- Medical Devices

- Epidural Guidance Systems Market

Epidural Guidance Systems Market Size, Share, and Growth Forecast, 2026 - 2033

Epidural Guidance Systems Market by Product Type (Single-Needle Systems, Double-Needle Systems, Imaging-guided Epidural Devices, Others), Technology (Ultrasound, Fluoroscopy, Image Guidance), and Regional Analysis for 2026 - 2033

Epidural Guidance Systems Market Size and Trends Analysis

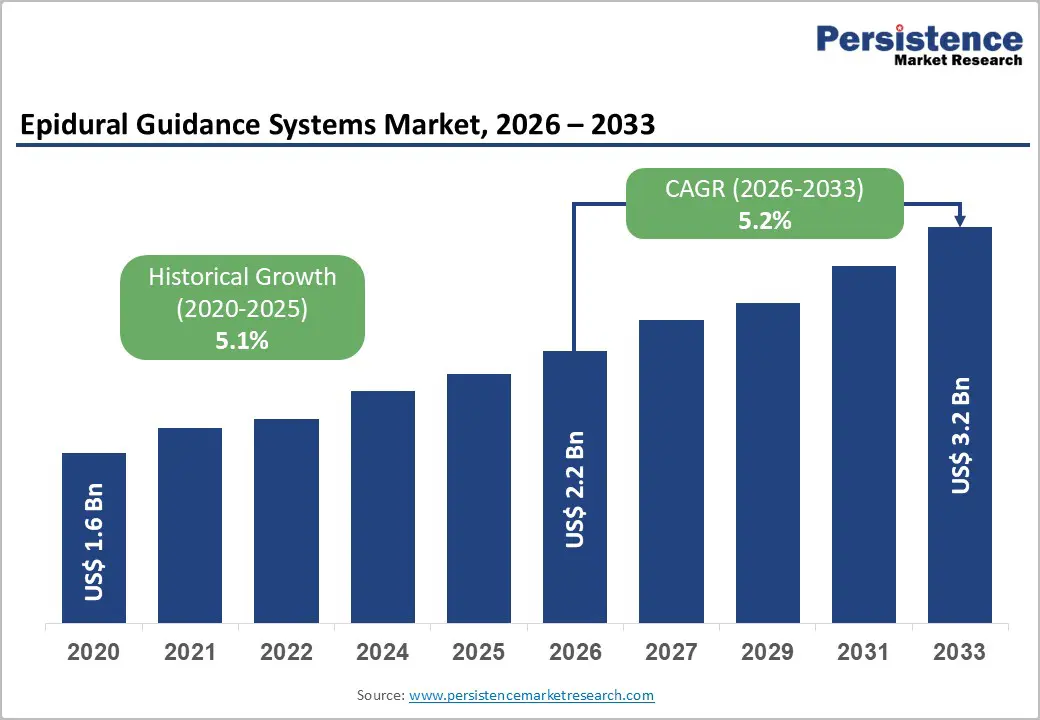

The global epidural guidance systems market size is likely to be valued at US$2.2 billion in 2026 and is expected to reach US$3.1 billion by 2033, growing at a CAGR of 5.5% during the forecast period from 2026 to 2033, driven by the increasing prevalence of chronic pain disorders, a rising number of surgical interventions requiring regional anesthesia, and growing demand for safer, image-assisted procedural techniques.

According to the World Health Organization, chronic musculoskeletal pain, particularly low back pain, affected an estimated 619 million people worldwide in 2020, making it the single leading cause of disability across age groups and with projected increases as populations age and expand. Healthcare providers are increasingly prioritizing real-time visualization tools to enhance clinical precision, reduce failed attempts, and improve patient outcomes, particularly in high-risk and anatomically challenging cases.

Key Industry Highlights:

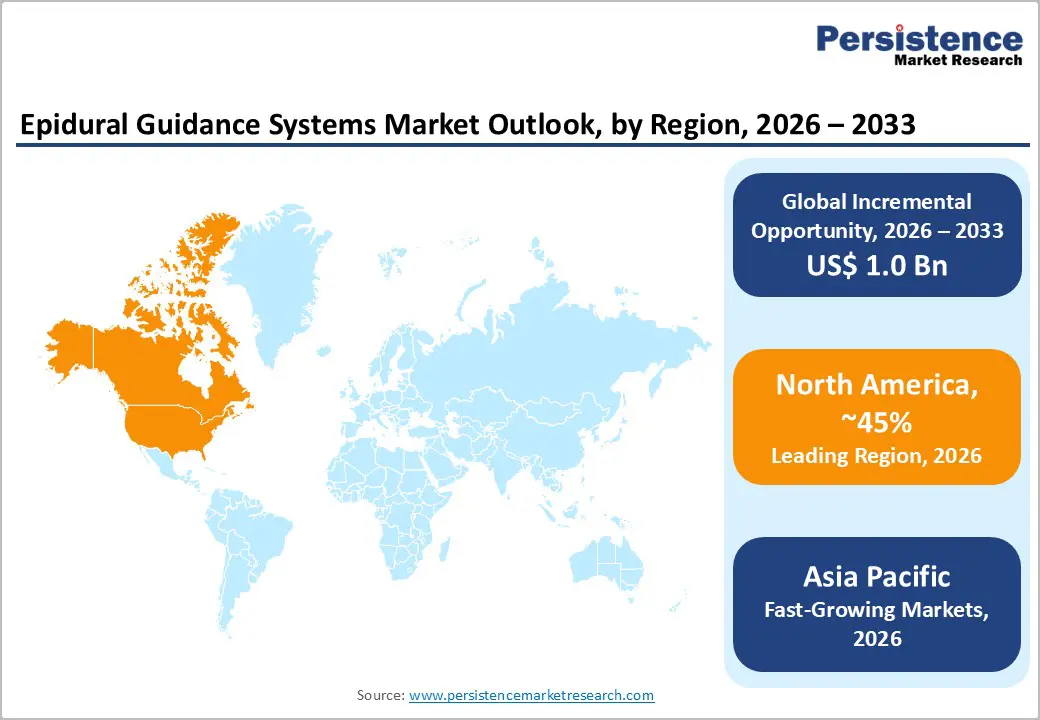

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 45% in 2026, driven by advanced healthcare infrastructure, high chronic pain prevalence, and strong adoption of innovative guidance technologies.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the epidural guidance systems in 2026, supported by expanding healthcare infrastructure, rising procedure volumes, and growing adoption of cost-effective guidance technologies.

- Leading Product Type: Imaging-guided epidural devices are projected to represent the leading product type in 2026, accounting for 40% of the revenue share, driven by superior real-time visualization and procedural accuracy.

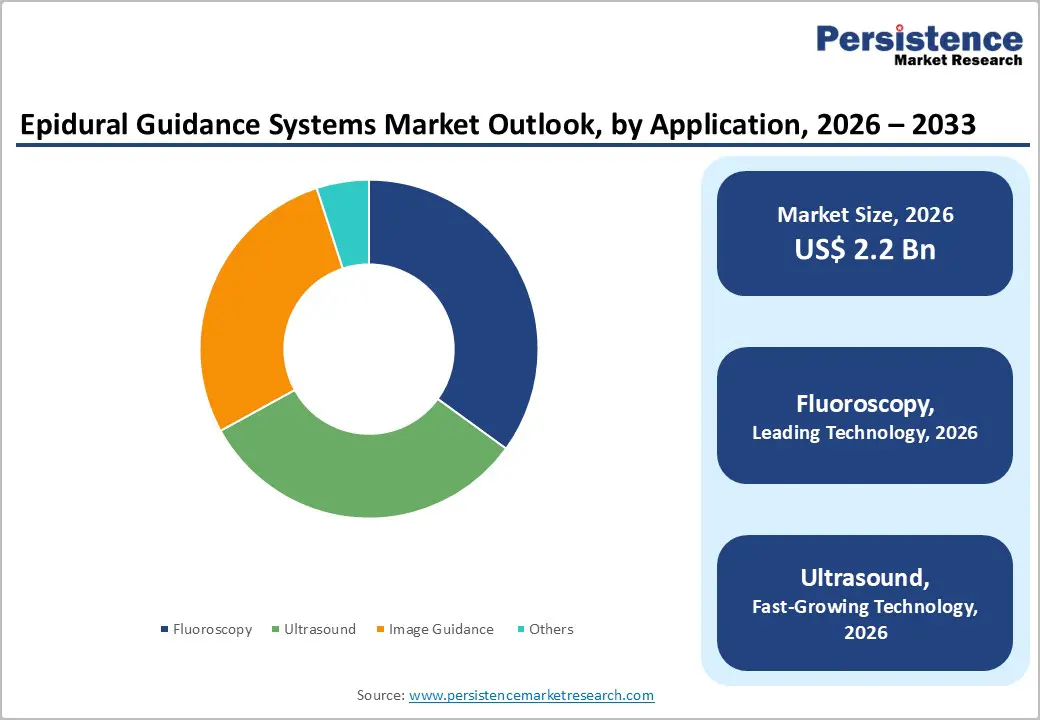

- Leading Technology: Fluoroscopy is anticipated to be the leading technology, accounting for over 35% of the revenue share in 2026, supported by its high precision in spine and orthopedic procedures and established adoption in tertiary hospitals.

| Key Insights | Details |

|---|---|

|

Epidural Guidance Systems Market Size (2026E) |

US$2.2 Bn |

|

Market Value Forecast (2033F) |

US$3.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Prevalence of Chronic Pain and Aging Populations

The rising prevalence of chronic pain, particularly musculoskeletal and neuropathic conditions, significantly drives the demand for epidural guidance systems. As populations age, the incidence of degenerative spinal disorders and associated pain increases, necessitating safer and more effective pain management interventions. Epidural procedures guided by advanced imaging reduce complications, improve procedural accuracy, and enhance patient comfort, which is particularly critical in elderly populations. Hospitals and ambulatory surgical centers are increasingly adopting these systems to manage rising caseloads efficiently, improve patient outcomes, and address the growing need for targeted analgesia. The demographic shift ensures sustained market expansion over the long term.

Chronic pain management is also influenced by increasing awareness among patients and clinicians regarding the risks of systemic medications and the benefits of minimally invasive interventions. Epidural guidance systems allow precise drug delivery and targeted nerve blockade, reducing reliance on oral analgesics and enhancing patient safety. Healthcare providers are integrating these systems into standard pain management protocols, particularly for post-surgical and long-term care in geriatric patients. The combination of growing chronic pain cases, population aging, and procedural advancements reinforces ongoing investment in equipment, training, and infrastructure, positioning the market for steady, evidence-based growth over the coming decade.

Technological Advancements in Imaging and Ultrasound Integration

Innovations in imaging, including high-resolution ultrasound and hybrid image-guided technologies, are key drivers of the epidural guidance systems market. Real-time visualization of soft tissues and bony landmarks enhances needle placement accuracy, reduces procedural complications, and shortens procedural time. Integration with portable and point-of-care ultrasound devices allows for broader adoption in ambulatory centers and remote healthcare settings. These advancements facilitate safer anesthesia administration in complex cases such as labor analgesia, spine surgeries, and orthopedic procedures, making them increasingly preferred over traditional manual techniques.

Emerging technologies, including 3D imaging, Doppler-assisted needle guidance, and contrast-enhanced visualization, expand the scope and reliability of epidural procedures. Training programs leverage ultrasound simulators to enhance clinician proficiency, accelerating adoption across regions. Digital integration with hospital information systems allows real-time procedural documentation, reducing errors and improving compliance with safety guidelines. These technological enhancements directly respond to the growing demand for precision, safety, and efficiency in pain management and surgical procedures, ensuring the continued evolution of the market while driving confidence among healthcare providers in the use of guided epidural interventions.

Barrier Analysis - Shortage of Trained Healthcare Professionals

The adoption of epidural guidance systems is constrained by a shortage of trained anesthesiologists, pain specialists, and clinicians skilled in image-guided procedures. Advanced systems require significant technical expertise, including proficiency in ultrasound interpretation, fluoroscopy, and hybrid navigation tools. Many regions, especially in emerging markets, face limited training infrastructure, slowing the integration of these devices into routine practice. This shortage affects both hospitals and ambulatory centers, as inexperienced personnel may underutilize or incorrectly operate guidance systems, increasing procedural risks. Workforce limitations remain a significant barrier to achieving full market potential despite growing clinical demand for safe and precise epidural interventions.

Training and certification programs are gradually expanding but remain insufficient to meet the rapid market growth. High staff turnover and uneven distribution of skilled professionals exacerbate access issues, particularly in rural and semi-urban healthcare facilities. Hospitals and device manufacturers are investing in on-site training and simulation-based education to overcome these challenges; however, scaling such programs is time-consuming and costly. The combination of technical complexity and workforce scarcity can limit adoption rates, especially in regions where procedural volumes are rising faster than the availability of qualified operators.

Technical Limitations in Certain Patient Populations

Certain patient populations, including obese individuals, patients with spinal deformities, or those with previous surgical interventions, present challenges for epidural procedures. Imaging and guidance systems may face reduced visibility, anatomical distortion, or limited access, resulting in increased procedural complexity. These technical limitations can lead to failed attempts, prolonged procedural time, or complications, reducing clinician confidence in adopting advanced systems in all cases. Hospitals may rely on traditional manual techniques for high-risk populations, slowing the overall uptake of guidance technologies despite their general advantages in standard patient groups.

Patient-specific factors such as variability in tissue density, calcifications, or co-morbidities can affect imaging quality, needle trajectory, and drug delivery accuracy. While emerging innovations such as AI-assisted needle tracking and adaptive imaging aim to mitigate these limitations, implementation is not yet widespread. A subset of patients remains challenging for consistent, reliable use of guided epidural systems, limiting universal applicability. These technical barriers necessitate ongoing R&D and clinician training to expand device utility and confidence across diverse patient populations, maintaining market growth potential while acknowledging procedural constraints.

Opportunity Analysis - Technological Convergence with AI and Robotics

The integration of AI and robotic technologies presents a major opportunity to enhance epidural guidance systems. AI algorithms can assist clinicians in identifying anatomical landmarks, predicting needle trajectories, and providing real-time feedback, improving procedural accuracy and reducing complication rates. Robotic-assisted platforms can standardize needle placement, minimize human error, and enhance reproducibility in complex procedures. Convergence with digital imaging systems enables data-driven decision-making, integration with hospital records, and predictive analytics for patient outcomes. These innovations position the market for next-generation solutions that combine precision, automation, and safety for widespread adoption in hospitals and specialized pain clinics.

AI and robotic integration also allows for enhanced training and simulation opportunities, enabling clinicians to gain proficiency without patient risk. Predictive models and automated guidance systems reduce variability between operators and improve efficiency, particularly in high-volume surgical centers. As healthcare systems increasingly embrace smart technologies, these convergent solutions offer differentiation for manufacturers and create new revenue streams. Early adoption in tertiary hospitals and research centers can drive broader market acceptance, while continuous innovation ensures that guidance systems evolve alongside emerging clinical needs.

Growth in Non-Opioid Pain Management Protocols

Rising concerns over opioid dependence and side effects have accelerated the adoption of non-opioid pain management strategies, including image-guided epidural interventions. Hospitals and clinics increasingly prefer targeted regional anesthesia and minimally invasive procedures that reduce systemic drug exposure while providing effective analgesia. Epidural guidance systems support these protocols by enabling precise drug delivery, optimizing dosage, and improving patient comfort. This shift aligns with initiatives promoting safer pain management practices and enhances procedural adoption in perioperative, obstetric, and chronic pain settings.

Non-opioid strategies also encourage multidisciplinary care approaches integrating interventional techniques, physiotherapy, and rehabilitation, which rely on precise procedural support. Imaging-guided epidural systems complement these approaches by providing accurate, minimally invasive analgesic delivery. The expansion of enhanced recovery after surgery (ERAS) programs and outpatient pain clinics drives demand for such systems, emphasizing safety, efficiency, and patient-centered care. As hospitals and regulatory agencies prioritize non-opioid protocols, the adoption of advanced guidance technologies is providing both clinical and commercial opportunities for manufacturers.

Category-wise Analysis

Product Type Insights

Imaging-guided epidural devices are expected to lead the epidural guidance systems market, accounting for approximately 40% of revenue in 2026, driven by their ability to provide superior real-time visualization, improve procedural accuracy, and reduce complications compared to manual techniques. Hospitals and ambulatory surgical centers increasingly rely on these devices for complex procedures such as spine surgeries, labor analgesia, and chronic pain interventions. For example, the integration of Philips ultrasound-guided epidural systems in leading U.S. hospitals has enhanced clinicians’ ability to visualize soft tissue and bony landmarks in real time, reducing failed attempts and procedural discomfort. Such systems are favored in tertiary hospitals where precision and patient safety are prioritized, particularly for elderly patients or those with anatomical challenges.

Non-invasive epidural systems are likely to represent the fastest-growing segment, supported by increasing demand for portable, radiation-free, and point-of-care compatible solutions. These systems appeal to hospitals, outpatient centers, and rural clinics aiming to provide safe, minimally invasive pain management and anesthesia procedures. For example, optical and pressure-based non-invasive devices are increasingly used in labor and delivery units to monitor epidural placement without ionizing radiation. The growth is supported by regulatory emphasis on patient safety and a preference for technologies that minimize procedural risk, particularly for vulnerable populations such as pregnant women or patients with comorbidities.

Technology Insights

Fluoroscopy is projected to lead the market, capturing around 35% of the revenue share in 2026, supported by its dominance in high-precision spine, orthopedic, and thoracic procedures that require clear visualization of bony landmarks. Hospitals performing complex surgeries, such as spinal fusion, rely on fluoroscopic guidance to enhance procedural accuracy and reduce complications. For example, tertiary care hospitals in the United States extensively use fluoroscopy in orthopedic spine interventions, ensuring safe and precise needle placement while minimizing procedural errors. The established infrastructure, including fluoroscopic imaging suites and trained radiology support, reinforces its adoption in high-volume centers.

Ultrasound is likely to be the fastest-growing technology, driven by portability, absence of ionizing radiation, and real-time soft tissue imaging advantages. Adoption is particularly notable in labor and delivery suites and ambulatory surgical centers, where ultrasound-guided epidural placement enhances safety and efficiency. For example, FUJIFILM Sonosite ultrasound systems are widely implemented in obstetric units to visualize the epidural space, reducing failed attempts and patient discomfort. The technology aligns with minimally invasive procedural trends, offering a cost-effective, user-friendly alternative to fluoroscopy. Clinicians benefit from the ease of training, ability to perform point-of-care imaging, and rapid procedural feedback, which increases confidence and adoption rates.

Regional Insights

North America Epidural Guidance Systems Market Trends

North America is anticipated to be the leading region, accounting for a market share of 45% in 2026, driven by advanced healthcare infrastructure, high procedural volumes, and strong clinical emphasis on patient safety and procedural accuracy. Hospitals and ambulatory surgical centers across the United States and Canada increasingly adopt image-guided technologies to support regional anesthesia and pain management procedures. For example, Koninklijke Philips N.V.’s ultrasound-based epidural guidance solutions are widely used in major U.S. medical centers to enhance labor analgesia outcomes and reduce procedure times by providing clinicians with high-resolution, portable imaging that supports accurate needle guidance.

North America also shows strong growth in outpatient and ambulatory settings as procedural volumes shift away from traditional hospital environments. Rising prevalence of chronic back pain, an aging population, and increasing utilization of minimally invasive pain interventions contribute to this trend, encouraging smaller clinics to invest in portable, user-friendly guidance platforms. Ultrasound adoption is particularly notable in labor and delivery suites and pain management clinics, where clinicians seek radiation-free alternatives that support safe, cost-effective care. Competitive dynamics in the region reflect both established multinationals and innovative specialized firms advancing feature-rich systems with AI-enabled imaging and digital workflow integration.

Europe Epidural Guidance Systems Market Trends

Europe is likely to be a significant market for epidural guidance systems in 2026, due to diversified healthcare systems, varied reimbursement policies, and increasing demand for precision anesthesia and pain management technologies across Western and Northern Europe. Hospitals and surgical centers in Germany, France, and the U.K. are investing in advanced imaging modalities to support complex procedures such as spine surgery, obstetric analgesia, and orthopedic interventions. Adoption is supported by growing clinician preference for ultrasound and fluoroscopic guidance to reduce complications and improve patient outcomes, particularly among aging populations with higher chronic pain incidence.

Despite fragmentation, competitive intensity is rising as both multinational corporations and regional specialists vie for a share in Western and emerging Eastern European markets. Local manufacturers and distributors capitalize on cost-effective imaging platforms tailored to mid-tier hospitals, while leaders emphasize feature-rich guidance systems with advanced software, real-time visualization, and seamless integration with hospital IT. For example, Northern Digital Inc.’s navigation-assisted epidural devices are gaining traction in specialty pain clinics and university hospitals for their precision tracking and reduced operator dependency.

Asia Pacific Epidural Guidance Systems Market Trends

The Asia Pacific region is likely to be the fastest-growing region in 2026, driven by healthcare infrastructure and clinical demand for precision anesthesia and pain management technologies increasing across China, India, Japan, and Southeast Asia. Rising prevalence of chronic pain conditions and greater surgical volumes in orthopedic, spine, and obstetric care are driving the adoption of real-time imaging guidance systems that improve needle placement accuracy and reduce complications. Clinicians in major urban hospitals are increasingly incorporating advanced guidance tools to enhance procedural confidence and patient safety.

Beyond major metropolitan centers, secondary cities and community hospitals are also investing in epidural guidance technologies to broaden access to safe procedural care. Cost-effective systems suited for point-of-care use are gaining traction in outpatient surgical centers and pain clinics, helping clinicians deliver targeted pain management with greater precision. For example, Northern Digital Inc.’s navigation-assisted guidance systems are being deployed in specialty spine and pain treatment centers throughout Australia, integrating optical tracking and imaging to support complex epidural placements with enhanced accuracy. These platforms help clinicians overcome anatomical variability and reduce procedure times, which is especially valuable in high-throughput clinical settings.

Competitive Landscape

The global epidural guidance systems market exhibits a moderately fragmented structure, driven by the presence of a mix of large multinational corporations and specialized medical device innovators investing in imaging, navigation, and point-of-care technologies. Demand for safer, more accurate regional anesthesia and pain management solutions has encouraged both established players and niche firms to expand their portfolios, with products spanning ultrasound guidance, fluoroscopic systems, and hybrid image-assisted platforms.

With key leaders including Koninklijke Philips N.V., FUJIFILM Sonosite, Inc., BK Medical Holding Company, Inc., and Northern Digital Inc. offering advanced imaging and navigation solutions tailored to epidural procedures, competitive dynamics remain robust across regions. These companies continuously refine hardware, software, and clinician support services to maintain clinical relevance and address evolving procedural needs. The competitive landscape is shaped by regional specialists, emerging innovators, and local manufacturers targeting cost-effective, portable systems for ambulatory and point-of-care use.

Key Industry Developments:

- In February 2026, Milestone Scientific launched its CompuFlo® Advisor Program to expand commercial adoption and support broader Medicare reimbursement for its computerized epidural guidance technology. The initiative, which began on February 1, targets high-volume interventional pain and anesthesia practices in key Medicare Administrative Contractor regions to generate clinical case data aimed at advancing reimbursement coding and utilization. The program engages reimbursement specialists to assist providers with claims and documentation, positioning the CompuFlo system’s pressure-guided feedback technology as a more consistent and precise alternative for epidural procedures.

- In November 2025, Robotron Surgical Technologies announced progress on Epiduro™, an AI-driven flexible robotic platform designed to enable next-generation epidural procedures. The system combines flexible robotics, AI-based navigation, and 3D anatomical modeling to facilitate minimally invasive access and treatment within the epidural space via the sacral hiatus. Unlike traditional robotic systems focused on screw placement, Epiduro™ aims to support targeted drug delivery, neuromodulation, and diagnostic endoscopy with enhanced control and real-time anatomical recognition. Early development efforts emphasize realistic simulation and integration of advanced imaging for improved safety, procedural efficiency, and patient outcomes, marking a notable advancement in spinal and epidural care technologies.

Companies Covered in Epidural Guidance Systems Market

- Shenzhen Ricso Technology Co., Ltd.

- BMV

- ERTUNÇ ÖZCAN

- KOELIS

- Konica Minolta, Inc.

- MLR System GmbH

- BK Medical Holding Company, Inc.

- Northern Digital Inc.

- Koninklijke Philips N.V.

- FUJIFILM Sonosite, Inc.

- Smith & Nephew

- Abbott Laboratories

- Olympus Corporation

Frequently Asked Questions

The global epidural guidance systems market is projected to reach US$2.2 billion in 2026.

Rising demand for safer and more accurate epidural procedures in anesthesia and pain management, driven by increasing surgical volumes and the need to reduce complications, primarily drives the epidural guidance systems market.

The epidural guidance systems market is expected to grow at a CAGR of 5.5% from 2026 to 2033.

Key market opportunities lie in the integration of AI-assisted and imaging-guided technologies, along with expanding reimbursement support and growing adoption in pain management and ambulatory surgical centers.

Shenzhen Ricso Technology Co., Ltd, BMV, ERTUNÇ ÖZCAN, and KOELIS are the leading players.