- Smart Packaging

- Feeder Container Market

Feeder Container Market Size, Share, and Growth Forecast, 2026 - 2033

Feeder Container Market by Product Type (Dry Containers, Reefer Containers, Others), Container Size (Medium Size, Small Size, Others), End-user and Regional Analysis for 2026 - 2033

Feeder Container Market Size and Trends Analysis

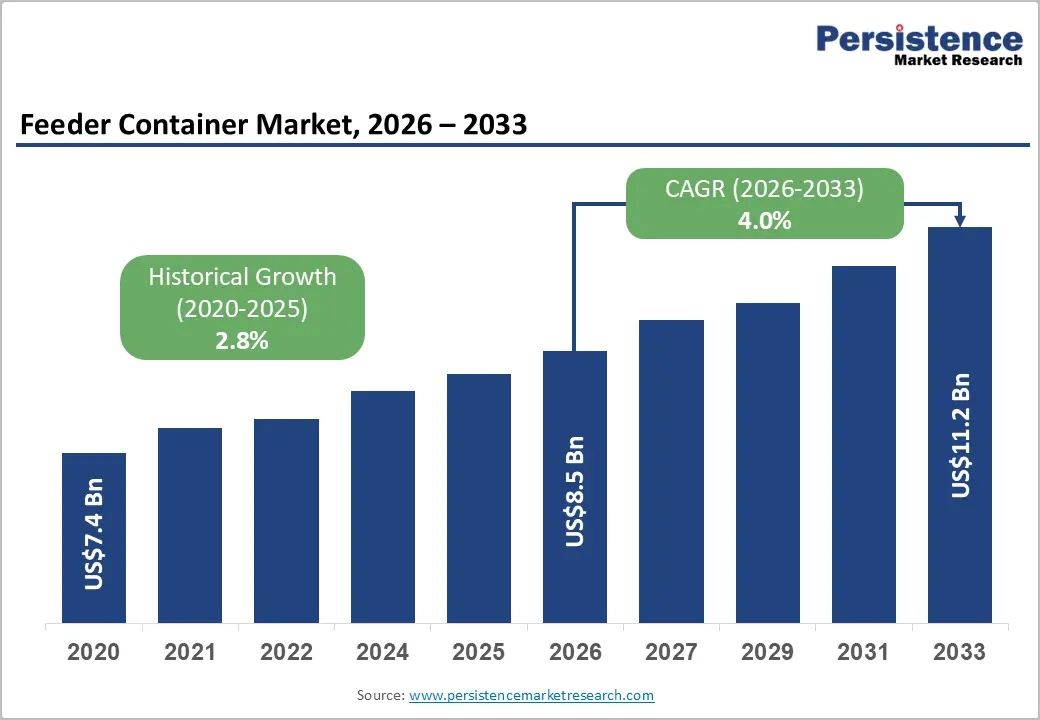

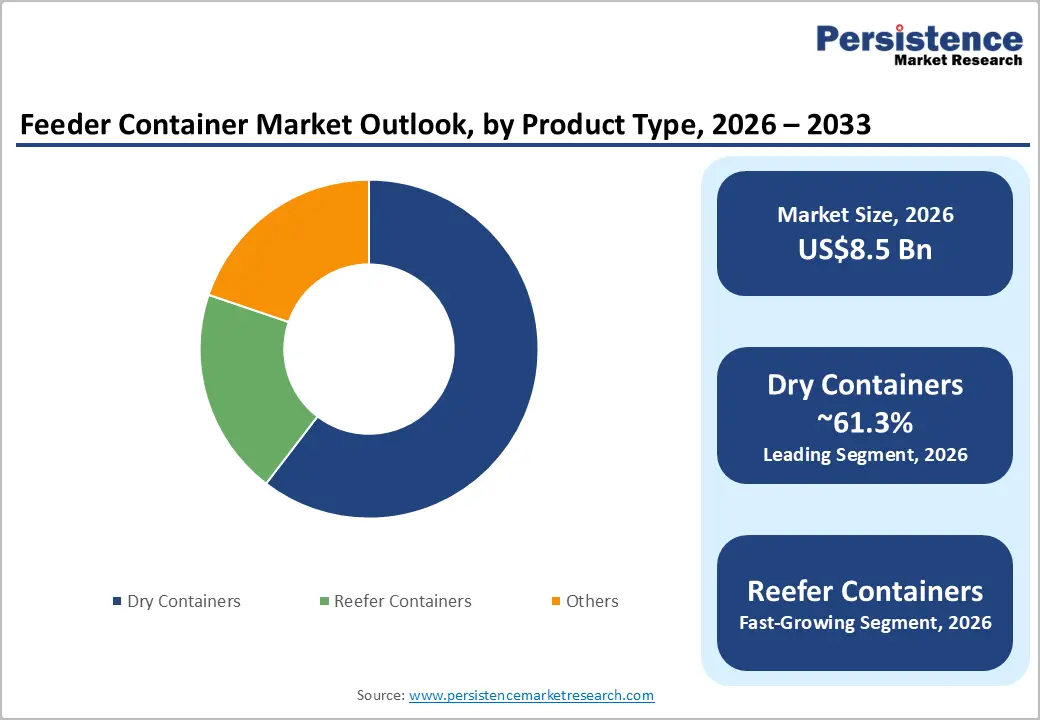

The global feeder container market size is likely to be valued at US$8.5 billion in 2026 and is expected to reach US$11.2 billion by 2033, growing at a CAGR of 4.0% between 2026 and 2033, driven by factors such as the structural expansion of intra-regional containerized trade, regulatory pressures for fleet renewal, and rising demand for temperature-controlled and high-value cargo transportation.

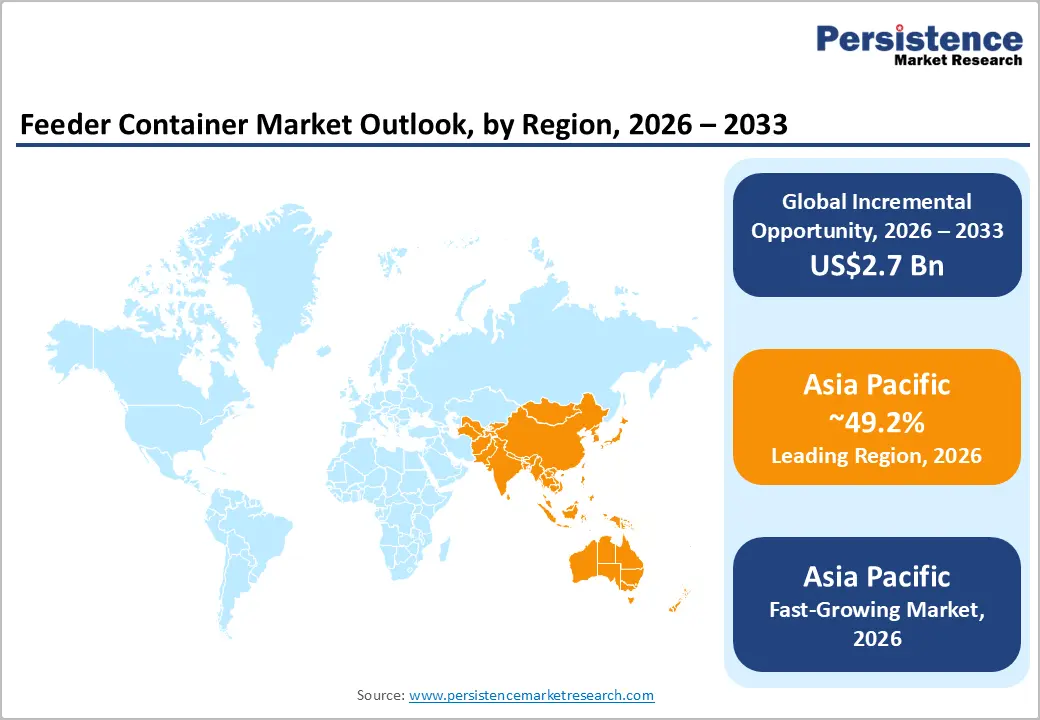

The Asia Pacific region, which accounts for more than 49.2% of global revenue, is anticipated to remain the fastest-growing market, bolstered by a concentration of manufacturing, investments in port infrastructure, and the expansion of coastal shipping networks. The competitive landscape is shaped by a concentrated manufacturing base and large global leasing companies, which influence fleet allocation, pricing trends, and strategies for asset modernization.

Key Industry Highlights:

- Leading Region: Asia Pacific dominates the market, projected to hold 49.2% of market share, due to manufacturing concentration in China, strong intraregional trade flows, and expanding port infrastructure across ASEAN and India.

- Fastest-growing Region: Asia Pacific is the fastest-growing region with growth supported by coastal shipping programs, cold-chain expansion, and container production scale advantages.

- Investment Plans: Focus on digital telemetry integration, energy-efficient reefer technology, port electrification, and asset-light leasing models, particularly in North America and Europe, to meet regulatory compliance standards.

- Dominant Product Type: Dry containers are anticipated to account for 61.3% market share, driven by cost efficiency, versatility, and high secondary market liquidity.

- Leading Container Size: Medium-sized containers are estimated to hold 39.7% of the market share, preferred for feeder operations due to an optimal balance of payload and handling efficiency, widely used by regional carriers, and favored in leasing and secondary markets.

| Key Insights | Details |

|---|---|

| Feeder Container Market Size (2026E) | US$8.5 Bn |

| Market Value Forecast (2033F) | US$11.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Intra-Regional Trade and Feeder Networks

Global trade patterns have increasingly shifted toward regional supply chains, particularly in Asia, where intra-Asian trade volumes continue to expand. Hub-and-spoke logistics models depend on feeder vessels that transport containers between large transshipment hubs and smaller regional ports. This structure increases the circulation and utilization of feeder containers. Port modernization programs, coastal shipping initiatives, and regional trade agreements strengthen feeder route density.

Short-sea shipping growth reduces inland trucking dependency and improves cost efficiency for bulk and semi-bulk cargo flows. This dynamic supports incremental demand for medium-sized dry containers and reefers optimized for shorter voyage cycles. Manufacturers respond by adjusting production toward regionally preferred container formats, while lessors increase fleet positioning in high-throughput feeder corridors.

Regulatory Compliance and Safety Standards Accelerating Fleet Renewal

Global enforcement of container safety standards, cargo weight verification requirements, and reporting mandates has increased compliance obligations for asset owners. Stricter inspection regimes and reporting frameworks encourage retirement of aging units and investment in certified, traceable containers. Environmental policies targeting emissions reduction in port operations further incentivize newer container fleets that align with lifecycle efficiency standards.

Compliance costs associated with older equipment often exceed refurbishment value, pushing operators toward replacement or leasing models. Regulatory-driven replacement cycles create sustained demand for new-build feeder containers. Leasing penetration increases as operators seek flexibility while maintaining compliance. Higher-specification units command pricing premiums, improving manufacturer and lessor revenue resilience.

Growth in Temperature-Sensitive and High-Value Cargo

The global expansion of perishable food trade, pharmaceuticals, and consumer electronics drives demand for specialized feeder containers. Cold-chain logistics are particularly sensitive to temperature control reliability during short-sea and regional distribution stages. Healthcare and pharmaceutical shipments require validated reefer units capable of maintaining strict temperature thresholds. Electronics shipments favor high-cube units that optimize cubic capacity while protecting delicate goods.

Reefer and telematics-enabled containers experience higher average selling prices and recurring service revenue opportunities. This shift elevates overall market value beyond simple volume growth and increases lifecycle monetization through maintenance, tracking, and analytics services.

Barrier Analysis - Cyclical Overcapacity and Pricing Volatility

Container manufacturing capacity expansion often follows shipping demand surges. When new vessel deliveries slow or global trade moderates, oversupply pressures container prices downward. Historical cycles show double-digit percentage declines in new-build pricing during oversupply phases. This cyclicality compresses margins for manufacturers and delays procurement decisions by asset owners, anticipating lower prices. Capital allocation becomes conservative during downturns, reducing innovation investment in specialized feeder units.

Raw Material and Supply Chain Volatility

Steel accounts for a significant portion of container bill-of-material costs. Fluctuations in global steel prices and logistics bottlenecks directly affect unit economics. Cost increases ranging from single-digit to low-double-digit percentages materially impact the total cost of ownership. Emerging market buyers and smaller lessors are particularly sensitive to these fluctuations. Financing constraints further amplify procurement delays, leading to uneven adoption of higher-cost, technology-enabled container formats.

Opportunity Analysis - Digitalization and Telematics Integration

Digitally enabled containers equipped with GPS tracking, temperature sensors, and predictive maintenance systems represent a high-margin opportunity. Integration with port systems and logistics platforms improves asset visibility and reduces dwell times. Operators can capture 2-4% incremental margin by bundling telemetry services with leasing contracts. Predictive maintenance reduces downtime and extends asset life, while enhanced tracking lowers insurance claims and loss incidents. Companies that standardize data protocols and offer interoperable digital platforms will gain a competitive advantage as supply chains prioritize transparency and traceability.

Retrofit and Circular Economy Monetization

Container retrofitting and conversion into storage units, mobile facilities, or specialized cold-chain modules extend asset lifecycles. This reduces scrappage rates and creates alternative revenue streams across construction, retail, and event sectors. Certified refurbishment programs allow asset owners to resell or redeploy aging units profitably. Secondary market valuation increasingly incorporates retrofit potential and structural condition assessments. This circular model reduces net capital expenditure requirements while supporting sustainability objectives aligned with global environmental targets.

Category-wise Analysis

Product Type Insights

Dry containers are anticipated to account for 61.3% of revenue share in 2026, maintaining their structural dominance across short- and medium-haul maritime trade routes. Their leadership reflects unmatched versatility in transporting consumer goods, industrial components, textiles, machinery parts, and packaged food products. Standard dry vans remain cost-efficient and universally compatible with port handling equipment, chassis systems, and intermodal rail infrastructure, ensuring seamless integration across multimodal networks. Secondary market liquidity further reinforces this segment’s dominance.

Dry containers are easier to remarket or reposition compared to specialized units, supporting leasing companies in maintaining utilization rates above industry averages reported by leading container lessors. Medium-sized dry units are particularly favored in intra-Asian trade corridors, including China, ASEAN, and Japan, South Korea routes, where frequent port calls and variable berth capacities necessitate flexible equipment. Stable pricing patterns relative to specialized containers enhance capital planning visibility for lessors and regional operators. Although sensitive to global steel price fluctuations, dry containers remain foundational to feeder network economics due to their standardized design and predictable lifecycle performance.

Reefer containers are projected to record the highest CAGR through 2033, supported by measurable structural demand drivers. Expansion of cold-chain logistics infrastructure across Asia Pacific and Latin America, rising exports of seafood and horticultural products, and stricter pharmaceutical transport compliance standards significantly accelerate adoption. According to international trade data from organizations such as the World Trade Organization (WTO), global trade in perishable food products has consistently outpaced overall merchandise trade growth, reinforcing structural reefer demand.

Technological advancements, including integrated IoT-based telemetry systems, energy-efficient refrigeration units, and enhanced insulation materials, have improved temperature stability and reduced spoilage risk. These upgrades support compliance with pharmaceutical distribution standards and food safety regulations administered by agencies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA). Although reefers involve higher upfront capital costs compared to dry units, operators offset these through premium leasing rates and long-term contracts with food exporters and healthcare distributors.

Container Size Insights

Medium-sized containers are anticipated to account for approximately 39.7% of market revenue in 2026, reflecting their optimal balance between payload capacity and handling efficiency. These containers provide sufficient cargo volume while remaining compatible with ports that have draft or crane capacity limitations, common across secondary and regional harbors. This operational flexibility supports feeder networks that connect major transshipment hubs with smaller domestic ports.

Regional carriers prioritize turnaround speed and berth efficiency over maximum vessel load factors, making medium-sized units particularly well suited to short-haul services. Leasing companies continue allocating substantial production and procurement capacity toward this segment due to consistent demand visibility and strong secondary resale markets. For example, feeder operators serving Indonesia’s archipelagic routes and the Philippines’ inter-island trade corridors rely heavily on medium-sized units due to infrastructure variability and frequent port calls.

Small-sized containers are projected to grow at the fastest rate within the size category, particularly across emerging economies. These containers offer lower capital expenditure requirements and improved maneuverability in secondary ports. Urban logistics expansion and last-mile consolidation strategies further support demand for smaller container formats.

For instance, feeder services linking inland manufacturing clusters in India or Vietnam to export gateways increasingly utilize smaller units to optimize vessel rotation schedules and reduce repositioning costs. Small containers also improve berth compatibility in ports with limited gantry crane capacity, reducing idle time and demurrage risks. High-cube containers are also gaining traction in trade lanes where infrastructure upgrades support larger dimensional capacity, particularly for lighter-density cargo such as consumer electronics and automotive components.

Regional Insights

North America Feeder Container Market Trends - High-ASP Reefer Demand and Regulatory-Driven Fleet Modernization

North America represents a high-value feeder container market, led by the U.S., with a structurally stable demand base supported by consumption-driven imports and diversified trade flows. Although the region accounts for a smaller share of global feeder container volumes compared to Asia Pacific, it commands higher average selling prices (ASPs) due to the concentration of specialized equipment, including reefers and high-specification dry containers.

According to the U.S. Census Bureau and data from the Port of Los Angeles and Port of Long Beach, containerized imports into the U.S. remain heavily weighted toward consumer goods, electronics, and food products, sustaining steady feeder movements between primary coastal gateways and secondary ports along the Gulf Coast and Eastern Seaboard. Cold-chain logistics plays a particularly important role in shaping regional demand.

The U.S. is a major importer of fresh produce, seafood, and temperature-sensitive pharmaceuticals. Regulatory compliance under the U.S. Food and Drug Administration’s Food Safety Modernization Act (FSMA) has increased traceability requirements in temperature-controlled transport, reinforcing reefer container modernization. Major leasing companies such as Textainer (headquartered in Hamilton, Bermuda, with significant U.S. operations) and Triton International (now part of Brookfield Infrastructure) have expanded digitally enabled reefer fleets to meet compliance and monitoring needs.

Regulatory drivers also influence equipment renewal cycles. The U.S. Environmental Protection Agency (EPA) and state-level initiatives, including California Air Resources Board (CARB) port emissions regulations, accelerate the retirement of older equipment and encourage the adoption of energy-efficient refrigeration systems. Port electrification projects at the Port of Los Angeles and Port of New York and New Jersey further incentivize modernization, indirectly benefiting manufacturers that supply newer feeder-compatible units.

Investment trends in North America increasingly emphasize telematics integration, intermodal optimization, and asset-light leasing models. The rise of digital freight platforms and data visibility solutions, supported by operators such as SeaCube Containers LLC (U.S.) in the reefer segment, enhances fleet tracking and predictive maintenance. This ecosystem strengthens compliance assurance and operational transparency, which are critical for securing long-term contracts with large retailers and multinational importers.

Europe Feeder Container Market Trends - Short-Sea Shipping Strengthened by EU ETS and Fit for 55 Compliance

Europe’s feeder container market benefits from a mature logistics infrastructure and one of the world’s most established short-sea shipping networks. Countries including Germany, the U.K., France, and Spain anchor regional performance through high-frequency maritime connectivity across the North Sea, Baltic Sea, and Mediterranean corridors. According to Eurostat and the European Sea Ports Organisation (ESPO), short-sea shipping accounts for a significant share of intra-European freight transport, structurally supporting feeder container utilization.

Germany’s export-oriented manufacturing sector, particularly automotive and industrial machinery, drives consistent feeder demand linking ports such as Hamburg and Bremerhaven to secondary Baltic and Scandinavian destinations. Automotive supply chains involving manufacturers such as Volkswagen AG (Germany) rely on reliable short-haul container flows for components and finished parts. Similarly, the U.K’s port network, including Felixstowe and Southampton, supports retail and industrial imports that feed regional distribution hubs.

Environmental policy plays a decisive role in shaping fleet modernization. The European Union’s “Fit for 55” climate package and the extension of the EU Emissions Trading System (EU ETS) to maritime transport increase compliance costs for older, less efficient equipment. While this regulatory framework raises short-term capital expenditure requirements, it enhances fleet standardization and accelerates the adoption of energy-efficient reefers and lightweight container designs.

Leasing companies such as CAI International (with strong European exposure) and manufacturers such as CIMC (China International Marine Containers), which supplies European operators, have adapted production lines to meet stricter environmental and safety standards. Investment flows increasingly target low-emission port upgrades and digital integration. The Port of Rotterdam and the Port of Antwerp-Bruges have implemented shore power and digital port community systems, improving operational efficiency for feeder services. Reefer specialization is also growing in Southern Europe, particularly in Spain, where horticultural exports require temperature-controlled equipment for intra-European and global distribution. Integrated logistics partnerships between shipping lines and inland transport operators enhance container circulation efficiency, reducing dwell times and improving asset productivity.

Asia Pacific Feeder Container Market Trends - Export Manufacturing Strength and Coastal Network Growth

Asia Pacific is projected to account for over 49.2% of market revenue in 2026 and remains both the dominant and fastest-growing region. The region’s leadership is structurally anchored in manufacturing scale, intraregional trade expansion, and container production capacity. China plays a central role, not only as the world’s largest exporter but also as the primary hub for container manufacturing. Companies such as CIMC (China International Marine Containers) and Dong Fang International Container (DFIC) collectively account for a substantial share of global container production capacity, providing cost efficiencies and supply leverage that reinforce Asia Pacific’s competitive advantage.

China’s port system, including Shanghai, Ningbo-Zhoushan, and Shenzhen, supports high-frequency feeder connections to Southeast Asia, Korea, and Japan. These networks facilitate component trade across electronics and machinery supply chains. Japan and South Korea, with advanced automotive and semiconductor industries, drive demand for high-specification and specialized containers, including high-cube and reefer units. Shipping operators such as Ocean Network Express (ONE, headquartered in Japan) integrate feeder services across regional routes, supporting equipment circulation efficiency.

India and ASEAN economies represent key growth accelerators. The Government of India’s Sagarmala Programme and coastal shipping incentives aim to enhance port connectivity and reduce logistics costs, indirectly strengthening feeder container deployment along domestic and export corridors. ASEAN economies, including Vietnam, Indonesia, and Thailand, have expanded port infrastructure and export manufacturing, particularly in electronics and textiles, reinforcing demand for medium and small-sized containers in secondary ports. Cold-chain growth is another structural driver.

Rising seafood exports from Vietnam and Thailand, along with pharmaceutical production in India, increase reefer container demand. Manufacturers respond by integrating digital monitoring systems and energy-efficient refrigeration technologies tailored to tropical operating conditions. Infrastructure investments across Southeast Asian ports, often supported by multilateral development banks, enhance berth capacity and crane efficiency, enabling higher container throughput and supporting sustained feeder expansion.

Competitive Landscape

The global feeder container market is moderately concentrated in manufacturing and oligopolistic in leasing. Large Chinese OEMs control substantial global capacity, while major lessors manage multi-million TEU fleets. Scale advantages enable better procurement pricing, asset rotation efficiency, and financing access. Smaller regional players compete on customization and conversion services. Leading firms pursue consolidation, vertical integration, and digital service bundling. Telemetry-enabled leasing, certified refurbishment programs, and asset-light financing structures represent key differentiators.

Key Industry Developments:

- In July 2025, Triton International completed its acquisition of Global Container International (GCI), integrating GCI’s container assets into its owned and managed fleet to expand service reach and provide greater container availability for feeder services.

Companies Covered in Feeder Container Market

- CIMC (China International Marine Containers)

- Dong Fang International Container (DFIC)

- CXIC Group Containers Company Limited

- Maersk Container Industry

- Singamas Container Holdings Limited

- China Shipping Container Lines (CSCL)

- Triton International

- Textainer Group Holdings Limited

- Seaco Global

- SeaCube Containers LLC

- Florens Container Services Company Limited

- CAI International

- Beacon Intermodal Leasing

- Touax Group

- CARU Containers

- W&K Container Inc.

- Staxxon

- Hoover Ferguson Group

Frequently Asked Questions

The global feeder container market size is projected to be valued at US$8.5 billion in 2026.

By 2033, the feeder container market is expected to reach approximately US$11.2 billion.

Key trends include digital telemetry integration in reefers, energy-efficient refrigeration systems, port electrification initiatives, asset-light leasing expansion, and growing demand from food & beverage supply chains.

Dry containers are the leading segment, accounting for an anticipated 61.3% market share, driven by versatility, cost efficiency, and strong secondary market liquidity.

The feeder container market is projected to grow at a CAGR of 4.0% between 2026 and 2033.

Major players include CIMC (China International Marine Containers), Triton International, Textainer Group Holdings Limited, Dong Fang International Container (DFIC), and SeaCube Containers LLC.