- Hardware & Software IT Services

- ESG Reporting Software Market

ESG Reporting Software Market Size, Share, and Growth Forecast, 2026 - 2033

ESG Reporting Software market by Organisation Size (Small & Medium Enterprises (SMEs), Large Enterprises), Deployment Mode (On-Premise, Cloud-Based, and Hybrid Deployment.), Industry (Banking, Financial Services & Insurance (BFSI), IT & Telecom, Manufacturing, Energy & Utilities, Healthcare & Life Sciences, Retail & Consumer Goods, Government & Public Sector, Transportation & Logistics, Real Estate & Construction, Misc.), and Regional Analysis for 2026 - 2033

ESG Reporting Software Market Size and Trends Analysis

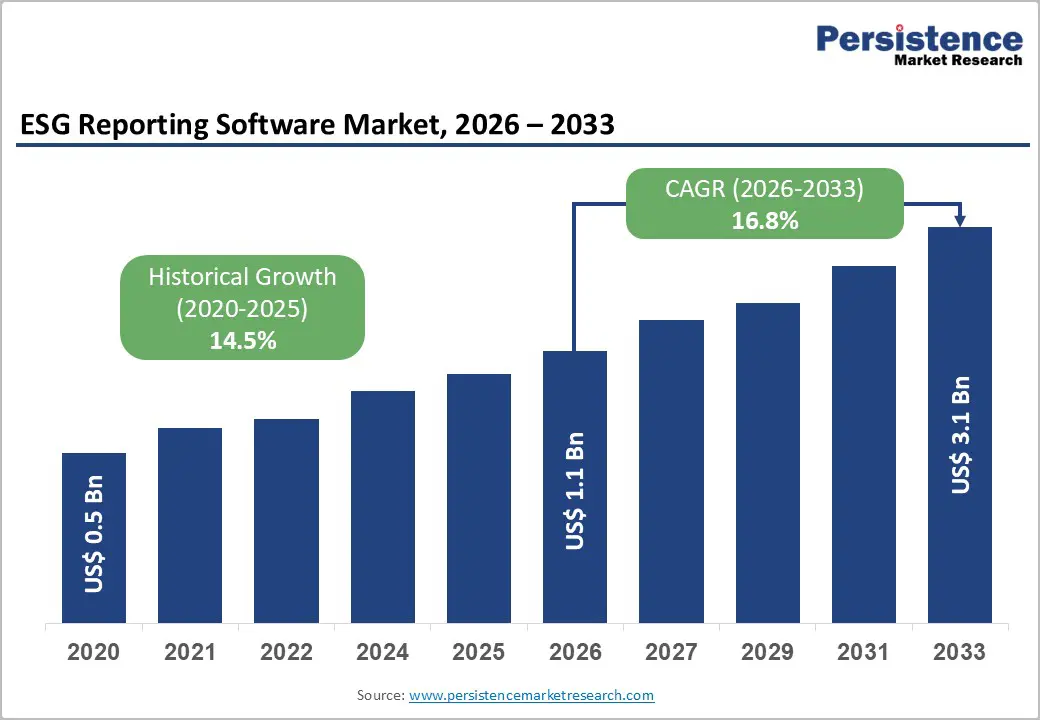

The global ESG reporting software market size is likely to be valued at US$ 1.1 billion in 2026 and is projected to reach US$ 3.1 billion by 2033, growing at a CAGR of 16.8% between 2026 and 2033. This substantial market expansion reflects organisations' urgent requirement to address the rise in regulatory mandates, including the EU Corporate Sustainability Reporting Directive (CSRD), ISSB standards, and emerging disclosure frameworks across geographies.

Market growth is fundamentally driven by mandatory environmental, social, and governance reporting requirements, particularly in the financial services and manufacturing sectors undergoing digital infrastructure transformation. Financial services firms operating under tightened capital requirements and manufacturing companies facing decarbonization mandates represent primary market expansion drivers, collectively representing over 50% of the ESG reporting software market demand through 2026.

Key Industry Highlights:

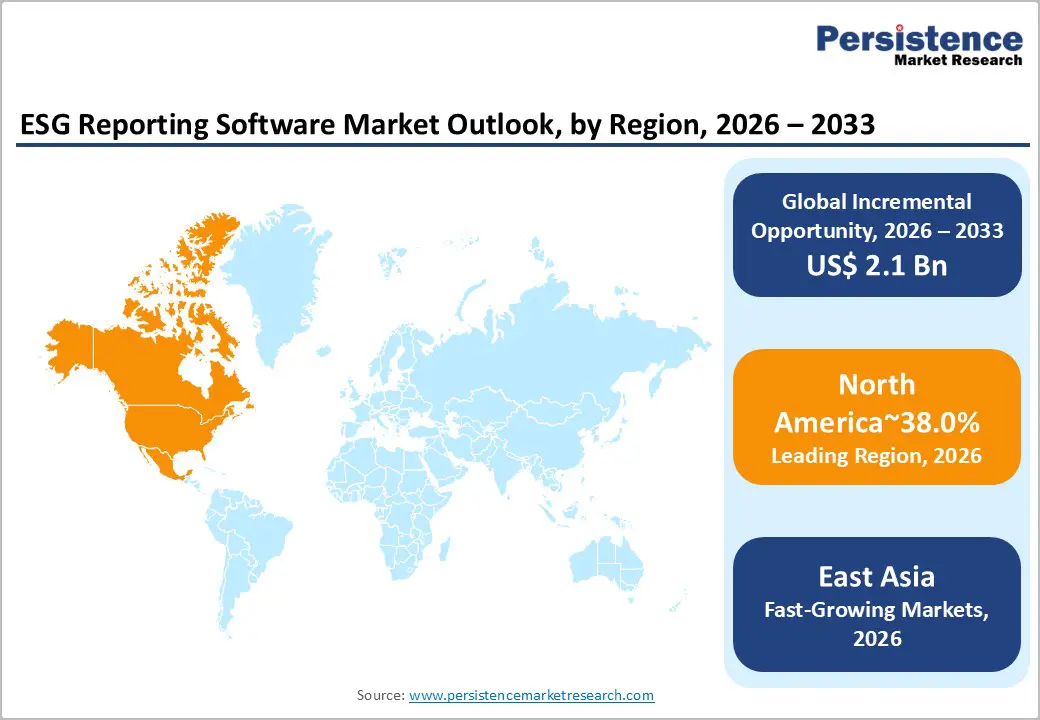

- Regional Leadership: North America leads the global ESG reporting software market with ~38% share through 2026, driven by mature financial markets, large-scale manufacturing activity, and rising ESG disclosure pressure from investors and regulators.

- Regulatory-Driven Region: Europe accounts for ~30% market share, underpinned by CSRD and ESRS mandates requiring nearly 49,000 organisations to deploy auditable ESG reporting infrastructure from 2025–2026.

- Fastest-Growing Region: East Asia captures ~18% market share and represents the fastest-growing region, supported by China’s expanding ESG regulations, Japan’s mature disclosure practices, and South Korea’s sustainability-focused technology ecosystem.

- Leading Deployment: Cloud-based ESG Reporting Software dominates with ~61% market share, favoured for scalability, rapid compliance readiness, automatic regulatory updates, and lower IT ownership costs.

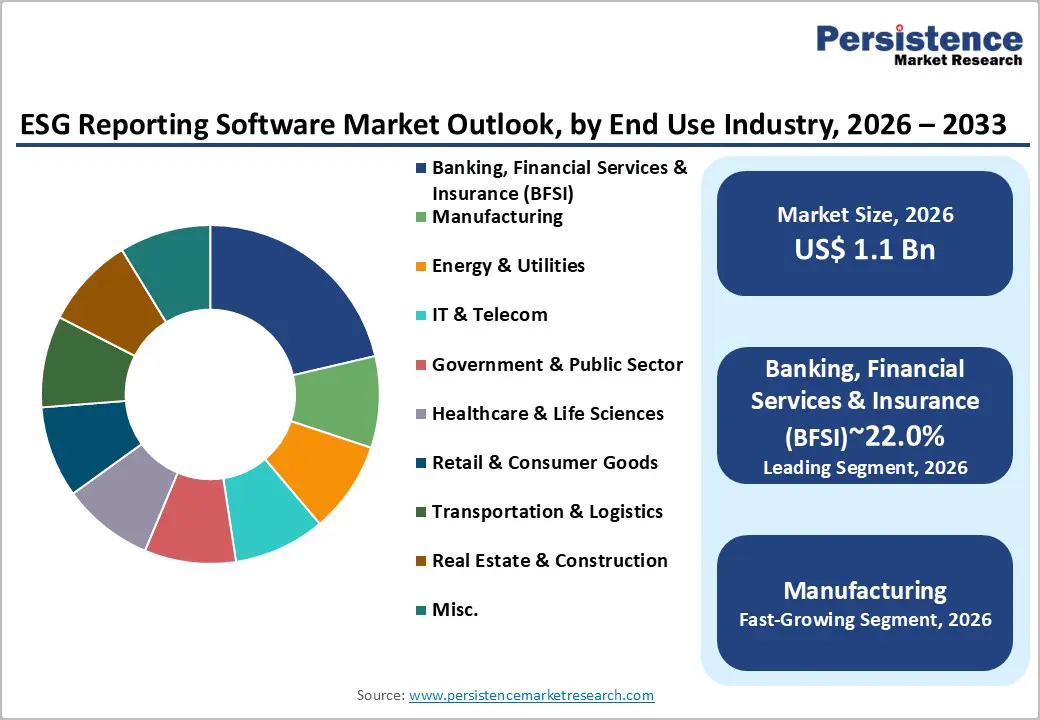

- Dominant Industry: Banking, Financial Services & Insurance (BFSI) leads with ~22% share, driven by ESG integration into capital adequacy, climate risk analytics, and regulatory reporting obligations.

- Fastest-Growing Industry: Manufacturing is the fastest-growing segment, fueled by decarbonization mandates, Scope 1–3 emissions tracking, CSRD compliance, and supply chain sustainability requirements.

- Notable Developments & Opportunity: AI-enabled ESG platforms and integrated ESG–financial planning solutions, such as CSRD-focused automation and emissions tracking, are accelerating adoption across manufacturing and energy transition use cases.

| Key Insights | Details |

|---|---|

|

ESG Reporting Software Market Size (2026E) |

US$ 1.1 Bn |

|

Market Value Forecast (2033F) |

US$ 3.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

16.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

14.5% |

Market Dynamics

Drivers - Regulatory Compliance Expansion and Mandatory Sustainability Reporting Requirements

Global regulatory frameworks have undergone unprecedented expansion, mandating that organisations across all sectors collect, validate, and disclose comprehensive environmental, social, and governance metrics aligned with standardised reporting frameworks, including the CSRD, ESRS, ISSB, and emerging national sustainability requirements. The regulatory expansion represents a structural shift from voluntary sustainability reporting toward mandatory, auditable, and material ESG disclosure requirements that directly impact organisational financial performance, stakeholder valuation, and regulatory compliance obligations. The ESG Reporting Software Market directly addresses this regulatory imperative through platforms automating data collection, consolidating reporting workflows, and facilitating compliance validation across multiple global frameworks.

The European Union's CSRD implementation represents the most consequential regulatory driver, mandating approximately 49,000 organisations across 27 member states to report sustainability data beginning in 2025-2026. Germany, France, Italy, Spain, and Poland, collectively representing over 65% of the EU financial and insurance sector value added and employment, will implement CSRD compliance, requiring a systematic transformation of ESG data infrastructure across thousands of financial institutions and manufacturing enterprises.

This regulatory mandate directly correlates to substantial ESG Reporting Software Market demand as organisations implement technology infrastructure enabling data collection, KPI calculation, and report generation aligned with ESRS (European Sustainability Reporting Standards) specifications. On June 30, 2025, PwC Germany and SAP launched CSRD.AI Manager, an AI-powered ESG reporting solution designed to automate data collection and KPI calculation, directly addressing organisational compliance requirements while reducing manual effort and improving reporting accuracy.

The market impact extends beyond Europe through ISSB (International Sustainability Standards Board) framework adoption, which is gaining regulatory traction in North America, Asia-Pacific, and emerging markets. Organisations implementing ISSB-aligned reporting face substantial technology infrastructure requirements that ESG Reporting Software platforms address through framework-agnostic solutions supporting multiple reporting standards simultaneously. The regulatory compliance driver is expected to sustain the ESG Reporting Software Market demand throughout the forecast period as regulatory frameworks continue evolving and the mandatory reporting scope expands beyond financial services toward all economic sectors.

Financial Services Sector Digitalisation and ESG Integration with Capital Requirements

The financial services sector globally is undergoing a profound digital transformation driven by capital adequacy requirements, stakeholder pressure, and competitive necessity to integrate environmental and social risk factors into lending, investment, and risk management decisions. India's banking, financial services, and insurance sector exemplifies this transformation momentum, having expanded 50-fold in market capitalisation to reach Rs. 91 lakh crore (US$ 1 trillion) in 2025 from Rs. 1.8 lakh crore in 2005, now contributing 27% to GDP. This financial sector expansion reflects digital transformation and ESG integration becoming central to strategic positioning, as banks and financial institutions require modern infrastructure supporting real-time ESG data integration, risk analytics, and regulatory reporting that legacy systems cannot deliver.

The European Union's financial and insurance activities sector generated €0.9 trillion in value added in 2022, employing nearly 5 million people across 867,000 enterprises, with productivity levels reflecting substantial technology investment capacity. European banking sector assets totalled €43.6 trillion in 2023, with organizational restructuring reducing credit institutions by 2.9% as institutions consolidate operations and implement digitalization-driven efficiency improvements that ESG data infrastructure facilitates.

The ESG Reporting Software Market captures financial services demand through specialised solutions incorporating regulatory reporting, climate risk quantification, and stakeholder disclosure capabilities essential for modern financial institutions. Nasdaq's recognition as Leader in 2025 Verdantix Green Quadrant for ESG & Sustainability Reporting Software underscores vendor innovation in supporting financial institution requirements, with Nasdaq Metrio™ and Sustainable Lens® platforms enabling disclosure quality enhancement and peer benchmarking.

Restraint - Implementation Complexity and Multi-Framework Integration Challenges

Despite regulatory mandates driving ESG reporting adoption, organisations face substantial implementation complexity arising from heterogeneous data sources, multiple reporting standards (CSRD, ESRS, ISSB, SEC climate disclosure rules, sectoral frameworks), and organisational systems integration requirements that delay platform deployment and increase total cost of ownership.

Organisations must consolidate data from disparate enterprise systems (financial management, procurement, facility operations, HR analytics), validate data quality against reporting standards, and implement governance workflows ensuring accuracy and auditability requirements exceeding purely technical software deployment. Integration complexity is particularly acute for multinational organisations operating across jurisdictions with divergent reporting requirements, necessitating platform architecture supporting regulatory fragmentation while maintaining consolidated reporting efficiency. These implementation barriers extend deployment timelines from months to years for large enterprises, limiting annual software deployment rates and constraining ESG Reporting Software Market growth velocity.

Opportunity - Manufacturing Sector Decarbonization and Industrial Emissions Tracking Infrastructure Deployment

Manufacturing organisations globally are pursuing aggressive decarbonization initiatives aligned with Science Based Targets, Net Zero commitments, and emerging regulatory mandates requiring systematic emissions quantification, reduction tracking, and sustainability performance reporting across operational facilities and value chains. This decarbonization imperative creates a substantial ESG Reporting Software Market opportunity as manufacturing firms implement technology infrastructure enabling real-time emissions monitoring, energy efficiency optimisation, and supply chain sustainability assessment that legacy systems and manual processes cannot efficiently support.

EU manufacturing decarbonization requirements are particularly acute: the sector's €5,860 billion production base faces CSRD reporting mandates, EU Emissions Trading System compliance obligations, and sectoral decarbonization targets across automotive, chemical, pharmaceutical, and equipment manufacturing that collectively demand comprehensive emissions tracking infrastructure.

Germany's 26% share of EU manufacturing output creates particular regulatory leverage for ESG reporting technology adoption, with automotive companies, chemical manufacturers, and machinery producers facing combined CSRD, ETS, and sectoral decarbonization pressures requiring an integrated ESG data infrastructure. The pharmaceutical sector, with €54 billion in sold production representing nearly double its output from a decade earlier, demonstrates manufacturing segment heterogeneity, while pharmaceutical manufacturing traditionally exhibits lower carbon intensity, regulatory compliance requirements and supply chain transparency demands create a parallel ESG Reporting Software Market opportunity.

U.S. manufacturing decarbonization opportunities emerge through sectoral procurement mandates, supply chain transparency requirements, and corporate sustainability commitments, establishing minimum ESG performance expectations for supplier relationships. Manufacturing firms competing for business within large corporate procurement organisations face explicit ESG performance requirements, necessitating technology infrastructure demonstrating environmental commitment and operational sustainability maturity. The ESG Reporting Software Market captures manufacturing opportunity through specialized platforms automating emissions calculation, facility energy monitoring, supply chain ESG data collection, and sustainability performance reporting that enable manufacturers to meet customer requirements, demonstrate environmental commitment, and support decarbonization targets.

Energy Transition Infrastructure and Renewable Energy Reporting Requirements

Energy and utilities organisations globally are undergoing a profound transition from traditional fossil fuel-dependent business models toward renewable energy and decarbonization-aligned portfolios, requiring systematic infrastructure investment, performance tracking, and sustainability reporting demonstrating energy transition commitment to stakeholders, regulators, and capital markets. This energy transition creates a substantial ESG reporting software market opportunity as energy companies implement technology infrastructure supporting renewable energy asset management, decarbonization tracking, and energy transition reporting aligned with emerging frameworks and stakeholder expectations.

U.S. energy sector data reveal this transition dynamic: renewable energy production and consumption reached record highs in 2023, driven by solar and wind deployment, while coal's share of primary energy production declined from 37% in 1950 to 9% in 2023. This dramatic energy mix transformation requires substantial operational and reporting infrastructure, renewable energy assets demand real-time performance monitoring, integration with grid management systems, and sustainability reporting demonstrating generation efficiency and environmental benefits.

The EU's energy transition demonstrates parallel momentum: renewable energy production reached 46% of total primary energy production, with natural gas, nuclear, and renewables collectively dominating energy supply while fossil fuels and coal decline. EU energy import dependency creates economic and security imperatives for accelerated renewable deployment and energy efficiency improvements, requiring substantial reporting infrastructure demonstrating transition progress and environmental impact quantification.

The ESG reporting software market captures energy transition opportunity through platforms automating renewable asset performance reporting, energy transition tracking, and emissions reduction quantification that demonstrate organizational commitment to decarbonization while supporting operational optimization and stakeholder communication. OneStream's April 8, 2025, launch of the ESG Reporting & Planning solution, enabling unified collection, analysis, and reporting of Scope 1, 2, and 3 emissions while aligning ESG metrics with financial planning, directly addresses energy sector requirements for integrated ESG-financial reporting supporting energy transition strategy execution and stakeholder communication.

Category-wise Analysis

Deployment Mode Insights

Cloud-based deployment represents the dominant market category within the ESG reporting software market, commanding 61% of market value through 2026, reflecting organizations' preference for scalable, accessible, continuously updated platforms requiring minimal internal IT infrastructure and supporting remote collaboration across geographically distributed teams. Cloud deployment architecture addresses fundamental organizational requirements: rapid deployment without extended internal implementation cycles, automatic software updates incorporating emerging regulatory framework changes, and accessibility from any location supporting hybrid and distributed workforce models increasingly prevalent across enterprises globally.

Cloud-based ESG reporting software platforms enable organizations to implement a comprehensive reporting infrastructure in weeks rather than months, allowing rapid compliance with regulatory deadlines and acceleration of ESG maturity from data collection toward strategic analytics and performance optimization.

The dominance of cloud deployment reflects vendor preference for software-as-a-service models providing recurring revenue streams, enhanced customer data access supporting analytics development, and reduced customer dependency on internal IT infrastructure that constrains adoption velocity. Financial services organizations representing 22% of end-use market share particularly favor cloud deployment due to IT infrastructure standardization, vendor management efficiency, and cost predictability that cloud models provide compared to on-premises infrastructure requiring substantial capital investment and ongoing maintenance obligations.

On-premises deployment represents the fastest-growing deployment mode segment, reflecting large enterprise organizations' security and data governance requirements necessitating internal infrastructure hosting, compliance with internal IT standards, and explicit control over data residency. Organizations managing sensitive employee data, financial information, or operating within highly regulated sectors, including healthcare, government, and defense, prefer on-premises deployment, ensuring data sovereignty, regulatory compliance with data residency mandates, and explicit control over infrastructure security and data access protocols.

Industry Insights

Banking, Financial Services & Insurance represents the dominant end-use industry category within the ESG Reporting Software Market, commanding approximately 22% of market value through 2026, reflecting the sector's regulatory compliance urgency, capital market scrutiny, and integration of ESG factors into financial decision-making frameworks essential for modern financial institution competitiveness. Financial institutions face unprecedented regulatory pressure to quantify climate risk, demonstrate sustainable lending practices, and report ESG performance aligned with emerging frameworks, including CSRD, ISSB, SEC climate disclosure rules, and sector-specific sustainability standards that require systematic data infrastructure supporting compliance and stakeholder communication

India's BFSI sector expansion reaching INR. 91 lakh crore (US$ 1 trillion) in 2025 and contributing 27% to GDP demonstrates financial services sector growth and modernization, creating substantial technology infrastructure requirements supporting ESG integration with capital allocation decisions and regulatory compliance.

Manufacturing represents the fastest-growing end-use industry category within the ESG Reporting Software Market, reflecting the sector's exposure to product lifecycle environmental impact requirements, supply chain sustainability expectations, and emerging regulatory mandates including CSRD and sectoral decarbonization targets requiring comprehensive emissions quantification and sustainability reporting.

Regional Insights and Trends

North America ESG Reporting Software Market Trends

North America commands 38% of the Global ESG reporting software market through 2026, reflecting the region's mature financial markets, substantial manufacturing base, and regulatory environment increasingly mandating ESG disclosure despite the absence of comprehensive federal sustainability reporting standards. The U.S. retail e-commerce sector reaching US$ 310.3 billion in seasonally adjusted sales in Q3 2025 (growing 5.1% year-on-year) demonstrates the broader digital transformation imperative driving organizations to modernize backend infrastructure supporting reporting and analytics requirements, including ESG metrics integration.

U.S. manufacturing represents a critical North American market segment for ESG reporting software, the sector contributes $2.90 trillion with 13 million employees, 52% of private-sector R&D, and $1.6 trillion in exports in 2024, with projected growth of 3.8 million jobs by 2033. This manufacturing scale creates substantial ESG reporting demand as U.S. manufacturers compete globally, comply with international customer sustainability requirements, and pursue domestic regulatory compliance with emerging state-level climate disclosure mandates. U.S. financial services organizations face regulatory pressure from SEC climate disclosure proposals, state attorneys general sustainability inquiries, and investor activism demanding ESG performance transparency and climate risk quantification that ESG Reporting Software platforms address.

East Asia ESG Reporting Software Market Trends

East Asia captures 18% of the Global ESG reporting software market through 2026, representing the fastest-growing regional segment driven by China's regulatory expansion, Japan's mature ESG adoption practices, and South Korea's technology sector leadership in sustainability innovation. China's banking and insurance sectors demonstrate substantial ESG reporting demand: banking assets reached RMB 467.3 trillion in Q2 2025 (up 7.9% year-on-year), with large commercial banks accounting for 43.7% of total banking assets and insurance sector assets growing 9.2% to RMB 39.2 trillion. This financial sector expansion correlates with China's emerging ESG disclosure requirements, government environmental commitments, and capital market evolution, demanding a systematic ESG reporting infrastructure.

China's manufacturing sector, while specific quantitative metrics are limited by the provided data, represents the world's largest manufacturing base producing substantial ESG reporting requirements across textile, electronics, automotive, chemical, and equipment manufacturing. Government ESG initiatives, carbon neutrality commitments, and international supply chain requirements create escalating ESG reporting software demand as Chinese manufacturers implement infrastructure supporting emissions tracking and supply chain sustainability reporting.

Japan's mature ESG adoption evidenced by WuXi Biologics' recognition by the Hong Kong ESG reporting awards (HERA) 2025 for Outstanding ESG Disclosure demonstrates organizational commitment to transparent ESG reporting and governance establishing regional benchmarks for ESG disclosure practices. South Korea's technology sector leadership, government sustainability policies, and corporate governance emphasis create East Asian ESG reporting innovation dynamics. The region demonstrates rapid ESG adoption acceleration as regulatory frameworks formalise, investor expectations heighten, and technology infrastructure investment accelerates, supporting regional ESG reporting infrastructure deployment.

Europe ESG Reporting Software Market Trends

Europe represents 30% of the Global ESG Reporting Software Market through 2026, reflecting the region's regulatory leadership through CSRD implementation, comprehensive financial services ESG requirements, and manufacturing sector decarbonization mandates, creating the most consequential ESG Reporting Software Market demand globally. The European Union's CSRD mandate requires approximately 49,000 organizations across 27 member states to implement a comprehensive ESG reporting infrastructure beginning in 2025-2026, creating immediate technology deployment requirements that drive substantial market expansion.

Competitive Landscape

The Global ESG reporting software market exhibits a moderately fragmented yet gradually consolidating structure, reflecting an oligopolistic nature at the top with active niche competition. Leading players such as Workiva Inc., SAP SE, Nasdaq Inc., Diligent Corporation, Refinitiv Ltd, and Sphera Solutions Inc. dominate the landscape by offering comprehensive, enterprise-grade platforms with strong regulatory alignment and advanced analytics. These companies benefit from global reach, deep integration capabilities, and strong client bases across regulated industries.

Specialized and mid-tier vendors including Envizi Pty Ltd, Intelex Technologies Inc., Novisto Inc., Persefoni AI Inc., Benchmark Gensuite Inc., and IsoMetrix Software (Pty) Ltd enhance market diversity through focused solutions in carbon accounting, risk management, and ESG data governance. This blend of dominant leaders and specialized providers prevents full consolidation while sustaining innovation. Overall, the market is characterized by a consolidating competitive core supported by a fragmented ecosystem of agile ESG technology specialists.

Key Industry Developments:

- In April, 2025 – OneStream, Inc. launched its ESG Reporting & Planning solution, enabling unified collection, analysis, and reporting of Scope 1, 2, and 3 emissions, aligning ESG metrics with financial planning, supporting scenario modeling, and helping enterprises meet global compliance while linking sustainability efforts to business performance.

- On June 27, 2025 – Verdantix in its Green Quadrant: ESG & Sustainability Reporting Software (2025) report highlighted that ESG software vendors are shifting strategies amid regulatory uncertainty, focusing on real-time, auditable data, multi-framework reporting, and cross-functional collaboration to enhance sustainability performance and enable data-driven strategic decision-making.

Companies Covered in ESG Reporting Software Market

- Benchmark Gensuite Inc.

- Diligent Corporation

- Enablon SA

- Envizi Pty Ltd

- ESG Enterprise Inc.

- Intelex Technologies Inc.

- IsoMetrix Software (Pty) Ltd

- LogicManager Inc.

- Nasdaq Inc.

- Novisto Inc.

- Persefoni AI Inc.

- Refinitiv Ltd

- SAP SE

- Sphera Solutions Inc.

- Workiva Inc.

Frequently Asked Questions

The global ESG reporting software market is projected to be valued at US$ 1.1 Bn in 2026.

The Banking, Financial Services & Insurance (BFSI) Management segment is expected to account for approximately 22.0% of the global ESG Reporting Software market by Industry in 2026.

The market is expected to witness a CAGR of 16.8% from 2026 to 2033.

The ESG Reporting Software market is driven primarily by expanding mandatory regulatory compliance requirements (CSRD, ESRS, ISSB), accelerating ESG integration within the financial services sector, and rising sustainability and emissions accountability across manufacturing and global supply chains.

Key market opportunities in the ESG Reporting Software market include manufacturing sector decarbonization and emissions tracking infrastructure deployment, alongside energy transition and renewable energy performance reporting requirements across global energy and utilities organizations.