- Technology

- Commercial Vehicle Financing Market

Commercial Vehicle Financing Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Commercial Vehicle Financing Market by Provider Type (Banks, Captive Finance Arms (OEM-linked financiers), Non-Banking Financial Companies (NBFCs), Credit Unions & Other Financial Institutions), Financing Type (Loans (Term Loans / Hire Purchase), Finance Lease, Operating Lease, Line of Credit / Revolving Credit), Vehicle Condition (New Commercial Vehicles, Used Commercial Vehicles), Vehicle Type (Light Commercial Vehicles, Medium Commercial Vehicles, Heavy Commercial Vehicles, Special-Purpose Vehicles), and Region Analysis for 2026 - 2033

Commercial Vehicle Financing Market Trend Analysis

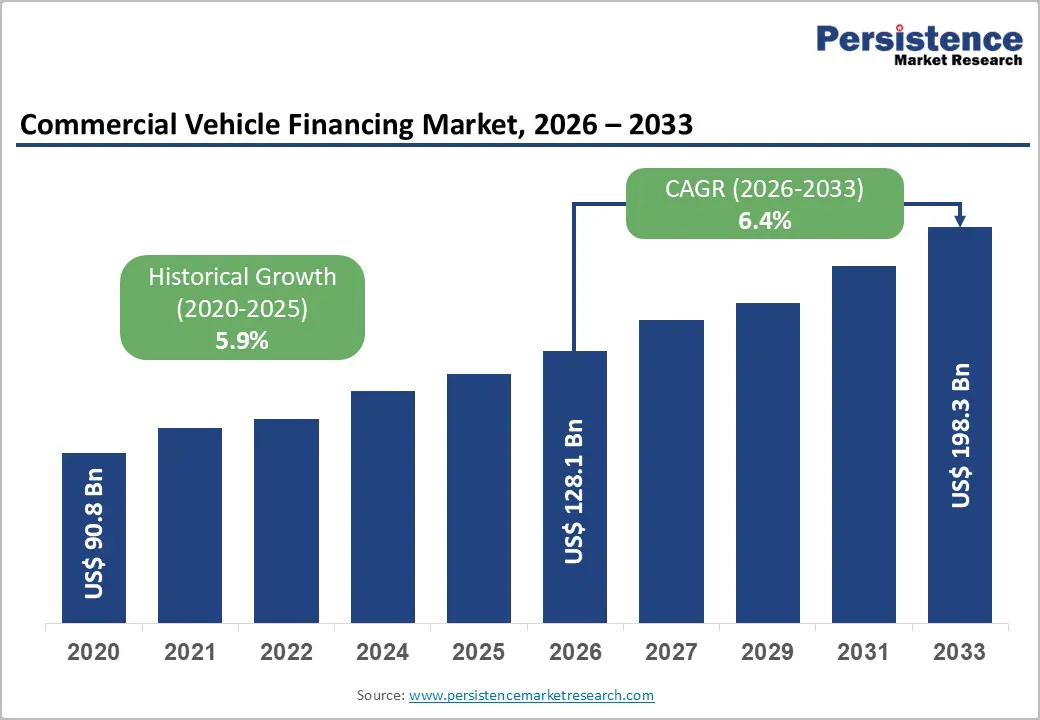

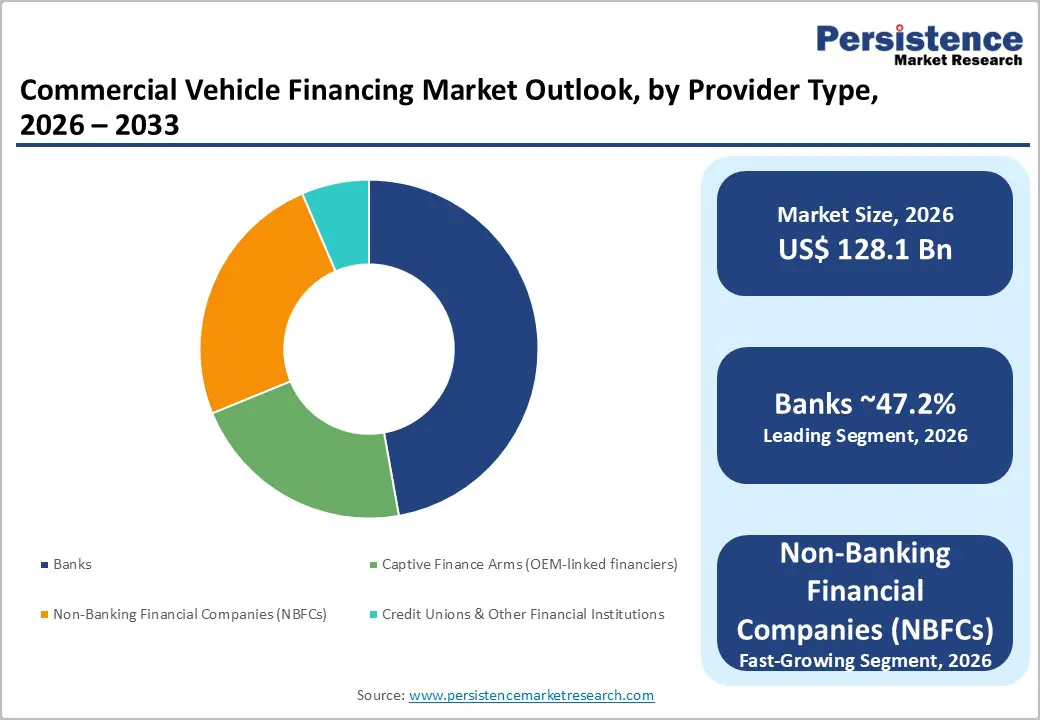

The global commercial vehicle financing market size is projected at US$ 128.1 billion in 2026 and is projected to reach US$ 198.3 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033.

Accelerating e-commerce logistics infrastructure, financing requirements for fleet electrification, and NBFC-led credit expansion into underserved owner-operator segments are the primary growth catalysts. Digital lending platforms are compressing loan approval timelines from weeks to hours, structurally lowering origination friction. Emerging market freight demand growth, particularly across India and Southeast Asia, is expanding the addressable financing base significantly through 2033.

Key Industry Highlights:

- Leading Provider Type: Banks lead provider type at 47.2% share; NBFCs grow fastest at 8.0% CAGR, driven by GPS-enabled credit scoring and digital lending penetration into informal owner-operator segments.

- Dominant Financing Type: Loans/hire purchase leads financing type at 64.5% share; Operating Lease grows fastest at 8.4% CAGR, driven by EV residual value risk management and ESG fleet optimization imperatives.

- Top Vehicle Type: LCVs lead vehicle type at 45.6% share; Heavy Commercial Vehicles grow fastest at 6.6% CAGR, driven by EV Class 8 truck financing programs with 2-3x higher unit values.

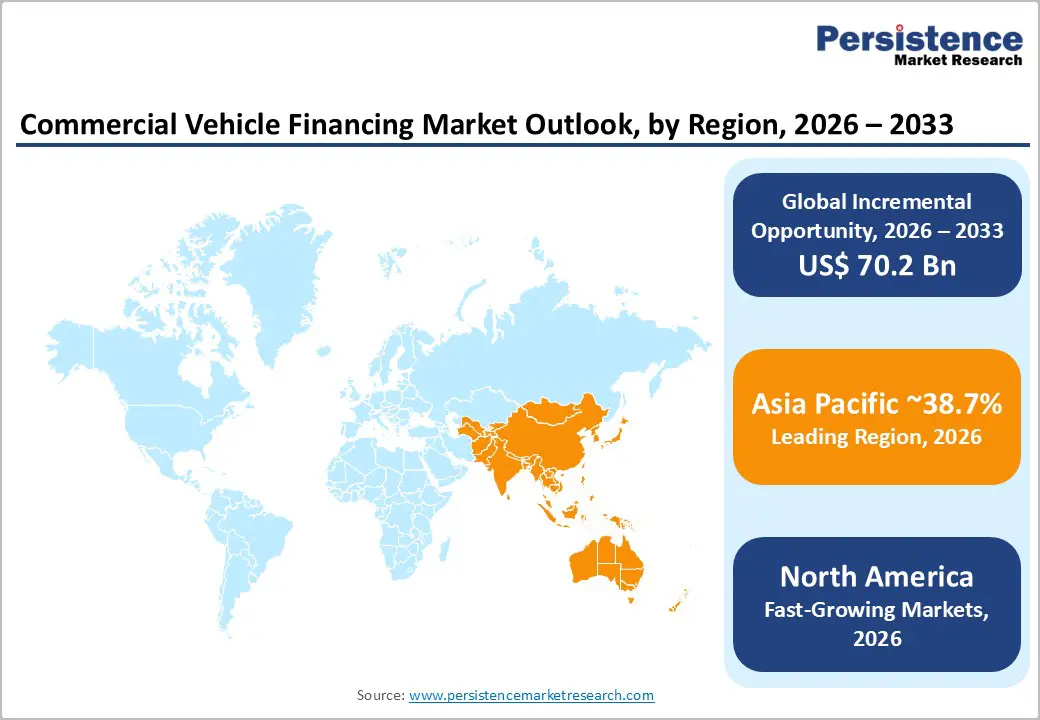

- Regional Performance: Asia Pacific dominates at 38.7% share; China's market is US$ 21.8 Bn and India's market is US$ 12.9 Bn in 2026; North America grows at 6.1% CAGR with the U.S. at US$ 30.8 Bn.

- Strategic Developments: Volvo Financial Services' EV lease program (September 2025) and PACCAR Financial's expansion of electric truck financing are reshaping the competitive dynamics of fleet electrification financing.

Market Dynamics Analysis

Drivers - E-Commerce Expansion and Freight Logistics Investment Driving Fleet Demand

The exponential growth of e-commerce is generating elevated demand for last-mile and long-haul commercial vehicle fleets, directly expanding the commercial vehicle financing addressable market. Global e-commerce sales exceeded US$ 5.8 trillion in 2023 (UNCTAD) and are projected to surpass US$ 8 trillion by 2027, requiring logistics operators to finance rather than purchase outright fleet expansion investments to preserve capital. The U.S. Bureau of Transportation Statistics recorded commercial truck freight volumes growing at 3.2% annually through 2025, sustaining replacement and expansion financing demand across U.S. fleet operators.

India's PM Gati Shakti National Master Plan, targeting US$ 1.3 trillion in infrastructure investment through 2025, and China's Belt and Road-linked freight corridor investments are driving large-scale commercial vehicle procurement programs that require institutional financing support. In Southeast Asia, ASEAN freight logistics investment is projected to grow at 8% annually through 2030 (Asian Development Bank), generating structured financing demand for light and medium commercial vehicle fleets across Vietnam, Indonesia, and Thailand. These macroeconomic infrastructure and trade investment drivers sustain multi-year commercial vehicle procurement pipelines, directly translating into financing origination volume growth.

Fleet Electrification Programs and Government EV Commercial Vehicle Incentives

Government-mandated fleet decarbonization programs and EV commercial vehicle adoption incentives are generating a new wave of financing demand specifically structured around higher-unit-value electric trucks, buses, and vans. The U.S. EPA's 2024 Heavy-Duty Vehicle Emissions Standards, which phase out diesel trucks by 2032, require fleet operators to initiate transition financing programs for electric replacements. Because the average Class 8 electric truck is priced 2-3 times higher than diesel equivalents, this significantly elevates per-unit financing costs. The U.S. Inflation Reduction Act's Section 45W commercial clean vehicle tax credits of up to US$ 40,000 per vehicle are enhancing EV financing economics for fleet operators.

In Europe, the EU's CO2 Standards for Heavy-Duty Vehicles regulation mandates a 90% reduction in emissions for new trucks by 2040, driving OEM captive finance arms, Daimler Truck Financial Services, Volvo Financial Services, and PACCAR Financial, to develop dedicated EV fleet financing programs with tailored residual value guarantees and battery performance warranties. India's FAME II scheme and PM E-Bus Sewa program, allocating INR 57,613 crore for electric bus procurement, are driving specialized public-sector commercial vehicle financing programs, expanding the addressable financing base beyond private-sector fleet operators into government-backed institutional procurement channels.

Restraints - Basel IV Capital Requirements Constraining Bank Commercial Vehicle Lending

European and globally active banks face significantly elevated capital reserve requirements under Basel IV, which will take effect from January 2025, with transport loan risk weights increasing materially for commercial vehicle portfolios. NatWest and European peer institutions reported measurable declines in new CV financing originations during the first half of 2025 following Basel IV implementation, as capital cost premiums rendered bank CV lending economically marginal against competing asset classes.

A PwC analysis identified a substantial capital shortfall across bank CV financing portfolios, prompting institutional decisions to securitize loan books or exit the asset class, structurally shifting market share toward NBFCs and captive finance arms offering more competitive pricing without equivalent regulatory capital burdens.

Asset Quality Deterioration Risk in Used Commercial Vehicle Financing

The rapid growth of used commercial vehicle financing, driven by NBFC penetration into informal owner-operator segments, introduces elevated credit risk exposure from borrowers with limited formal financial documentation, irregular income streams, and insufficient collateral beyond vehicle asset hypothecation. ICRA's 2026 analysis identified pre-owned asset NPAs trending higher across NBFC portfolios, with used-vehicle loan delinquency rates running 1.5-2.0x higher than those for new-vehicle equivalents in India.

As the used-vehicle financing share in NBFC portfolios grows to 41% by March 2027 (ICRA), managing asset quality deterioration through GPS-enabled credit monitoring and telematics-based early warning systems becomes a structural operational imperative for portfolio health.

Opportunities - Digital Lending Platforms and Fintech-Enabled Credit Scoring for Informal Operators

Approximately 60-70% of commercial vehicle ownership in Asia Pacific, particularly in India, Indonesia, and Vietnam, is held by informal single-owner or small-fleet operators who lack the audited financial documentation required by conventional bank credit assessment frameworks. Fintech-enabled digital lending platforms that integrate mobile money transaction data, fuel card purchase histories, GPS-tracked vehicle utilization metrics, and GST filing records are enabling NBFCs and digital lenders to underwrite previously unbankable owner-operators with credit accuracy comparable to traditional documentation-based approaches.

Mahindra Finance's GPS-enabled credit scoring program, which significantly expanded its commercial vehicle book in fiscal 2025, and Shriram Finance's mobile-first origination platform exemplify the commercial scale this opportunity has reached. The addressable market of informal commercial vehicle operators currently underserved by traditional financing channels is estimated at 15-20 million owner-operators across Asia Pacific alone, representing a US$ 25-35 Bn incremental financing addressable market for digitally enabled NBFC and fintech entrants that can deploy scalable, data-driven underwriting at the required volume and speed.

Operating Lease and Mobility-as-a-Service Financing Models

The structural shift from vehicle ownership to fleet-as-a-service operational models, driven by logistics companies seeking capital efficiency, EV residual value uncertainty, and asset utilization optimization, is creating significant growth opportunities for operating lease financing structures that retain vehicle ownership with the financier while delivering monthly usage-based payments to fleet operators. Volvo Financial Services' September 2025 European electric truck lease program, offering lower down payments and extended repayment terms, demonstrates OEM captive arms' active investment in this structural shift.

Operating leases reduce fleet operator balance sheet leverage and provide access to the latest commercial vehicle technology without long-term capital commitment, particularly compelling for EV fleet transition, where technology evolution risk and residual value uncertainty make outright purchase financially unattractive. The operating lease segment is the fastest-growing financing type, with a 8.4% CAGR through 2033, and an estimated addressable pool of US$ 18-22 Bn annually in Europe and North America as logistics operators progressively migrate from ownership to service-based fleet procurement models aligned with ESG reporting frameworks.

Category-wise Analysis

Provider Type Insights

Banks lead the provider type segment with a 47.2% share in 2026. Their dominance reflects institutional advantages in deposit-funded lending capacity, established corporate banking relationships with large fleet operators, and regulatory trust credentials that facilitate multi-million-dollar fleet financing mandates. Banks maintain deep integration with OEM dealer networks and offer bundled treasury and trade finance services alongside vehicle financing that smaller NBFCs cannot replicate.

However, Basel IV capital requirement increases are structurally compressing bank CV lending profitability in Europe and North America, creating a progressive market share migration toward NBFCs and captive finance arms that benefit from regulatory arbitrage and superior pricing flexibility for owner-operator and SME fleet segments.

NBFCs are the fastest-growing provider type. Their competitive advantages in serving informal and semi-formal operators through mobile-first digital underwriting, GPS-enabled credit scoring, and flexible repayment structures, particularly across India, Southeast Asia, and Sub-Saharan Africa, are driving accelerating market share expansion.

Financing Type Insights

Loans (Term Loans / Hire Purchase) lead the financing type segment with a dominant 64.5% market share in 2026. Term loans and hire purchase structures remain the foundational commercial vehicle financing instrument globally, offering straightforward ownership transfer, tax depreciation benefits for corporate fleet buyers, and familiarity across borrower segments from large corporations to individual owner-operators. Hire purchase structures, enabling vehicle title transfer upon final installment, align with the strong asset ownership preferences of commercial vehicle operators in the Asia Pacific and emerging markets. Finance Lease and Operating Lease serve distinct financial reporting and fleet management optimization needs, while Line of Credit products serve working capital-linked fleet financing for larger logistics enterprises. Loan dominance is expected to remain structurally intact through 2033.

Operating Lease is the fastest-growing financing type. Fleet electrification transition uncertainty, EV residual value risk management, and ESG balance sheet optimization requirements are systematically driving logistics operators toward operating lease structures.

Vehicle Condition Insights

New commercial vehicles lead the vehicle condition segment with a 57.7% share in 2026. New vehicle financing commands premium loan values, reflecting higher unit prices across electric trucks, advanced telematics-equipped trucks, and Euro VI/BS VI emission-compliant models, and benefits from OEM captive finance arm channel integration that provides point-of-sale financing access directly at dealerships. New vehicle financiers benefit from lower default risk profiles, established residual value benchmarks, and OEM warranty-backed collateral security.

While used commercial vehicle financing is growing rapidly through NBFC-led penetration, new vehicle financing retains revenue leadership due to higher per-unit financing values and the ongoing fleet modernization and electrification replacement cycle.

Used commercial vehicles are the fastest-growing vehicle condition segment at 8.0% CAGR through 2033. NBFC digital lending expansion into owner-operator segments, ICRA-documented pre-owned asset financing growth toward 41% of NBFC portfolios by March 2027, and organized used vehicle markets in India and China are driving accelerating penetration.

Vehicle Type Insights

Light commercial vehicles (LCVs) lead the vehicle type segment with a 45.6% share in 2026. LCVs dominate by volume across last-mile delivery, micro-distribution, and intra-city logistics applications, segments experiencing structural growth from e-commerce expansion and urban freight demand. Their lower unit values broaden the eligible borrower pool to include individual owner-operators and micro-enterprises, enabling NBFCs and digital lenders to deploy high-volume, lower-ticket financing portfolios at scale.

LCV financing dominance is reinforced by the exponential growth of quick-commerce and food-delivery logistics platforms worldwide. While heavy commercial vehicles command higher per-unit financing values, LCV volume-driven revenue base ensures segment leadership through 2033.

Heavy commercial vehicles are the fastest-growing vehicle type, with a CAGR of 6.6% over the forecast period. Infrastructure construction demand, highway freight growth, and financing programs for fleet electrification of Class 8 trucks, with per-unit EV values 2-3x higher than diesel equivalents, are the primary drivers of acceleration.

Regional Insights

North America Commercial Vehicle Financing Market Insights

North America holds a considerable share of the global commercial vehicle financing Market, expected to achieve a 6.1% CAGR through 2033, with the U.S. market estimated at ~US$ 30.8 Bn, anchored by its mature financing ecosystem, world-class logistics infrastructure, and fleet electrification transition imperative.

U.S. Commercial Vehicle Financing Market

The U.S. EPA's 2024 Heavy-Duty Vehicle Emissions Standards and IRA Section 45W clean vehicle tax credits, offering up to US$ 40,000 per commercial EV, are driving a new electrification-linked financing cycle that elevates per-unit loan values significantly. Wells Fargo Equipment Finance, PACCAR Financial, and Daimler Truck Financial Services anchor the competitive landscape, with digital fintech entrants disrupting SME fleet origination. Canada contributes meaningful fleet financing demand from its resource extraction and cross-border logistics sectors. North America's growth is driven by e-commerce logistics fleet expansion, EV transition financing programs, and infrastructure investment-driven heavy truck procurement across highway freight corridors.

Europe Commercial Vehicle Financing Market Insights

Europe holds a 19.4% share of the global commercial vehicle financing market in 2025, anchored by the EU's CO2 heavy-duty vehicle standards, ESG-linked fleet lending mandates, and regulatory harmonization creating premium financing demand across electrified commercial fleets.

Germany Commercial Vehicle Financing Market: Regulation

Germany accounts for approximately US$ 6.1 Bn, underpinned by its position as Europe's largest commercial vehicle market with OEM headquarters of Daimler Truck, MAN, and Volkswagen Commercial Vehicles directly driving captive finance arm origination volumes. The EU CO2 regulation mandating 90% truck emissions reduction by 2040, combined with Basel IV capital requirements reshaping bank CV lending economics, is accelerating the shift toward OEM captive and NBFC financing alternatives.

France, Spain, and the U.K. contribute commercial fleet financing demand across logistics, construction, and municipal transport sectors. Europe's growth is anchored by EV fleet financing program expansion from Volvo Financial Services and Mercedes-Benz Financial, ESG lending mandates, and cross-border fleet financing harmonization frameworks.

Asia Pacific Commercial Vehicle Financing Market Insights

Asia Pacific commands the dominant 38.7% share of the global Commercial Vehicle Financing Market in 2025 and is the fastest-growing region, driven by the world's largest commercial vehicle production and sales volumes, expanding freight infrastructure, and rapidly scaling NBFC digital lending ecosystems.

China & India Commercial Vehicle Financing Market

China is the single largest national market, estimated at US$ 21.8 billion in 2026, anchored by its freight corridor infrastructure investments, 30+ million annual commercial vehicle parc, and NBFC-equivalent financing institution growth. India, estimated at US$ 12.9 billion, is growing at 12.5% CAGR through 2033, driven by PM Gati Shakti infrastructure investment, NBFC penetration into owner-operator segments, and FAME II EV bus procurement financing. Japan contributes high-value precision fleet financing through Mitsubishi UFJ and Sumitomo Mitsui captive programs, while ASEAN markets grow rapidly through digital lending platforms.

Asia Pacific's manufacturing scale advantages, government infrastructure financing programs, and expanding NBFC ecosystems make it the most strategically critical commercial vehicle financing growth region through 2033.

Competitive Landscape

The global commercial vehicle financing market is moderately fragmented, with leading institutions, Wells Fargo, Toyota Financial Services, Volkswagen Financial Services, Daimler Truck Financial, and Shriram Finance, collectively accounting for approximately 25-30% of global origination volume in 2025. Regional banks, OEM captive arms, and domestic NBFCs hold significant local share. Market leaders differentiate through integrated dealer-point financing, EV-specific lease programs, and AI-driven credit risk analytics platforms.

Technology innovation in digital underwriting, GPS-linked credit scoring, and EV residual value analytics, geographic expansion into Asia Pacific NBFC ecosystems, and operating lease product development for fleet electrification transitions define the dominant competitive strategy themes shaping the global commercial vehicle financing landscape through 2033.

Strategic Developments:

- In September 2025, Volvo Financial Services launched a dedicated electric truck lease program in Europe, offering lower down payments and extended repayment terms to accelerate fleet electrification for logistics operators, supporting EU CO2 compliance while expanding operating lease market share.

- In March 2024, Shriram Finance Limited reported strong growth in its commercial vehicle loan portfolio, driven primarily by rising demand for used commercial vehicles, supported by higher new vehicle prices following emission-related regulatory changes, which accelerated financing demand among cost-sensitive fleet operators.

- In June 2024, PACCAR Financial Corp expanded its EV commercial vehicle financing program across North America for Kenworth and Peterbilt electric truck customers, integrating battery performance warranty-linked residual value guarantees that reduce lender risk in electric fleet financing originations.

Commercial Vehicle Financing Market - Key Insights & Scope

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 90.8 Bn |

| Current Market Value (2026) | US$ 128.1 Bn |

| Projected Market Value (2033) | US$ 198.3 Bn |

| CAGR (2026 - 2033) | 6.4% |

| Leading Region | Asia Pacific |

| Dominant Provider Type | Banks - 47.2% Share |

| Top-ranking Financing Type | Loans / Term Loans / Hire Purchase - 64.5% Share |

| Incremental Opportunity | US$ 70.2 Bn |

Companies Covered in Commercial Vehicle Financing Market

- Volkswagen Financial Services AG

- Toyota Financial Services Corporation

- Daimler Truck Financial Services

- Wells Fargo Equipment Finance

- Volvo Financial Services

- PACCAR Financial Corp

- Shriram Finance Limited

- Mahindra Financial Services

- JPMorgan Chase & Co.

- BNP Paribas Leasing Solutions

- HSBC Holdings plc

- Sumitomo Mitsui Banking Corporation

- Mitsubishi UFJ Financial Group

- Deutsche Bank AG

- Tata Motors Finance

Frequently Asked Questions

The commercial vehicle financing market is valued at US$ 128.1 Bn in 2026, projected to reach US$ 198.3 Bn by 2033.

E-commerce logistics fleet expansion, fleet electrification financing programs, and NBFC digital lending penetration into underserved informal owner-operator segments are the primary growth drivers.

The market is projected to grow at a CAGR of 6.44% from 2026 to 2033.

Fintech-enabled digital NBFC lending to informal operators and operating lease model adoption for EV fleet electrification transitions represent the most strategically actionable near-term opportunities.

Volkswagen Financial Services, Toyota Financial Services, Daimler Truck Financial, Wells Fargo, Volvo Financial Services, Shriram Finance, Mahindra Finance, PACCAR Financial, and JPMorgan Chase are the leading global participants.