- Electrical Equipment & Services

- Electric Motor Market

Electric Motor Market Size, Share, and Growth Forecast, 2026 - 2033

Electric Motor Market by Voltage (Low Voltage, Medium Voltage, Others), Speed (Regular Speed, High Speed, Others), Power Rating, Application, and Regional Analysis for 2026 - 2033

Electric Motor Market Size and Trends Analysis

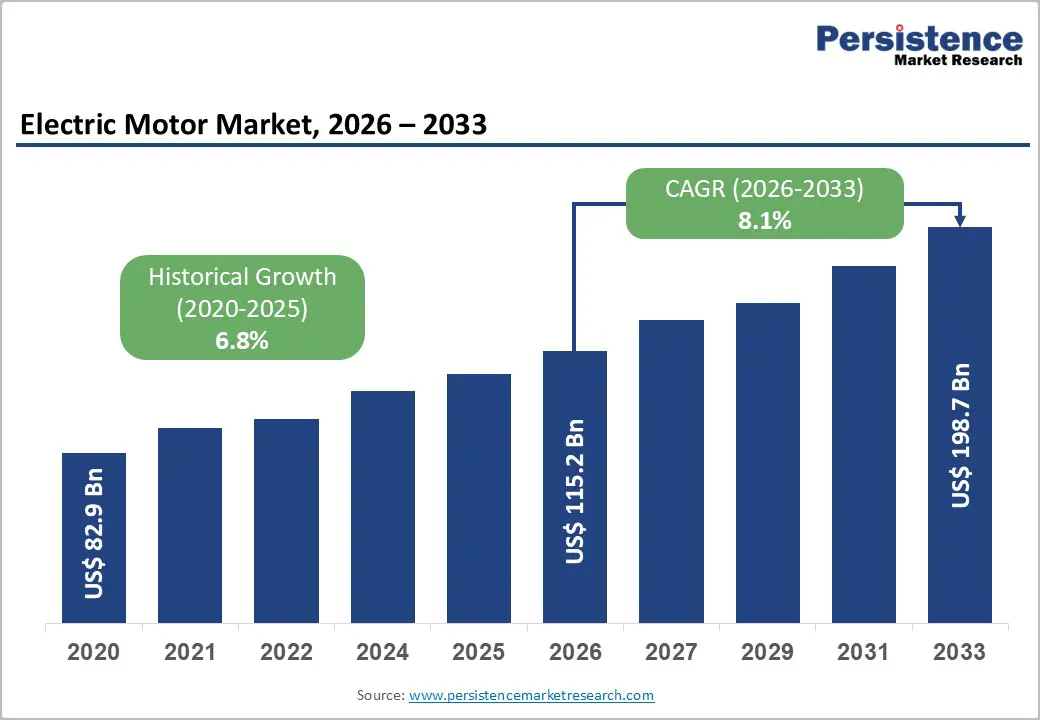

The global electric motor market size is likely to be valued at US$ 115.2 billion in 2026 and is expected to reach US$ 198.7 billion by 2033, growing at a CAGR of 8.1% between 2026 and 2033, driven by accelerating electrification across transportation (EV powertrains), expanding industrial automation (smart factories and variable-speed drives), and rising demand for energy-efficient motor replacements.

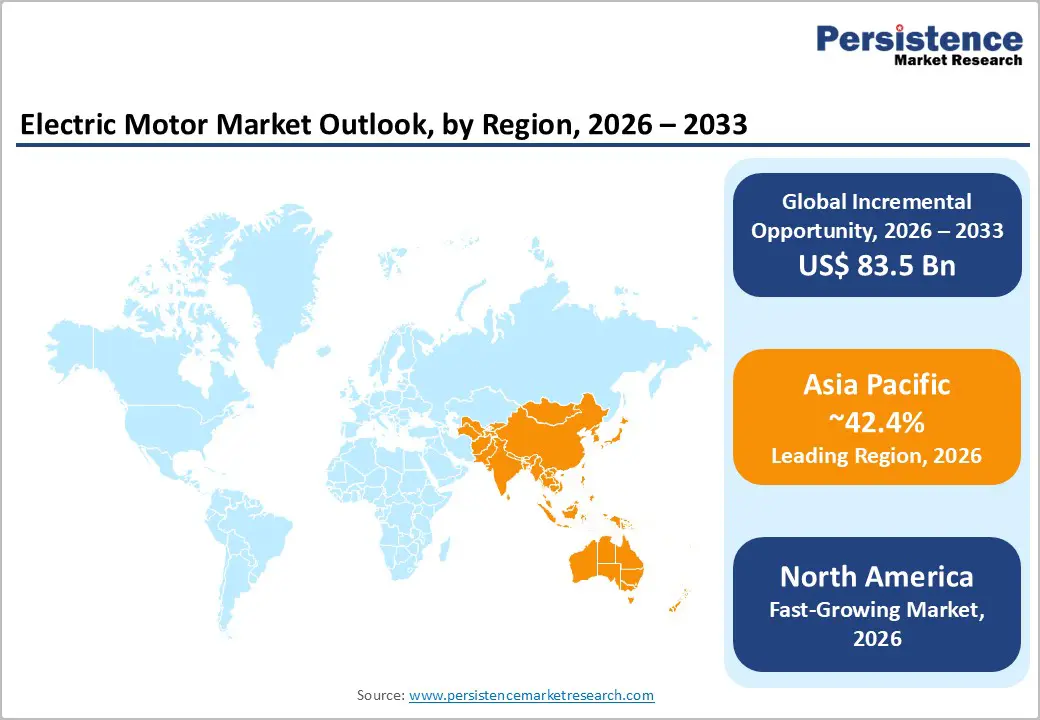

Asia Pacific remains the dominant regional market, supported by strong manufacturing ecosystems and increasing infrastructure investments. Supply-side consolidation and technology-led differentiation, such as high-efficiency motor platforms, reduced rare-earth dependency, and intelligent motor control systems, are reshaping competitive dynamics. Increasing EV adoption and tightening energy-efficiency regulations are boosting demand for high-performance, power-dense motors. Industrial digitalization is accelerating the use of servo and variable-frequency drive-compatible motors, while HVAC and infrastructure upgrades are sustaining a steady retrofit cycle. Recent investments in production capacity and strategic restructuring among manufacturers indicate a shift toward localized manufacturing and faster delivery capabilities.

Key Industry Highlights:

- Leading Region: Asia Pacific is the leading region in the market, accounting for an anticipated 42.4% share of the market, driven by large-scale manufacturing, strong EV production, and robust industrial demand.

- Fastest-growing Region: North America is the fastest-growing region, supported by increasing EV adoption, industrial automation, and favorable government policies promoting energy efficiency and domestic manufacturing expansion.

- Investment Plans: Market participants are actively investing in regional manufacturing expansion and capacity enhancement, particularly in Europe and Asia Pacific, to improve supply chain efficiency, reduce lead times, and support growing demand for high-efficiency and EV-specific motors.

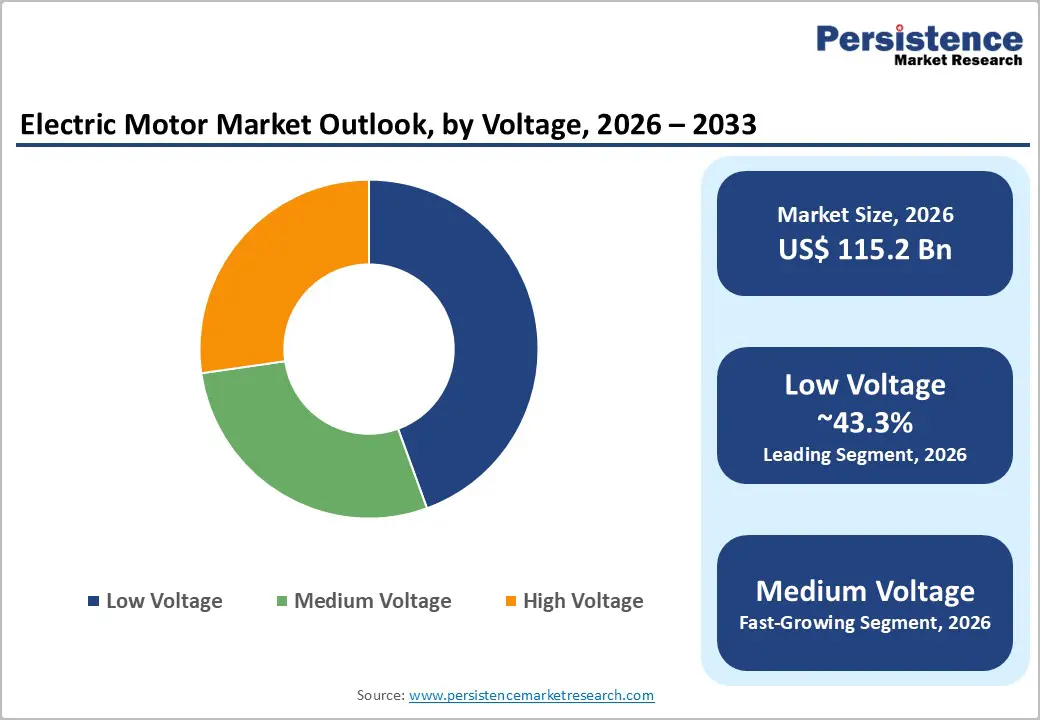

- Dominant Voltage: Low-voltage motors (up to 1 kV) dominate the voltage segment, holding an anticipated 43.3% market share, due to their widespread use across industrial machinery, HVAC systems, and household applications.

- Leading Speed: Regular speed motors (up to 3000 rpm) lead the speed segment with an anticipated 81.2% share, driven by their extensive application in pumps, fans, conveyors, and other conventional industrial equipment.

| Key Insights | Details |

|---|---|

| Electric Motor Market Size (2026E) | US$115.2 Bn |

| Market Value Forecast (2033F) | US$198.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Electrification of Transport and EV Powertrain Adoption

The global transition toward electric mobility represents a fundamental growth driver for the electric motor market. As electric vehicles scale across passenger, commercial, and industrial segments, demand for traction motors and auxiliary systems continues to expand. These motors are more complex and higher-value compared to traditional industrial motors, requiring enhanced thermal management, efficiency, and precision control. This shift increases both unit demand and average selling prices. The expansion of EV manufacturing ecosystems globally is also encouraging motor manufacturers to invest in specialized production facilities and localized supply chains, strengthening long-term revenue growth prospects.

Energy-Efficiency Regulations and Industrial Electrification

Stringent global energy-efficiency standards are accelerating the replacement of older motors with advanced, high-efficiency variants such as IE3, IE4, and IE5. Motors consume a significant share of industrial electricity, making efficiency upgrades a cost-effective strategy for reducing operational expenses. Regulatory mandates are encouraging industries to adopt low-loss motors, thereby increasing demand for premium products. This transition is not limited to new installations but also includes large-scale retrofits across manufacturing plants, utilities, and commercial buildings, expanding the overall addressable market.

Industrial Automation and Digitalization

The rise of Industry 4.0 is significantly influencing motor demand, particularly for smart, connected, and variable-speed systems. Manufacturers are integrating motors with sensors, digital monitoring tools, and predictive maintenance capabilities to enhance operational efficiency. These advanced systems enable real-time performance tracking and reduced downtime, creating additional value beyond hardware sales. The growing adoption of robotics, automated production lines, and material handling systems further drives demand for high-precision motors, increasing both unit volumes and service-based revenue opportunities.

Barrier Analysis - Raw Material and Component Cost Volatility

Fluctuations in the prices of key raw materials such as copper, steel, and rare-earth elements create cost pressures for motor manufacturers. These materials are essential for winding, structural components, and permanent magnets. Price volatility can increase production costs and reduce profit margins, especially when manufacturers are unable to pass on costs to end users. In periods of sharp price increases, customers may delay purchasing decisions, particularly for premium motors, impacting short-term demand and slowing market growth.

Fragmented Aftermarket and Regulatory Variability

The electric motor aftermarket remains highly fragmented, with varying standards and service practices across regions. Differences in regulatory frameworks, testing standards, and certification requirements increase complexity for global manufacturers. These inconsistencies can lead to longer product approval timelines and higher compliance costs. The lack of standardization also limits scalability for service-based business models, such as predictive maintenance and lifecycle management solutions, thereby constraining long-term value creation.

Opportunity Analysis - Energy-Efficiency Retrofit Programs

A large installed base of aging motors presents a significant opportunity for replacement with high-efficiency models, particularly as legacy systems often operate below current efficiency standards such as IE3 and IE4. Government incentives and utility rebate programs are actively encouraging industries to upgrade equipment, enabling measurable reductions in energy consumption and carbon emissions. For instance, energy-efficiency initiatives led by agencies such as the U.S. Department of Energy and frameworks aligned with the International Energy Agency emphasize motor system optimization as a key lever for industrial decarbonization. These retrofit programs generate recurring revenue streams through maintenance, spare parts, and service contracts.

Localization of Manufacturing and Supply Chains

The ongoing shift toward regional manufacturing is creating strategic opportunities for motor producers to establish production facilities closer to end markets. Localization reduces logistics costs, shortens delivery timelines, and mitigates risks associated with global supply chain disruptions and trade restrictions. This approach is particularly advantageous in high-growth regions such as Asia Pacific and Europe, where proximity to OEMs and industrial clusters enhances responsiveness and collaboration. Governments are also supporting localization through industrial policies and incentives aimed at boosting domestic manufacturing capabilities. Companies investing in regional production hubs can benefit from improved demand forecasting, faster customization, and stronger customer engagement.

Smart Motors and Digital Service Integration

The integration of digital technologies into motor systems is unlocking new revenue streams through value-added services and performance-based offerings. Smart motors equipped with sensors, IoT connectivity, and embedded analytics enable predictive maintenance, condition monitoring, and real-time performance optimization. This shift allows manufacturers to transition from traditional product sales to service-oriented business models that emphasize uptime and efficiency. For example, companies such as Siemens and ABB are actively deploying digital platforms that integrate motors with cloud-based monitoring systems, enabling remote diagnostics and energy management. These capabilities reduce unplanned downtime, extend equipment lifespan, and lower the total cost of ownership for end users.

Category-wise Analysis

Voltage Insights

Low-voltage motors dominate the market, accounting for an anticipated 43.3% of market share in 2026, reflecting their extensive deployment across industrial machinery, HVAC systems, and household appliances. Their compatibility with standard electrical infrastructure makes them cost-effective, easy to install, and widely accessible for both OEM and retrofit applications. These motors are heavily used in pumps, compressors, conveyors, and ventilation systems across manufacturing plants and commercial buildings. For example, low-voltage induction motors are commonly deployed in HVAC units in commercial complexes and in assembly-line equipment in automotive manufacturing. The large installed base ensures steady demand for maintenance, replacement, and spare parts, reinforcing their dominance in both primary sales and the aftermarket ecosystem.

Medium-voltage motors are the fastest-growing segment, driven by increasing demand from heavy industries such as mining, oil and gas, power generation, and water treatment. These applications require high-power motors capable of operating under demanding conditions with improved efficiency and durability. The growing adoption of medium-voltage variable-frequency drives enhances energy savings and process control, making them increasingly attractive for large-scale operations. For instance, medium-voltage motors are widely used in pipeline pumping stations, large industrial compressors, and mining haulage systems. Rising investments in infrastructure and industrial electrification, particularly in emerging economies, are expected to further accelerate adoption and expand this segment’s market share over the forecast period.

Speed Insights

Regular-speed motors hold the largest share, accounting for an anticipated 81.2% of the market in 2026, due to their widespread use in conventional industrial and commercial applications. These motors are well-suited for equipment such as pumps, fans, blowers, and conveyors, where consistent and moderate rotational speeds are sufficient. Their cost-effectiveness, durability, and compatibility with existing mechanical systems make them the preferred choice for a broad range of industries. For example, regular-speed motors are extensively used in water treatment plants, HVAC air handling units, and material handling systems in warehouses. Their standardized designs and well-established global supply chains ensure consistent availability, supporting sustained demand across both developed and developing markets.

High-speed motors are experiencing the fastest growth, driven by increasing demand for compact, lightweight, and high-performance solutions. These motors are critical in applications requiring high power density, such as electric vehicle powertrains, aerospace actuation systems, and high-speed compressors. For instance, EV traction motors often operate at higher speeds to optimize efficiency and reduce system size, while aerospace systems rely on high-speed motors for precision and weight reduction. Advances in materials, cooling technologies, and rotor dynamics are enabling improved performance and reliability at higher speeds. As industries continue to prioritize efficiency, miniaturization, and performance optimization, high-speed motors are expected to gain significant traction in next-generation applications.

Regional Insights

North America Electric Motor Market Trends - EV-Driven Demand & Smart Motor Integration in Industrial Automation

North America is experiencing strong growth driven by industrial modernization, the reshoring of manufacturing, and increasing EV adoption. The U.S. leads the regional market due to its advanced industrial base, high HVAC penetration, and expanding EV ecosystem. Government policies supporting energy efficiency and electrification are accelerating the adoption of high-performance motors, particularly in manufacturing and commercial infrastructure. For example, initiatives under the Inflation Reduction Act have encouraged domestic EV production, indirectly boosting demand for traction motors and auxiliary motor systems. At the corporate level, companies such as Regal Rexnord and Rockwell Automation are expanding automation and motion control capabilities, integrating motors with digital control platforms.

Investments in domestic manufacturing and automation technologies are further strengthening the region’s position. Tesla’s continued expansion of EV production facilities has significantly increased demand for high-speed and high-efficiency motors, while ABB has expanded its U.S. footprint with new manufacturing and service facilities to support industrial electrification. The growing adoption of smart motor solutions, predictive maintenance platforms, and energy-efficient retrofits across sectors such as oil & gas, water treatment, and logistics is contributing to sustained long-term growth and higher aftermarket revenues.

Europe Electric Motor Market Trends - Energy Efficiency Mandates & Decarbonization-Led Motor Upgrades

Europe’s electric motor market is defined by stringent energy-efficiency regulations, decarbonization targets, and a strong focus on industrial sustainability. Countries such as Germany, the U.K., France, and Spain are leading adopters of advanced motor technologies, supported by regulatory frameworks mandating high-efficiency standards. The European Union’s Ecodesign Directive has accelerated the transition toward IE3 and IE4 motors, driving replacement demand across industrial and commercial sectors. This harmonization of standards reduces compliance complexity and enables manufacturers to scale operations across multiple countries.

Corporate developments are reinforcing regional growth dynamics. Siemens continues to invest in digitalized motor and drive systems integrated with industrial automation platforms, enhancing efficiency in manufacturing environments. Similarly, WEG has expanded its production capacity in Europe to improve supply chain responsiveness and reduce delivery timelines for regional customers. Investments in renewable energy projects, such as wind and hydrogen infrastructure, are also increasing demand for high-capacity and medium-voltage motors. Europe’s emphasis on carbon neutrality and energy savings continues to create a favorable environment for advanced motor adoption and technological innovation.

Asia Pacific Electric Motor Market Trends-Manufacturing Scale & EV Ecosystem-Driven Motor Expansion

Asia Pacific is projected to dominate the global market, accounting for an anticipated 42.4% share in 2026, supported by large-scale manufacturing, rapid industrialization, and strong demand from automotive and infrastructure sectors. China leads in both production and consumption, driven by its extensive EV manufacturing ecosystem and government-backed electrification initiatives. Major domestic players such as Nidec and Mitsubishi Electric are expanding production capacities and investing in high-efficiency and EV-specific motor technologies to meet growing demand.

Japan remains a leader in precision motor engineering, particularly in robotics and automation, while India is emerging as a high-growth market due to infrastructure expansion, increasing electrification, and government initiatives such as “Make in India.” Companies such as Tata Motors are accelerating EV adoption, driving demand for traction motors and related components. The region benefits from cost-effective manufacturing, integrated supply chains, and proximity to major OEMs, enabling faster production cycles and competitive pricing. Recent investments in manufacturing facilities, including capacity expansions by global and regional motor manufacturers, are further strengthening the region’s leadership. ASEAN countries are witnessing rising adoption of industrial automation and electrified transport systems, contributing to incremental growth. Overall, Asia Pacific’s combination of scale, policy support, and industrial capability continues to position it as the primary growth engine for the global electric motor market.

Competitive Landscape

The global electric motor market is moderately consolidated at the top, with major multinational companies holding significant shares in high-value segments. However, the market remains fragmented overall, with numerous regional and niche players serving specific applications. Leading companies benefit from economies of scale, global distribution networks, and strong R&D capabilities. Competitive intensity is highest in low-voltage and standard motor segments, while specialized segments such as EV motors and high-efficiency systems exhibit higher entry barriers. Key strategies include innovation in high-efficiency motor technologies, expansion of regional manufacturing capabilities, and integration of digital services. Companies are focusing on offering complete solutions that combine motors, drives, and analytics to enhance customer value and ensure long-term revenue growth.

Key Industry Developments:

- In November 2025, Nidec inaugurated a new manufacturing hub in India (Hubli, Karnataka) as part of its global expansion strategy, aimed at increasing production capacity and strengthening its supply chain to meet rising demand for automotive and industrial electric motors.

- In September 2025, ABB announced the launch of its IE5 ultra-premium efficiency motor range in India, alongside an investment of over INR 140 crore (US$15.0 million) to expand its low-voltage motor manufacturing facility, aiming to reduce energy losses by up to 40% and strengthen its position in high-efficiency industrial motor solutions.

Companies Covered in Electric Motor Market

- Nidec

- ABB

- Siemens

- WEG

- Mitsubishi Electric

- Regal Rexnord

- Rockwell Automation

- Toshiba

- Johnson Electric

- Franklin Electric

- Brook Crompton

- Baldor Electric Company

- TECO Electric & Machinery

- Hitachi

- Hyosung Heavy Industries

- CG Power and Industrial Solutions

Frequently Asked Questions

The global electric motor market size is estimated to be US$115.2 billion in 2026.

The electric motor market is projected to reach US$198.7 billion by 2033.

Key trends include increasing electrification of transportation (EV powertrains), rising adoption of energy-efficient motors (IE3-IE5), growing integration of smart and connected motor systems, and expansion of industrial automation and digital manufacturing.

The Low Voltage segment (up to 1 kV) is the leading segment, accounting for approximately 43.3% of the market share, driven by its widespread use across industrial machinery, HVAC systems, and household applications.

The electric motor market is expected to grow at a CAGR of 8.1% from 2026 to 2033.

Major companies with strong product portfolios include Nidec, ABB, Siemens, WEG, and Mitsubishi Electric.