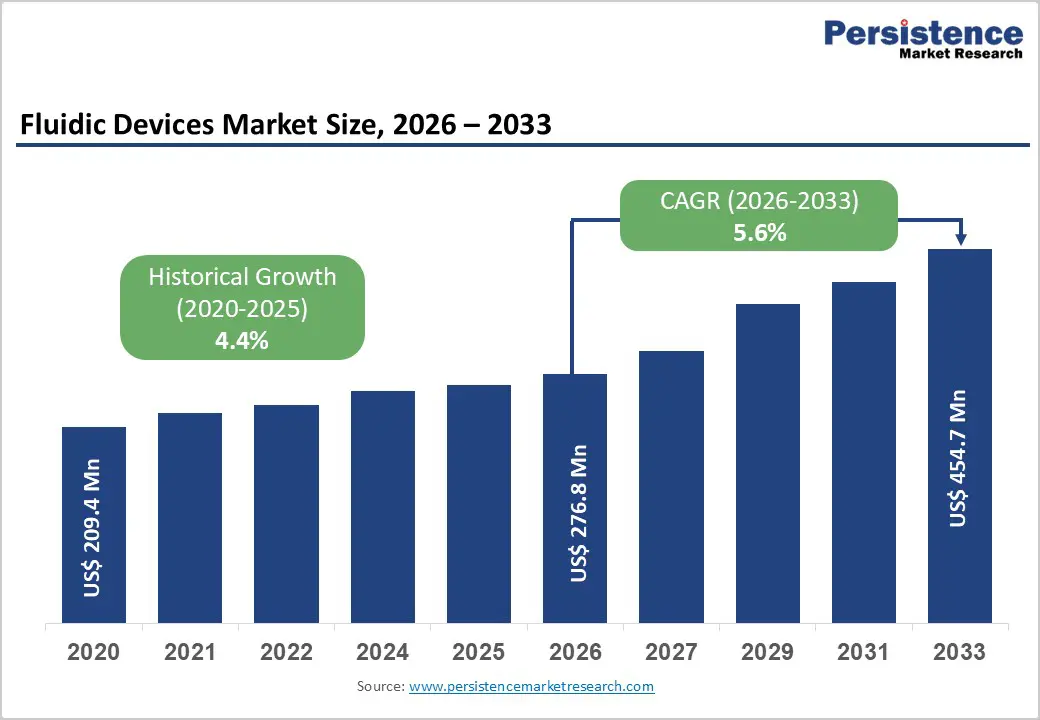

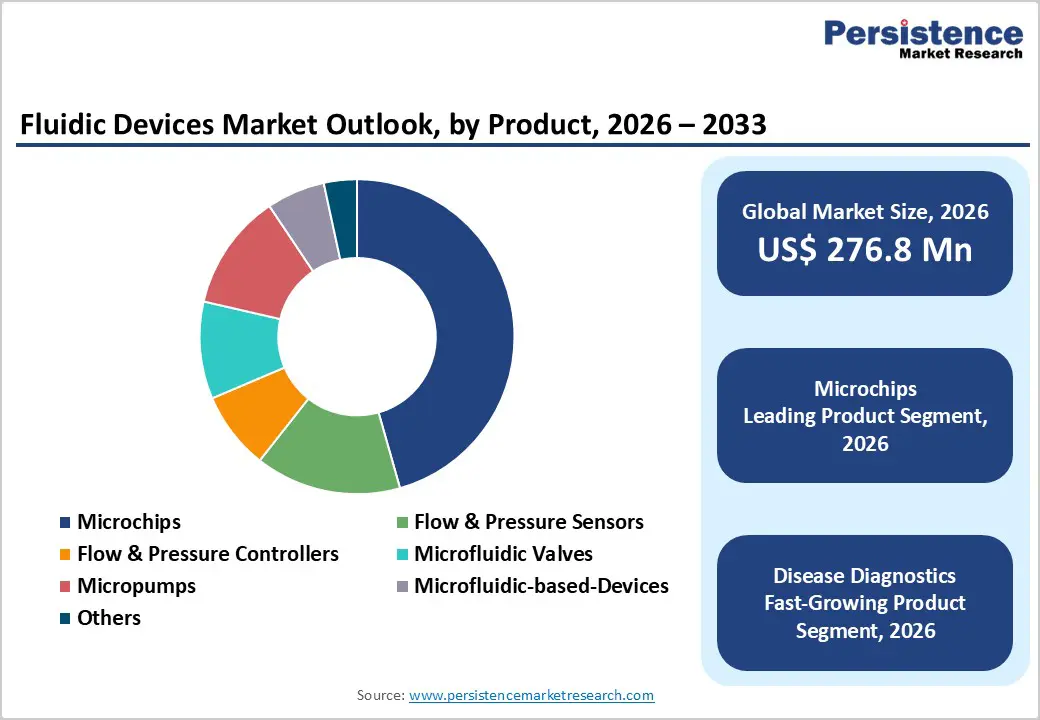

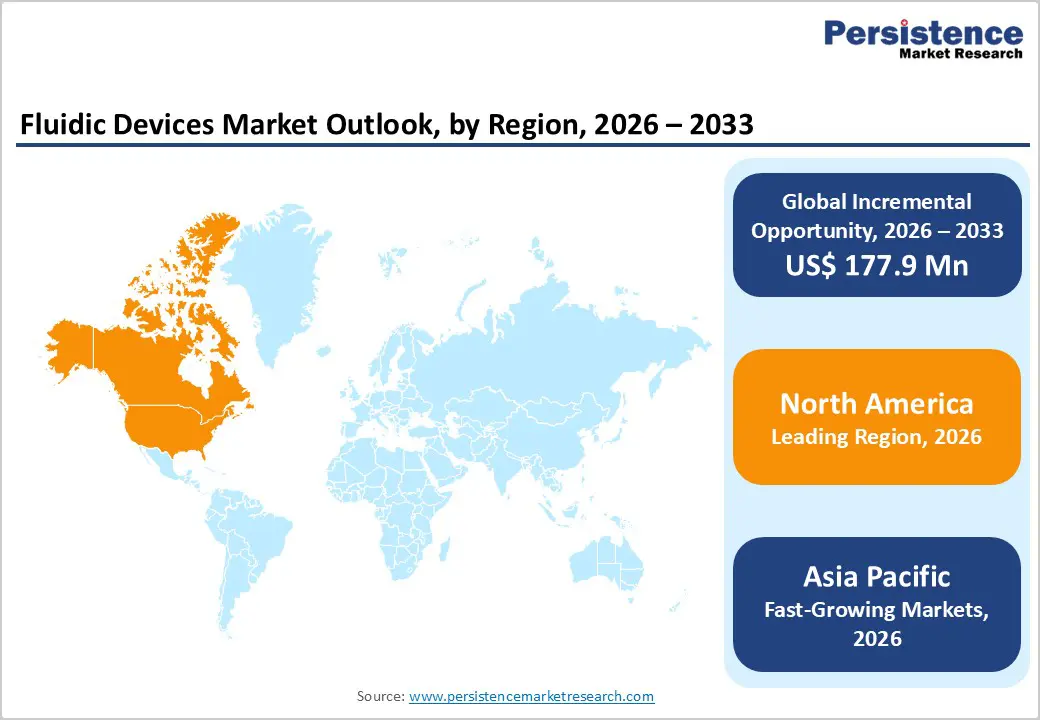

The global fluidic devices market size is estimated to grow from US$ 276.8 Mn in 2026 to US$ 454.7 Mn by 2033. The market is projected to record a CAGR of 5.6% during the forecast period from 2026 to 2033.

Global demand for fluidic devices is increasing steadily, driven by the growing need for rapid, accurate, and automated fluid handling across diagnostics, life sciences, and research applications. Rising prevalence of chronic and infectious diseases, along with increasing emphasis on early detection and preventive healthcare, is significantly expanding testing volumes worldwide. Aging populations, urban lifestyles, and higher disease screening rates are further strengthening demand for advanced diagnostic solutions that rely on precise fluid control. Fluidic devices are widely adopted across hospitals, diagnostic centers, and research laboratories due to their ability to improve analytical accuracy, reduce reagent usage, shorten turnaround times, and support miniaturized testing platforms.

Increasing adoption of point-of-care and decentralized diagnostics is further accelerating market growth. Expansion of laboratory automation, growth of high-throughput testing facilities, and rising penetration of integrated diagnostic systems are reinforcing global demand. Continuous technological advancements, including enhanced microfabrication techniques, improved flow and pressure control, and integration with sensors and digital analytics, are improving device performance and reliability. Additionally, expanding healthcare and research infrastructure in emerging markets, coupled with rising investments in life sciences and biotechnology, is supporting long-term growth of the global fluidic devices market.

Key Industry Highlights• Leading Region: North America holds the largest share at 47.3%, supported by advanced healthcare infrastructure, high adoption of laboratory automation and point-of-care diagnostics, strong research funding, favorable reimbursemen

- Leading Region: North America holds the largest share at 47.3%, supported by advanced healthcare infrastructure, high adoption of laboratory automation and point-of-care diagnostics, strong research funding, favorable reimbursement environments, and widespread use of fluidic technologies across hospitals, diagnostic laboratories, and research institutions.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to increasing disease burden, rapidly aging populations, improving healthcare access, urbanization, rising investment in diagnostic infrastructure, and expansion of private laboratories and research facilities.

- Leading Product Segment: Microchips dominate the market due to their central role in microfluidic systems, high adoption in diagnostics and research, scalability for mass testing, and compatibility with automated and point-of-care platforms.

- Fastest-Growing Product Segment: Flow & pressure sensors are growing rapidly as demand increases for precise fluid regulation, real-time monitoring, and enhanced system reliability across advanced diagnostic and analytical applications.

- Leading Application Segment: Disease diagnostics remains the top segment, driven by high testing volumes, increasing focus on early disease detection, and widespread deployment of fluidic-based diagnostic platforms in clinical settings.

- Fastest-Growing Application Segment: Pharma & life science research & manufacturing is scaling rapidly due to growing R&D activity, expanding drug discovery pipelines, increased use of microfluidics in cell analysis and screening, and rising demand for automated and high-throughput research tools.

| Global Market Attributes | Key Insights |

|---|---|

| Fluidic Devices Market Size (2026E) | US$ 276.8 Mn |

| Market Value Forecast (2033F) | US$ 454.7 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

Market Dynamics

Driver – Growing Demand for Rapid Diagnostics, Laboratory Automation, and Precision Fluid Control

Market expansion is primarily driven by the rising demand for fast, accurate, and reliable diagnostic solutions across healthcare, research, and industrial settings. Increasing prevalence of chronic and infectious diseases has intensified the need for early detection, routine screening, and continuous monitoring, placing fluidic devices at the center of modern diagnostic workflows. Hospitals, diagnostic centers, and laboratories are rapidly adopting microfluidic platforms to improve throughput, reduce reagent consumption, and enhance analytical accuracy. The global shift toward point-of-care and decentralized testing further accelerates demand, as fluidic devices enable compact, portable, and automated diagnostic systems.

Advances in microfabrication, sensor integration, and flow-control technologies have significantly improved device precision and repeatability, strengthening confidence among clinicians and researchers. Growing investment in life sciences research, genomics, proteomics, and drug discovery has also expanded application scope beyond diagnostics. Additionally, automation in laboratory environments is increasing reliance on fluidic controllers, valves, and pumps to standardize workflows and reduce manual errors. Supportive regulatory frameworks for diagnostic innovation and increasing healthcare expenditure in developed markets continue to reinforce sustained adoption across multiple end-use segments.

Restraints – High System Costs, Technical Complexity, and Limited Adoption in Resource-Constrained Settings

Market growth faces constraints from the relatively high cost of advanced fluidic systems, particularly those integrated with automation, sensors, and analytical instruments. Initial capital investment for microfluidic platforms, precision flow controllers, and associated software can be substantial, limiting adoption among small laboratories and healthcare facilities with budgetary constraints. Maintenance requirements, calibration needs, and dependency on specialized consumables further increase total cost of ownership.

Technical complexity also poses challenges, as effective operation of fluidic devices often requires skilled personnel with expertise in system integration, calibration, and troubleshooting. In low-resource or rural settings, lack of trained professionals and limited access to advanced laboratory infrastructure restrict broader penetration. Standardization challenges, including variability in device formats, materials, and interfaces, can complicate interoperability across different platforms. Regulatory approval processes for diagnostic applications can be lengthy, delaying commercialization timelines. Additionally, concerns related to scalability, long-term reliability, and reproducibility in high-volume applications may limit adoption in certain industrial and clinical environments, particularly in emerging economies.

Opportunity – Expansion of Point-of-Care Testing, Emerging Market Growth, and Next-Generation Microfluidic Innovation

Significant growth opportunities are emerging from the rapid expansion of point-of-care testing and decentralized diagnostic models, where compact and efficient fluidic devices play a critical role. Increasing emphasis on preventive healthcare, home-based testing, and remote monitoring is creating strong demand for portable and user-friendly microfluidic platforms. Emerging markets across Asia Pacific, Latin America, and parts of the Middle East and Africa present substantial untapped potential, supported by rising healthcare investment, expanding diagnostic networks, and improving laboratory infrastructure.

Technological innovation represents another major opportunity, particularly through development of next-generation microfluidic devices with enhanced sensitivity, multi-analyte capability, and seamless integration with digital and AI-enabled analytical tools. Advancements in materials, such as low-cost polymers and disposable substrates, are improving affordability and scalability. Strategic collaborations between device manufacturers, diagnostic companies, and research institutions are accelerating product development and market entry. Additionally, increasing adoption of fluidic devices in pharmaceutical research, bioprocessing, and environmental testing is broadening the addressable market, supporting long-term and diversified revenue growth.

Category-wise Analysis

By Product, Microchips Lead Due to High Adoption in Miniaturized and High-Precision Fluid Handling

Microchips are projected to dominate the global fluidic devices market in 2026, accounting for a revenue share of 45.6%. Their leadership is primarily driven by widespread adoption across disease diagnostics, life science research, and lab-on-chip applications, where precise fluid manipulation at micro-scale is critical. Microchips enable rapid sample processing, reduced reagent consumption, and high-throughput analysis, making them essential for point-of-care diagnostics and automated laboratory workflows. Continuous advancements in microfabrication techniques, material science, and integration with sensors and imaging systems have significantly enhanced performance reliability and scalability. Expanding use in genomics, proteomics, and cell-based assays further strengthens demand. Additionally, increasing preference for compact, portable, and disposable diagnostic platforms supports sustained adoption. Strong compatibility with digital health tools and analytical instruments, along with cost efficiency at scale, reinforces the dominant position of microchips within the global fluidic devices market.

By Application, Disease Diagnostics Dominates Due to Rising Demand for Rapid and Accurate Testing

The disease diagnostics segment is expected to dominate the global fluidic devices market in 2026, capturing a revenue share of 53.4%. This dominance is driven by the growing need for rapid, accurate, and decentralized diagnostic solutions across hospitals, diagnostic laboratories, and point-of-care settings. Rising prevalence of chronic and infectious diseases, coupled with aging populations globally, has significantly increased diagnostic testing volumes. Fluidic devices enable precise sample handling, faster turnaround times, and high sensitivity, which are critical for early disease detection and monitoring. Increased adoption of point-of-care testing, especially in emergency care and remote settings, further supports segment growth. Advancements in microfluidic diagnostic platforms, integration with biosensors, and automation have improved test accuracy and workflow efficiency. Additionally, growing awareness of preventive healthcare and routine screening programs continues to expand diagnostic applications, ensuring disease diagnostics remains the largest revenue-contributing segment.

By End User, Diagnostic Centers Lead Due to High Testing Volumes and Specialized Diagnostic Capabilities

Diagnostic centers are projected to dominate the global fluidic devices market in 2026, accounting for a revenue share of 34.0%. This leadership is driven by high diagnostic testing volumes, strong focus on routine and specialized testing, and widespread adoption of advanced fluidic and microfluidic technologies. Diagnostic centers are increasingly equipped with automated laboratory systems, point-of-care testing platforms, and high-throughput analyzers that rely on precise fluid handling for accurate and rapid results. Their operational efficiency, faster turnaround times, and cost-effective service models make them preferred choices for both patients and healthcare providers. Comprehensive diagnostic capabilities, including molecular diagnostics, immunoassays, and clinical chemistry, support broad application of fluidic devices. Higher capital investments enable diagnostic centers to adopt advanced flow control systems, microchips, and integrated diagnostic platforms. Strong referral networks, expanding preventive screening programs, and growing demand for decentralized diagnostics further reinforce the dominant position of diagnostic centers in the global fluidic devices market.

Region-wise Insights

North America Fluidic Devices Market Trends

North America is expected to dominate the global fluidic devices market with a value share of 47.3% in 2026, led primarily by the United States. The region benefits from a well-established healthcare and life sciences ecosystem, strong adoption of advanced diagnostic technologies, and high R&D investment intensity. Widespread use of point-of-care diagnostics, laboratory automation, and microfluidic platforms across hospitals, diagnostic laboratories, and research institutions drives sustained demand. A high prevalence of chronic diseases and strong emphasis on early diagnosis and preventive care further support market growth.

Favorable reimbursement policies and streamlined regulatory pathways accelerate commercialization of innovative fluidic technologies. The presence of leading manufacturers, robust academic–industry collaborations, and extensive clinical and translational research activities strengthen regional leadership. Continuous technological upgrades, integration of digital health solutions, and strong purchasing power ensure North America maintains its dominant position throughout the forecast period.

Europe Fluidic Devices Market Trends

The Europe fluidic devices market is expected to grow steadily, supported by strong public healthcare systems and increasing adoption of advanced diagnostic and research technologies. Countries such as Germany, the U.K., France, Italy, and Spain contribute significantly due to well-developed hospital infrastructure and strong academic research networks. Aging populations and rising incidence of chronic and infectious diseases are key drivers for diagnostic testing demand. Universal healthcare coverage across many European countries improves patient access to advanced diagnostic solutions, supporting broader adoption of fluidic devices.

Hospitals and diagnostic laboratories increasingly rely on microfluidic platforms to improve testing efficiency, accuracy, and cost-effectiveness. Strict regulatory and quality standards promote high product reliability and physician confidence. Growing investments in life science research, biobanking, and personalized medicine further support market expansion. Europe remains a mature and stable market with consistent demand across healthcare and research applications.

Asia Pacific Fluidic Devices Market Trends

The Asia Pacific fluidic devices market is expected to register a relatively higher CAGR of around 7.6% between 2026 and 2033, driven by rapid improvements in healthcare infrastructure and expanding diagnostic capacity. Rising prevalence of chronic diseases, increasing healthcare awareness, and aging populations across China, India, Japan, South Korea, and Australia are significantly increasing demand for advanced diagnostic technologies. Expansion of private hospitals, diagnostic chains, and research laboratories is enhancing adoption of fluidic devices.

Government initiatives focused on strengthening healthcare access, disease surveillance, and laboratory modernization further support market growth. Increasing local manufacturing, cost-effective device availability, and entry of global players are improving affordability and accessibility. Growing investment in life sciences research, biotechnology, and point-of-care diagnostics positions Asia Pacific as the fastest-growing regional market over the forecast period.

Market Competitive Landscape

The global fluidic devices market is highly competitive, with strong participation from companies such as Cellix Ltd., Elveflow, Nortis Inc., Fluigent SA, and PerkinElmer, Inc. These players leverage established global distribution networks, strong brand presence, and broad microfluidic and fluid control technology portfolios to address the growing demand for miniaturized, high-precision, and automated fluid handling solutions across diagnostics, life sciences, and research applications.

Their offerings focus on advanced microfluidic platforms, precise flow and pressure control, high system reliability, integration with analytical and imaging technologies, and compatibility with laboratory automation and point-of-care settings. Continuous technological innovation, regulatory compliance, product validation, performance accuracy, and adherence to international quality and manufacturing standards remain critical for sustaining competitive positioning in the global fluidic devices market.

Key Industry Developments:

- In September 2025, FluidAI received U.S. FDA 510(k) clearance for Origin™, an inline sensing system that enables real-time bedside monitoring of post-operative surgical effluent. The device connects to standard surgical drains, provides continuous pH data visualization, and can operate independently or integrate with FluidAI’s AI-enabled Stream Care™ Surgical Expert Suite.

Companies Covered in Fluidic Devices Market

- Cellix Ltd.

- Elveflow

- Nortis Inc.

- Fluigent SA

- Perkinelmer, Inc.

- Fluidic Analytics

- Blacktrace Holdings Ltd. (Dolomite Microfluidics)

- SynVivo, Inc.

- Emulatebio

- Micronit B.V.

- Emerson Electric Co.

- LUMICKS

- microfluidic ChipShop GmbH

- Bartels Mikrotechnik GmbH

- Others

Frequently Asked Questions

The global fluidic devices market is projected to be valued at US$ 276.8 Mn in 2026.

Rising adoption of point-of-care diagnostics and increasing use of microfluidic technologies in life science research and disease detection are driving the global fluidic devices market.

The global fluidic devices market is poised to witness a CAGR of 5.6% between 2026 and 2033.

Growing demand for lab-on-chip systems and decentralized diagnostics in emerging markets presents a significant growth opportunity for fluidic device manufacturers.

Cellix Ltd., Elveflow, Nortis Inc., Fluigent SA, and Perkinelmer, Inc. are some of the key players in the transcatheter heart valve replacement repair market.