- Specialty & Fine Chemicals

- Expanded Clay Market

Expanded Clay Market Size, Share, and Growth Forecast, 2026-2033

Expanded Clay Market Form (Granules, Powder, Custom Shapes), Production Process (Rotary Kiln Expansion, Fluidized Bed Expansion, Plasma Activation), Application (Construction, Horticulture, Wastewater Treatment, Environmental Remediation), and Regional Forecast for 2026-2033

Expanded Clay Market Share and Trends Analysis

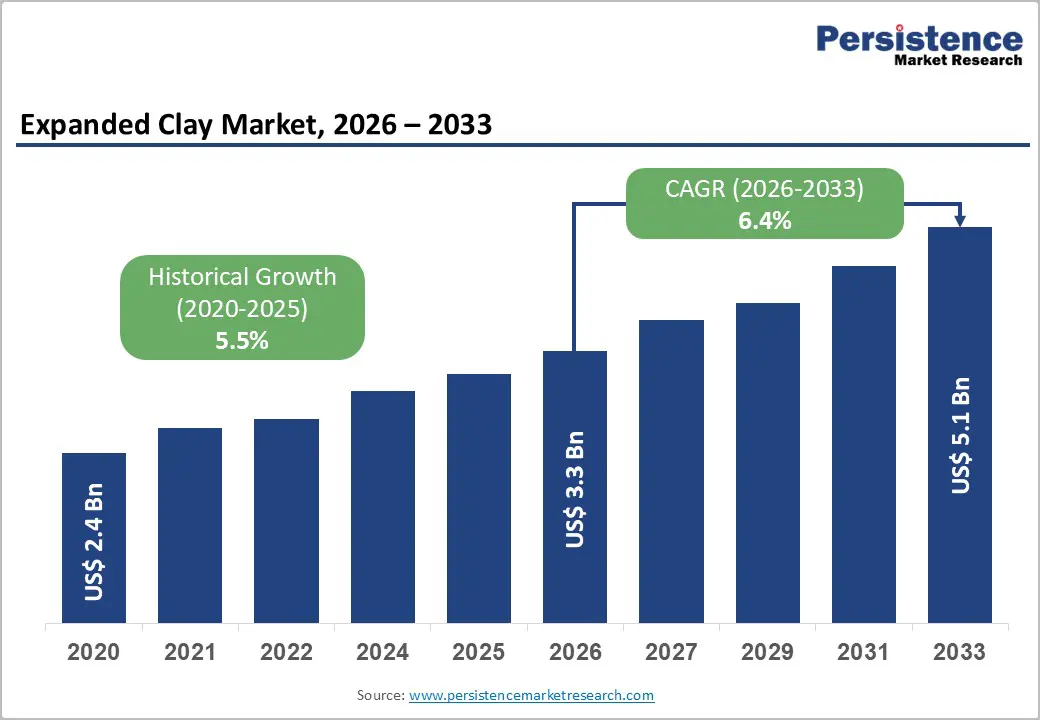

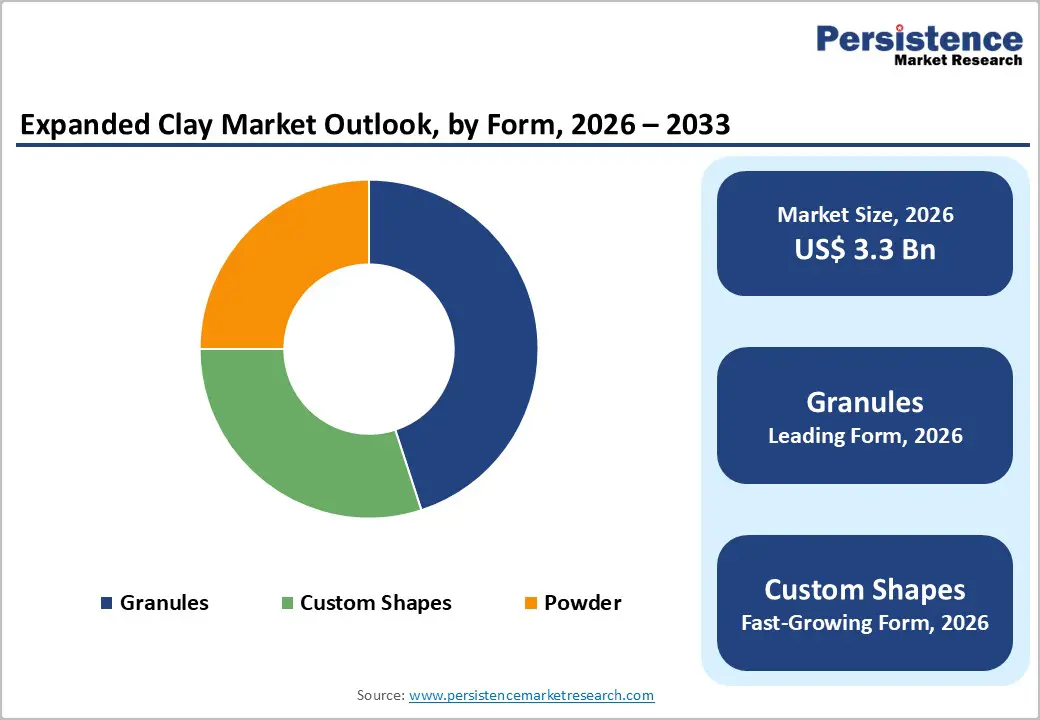

The global expanded clay market size is likely to be valued at US$ 3.3 billion in 2026, and is projected to reach US$ 5.1 billion by 2033, growing at a CAGR of 6.4% during the forecast period 2026-2033.

Market expansion is being supported by sustained demand from construction materials, lightweight aggregates, and environmental applications. Tightening building energy efficiency regulations and rising investment in urban infrastructure are continuing to increase the use of lightweight and thermally efficient materials. Expanded clay is increasingly being specified in structural concrete, insulation layers, and geotechnical applications as developers are prioritizing durability, weight reduction, and long-term performance in large-scale projects.

The increasing adoption of sustainable construction materials and technological improvements in production processes are furthering brightening the long-term growth outlook of the market. Advancements in kiln efficiency and process optimization are reducing energy consumption and emissions, which is strengthening the environmental profile of expanded clay. At the same time, application diversity is expanding, with growing use in horticulture for soil aeration and water retention, as well as in wastewater treatment systems for filtration and biological support media. These emerging applications are broadening the addressable market beyond traditional construction uses and are supporting more stable demand cycles. Producers that are investing in energy-efficient manufacturing, product quality consistency, and application-specific solutions can strengthen their competitive positioning as sustainability and regulatory compliance continue to shape material selection decisions.

Key Industry Highlights

- Leading Form: Granules are likely to account for 45% of revenue in 2026, given their extensive use in lightweight concrete, horticulture, and geotechnical applications.

- Dominant Production Process: Rotary kiln expansion is estimated to lead with nearly 60% revenue share in 2026 due to scalable production and consistent quality.

- Fastest-growing Production Process: Fluidized bed expansion is expected to grow the fastest at roughly 7.1% CAGR through 2033, reflecting increasing adoption of energy-efficient, low-emission technologies.

- Application Insights: Construction is expected to dominate with 40% revenue share in 2026, supported by large-scale infrastructure development, while wastewater treatment is set to post the highest 2026-2033 CAGR, driven by sustainability initiatives.

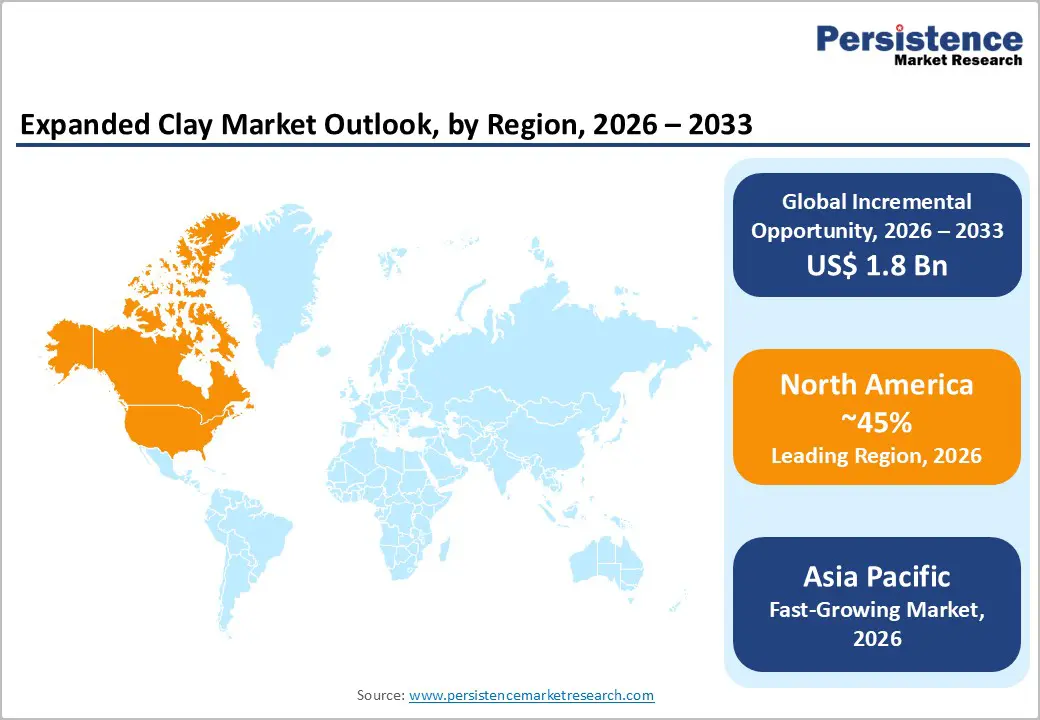

- Regional Leadership: North America is projected to lead with about 45% share in 2026, fueled by green building certifications, while Asia Pacific is slated to be the fastest-growing market at around 6.5% CAGR, driven by infrastructure expansion projects.

- Competitive Environment: Capacity enhancements, technology upgrades, and sustainability-focused investments by top players are creating opportunities for differentiation and innovation.

| Key Insights | Details |

|---|---|

| Expanded Clay Market Size (2026E) | US$ 3.3 Bn |

| Market Value Forecast (2033F) | US$ 5.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Demand for Lightweight, Energy-Efficient, and Multi-Functional Construction Materials

Expanded clay is in demand for its lightweight structure, high compressive strength, thermal insulation, and chemical stability, making it suitable for construction and environmental applications. Its versatility allows it to meet both structural and sustainability requirements, making it a preferred choice for modern building projects. Buildings account for nearly 30% of global energy consumption, driving focus on energy-efficient materials. National codes in the U.S., European Union (EU), and Japan encourage lightweight concrete usage, further boosting adoption. According to the World Bank global infrastructure investment needs are expected to exceed US$ 94 trillion by 2040, with Asia Pacific contributing over 55% of incremental demand. Rapid urbanization, high-rise construction, and large-scale projects increase the need for materials that reduce load and improve thermal performance. Expanded clay aggregates address these needs, offering durability, efficiency, and regulatory compliance.

Beyond construction, the U.S. Environmental Protection Agency (EPA) and the European Environment Agency (EEA) highlight the importance of filtration media in wastewater treatment and soil remediation. Expanded clay’s high porosity and inert nature make it ideal for biofiltration, stormwater management, and environmental remediation, creating a dual demand driver. Stricter environmental regulations and global sustainability initiatives support adoption in eco-conscious projects. Its adaptability to high-rise, infrastructure, and ecological projects positions expanded clay as a reliable solution for urban development. Demand is further supported by green building certifications and sustainable procurement policies. By combining construction efficiency with environmental utility, expanded clay strengthens its strategic value. These factors make it a multi-purpose, high-demand aggregate with broad growth potential.

High Production Costs and Competitive Pressure from Alternative Materials

Expanded clay production relies on high-temperature rotary kilns, often exceeding 1,100°C, making energy costs a significant structural challenge. Industrial energy prices have increased by 20–35% in several regions in recent years, directly affecting producer margins and the price competitiveness of expanded clay compared to natural aggregates. Smaller manufacturers face disproportionate exposure to energy price volatility, increasing exit risk during periods of cost fluctuations. Additionally, the market faces competitive pressure from alternative lightweight materials such as expanded shale, perlite, pumice, and synthetic foams. In price-sensitive applications, particularly in developing economies, locally available natural aggregates can undercut expanded clay on cost. This combination of high production costs and competitive alternatives constrains market growth and pricing power.

The risk of material substitution remains moderate but persistent, especially in regions where performance-based standards are not strictly enforced. Manufacturers must maintain cost efficiency and production reliability to remain competitive. Energy-intensive operations also limit flexibility in scaling production in response to surges in demand. Moreover, market fragmentation and the presence of numerous low-cost substitutes make it difficult for smaller players to achieve economies of scale. These factors collectively create a structural restraint, affecting both profitability and market expansion in the expanded clay industry. By addressing energy efficiency and competitive differentiation, producers can mitigate these challenges and maintain long-term market relevance.

Convergence of Sustainability, Technological Innovation, and Controlled-Environment Agriculture

The rising focus on green building certifications and ESG-driven procurement is creating significant opportunities for expanded clay suppliers. Materials that improve thermal efficiency, durability, and recycled content are increasingly favored in construction projects. Green-certified floor space is growing at over 8% annually, highlighting a sizeable addressable market. Suppliers aligning with ESG reporting standards can secure preferred status in public and institutional projects. For instance, several Leadership in Energy and Environmental Design (LEED) and Building Research Establishment Environmental Assessment Method (BREEAM)-certified commercial projects in Europe specify expanded clay for lightweight concrete and insulation to earn green building credits. This combination of sustainability credentials and regulatory alignment is expected to drive adoption in energy-efficient and environmentally conscious construction over the coming decade.

The technological advancements and controlled-environment agriculture are expanding market scope. Adoption of low-emission production technologies such as fluidized bed expansion, plasma activation, waste heat recovery, and alternative fuels can reduce CO? emissions by 15–25%, enhancing efficiency and compliance. Meanwhile, urban farms and vertical farming facilities in the U.S. and Japan increasingly use expanded clay granules as reusable, inert growing media, valued for water retention and minimal soil dependence. This application offers higher margins and lower exposure to construction cycles, creating a complementary growth avenue. Sustainability initiatives, innovation in production, and agricultural applications collectively present a multi-dimensional opportunity for the expanded clay market.

Category-wise Analysis

Product Type Insights

Granules are estimated to hold the dominant market share at roughly 45% in 2026, on account of their widespread use in lightweight concrete, geotechnical fills, and horticulture where size and mechanical strength are essential. Their structural performance ties them to infrastructure and residential construction cycles, making them a preferred baseline material. Liapor GmbH expanded its European production lines to meet rising demand for high-performance granules in structural applications. Granules’ integration into standard mix designs and compliance with construction specifications reinforces their leading position. The segment’s steady demand underpins revenue contribution, while regulatory emphasis on sustainable aggregates supports continued adoption.

Custom shapes are likely to be the fastest-growing form segment, with a projected CAGR of 8.2% between 2026 and 2033, driven by modular construction and engineered filtration systems. Tailored performance enables them to serve niche high-value applications where standard granules fall short. For example, Argex partnered on engineered aggregate solutions for filtration and water management systems, showing industry focus on bespoke solutions. Advanced engineering, premium pricing, and higher functionality drive adoption, positioning this sub-segment as a strong growth engine for the market.

Production Process Insights

Rotary kiln expansion is likely to remain dominant, with an estimated 60% revenue share in 2026, due to scalability and operational reliability. It produces consistent, high-quality aggregates for structural and bulk applications, supporting global construction demand. Laterlite S.p.A. upgraded its rotary kiln process to improve moisture resistance and load-bearing performance for infrastructure projects. The widespread use of rotary kilns ensures predictable output and quality essential for large-scale applications. Regulatory familiarity and proven performance preserve its leadership role in the market.

Fluidized bed expansion is anticipated to be the fastest?growing process, displaying an estimated 7.1% CAGR from 2026 to 2033, owing to the energy efficiency and lower emissions of the process relative to traditional methods. This process provides enhanced control over porosity and particle characteristics, which benefits specialized applications such as advanced filtration and premium construction materials. Adoption is particularly strong in markets with stringent environmental standards that reward lower emissions and sustainable manufacturing practices. The technology’s growth reflects broader industry shifts toward cleaner and more efficient production. As manufacturers invest in regulatory?aligned operations, fluidized bed techniques gain traction as a strategic differentiator.

Application Insights

Construction is projected to command approximately 40% of the expanded clay market revenue share in 2026. Demand is being driven by the use of lightweight aggregates in structural concrete, insulation layers, and geotechnical applications across public, commercial, and residential projects. Expanded clay is reducing structural load and improving thermal performance, which is aligning with urbanization trends and large-scale infrastructure investment. Construction stakeholders are increasingly selecting materials that support energy efficiency and long-term durability. Industry collaboration is reinforcing adoption, such as Expanded Clay Solutions partnering with a major construction firm to develop lightweight concrete solutions tailored to modern building requirements. Regulatory encouragement for sustainable construction materials is supporting scale-driven demand, which is ensuring continued dominance of construction applications.

Wastewater treatment and environmental remediation is slated to be the fastest-growing application segment through 2033, driven by tightening environmental regulations and rising investment in water infrastructure upgrades. Expanded clay is offering high porosity, chemical inertness, and effective filtration performance, which is making it well suited for biofiltration systems, stormwater management, and remediation projects. Product innovation is supporting this shift. For example, Sika AG has announced plans of launching an eco-friendly expanded clay aggregate line optimized for environmental applications. Sustainability commitments and infrastructure modernization programs are strengthening long-term demand, positioning wastewater and environmental applications as a high-growth opportunity within the expanded clay market.

Regional Insights

North America Expanded Clay Market Trends

North America is expected to lead with an estimated 45% of the expanded clay market share in 2026, anchored by sustained demand from the United States construction sector and the widespread adoption of LEED building codes. Federal infrastructure programs such as the Infrastructure Investment and Jobs Act (IIJA) are supporting the use of lightweight concrete and geotechnical fill materials, which are reducing structural dead loads by approximately 25-40% in large projects. State-level energy efficiency mandates are driving the use of thermally efficient aggregates across commercial buildings and resilient infrastructure. Innovation hubs in Texas and kiln manufacturing centers in the Midwest are accelerating the adoption of low-emission production processes, which are cutting carbon dioxide (CO?) emissions by nearly 20%. Competitive intensity is remaining moderate, with producers such as Big River Resources and LECA North America focusing on operational efficiency, capacity optimization, and compliance with sustainability standards. Big River Resources is expanding kiln capacity in Texas to meet rising demand from LEED-certified construction projects.

The market for expanded clay in North America is growing at a stable pace, supported by sustainability-driven construction, urban retrofit programs, and expanding wastewater treatment investments. Institutional procurement policies are favoring large-scale infrastructure projects such as highway embankments, bridge approaches, and flood mitigation systems, where lightweight aggregates deliver structural and cost advantages. Ongoing production innovations are reducing the environmental footprint of expanded clay while supporting premium product development for horticulture and hydroponic applications. Resilient infrastructure investment cycles and long-term federal incentives are strengthening adoption across public sector projects. Strong research and development capabilities are enabling manufacturers to improve energy efficiency and product consistency. The proven performance of expanded clay in lightweight concrete applications is ensuring stable volume uptake, while an established regional supply chain is maintaining reliable delivery for time-sensitive public works and commercial developments.

Europe Expanded Clay Market Trends

Europe is expected to hold a sizable share of the expanded clay market, with Germany, the United Kingdom, France, and Spain serving as the primary consumption centers. Demand is being driven by strong regulatory alignment and technology leadership, particularly through standards such as European Norm (EN) 13055, which is favoring lightweight aggregates in energy-efficient construction. Carbon pricing mechanisms under the European Union Emissions Trading System (EU ETS) are incentivizing material substitution, as buildings using expanded clay are reducing reliance on structural steel by an estimated 15-20%. Sustained urban investment is supporting both residential and infrastructure projects, while environmental, social, & governance (ESG) compliance requirements are increasing the use of expanded clay in precast concrete panels and filtration media. Market leaders such as Laterlite and Argilith are maintaining quality and consistency through advanced rotary kiln technologies, reinforcing trust among large construction and municipal buyers.

Regional growth is continuing to be supported by the EU Green Deal, which is accelerating renovation activity across aging building stock and public infrastructure. Applications in wastewater treatment and soil remediation are complementing demand from structural construction, improving overall market resilience. Fluidized bed production technologies are enabling the development of premium horticultural products with consistent particle size and performance characteristics. Germany’s precast construction industry is leading adoption in multi-family housing and urban redevelopment projects, where weight reduction and thermal efficiency are critical. Circular economy initiatives are enhancing the recycling and reuse of expanded clay within construction waste streams, which is improving lifecycle performance metrics. Regulatory support, combined with diversified end uses and advanced production technologies, is reinforcing Europe’s premium positioning and long-term competitiveness in the global expanded clay market.

Asia Pacific Expanded Clay Market Trends

Asia Pacific is projected to be the fastest-growing regional market for expanded clay at an estimated 6.5% CAGR between 2026 and 2033. Rapid urbanization, large-scale infrastructure projects, and competitive manufacturing costs drive adoption of lightweight, thermally efficient aggregates. Government initiatives, including China’s sponge city program and India’s National Infrastructure Pipeline, support the use of expanded clay in public housing, rail embankments, and flood management projects, filling 30–50% of voids efficiently. Japan focuses on sustainable urban retrofits and high-rise residential projects, while ASEAN countries increasingly adopt expanded clay for water treatment and geotechnical fills. Leading industry developments include Plasmor India’s 50,000-ton plant in Gujarat and Shandong-based kiln expansions in China, improving supply chain reach. Regional adoption is supported by rising standards for energy efficiency and low-carbon construction.

Massive infrastructure pipelines and ongoing residential expansion sustain strong demand for construction-grade expanded clay, particularly in high-rise buildings and large civil works. National low-carbon pledges encourage the adoption of hydroponics and environmental remediation applications, expanding usage beyond traditional structural roles. Investments in water supply, sanitation, and stormwater management amplify non-structural applications such as filtration media and geotechnical fills. Metro and railway expansions create consistent demand for lightweight aggregates in embankments and substructures. Rapid urbanization, combined with growing domestic production, positions. Southeast Asian manufacturing hubs are increasingly serving as export platforms to Oceania, further strengthening supply chains and market reach.

Competitive Landscape

The global expanded clay market structure is moderately consolidated, with established producers such as Laterlite S.p.A., Argex, Liapor GmbH, Big River Resources, and Plasmor India Private Limited accounting for the lion’s share of global revenue. These companies are leveraging extensive distribution networks, long-standing customer relationships across construction and environmental sectors, and deep expertise in rotary kiln and fluidized bed production technologies. Continuous investment in research and development is enabling them to maintain consistent product quality, improve energy efficiency, and reduce emissions during manufacturing. This focus is strengthening their ability to supply application-specific solutions for segments such as structural lightweight concrete, hydroponics, and geotechnical engineering, where performance consistency and regulatory compliance are critical purchasing criteria.

At the same time, regional and niche manufacturers such as LECA North America, Argilith GmbH, and Shandong LECA plants are maintaining relevance by focusing on localized supply models, specialized lightweight aggregate grades, and environmental applications. High capital intensity, volatile energy costs, and stringent environmental regulations are continuing to limit large-scale new market entry. However, innovation in low-emission production processes and customized product geometries is gradually creating opportunities for smaller firms to differentiate. Market consolidation is progressing steadily, as leading players are expanding through capacity additions, joint ventures, and regional plant investments. Technological partnerships are improving production efficiency and are enabling premium product development, which is supporting gradual entry into higher-margin environmental and horticultural applications.

Key Industry Developments

- In November 2025, BASF showcased its Cavipor® expanded clay foam insulation product at the Klimafestival Berlin 2025, highlighting a new material class designed to improve energy-efficiency in building renovations and insulation applications. The mineral-based clay foam expands on site from three water-based components to fill cavities, is non-flammable, water-repellent, and vapor-permeable.

- In June 2025, LECA International actively participated in the European Expanded Clay Association General Assembly, emphasizing sustainability, decarbonization, and regulatory alignment. The company contributed to discussions on circular economy practices and emissions reduction pathways affecting lightweight aggregates. ?

- In March 2025, Northern Ireland’s Department of Agriculture, Environment and Rural Affairs (DAERA) reported that lightweight expanded clay aggregate (LECA) was applied to uncovered above-ground slurry stores at the CAFRE Farm Centres to reduce ammonia emissions from slurry. LECA is a naturally produced clay sphere aggregate that floats on the slurry surface and forms a mitigation layer, offering a lower-cost emission reduction option compared with impermeable covers and other alternatives.

Companies Covered in Expanded Clay Market

- LECA International

- Saint-Gobain

- Arcosa Inc.

- Holcim Group

- Uralita Group

- Leca Asia

- Argex Group

- Laterlite S.p.A.

- Maxit Group

- Buildex

- Shandong Leca

- ESCS

Frequently Asked Questions

The global expanded clay market is projected to reach US$ 3.3 billion in 2026.

Rising demand for lightweight, energy-efficient construction materials and increasing investment in sustainable infrastructure are the primary growth drivers.

The market is poised to witness a CAGR of 6.4% from 2026 to 2033.

Opportunities include adoption of sustainable materials in green buildings, wastewater treatment systems, and hydroponics driven by low-carbon construction mandates.

Laterlite S.p.A., Argex, Liapor GmbH, Big River Resources, and Plasmor India are among the key market players.