- Executive Summary

- Global Flavored and Functional Water Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Market Dynamics

- Driver

- Restraint

- Opportunities

- Trends

- Macro-Economic Factors

- Global GDP Outlook

- Global Food & Beverage Industry Outlook

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- Value Added Insights

- Value Chain analysis

- Key Market Players

- Product Adoption Analysis

- Key Promotional Strategies by key players

- PESTLE Analysis

- Porter's Five Forces Analysis

- Regulatory and Technology Landscape

- Global Flavored and Functional Water Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Global Flavored and Functional Water Market Outlook: Product Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Product Type, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Product Type, 2026-2033

- Flavored Water

- Functional Water

- Market Attractiveness Analysis: Product Type

- Global Flavored and Functional Water Market Outlook: Ingredient

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Ingredient, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Ingredient, 2026-2033

- Vitamins & Minerals

- Botanical Extracts

- Electrolytes

- Antioxidants

- Others

- Market Attractiveness Analysis: Ingredient

- Global Flavored and Functional Water Market Outlook: Flavor

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Flavor, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Flavor, 2026-2033

- Citrus

- Berry

- Tropical

- Others

- Market Attractiveness Analysis: Flavor

- Global Flavored and Functional Water Market Outlook: Distribution Channel

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Distribution Channel, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Distribution Channel, 2026-2033

- Supermarkets / Hypermarkets

- Convenience Stores

- Online Retail

- Others

- Market Attractiveness Analysis: Distribution Channel

- Global Flavored and Functional Water Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Flavored and Functional Water Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- North America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) Forecast, by Product Type, 2026-2033

- Flavored Water

- Functional Water

- North America Market Size (US$ Bn) Forecast, by Ingredient, 2026-2033

- Vitamins & Minerals

- Botanical Extracts

- Electrolytes

- Antioxidants

- Others

- North America Market Size (US$ Bn) Forecast, by Flavor, 2026-2033

- Citrus

- Berry

- Tropical

- Others

- North America Market Size (US$ Bn) Forecast, by Distribution Channel, 2026-2033

- Supermarkets / Hypermarkets

- Convenience Stores

- Online Retail

- Others

- Europe Flavored and Functional Water Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Europe Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) Forecast, by Product Type, 2026-2033

- Flavored Water

- Functional Water

- Europe Market Size (US$ Bn) Forecast, by Ingredient, 2026-2033

- Vitamins & Minerals

- Botanical Extracts

- Electrolytes

- Antioxidants

- Others

- Europe Market Size (US$ Bn) Forecast, by Flavor, 2026-2033

- Citrus

- Berry

- Tropical

- Others

- Europe Market Size (US$ Bn) Forecast, by Distribution Channel, 2026-2033

- Supermarkets / Hypermarkets

- Convenience Stores

- Online Retail

- Others

- East Asia Flavored and Functional Water Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- East Asia Market Size (US$ Bn) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) Forecast, by Product Type, 2026-2033

- Flavored Water

- Functional Water

- East Asia Market Size (US$ Bn) Forecast, by Ingredient, 2026-2033

- Vitamins & Minerals

- Botanical Extracts

- Electrolytes

- Antioxidants

- Others

- East Asia Market Size (US$ Bn) Forecast, by Flavor, 2026-2033

- Citrus

- Berry

- Tropical

- Others

- East Asia Market Size (US$ Bn) Forecast, by Distribution Channel, 2026-2033

- Supermarkets / Hypermarkets

- Convenience Stores

- Online Retail

- Others

- South Asia & Oceania Flavored and Functional Water Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Product Type, 2026-2033

- Flavored Water

- Functional Water

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Ingredient, 2026-2033

- Vitamins & Minerals

- Botanical Extracts

- Electrolytes

- Antioxidants

- Others

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Flavor, 2026-2033

- Citrus

- Berry

- Tropical

- Others

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Distribution Channel, 2026-2033

- Supermarkets / Hypermarkets

- Convenience Stores

- Online Retail

- Others

- Latin America Flavored and Functional Water Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Latin America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) Forecast, by Product Type, 2026-2033

- Flavored Water

- Functional Water

- Latin America Market Size (US$ Bn) Forecast, by Ingredient, 2026-2033

- Vitamins & Minerals

- Botanical Extracts

- Electrolytes

- Antioxidants

- Others

- Latin America Market Size (US$ Bn) Forecast, by Flavor, 2026-2033

- Citrus

- Berry

- Tropical

- Others

- Latin America Market Size (US$ Bn) Forecast, by Distribution Channel, 2026-2033

- Supermarkets / Hypermarkets

- Convenience Stores

- Online Retail

- Others

- Middle East & Africa Flavored and Functional Water Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Middle East & Africa Market Size (US$ Bn) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) Forecast, by Product Type, 2026-2033

- Flavored Water

- Functional Water

- Middle East & Africa Market Size (US$ Bn) Forecast, by Ingredient, 2026-2033

- Vitamins & Minerals

- Botanical Extracts

- Electrolytes

- Antioxidants

- Others

- Middle East & Africa Market Size (US$ Bn) Forecast, by Flavor, 2026-2033

- Citrus

- Berry

- Tropical

- Others

- Middle East & Africa Market Size (US$ Bn) Forecast, by Distribution Channel, 2026-2033

- Supermarkets / Hypermarkets

- Convenience Stores

- Online Retail

- Others

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- The Coca-Cola Company

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- PepsiCo

- Nestlé

- Danone

- Keurig Dr Pepper

- Suntory Beverage & Food

- Talking Rain Beverage Company

- National Beverage Corp.

- Hint Water Inc.

- Spindrift Beverage Co.

- Penta Water

- Vita Coco Company

- The Coca-Cola Company

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Beverages

- Flavored and Functional Water Market

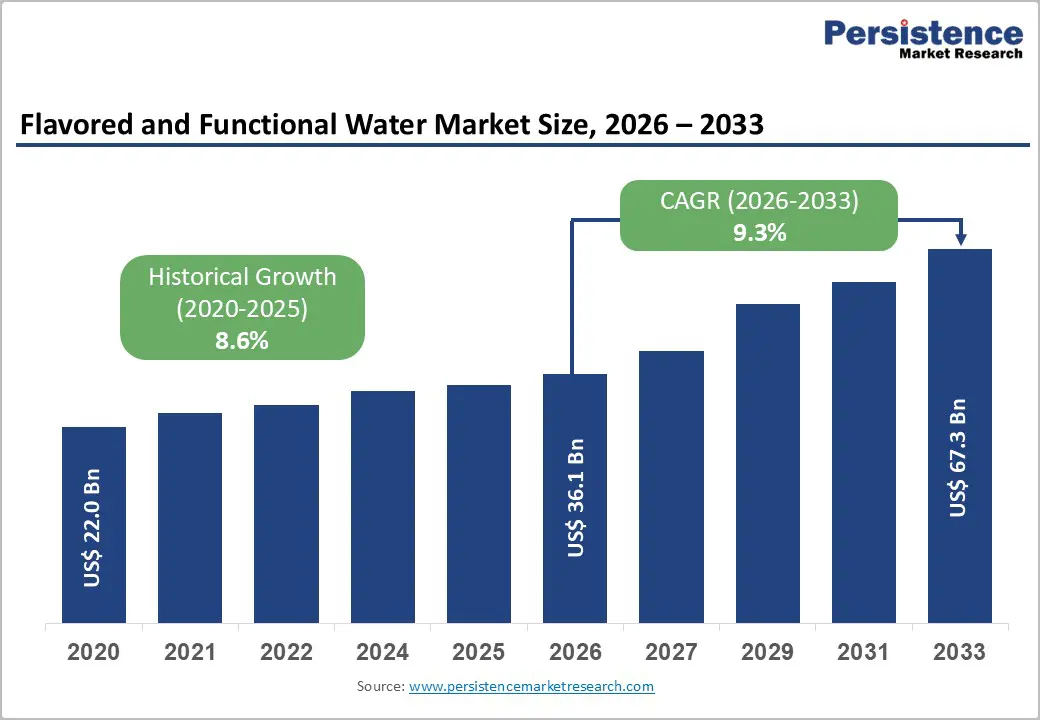

Flavored and Functional Water Market Size, Share, and Growth Forecast 2026 - 2033

Flavored and Functional Water Market by Product Type (Flavored Water, Functional Water), by Ingredient (Vitamins & Minerals, Botanical Extracts, Electrolytes, Antioxidants, Others), by Flavor (Citrus, Berry, Tropical, Others), by Distribution Channel (Supermarkets / Hypermarkets, Convenience Stores, Online Retail, Others), and Regional Analysis, 2026 - 2033

Key Industry Highlights:

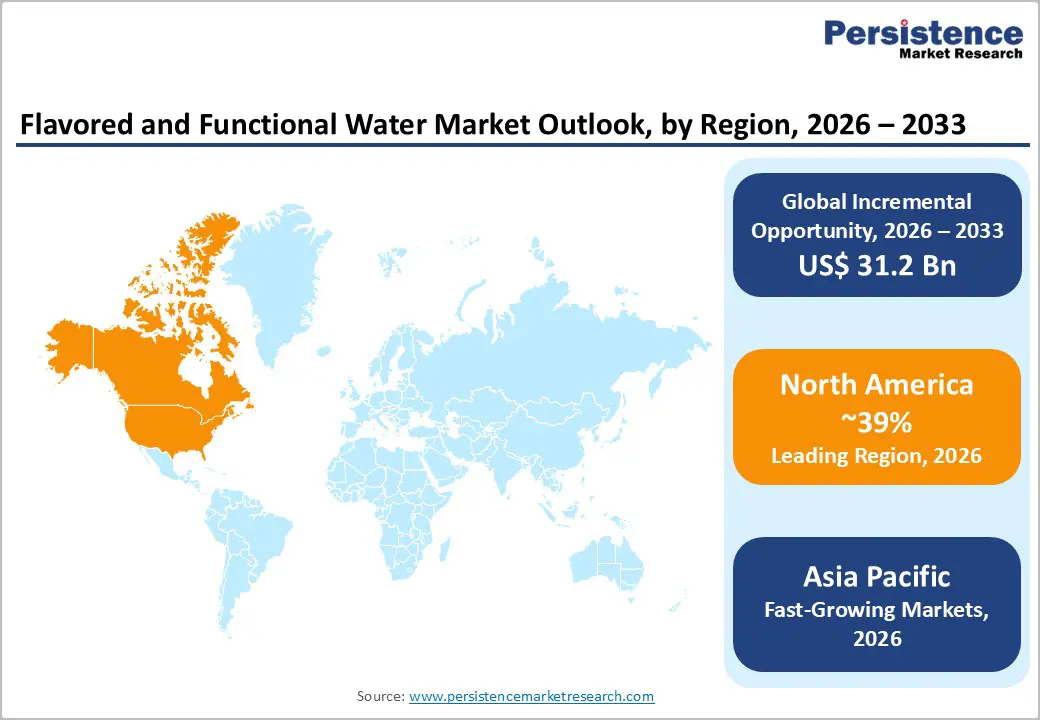

- North America is the leading region in the global flavored and functional water market, holding around 39% share in 2025, driven by high bottled water consumption, strong health-and-wellness trends, and portfolio expansion from major players like the Coca-Cola Company, PepsiCo, Keurig Dr Pepper, and Nestlé into flavored and functional water offerings.

- Asia Pacific is the fastest-growing regional market, benefiting from rapid urbanization, rising disposable incomes, growing health awareness, and concerns over tap water quality in countries such as China, India, and Southeast Asian nations, which are propelling demand for premium, safe, and functional hydration products.

- Within product types, functional water is the dominant segment by value, contributing an estimated 52% share in 2025, as consumers increasingly favor beverages that deliver added benefits via vitamins, minerals, electrolytes, and botanicals, positioning functional water at the intersection of hydration and wellness.

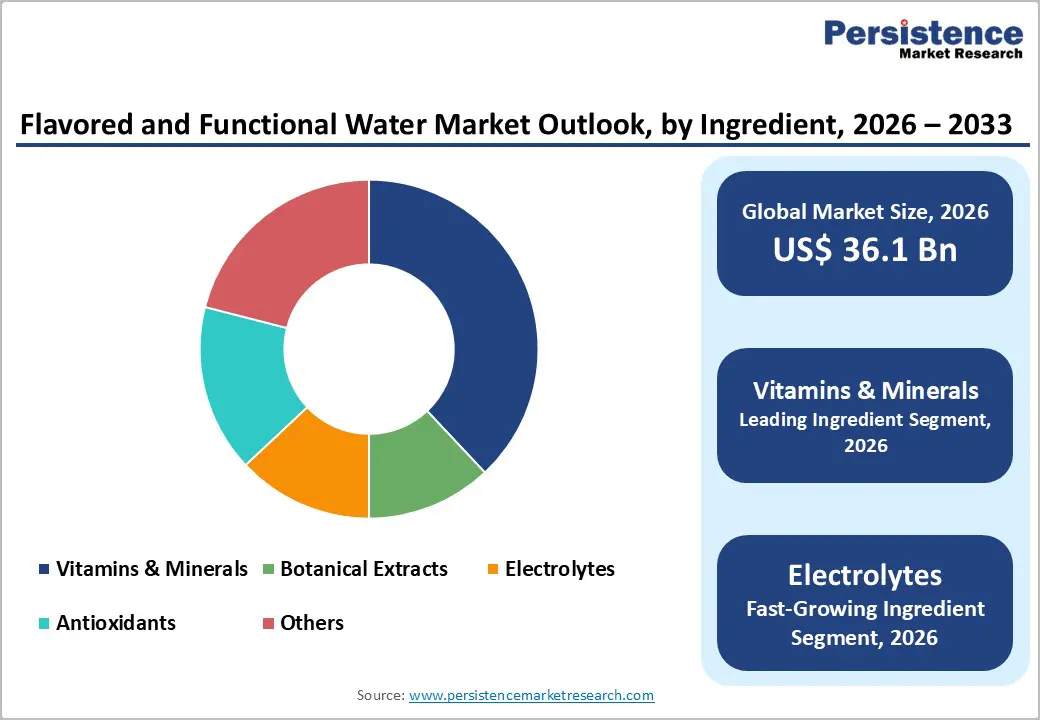

- Among ingredient categories, electrolytes represent the fastest-growing segment, reflecting strong consumer interest in hydration, sports performance, and recovery, while Vitamins & Minerals remain the largest ingredient segment with about 38% share in 2025, supported by widespread familiarity and regulatory acceptance.

- Key market opportunities revolve around clean-label, botanical, and electrolyte-enriched formulations; sustainable packaging innovations like 100% rPET and aluminum; and digital-first distribution models, enabling both multinational and emerging brands to capture premium margins and meet evolving consumer expectations for health, convenience, and environmental responsibility.

| Key Insights | Details |

|---|---|

|

Flavored and Functional Water Market Size (2026E) |

US$ 36.1 billion |

|

Market Value Forecast (2033F) |

US$ 67.3 billion |

|

Projected Growth CAGR (2026-2033) |

9.3% |

|

Historical Market Growth (2020-2025) |

8.6% |

Market Dynamics

Drivers - Health and Wellness Shift Away from Sugary Soft Drinks

A powerful driver of the flavored and functional water market is the global pivot toward health and wellness and the corresponding decline in sugary carbonated beverage consumption. Public health authorities and medical organizations have linked high sugar intake to obesity, type 2 diabetes, and cardiovascular disease, prompting consumers to reduce consumption of sugar-sweetened beverages worldwide. As a result, flavored and functional waters that offer zero or low calories, no added sugar, and added benefits such as vitamins, minerals, and antioxidants are increasingly viewed as better-for-you alternatives that fit into weight management and active lifestyle routines. Analyses show that consumers are specifically migrating from sodas and juice drinks to flavored water as their primary flavored beverage, with brands like vitaminwater, smartwater, bubly, AHA, Hint, and Spindrift positioned as modern hydration tools rather than indulgent treats. This behavioral shift is reinforced by government initiatives promoting healthier diets, sugar taxes in markets such as Mexico, the U.K., and parts of U.S. municipalities, and corporate reformulation targets, collectively boosting long-term demand for flavored and functional water.

Premiumization, Convenience, and Packaging Innovation

The second major growth driver is premiumization combined with convenience and packaging innovation that enhances consumer appeal and willingness to pay. Many functional water products are marketed as premium lifestyle beverages with enhanced hydration benefits, clean-label positioning, and sophisticated flavors (for example, cucumber-lime, strawberry-blackberry, watermelon-mint, and botanically infused variants). Beverage companies have expanded their portfolios to include flavored still and sparkling waters, vitamin- and mineral-enriched waters, and electrolyte waters aimed at fitness and recovery, often in sleek PET or aluminum packaging that signals quality and sustainability. For instance, PepsiCo announced that LIFEWTR would move to 100% rPET packaging and that bubly sparkling water would no longer be packaged in plastic, eliminating more than 8,000 metric tons of virgin plastic and around 11,000 metric tons of greenhouse gas emissions annually, appealing strongly to environmentally conscious consumers. Similarly, The Coca-Cola Company has rapidly scaled brands like AHA and broadened smartwater flavored variants to address consumer demand for variety and functionality. These innovations, combined with omnichannel distribution through supermarkets, convenience stores, and online platforms, make it easier for consumers to incorporate flavored and functional waters into daily routines.

Restraints - Pricing Premiums and Affordability Constraints in Developing Markets

Despite strong demand drivers, higher price points relative to plain bottled water and some traditional beverages act as a barrier, particularly in price-sensitive developing markets. Functional and flavored waters often carry premiums due to added ingredients, branding, and packaging, with some products priced at levels closer to premium soft drinks or juices. While rising incomes in emerging economies are improving affordability, a significant portion of consumers still opt for low-cost plain bottled water or local beverages, especially in rural and lower-income segments. Manufacturers note that although flavored and functional water is “a bit expensive,” increasing income levels primarily among urban middle-class consumers currently underpin demand, and broader penetration into mass markets depends on cost-efficient formulations and pack sizes.

Regulatory Scrutiny on Health Claims and Ingredients

Another important restraint is regulatory scrutiny on health claims, labeling, and certain functional ingredients, which can slow product development and create compliance costs. Authorities in regions such as North America and Europe closely monitor claims around immunity support, energy, detoxification, and weight loss, requiring robust scientific evidence for specific claims under frameworks like the European Food Safety Authority (EFSA) health claim regulations. Additionally, some botanical extracts and novel ingredients require safety evaluations or approvals before use in beverage applications, extending time-to-market. Clean-label expectations such as “no artificial colors,” “no preservatives,” “all natural flavors,” and “zero sugar” also raise formulation complexity, as brands must deliver taste and functional benefits while minimizing additives and sweeteners. These factors increase R&D and regulatory costs and can limit smaller players’ ability to compete with large multinational beverage companies that have dedicated regulatory and scientific resources.

Opportunities - Electrolyte-Enhanced Functional Waters for Hydration and Sports Recovery

A prominent market opportunity lies in the rapidly growing segment of electrolyte-enhanced functional waters targeting hydration, sports performance, and recovery. Consumers engaged in fitness and outdoor activities increasingly look for products that replenish electrolytes lost through sweat without the sugar and artificial additives commonly found in traditional sports drinks. Functional waters that include sodium, potassium, magnesium, and calcium electrolytes in balanced amounts, often with light natural flavors, are gaining traction as everyday hydration solutions suitable for before, during, and after exercise. Both legacy brands and emerging players are developing electrolyte water lines that overlap with the sports drinks and better-for-you beverages categories, allowing cross-merchandising in retail spaces. Given that electrolytes are identified as the fastest-growing ingredient segment reflecting rising consumer understanding of hydration science, companies that can combine evidence-based formulations with clean labels and compelling branding are well positioned to capture outsized growth in this space.

Botanical and Functional Ingredient Innovation with Clean-Label Positioning

A second major opportunity is innovation in botanical extracts, antioxidants, and other functional ingredients that move flavored and functional water beyond simple refreshment into the realm of holistic wellness. Market analyses and product launches show growing incorporation of botanicals such as green tea extract, hibiscus, chamomile, ginger, and adaptogenic herbs, which consumers increasingly associate with stress support, immunity, digestion, and cognitive function. The botanical and herbal segment has effectively transformed flavored water into a functional beverage category, enabling premium pricing and differentiation in a crowded shelf environment. Brands like Vitaminwater, Hint, Spindrift, and various niche start-ups are emphasizing “no artificial colors,” “no preservatives,” and “all natural flavors,” coupled with clear communication around functional benefits, resonating strongly with health-conscious millennials and Gen Z consumers. As regulatory guidance on botanical claims becomes more defined and scientific substantiation grows, there is ample room for flavored and functional waters that deliver targeted benefits (energy, focus, relaxation, immunity) without high sugar or caffeine loads, opening new consumption occasions throughout the day.

Category-wise Analysis

Product Type Insights

Within the product type category, Functional Water is emerging as the leading segment by value, estimated to account for a slightly higher market share than flavored-only water, approximately 52% of global sales in 2025. Functional water products are defined by added ingredients that provide perceived health benefits beyond basic hydration, such as vitamins, minerals, electrolytes, antioxidants, and botanicals. As consumers increasingly scrutinize beverage choices through a wellness lens, they are more willing to pay for multifunctional products that can support energy, immunity, beauty-from-within, or cognitive function while also serving as daily hydration. Persistent consumer education from major beverage brands through marketing campaigns tying water to fitness, skincare, and mental performance has further elevated functional water from a niche to a mainstream category. Flavored water remains critical in volume terms as an entry point for consumers transitioning away from sodas, but the additional value density in functional water positions it as the primary revenue driver and the core innovation frontier for leading companies.

Flavor Insights

In terms of flavor, Citrus variants represent the leading segment, accounting for an estimated 34% share of the flavored and functional water market in 2025. Citrus flavors such as lemon, lime, orange, grapefruit, and combinations like lime-watermelon or citrus-green tea are perceived as refreshing, light, and naturally associated with hydration, making them ideal bases for both flavored and functional formulations. Large beverage companies often anchor new product lines with citrus-forward combinations before expanding into more experimental profiles, as seen with AHA sparkling water and various citrus-infused smartwater and bubbly offerings. Berry flavors (strawberry, raspberry, blueberry, mixed berries) form the second-largest segment, resonating with consumers seeking slightly sweeter yet still “healthy” taste profiles, while tropical flavors like mango, pineapple, and passionfruit are gaining ground in Asia Pacific and Latin America as brands localize flavor portfolios to regional palates. Complex multi-fruit and botanical blends are increasingly used to differentiate premium SKUs.

Distribution Channel Insights

By distribution channel, supermarkets/hypermarkets are the leading segment, representing an estimated 48% of global flavored and functional water sales in 2025. Large-format retailers are critical points of purchase where consumers encounter extensive assortments of bottled water, flavored water, functional beverages, and soft drinks, often benefiting from prominent shelf placements, in-store promotions, and multipack offerings. Supermarkets and hypermarkets serve as primary outlets for household stock-up missions, with shoppers purchasing multi-bottle packs or cases of flavored and functional water as a staple alongside groceries. Convenience Stores hold a significant share, especially for on-the-go and single-serve consumption, and are particularly important in North America and Asia Pacific where impulse hydration purchases are common. Online Retail is the fastest-growing channel, driven by the rapid adoption of e-commerce, direct-to-consumer subscription models, and quick commerce platforms that deliver beverages to consumers’ homes or offices. Brands like Hint Water Inc. and several niche functional water players have successfully leveraged direct online channels combined with social media marketing to build loyal customer bases, while major retailers’ online marketplaces further expand digital shelf space.

Regional Insights

North America Flavored and Functional Water Market Trends and Insights

North America dominates the flavored and functional water market due to strong consumer awareness regarding health, hydration, and low-calorie beverage alternatives. Rising concerns about sugar consumption and obesity have encouraged consumers to shift from carbonated soft drinks toward flavored and nutrient-enriched water products. The region benefits from a well-established beverage industry, advanced distribution networks, and continuous product innovation focused on vitamins, electrolytes, and plant-based ingredients. Increasing demand for clean-label, zero-sugar, and naturally flavored beverages is further strengthening market growth. Additionally, the growing popularity of fitness lifestyles and sports nutrition products has increased the consumption of electrolyte-infused and performance-enhancing water drinks. Companies are also introducing new flavor combinations, functional ingredients, and sustainable packaging solutions to attract health-conscious consumers. Strong retail presence across supermarkets, convenience stores, and online channels improves product accessibility and visibility. Moreover, strategic marketing campaigns and celebrity endorsements continue to boost brand awareness and consumer engagement.

Asia Pacific Flavored and Functional Water Market Trends and Insights

The Asia Pacific flavored and functional water market is emerging as a rapidly expanding region due to increasing health awareness, rising disposable incomes, and changing beverage consumption habits. Consumers across countries such as China, India, Japan, and South Korea are gradually shifting from sugary carbonated drinks to healthier hydration options, including vitamin-enriched and naturally flavored water products. Urbanization and the growing middle-class population are further supporting demand for convenient and functional beverages. The rising popularity of fitness, sports activities, and preventive healthcare has also increased interest in electrolyte-infused and nutrient-fortified water. In addition, the region’s young population and expanding e-commerce platforms are helping brands reach a wider consumer base. Manufacturers are introducing innovative flavors inspired by regional fruits and botanical ingredients to appeal to local tastes. The presence of expanding retail infrastructure, including supermarkets and convenience stores, is improving product availability.

Competitive Landscape

The flavored and functional water market is highly competitive, driven by increasing consumer demand for healthier beverage options. Market participants focus on product innovation by introducing new flavors, functional ingredients such as vitamins, minerals, and electrolytes, and clean-label formulations to attract health-conscious consumers. Companies are also emphasizing low-calorie, sugar-free, and naturally flavored beverages to align with evolving consumer preferences. In addition, sustainable packaging solutions and eco-friendly materials are gaining importance as brands aim to strengthen their environmental positioning. Expansion of distribution channels, including supermarkets, convenience stores, and online retail platforms, further intensifies competition.

Key Developments:

- In January 2026, Karma Water launched its new Pineapple Coconut Probiotic Water, a refreshed version of one of its original bestselling flavors. The product was introduced at the 2026 Winter Fancy Food Show in San Diego and was designed to align with growing consumer interest in gut health and functional beverages.

- In January 2026, BUBBL’R entered into a partnership with Alex Warren to support the launch of its new antioxidant sparkling water flavor, Fruit Punch’r. The collaboration aimed to strengthen the brand’s connection with younger consumers through Warren’s strong digital presence and fan base. As part of the partnership, Warren promoted the new beverage through marketing campaigns and social media engagement, helping increase product visibility and brand awareness.

- In May 2024, Unilever reported that its hydration brand Liquid I.V. expanded its growth strategy through product innovation, partnerships, and international market expansion. The brand strengthened its portfolio by introducing new sugar-free hydration products to meet increasing consumer demand for healthier functional beverages.

Companies Covered in Flavored and Functional Water Market

- The Coca-Cola Company

- PepsiCo, Inc.

- Nestlé S.A.

- Danone S.A.

- Keurig Dr Pepper Inc.

- Suntory Beverage & Food Ltd.

- Talking Rain Beverage Company

- National Beverage Corp.

- Hint Water Inc.

- Spindrift Beverage Co.

- Penta Water

- Vita Coco Company

- BlueTriton Brands

- San Benedetto

Frequently Asked Questions

The global Flavored and Functional Water market is expected to reach approximately US$ 36.1 billion in 2026 and is projected to further expand to about US$ 67.3 billion by 2033, registering a forecast CAGR of 9.3% from 2026 to 2033.

Key demand drivers include the global shift away from sugary soft drinks toward low- or zero-calorie hydration, increasing awareness of lifestyle-related diseases such as obesity and diabetes, rising preference for beverages with added vitamins, minerals, electrolytes, and botanicals, and strong health-and-wellness positioning supported by innovation in flavors, functionality, and sustainable packaging.

North America currently leads the global flavored and functional water market with around 39% share in 2025, driven by high bottled water consumption, strong health-conscious consumer behavior, and the extensive portfolios and marketing investments of major beverage companies such as The Coca-Cola Company, PepsiCo, Keurig Dr Pepper, Nestlé, and Danone.

A major growth opportunity lies in electrolyte-enhanced and botanically enriched functional waters that deliver targeted hydration and wellness benefits with clean-label formulations, alongside expansion into rapidly growing Asia Pacific markets where urbanization, rising incomes, and health awareness are driving uptake of premium, better-for-you beverages.

Leading companies include The Coca-Cola Company, PepsiCo, Inc., Nestlé S.A., Danone S.A., Keurig Dr Pepper Inc., Suntory Beverage & Food Ltd., Talking Rain Beverage Company, National Beverage Corp., Hint Water Inc., Spindrift Beverage Co., Penta Water, and Vita Coco Company, along with several regional and niche brands competing on flavor innovation, functionality, and sustainability.