- Electric Mobility

- EV Drive Module Market

EV Drive Module Market Size, Share, and Growth Forecast, 2026 - 2033

EV Drive Module Market by Powertrain Type (BEV (Battery Electric Vehicle), PHEV (Plug-in Hybrid Electric Vehicle), Others), Peak Power Type (<150 kW, ≥150 kW), Vehicle Type, Sales Channel, and Regional Analysis for 2026 - 2033

EV Drive Module Market Size and Trends Analysis

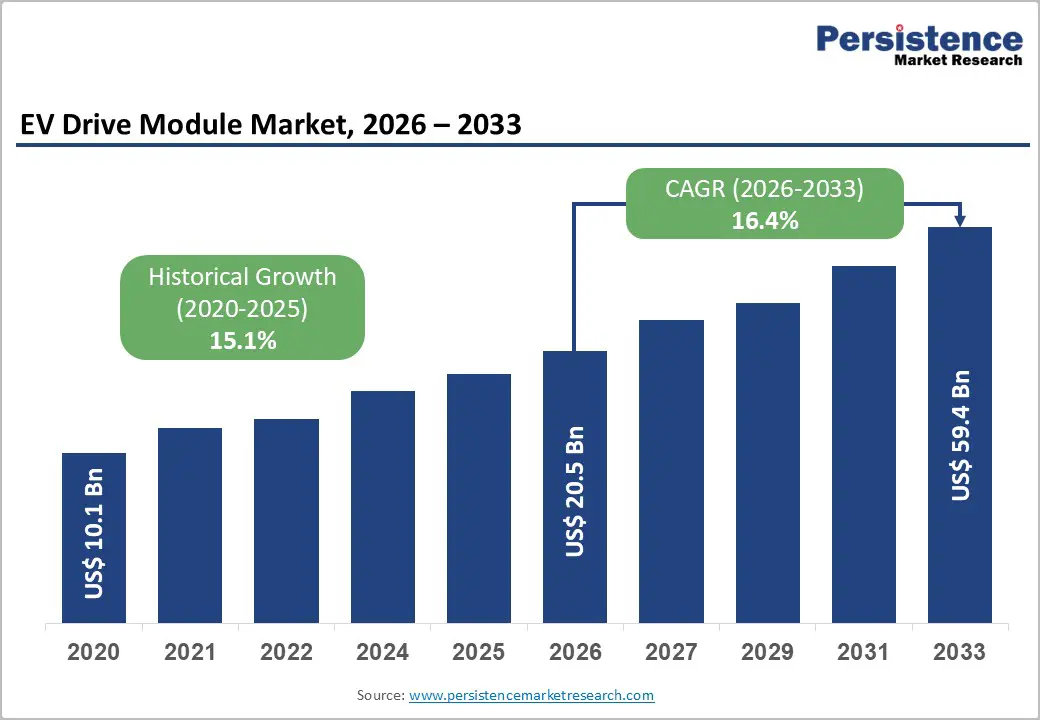

The global EV drive module market size is likely to be valued at US$20.5 billion in 2026 and is expected to reach US$59.4 billion by 2033, growing at a CAGR of 16.4% between 2026 and 2033, driven by increasing electric vehicle adoption, advancements in integrated e-axle technologies, and growing demand for compact and efficient powertrain architectures. Vehicle manufacturers are increasingly adopting integrated drive modules that combine electric motors, power electronics, and transmission systems into a single unit to improve vehicle efficiency, reduce weight, and optimize manufacturing costs. Rising investments in EV production, supportive government policies, and expanding charging infrastructure are expected to further strengthen demand throughout the forecast period.

Key Industry Highlights:

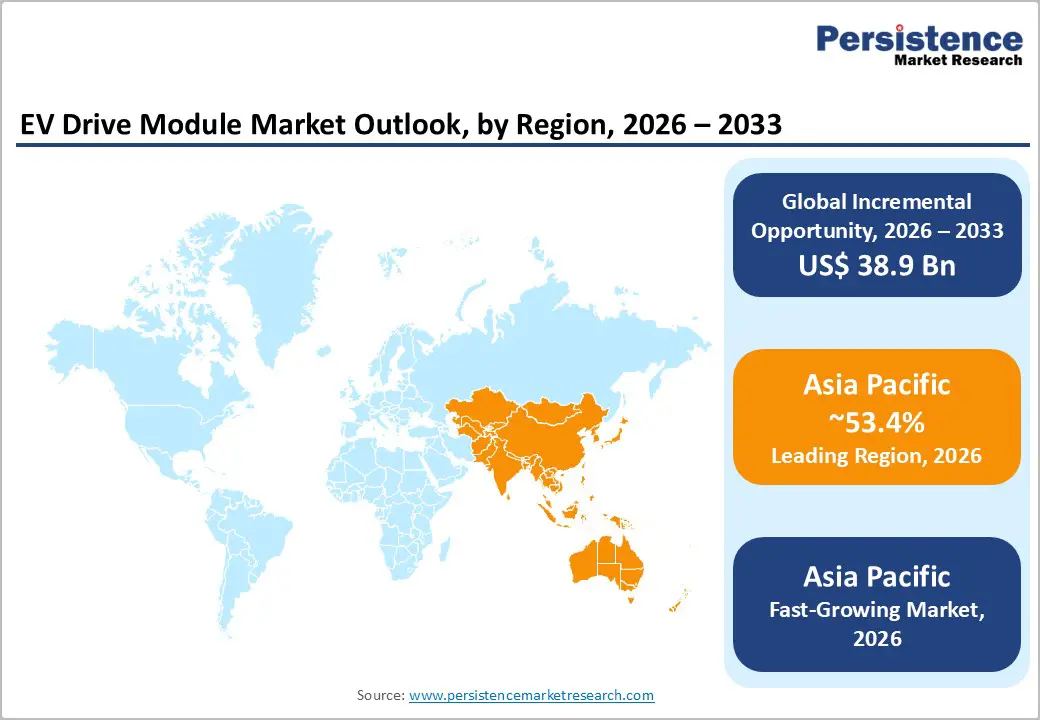

- Leading Region: Asia Pacific is projected to account for approximately 53.4% of the market share in 2026, driven by China's dominant EV production and consumption ecosystem, extensive battery manufacturing capacity, and integrated supply chains.

- Fastest-growing Region: Asia Pacific is expected to register the highest growth rate through 2033, supported by rapid EV adoption in China, India, and Southeast Asia, alongside continued investments in localized manufacturing and charging infrastructure.

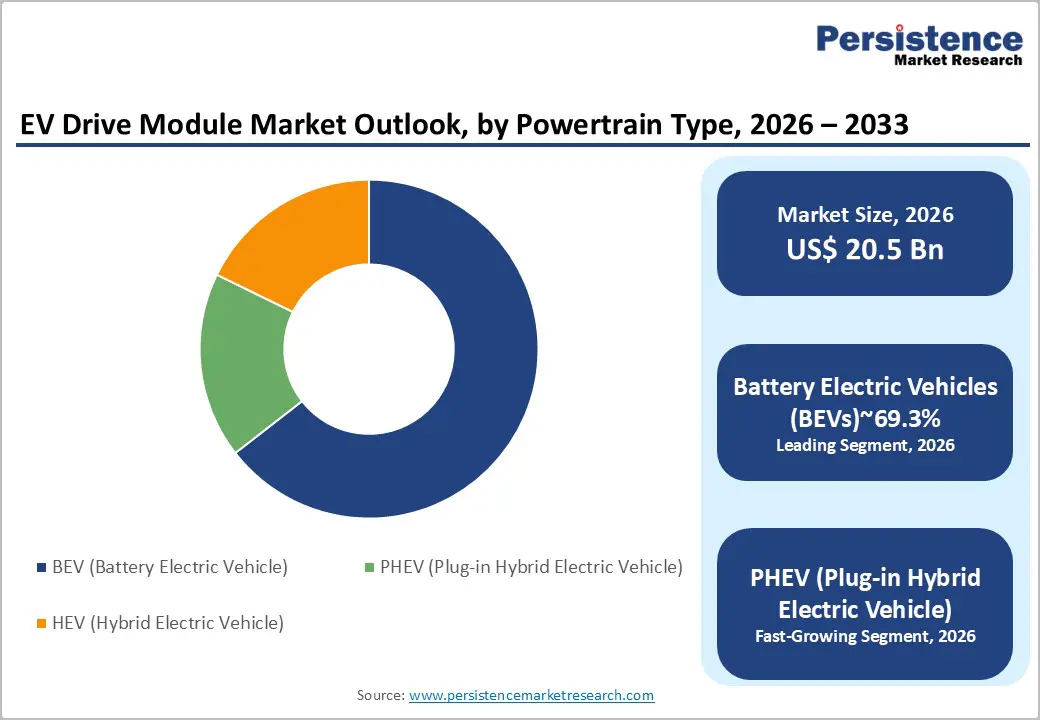

- Dominant Powertrain Type: Battery Electric Vehicles (BEVs) are expected to hold an anticipated 69.3% market share in 2026, supported by growing deployment of dedicated EV platforms and increasing consumer preference for fully electric vehicles.

- Leading Peak Power Type: The <150 kW drive module segment is estimated to account for approximately 65.3% market share in 2026, reflecting its widespread adoption in compact and mid-sized passenger EVs, which represent the highest-volume segment of the global electric vehicle market.

DRO Analysis

Driver - Rising Electric Vehicle Adoption Accelerates Demand for Integrated Drive Modules

Global electric vehicle adoption continues to serve as the primary growth engine for the EV Drive Module Market. According to international energy agencies, global EV sales surpassed 17 million units in 2024, representing more than 20% of total vehicle sales worldwide. Growing consumer acceptance of battery electric vehicles (BEVs), combined with stricter emissions regulations, is encouraging automakers to expand electrified vehicle portfolios.

Integrated drive modules have emerged as a preferred solution because they simplify vehicle architecture, improve powertrain efficiency, and reduce manufacturing complexity. Automakers are increasingly standardizing drive module platforms across multiple vehicle models, allowing greater economies of scale and faster product development cycles. As global EV production capacity expands, the demand for high-performance and cost-efficient drive modules is expected to rise proportionally, creating sustained revenue opportunities for suppliers throughout the value chain.

Government Regulations and Charging Infrastructure Expansion Support Market Growth

Government initiatives promoting vehicle electrification continue to strengthen the market outlook. Regulatory authorities across North America, Europe, and Asia Pacific have implemented stricter vehicle emission standards, fuel economy requirements, and zero-emission vehicle targets. These policies are encouraging automotive manufacturers to accelerate electrification investments and increase EV production volumes.

Simultaneously, substantial investments in charging infrastructure are reducing consumer concerns related to driving range and charging accessibility. Expanding public charging networks improves the practicality of EV ownership while supporting fleet electrification programs for commercial vehicles. The combined effect of regulatory support and infrastructure development is creating favorable conditions for broader EV adoption, directly increasing demand for integrated drive modules across both passenger and commercial vehicle applications.

Restraint - High Development Costs and Technical Complexity Limit Market Expansion

Despite strong growth prospects, high development and manufacturing costs remain a significant challenge for the EV Drive Module Market. Modern drive modules integrate multiple high-value components, including electric motors, inverters, reduction gearboxes, thermal management systems, and software controls. This integration requires extensive engineering expertise, testing, and validation procedures.

Automakers also demand multiple power configurations and vehicle-specific adaptations, increasing product development costs for suppliers. In cost-sensitive markets, manufacturers may prioritize lower-cost electrification strategies or hybrid powertrain solutions instead of fully integrated electric drive systems. Furthermore, fluctuations in semiconductor availability and raw material prices can increase production expenses, affecting supplier profitability and slowing broader market penetration.

Regional Policy Variability Creates Demand Uncertainty

The pace of EV adoption varies considerably across regions due to differences in government incentives, charging infrastructure availability, and consumer purchasing behavior. Changes in subsidy programs or regulatory priorities can significantly impact EV demand forecasts.

As drive module suppliers typically invest several years before vehicle production begins, uncertainty surrounding future EV volumes may affect investment decisions and capacity expansion plans. Uneven adoption rates across major automotive markets can also create challenges related to production planning, inventory management, and manufacturing utilization rates, potentially impacting long-term profitability.

Opportunity - Localization of EV Manufacturing Creates New Revenue Streams

Asia Pacific has emerged as the largest EV manufacturing hub globally, creating substantial opportunities for localized drive module production. Regional governments continue to support domestic EV manufacturing through industrial policies, investment incentives, and supply chain development initiatives.

Localizing drive module manufacturing enables suppliers to reduce logistics costs, improve supply chain resilience, and strengthen relationships with regional vehicle manufacturers. Growing EV production in China, India, and Southeast Asia is expected to generate significant demand for locally sourced drive modules, creating opportunities for both global suppliers and regional component manufacturers.

High-Power Drive Modules Present Significant Growth Potential

Demand for higher-output electric powertrains is increasing as automakers introduce premium electric vehicles, performance SUVs, electric buses, and heavy-duty commercial vehicles. These applications require advanced drive modules capable of delivering superior torque, acceleration, and continuous power output.

The transition toward 800-volt electrical architectures and high-performance electric platforms is further supporting demand for advanced drive systems. Suppliers capable of delivering efficient thermal management, power-dense motor technologies, and integrated software capabilities are expected to capture significant market share within this rapidly expanding segment.

Category-wise Analysis

Powertrain Type Insights

Battery Electric Vehicles (BEVs) are anticipated to account for approximately 69.3% of the market share in 2026, making them the dominant powertrain segment. Their leadership stems from complete reliance on electric propulsion systems, which require integrated drive modules as a core drivetrain component. Growing adoption of dedicated EV platforms such as the Tesla Model Y, BYD Seal, and Hyundai IONIQ 5 continues to support demand for standardized e-drive architectures. Declining battery costs and increasingly stringent emissions regulations are further accelerating BEV production worldwide.

Plug-in Hybrid Electric Vehicles (PHEVs) are expected to be the fastest-growing segment. Strong demand for models such as the BYD Song Plus DM-i, Li Auto L-series, and Mitsubishi Outlander PHEV highlights growing consumer preference for extended driving range without full dependence on charging infrastructure. Meanwhile, Hybrid Electric Vehicles (HEVs) maintain steady growth, particularly in cost-sensitive markets where gradual electrification remains a preferred strategy.

Peak Power Type Insights

Drive modules rated below 150 kW are anticipated to hold approximately 65.3% of the market share, making them the leading power category. These systems are commonly deployed in high-volume passenger EVs such as the Nissan Leaf, MG4 Electric, and BYD Dolphin, where efficiency, affordability, and compact packaging are key priorities. Their widespread use across compact and mid-sized vehicle segments continues to support market dominance.

Drive modules rated 150 kW and above are projected to be the fastest-growing segment through 2033. Demand is being driven by premium and performance-oriented EVs such as the Tesla Model S Plaid, Porsche Macan Electric, Kia EV9 GT, and emerging electric truck platforms. Advances in 800V architectures, thermal management systems, and power electronics are enabling higher output levels while maintaining efficiency, making this category increasingly attractive for both luxury and commercial vehicle applications.

Regional Insights

North America EV Drive Module Market Trends

North America is supported by strong technological innovation, advanced automotive manufacturing capabilities, and increasing EV adoption. The region remains a key center for power electronics, electric motors, and software-defined vehicle development, creating favorable conditions for drive module suppliers. Growing demand for electric pickup trucks, SUVs, and commercial EVs continues to drive investment in localized production and supply chain expansion.

U.S. EV Drive Module Market

The U.S. represents the largest market in North America, accounting for more than 80% of regional demand. Growth is supported by increasing production of electric vehicles from both established automakers and emerging EV manufacturers. Strong consumer demand for electric pickup trucks, premium SUVs, and fleet vehicles is accelerating adoption of integrated drive modules. Investments in domestic battery manufacturing, semiconductor production, and EV assembly facilities are further strengthening the regional supply chain.

Canada EV Drive Module Market Trends

Canada plays an important role in the North American EV ecosystem through its battery material resources and growing EV manufacturing investments. Government initiatives supporting battery production, critical mineral processing, and zero-emission vehicle adoption are encouraging the development of local EV supply chains. The country's strong focus on clean energy also creates favorable conditions for long-term EV market growth.

Europe EV Drive Module Market Trends

Europe is supported by stringent emissions regulations, ambitious electrification targets, and a highly developed automotive industry. The region remains a major center for EV technology development and powertrain innovation, driving demand for advanced integrated drive modules.

Germany EV Drive Module Market Trends

Germany is the largest EV drive module market in Europe and serves as the region's automotive manufacturing hub. The country benefits from a strong supplier ecosystem, extensive engineering expertise, and significant investments in next-generation electric vehicle platforms. German automakers continue to expand dedicated EV production, creating sustained demand for high-efficiency drive modules and e-axle systems.

U.K. EV Drive Module Market Trends

The U.K. continues to strengthen its EV market through investments in charging infrastructure and clean mobility initiatives. Rising adoption of electric passenger vehicles and commercial fleets is supporting increased demand for electric propulsion technologies. The country also remains an important center for EV research, software development, and advanced automotive engineering.

France EV Drive Module Market Trends

France has emerged as a key EV market due to supportive government policies, consumer incentives, and strong commitments to transportation decarbonization. Domestic automotive manufacturers continue to expand their electric vehicle portfolios, increasing demand for integrated drive systems and high-efficiency powertrain technologies.

Europe's continued focus on sustainability, emissions reduction, and electrification is expected to generate significant opportunities for suppliers specializing in compact, efficient, and software-enabled drive module solutions.

Asia Pacific EV Drive Module Market Trends

Asia Pacific is both the largest and fastest-growing regional market, accounting for approximately 53.4% of market revenue in 2026. The region benefits from extensive EV manufacturing capacity, integrated supply chains, strong government support, and leadership in battery production. Rapid urbanization, rising vehicle electrification rates, and expanding domestic EV industries continue to reinforce regional dominance.

China EV Drive Module Market Trends

China dominates the Asia Pacific market, contributing approximately 77% of regional revenue. As the world's largest EV producer and consumer, China serves as the primary growth engine for global EV drive module demand. Strong government support, extensive charging infrastructure, and vertically integrated supply chains have enabled large-scale deployment of electric vehicles across passenger and commercial segments. The country also leads in battery manufacturing, electric motor production, and power electronics development.

Japan EV Drive Module Market Trends

Japan accounts for approximately 9% of the Asia Pacific market and remains an important center for advanced automotive technologies. Japanese manufacturers continue to invest in electrification, hybrid technologies, and high-efficiency powertrain systems. The country's strengths in motor engineering, precision manufacturing, and automotive innovation support steady demand for advanced drive modules.

South Korea EV Drive Module Market Trends

South Korea contributes approximately 7% of regional demand, supported by its globally competitive automotive and battery industries. Strong investments in EV production, battery technology, and semiconductor manufacturing have positioned the country as a key supplier of electrification components. Increasing exports of electric vehicles are expected to further drive demand for integrated drive systems.

Competitive Landscape

The global EV drive module market is moderately consolidated, with a combination of global automotive suppliers and specialized electrification technology providers competing for market share. Competition centers on technological innovation, manufacturing scale, powertrain efficiency, and regional production capabilities. Long-term supply agreements with vehicle manufacturers and localized production networks remain key competitive advantages. Market participants continue to invest heavily in research and development to improve performance, reduce system costs, and enhance power density.

Market leaders continue to focus on product integration, manufacturing localization, and scalable platform development. Investment priorities include high-voltage architectures, software-defined powertrain controls, thermal management innovations, and cost optimization. Strategic partnerships with vehicle manufacturers and expansion into emerging EV markets remain critical growth initiatives.

Key Industry Developments:

- In March 2026, Valeo inaugurated a new electric powertrain manufacturing line in Pune, India, to produce highly integrated 3-in-1 e-Axles for Mahindra’s Born Electric vehicle platform.

- In June 2025, ZF Friedrichshafen AG launched its new SELECT e-drive platform, a modular electric drive architecture covering power outputs from 100 kW to 300 kW.

- In April 2025, BorgWarner introduced its iM-575 integrated inverter-motor drive module for heavy-duty electric commercial vehicles at the Advanced Clean Transportation (ACT) Expo 2025.

Companies Covered in EV Drive Module Market

- Robert Bosch GmbH

- ZF Friedrichshafen AG

- Magna International Inc.

- BorgWarner Inc.

- Valeo SA

- Schaeffler AG

- GKN Automotive Limited

- Nidec Corporation

- Hitachi Astemo, Ltd.

- Dana Incorporated

- MAHLE GmbH

- Continental AG

- Aisin Corporation

- Hyundai Mobis Co., Ltd.

- Denso Corporation

- Vitesco Technologies Group AG

Frequently Asked Questions

The global EV drive module market is estimated to be valued at US$20.5 billion in 2026.

The EV drive module market is projected to reach US$59.4 billion by 2033.

Key trends include the growing adoption of integrated e-axle systems, increasing deployment of high-power drive modules (≥150 kW), expansion of 800V vehicle architectures, localization of EV manufacturing, and rising electrification of commercial vehicles.

Battery Electric Vehicles (BEVs) are the leading segment, accounting for approximately 69.3% of the market share, owing to their complete reliance on electric propulsion systems.

The EV drive module market is expected to grow at a CAGR of 16.4% between 2026 and 2033.

Major companies include Robert Bosch GmbH, ZF Friedrichshafen AG, Magna International Inc., BorgWarner Inc., and Valeo SA.