- Pharmaceuticals

- Enthesopathy Treatment Market

Enthesopathy Treatment Market Size, Share, and Growth Forecast, 2026 - 2033

Enthesopathy Treatment Market by Treatment Type (Non-Steroidal Anti-Inflammatory Drugs, Corticosteroid Injections, Others), Disease Indication (Plantar Fasciitis, Others), End-user (Hospitals & Clinics, Others), and Regional Analysis for 2026 – 2033

Enthesopathy Treatment Market Size and Trends Analysis

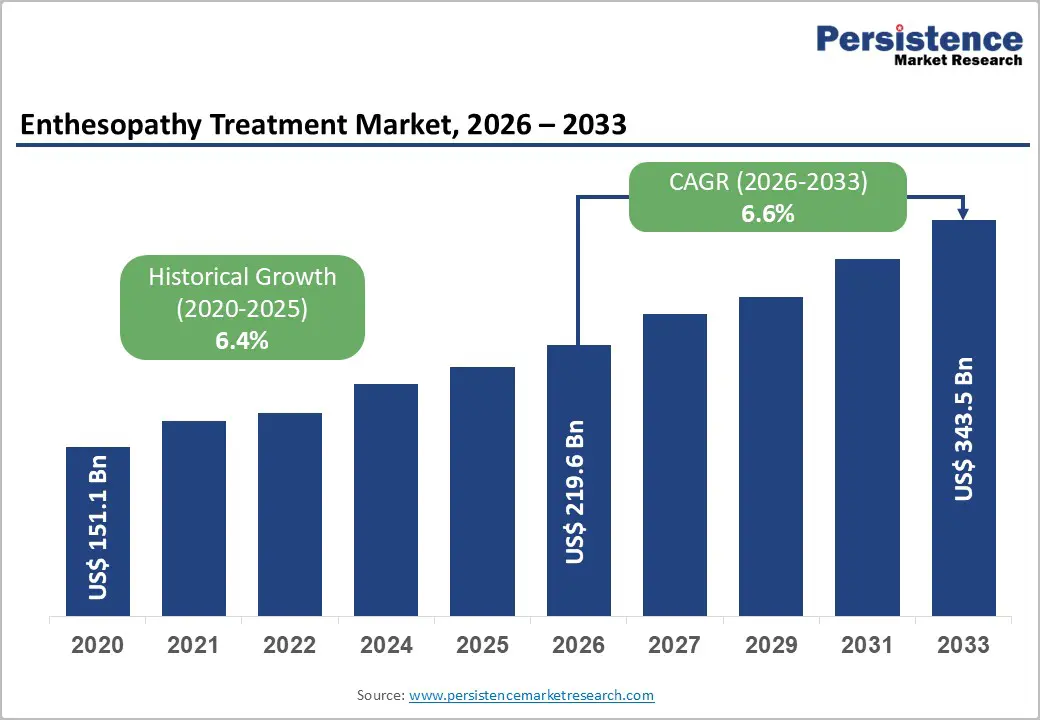

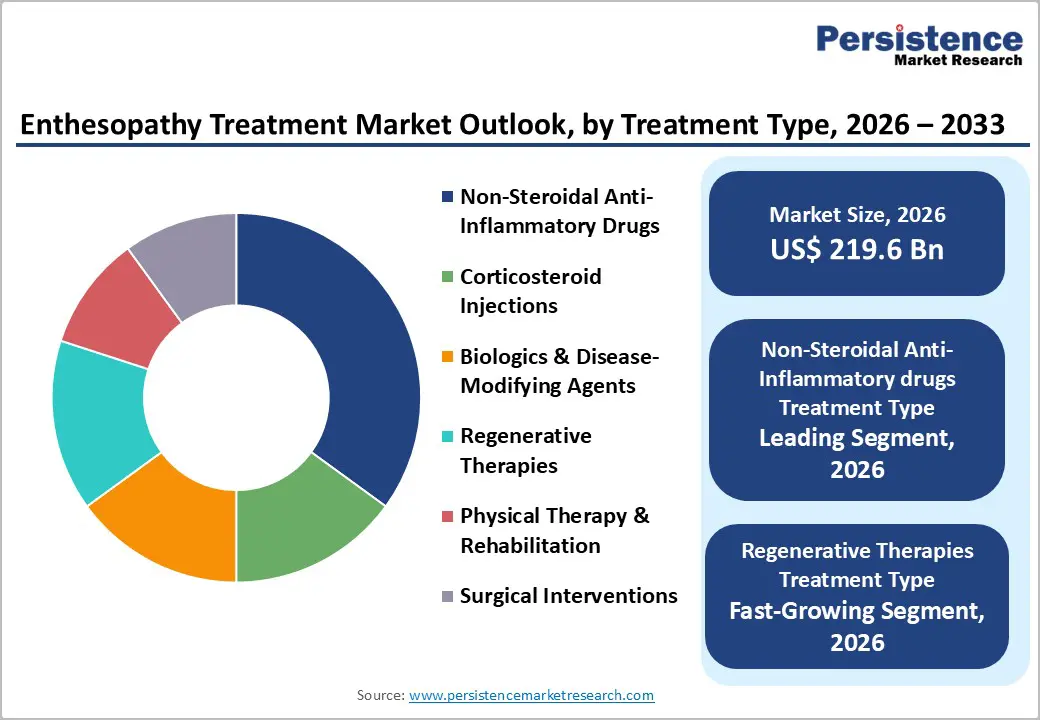

The global enthesopathy treatment market size is likely to be valued at US$219.6 billion in 2026, and is expected to reach US$343.5 billion by 2033, growing at a CAGR of 6.6% during the forecast period from 2026 to 2033, driven by the increasing prevalence of musculoskeletal disorders, rising geriatric population prone to degenerative tendon conditions, and growing adoption of biologic and regenerative therapies for chronic enthesopathy management.

The growing demand for non-invasive, disease-modifying treatments for enthesopathy, including corticosteroid injections and biologics for conditions like plantar fasciitis and rotator cuff tendinopathy, is driving adoption. Advances in regenerative therapies (PRP, stem cells) and targeted DMARDs are further enhancing long-term outcomes and reducing steroid use. The increasing focus on enthesopathy treatment to improve mobility, reduce disability, and manage spondyloarthropathies in aging populations is fueling market growth.

Key Industry Highlights:

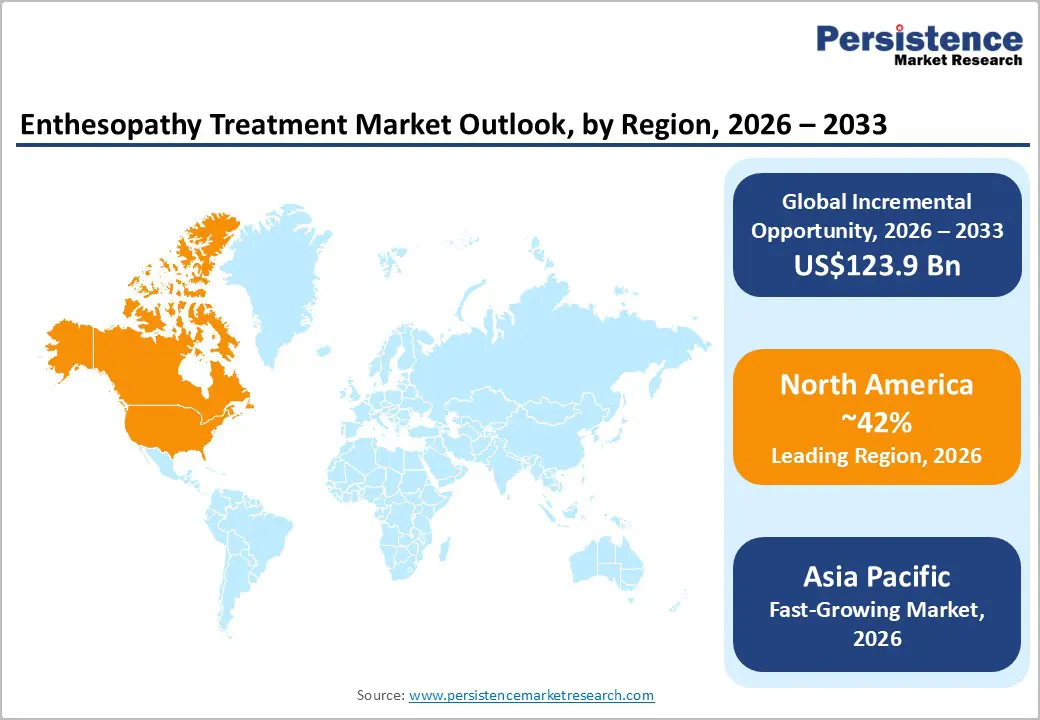

- Leading Region: North America, anticipated to account for a 42% market share in 2026, driven by high adoption of innovative therapies, including biologics, regenerative treatments, and advanced surgical interventions.

- Fastest-growing Region: Asia Pacific, fueled by rising musculoskeletal disease burden, expanding specialty orthopedic infrastructure, and growing investments in biologics in China and India.

- Dominant Treatment Type: Non-steroidal anti-inflammatory drugs, to hold approximately 38% of the market share, as they remain first-line therapy for acute and chronic pain control.

- Leading Disease Indication: Plantar fasciitis, contributing nearly 28% of the market revenue, due to highest community prevalence.

| Key Insights | Details |

|---|---|

| Enthesopathy Treatment Market Size (2026E) | US$219.6 Bn |

| Market Value Forecast (2033F) | US$343.5 Bn |

| Projected Growth CAGR (2026-2033) | 6.6% |

| Historical Market Growth (2020-2025) | 6.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Rising Prevalence of Musculoskeletal Disorders and Geriatric Population Growth

The rising prevalence of musculoskeletal disorders, combined with rapid growth in the geriatric population, is a key factor driving demand for enthesopathy treatments. Musculoskeletal conditions such as tendon disorders, joint degeneration, and chronic inflammatory diseases are becoming more common due to sedentary lifestyles, repetitive strain from work, obesity, and increased participation in sports and physical activities. These factors place continuous stress on tendons and ligaments, increasing the risk of inflammation and degeneration at enthesis sites over time.

Global populations are aging, and older adults are particularly vulnerable to enthesopathy. Age-related changes, including reduced tissue elasticity, slower healing capacity, and cumulative mechanical wear, increase susceptibility to tendon and ligament attachment injuries. Many elderly individuals also live with comorbid conditions such as arthritis or osteoporosis, which further elevate the risk of chronic pain and functional limitation. As life expectancy increases, maintaining mobility and independence has become a priority for aging populations. This has led to greater demand for effective treatments that manage pain, restore function, and improve quality of life.

Increasing Adoption of Regenerative Therapies and Biologics in Refractory Cases

The increasing adoption of regenerative therapies and biologics in refractory enthesopathy cases reflects a shift toward more targeted and durable treatment approaches when conventional options fail. Refractory cases where patients do not respond adequately to NSAIDs, physical therapy, or corticosteroid injections often involve chronic inflammation or structural damage at the tendon or ligament insertion site. In such situations, biologics offer an advantage by targeting specific inflammatory pathways, helping to control persistent symptoms and slow disease progression, particularly in inflammatory-related enthesopathies.

Regenerative therapies, such as platelet-rich plasma and cell-based treatments, are also gaining traction because they aim to stimulate tissue repair rather than simply manage pain. These approaches are increasingly considered for patients with recurring symptoms, athletes, and individuals seeking to avoid long-term drug use or surgery. Advances in imaging and diagnostic techniques have further supported adoption by enabling more precise targeting of affected enthesis sites, improving treatment confidence among clinicians. Although cost and regulatory challenges remain, growing clinical experience and improving outcomes are encouraging broader use of these advanced therapies in difficult-to-treat cases.

Barrier Analysis – High Cost of Biologics, Regenerative Therapies, and Surgical Interventions

The high cost of biologics, regenerative therapies, and surgical interventions is a major restraint in the enthesopathy treatment market, limiting widespread adoption despite their clinical potential. Biologic drugs, which target specific inflammatory pathways, are expensive to develop and manufacture due to complex production processes, stringent quality controls, and cold-chain storage requirements. These high production costs are often reflected in treatment pricing, making biologics unaffordable for many patients, especially in regions with limited insurance coverage or out-of-pocket payment models.

Regenerative therapies such as platelet-rich plasma and stem cell treatments also involve high costs. These procedures require specialized equipment, trained medical personnel, and controlled clinical settings. In addition, variability in preparation methods and the lack of large-scale standardization increase operational expenses. Many healthcare systems classify these therapies as elective or experimental, resulting in limited reimbursement and further restricting patient access. Surgical interventions for severe or chronic enthesopathy add another layer of financial burden. Surgery involves hospital stays, advanced imaging, anesthesia, and extended rehabilitation, all of which contribute to high overall treatment costs.

Slow Clinical Validation and Regulatory Hurdles

Slow clinical validation and regulatory hurdles represent a significant restraint in the enthesopathy treatment market, particularly for newer and advanced therapies. Many emerging treatment options, such as biologics and regenerative approaches including platelet-rich plasma and stem cell–based therapies, require extensive clinical evaluation to demonstrate long-term safety, effectiveness, and consistency of outcomes. Enthesopathy is a heterogeneous condition with varying causes and severity, which makes it difficult to design large, standardized clinical trials. As a result, gathering robust clinical evidence often takes longer compared to treatments for more clearly defined diseases.

Regulatory agencies also apply strict scrutiny to these therapies because they directly affect musculoskeletal function and quality of life. Developers must meet complex requirements related to manufacturing processes, quality control, and patient safety, which can significantly extend approval timelines. For regenerative treatments in particular, differences in sourcing, processing, and delivery methods raise additional regulatory concerns, increasing the burden of compliance.

Opportunity Analysis – Innovation in Next-Generation Biologics

Opportunities in next-generation biologics, point-of-care regenerative therapies, and value-based outpatient models are transforming enthesopathy management by addressing two major challenges, limited disease modification and high procedural costs. Next-generation platforms (JAK inhibitors, IL-23-specific agents, bispecific antibodies) are engineered to achieve deeper entheseal remission with better safety profiles, reducing steroid dependence and progression to irreversible damage. Innovations, such as single-injection PRP systems, ultrasound-guided autologous therapies, and office-based biologic delivery, significantly improve accessibility and lower delivery costs, broadening use in community settings.

Progress in value-based care models, bundled payments, and tele-rehabilitation integration supports higher adherence and outcomes while containing payer expenditure. These formats eliminate conventional treatment trade-offs, enhance patient recovery, and allow versatile use across chronic and acute cases, making them highly suitable for mass orthopedic programs. New technologies such as AI-guided injection, biomarker-driven patient selection, and digital outcome tracking further enhance precision and response.

Expansion in Point-of-Care Regenerative Therapies and Value-Based Outpatient Models

Point-of-care regenerative therapies and value-based outpatient models are increasingly shaping the treatment landscape for enthesopathy and other musculoskeletal conditions. Point-of-care regenerative approaches, such as platelet-rich plasma and autologous cell-based treatments, are administered directly at the clinical site, reducing the need for complex laboratory processing or multiple patient visits. This immediacy allows clinicians to deliver targeted therapy during a single appointment, improving patient convenience and potentially accelerating recovery. By using a patient’s own biological materials, these therapies also reduce risks related to immune reactions and long-term drug dependence.

Value-based outpatient care models are gaining importance as healthcare systems focus on outcomes rather than volume of services. These models emphasize cost efficiency, measurable improvements in pain and mobility, and shorter recovery times. Treating enthesopathy in outpatient settings minimizes hospital stays, lowers procedural costs, and reduces disruption to patients’ daily lives. Rehabilitation, follow-up monitoring, and outcome tracking are often integrated into a single care pathway, improving continuity of care. Point-of-care regenerative therapies and value-based outpatient models support more personalized, efficient treatment strategies.

Category-wise Analysis

Treatment Type Insights

Non-steroidal anti-inflammatory drugs are expected to lead the market, holding 38% of the share in 2026, due to their widespread use as first-line therapy for pain and inflammation. NSAIDs are commonly prescribed because they provide rapid symptom relief, are widely available, and are relatively affordable compared with advanced therapies. They are effective across a broad range of enthesopathy conditions and can be used in both acute and early-stage cases. Naproxen marketed under the brand name Aleve by Bayer, and ibuprofen, sold as Advil and Motrin by Pfizer, are frequently recommended as first-line medications to relieve pain and inflammation associated with plantar fasciitis and similar tendon insertion disorders. These NSAIDs are often suggested by clinicians to ease symptoms so patients can continue with stretching, physical therapy, and other conservative measures, especially in early or mild cases.

Regenerative therapies are likely the fastest-growing treatment type, fueled by their ability to address the underlying cause of tissue damage rather than only managing symptoms. Approaches such as platelet-rich plasma and cell-based therapies aim to stimulate natural healing at tendon and ligament attachment sites, making them attractive for chronic and refractory cases. Growing patient preference for minimally invasive options, combined with advances in imaging and targeted delivery, is increasing clinician confidence in these treatments. The use of Platelet-Rich Plasma (PRP) injections which are widely offered as a biologic treatment for chronic tendon injuries. Clinics and practices across the U.S. routinely use PRP therapy to treat conditions such as tendinopathies (e.g., tennis elbow, Achilles tendinopathy, and plantar fasciitis) by concentrating a patient’s own blood platelets and injecting them into the affected area to stimulate healing and tissue regeneration.

Disease Indication Insights

Plantar fasciitis is expected to dominate the market, contributing nearly 28% of revenue in 2026, propelled by its high prevalence and frequent need for medical intervention. It is one of the most common causes of heel pain, affecting a wide range of individuals, including older adults, athletes, and people with prolonged standing or obesity. The condition often requires repeated treatment through medications, physical therapy, orthotics, or injections, which increases overall healthcare spending. Pfizer’s Advil (ibuprofen), a widely used NSAID, is commonly recommended by clinicians to manage pain and inflammation in patients with plantar fasciitis, one of the most prevalent enthesopathies. According to Mayo Clinic, non-steroidal anti-inflammatory drugs such as ibuprofen (marketed by Pfizer as Advil) are routinely used in the initial treatment protocol for plantar fasciitis to reduce heel pain and swelling.

Rotator cuff tendinopathy represents the fastest-growing indication, driven by increasing prevalence of shoulder injuries from aging, repetitive overhead activities, and sports participation. The condition often leads to chronic pain, reduced mobility, and functional limitations, driving demand for both conservative and advanced therapies. Rising awareness among patients and clinicians about the long-term impact of untreated rotator cuff injuries has accelerated adoption of targeted treatments, including physical therapy, NSAIDs, corticosteroid injections, and regenerative approaches. Smith & Nephew plc, a global medical technology company that markets REGENETEN® Bioinductive Implant for rotator cuff repair. This implant is designed to support biological healing and is increasingly used in surgical procedures for patients with chronic rotator cuff tendinopathy, where traditional conservative treatments have been insufficient. Its adoption reflects rising clinical demand for advanced solutions aimed at improving tendon healing and functional outcomes.

Regional Insights

North America Enthesopathy Treatment Market Trends

North America is projected to dominate the market, accounting for nearly 42% of the revenue in 2026, supported by the region’s high musculoskeletal disorder prevalence, strong reimbursement for biologics and injections, and high public awareness of advanced orthopedic care. Treatment systems in the U.S. and Canada provide extensive support for enthesopathy programs, ensuring wide accessibility across NSAIDs, biologics, and regenerative populations. Increasing demand for outpatient, convenient, and easy-to-administer forms is further accelerating adoption, as these formats improve compliance and reduce barriers associated with surgical escalation.

Innovation in enthesopathy treatment technology, including stable regenerative, improved biologic delivery, and targeted personalized enhancement, is attracting significant investment from both public and private sectors. Government initiatives and CMS campaigns continue to promote use against disability risks, chronic pain burden, and emerging aging threats, creating sustained market demand. The growing focus on rotator cuff grades and specialty uses, particularly for plantar fasciitis and others, is expanding the target applications for enthesopathy treatment.

Europe Enthesopathy Treatment Market Trends

Europe is showing significant growth by increasing awareness of biologic and regenerative benefits, strong regulatory systems, and government-led musculoskeletal health programs. Countries such as Germany, France, Italy, and Spain have well-established orthopedic frameworks that support routine enthesopathy treatment and encourage adoption of innovative therapy delivery methods, including biologics and regenerative approaches. These advanced formulations are particularly appealing for plantar fasciitis populations, regulation-conscious specialists, and rotator cuff users, improving outcomes and coverage rates.

Technological advancements in enthesopathy treatment development, such as enhanced injection precision, application-targeted delivery, and improved regenerative grades, are further boosting market potential. European authorities are increasingly supporting research and trials for therapies against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, non-surgical options is aligned with the region’s focus on preventive disability reduction and healthcare cost control. Public awareness campaigns and promotion drives are expanding reach in both urban and rural areas, while providers are investing in biologics and novel variants to increase efficacy.

Asia Pacific Enthesopathy Treatment Market Trends

Asia Pacific is likely to be the fastest-growing market for enthesopathy treatment in 2026, driven by rising musculoskeletal awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Japan, and South Korea are actively promoting treatment campaigns to address aging populations and emerging orthopedic needs. Enthesopathy treatments are particularly attractive in these regions due to their scalable administration, ease of access, and suitability for large-scale outpatient drives in both urban and rural populations.

Technological advancements are supporting the development of stable, effective, and easy-to-deliver enthesopathy therapies, which can withstand challenging reimbursement conditions and minimize procedural dependence. These innovations are critical for reaching domestic patients and improving overall care coverage. Growing demand for NSAIDs, corticosteroid injections, and biologics applications is contributing to market expansion. Public-private partnerships, increased healthcare expenditure, and rising investment in orthopedic research and clinic capacity are further accelerating growth. The convenience of treatment delivery, combined with improved mobility and reduced risk of disability, positions enthesopathy treatment as a preferred choice.

Competitive Landscape

The global enthesopathy treatment market features competition between established pharmaceutical leaders and emerging regenerative therapy specialists. In North America and Europe, Eli Lilly and Co. Ltd and Janssen Biotech, Inc. lead through strong R&D, distribution networks, and guideline inclusion, bolstered by innovative biologics and DMARD programs. In Asia Pacific, domestic players advance with cost-competitive NSAIDs and injection solutions, enhancing accessibility. Regenerative delivery boosts long-term outcomes, cuts steroid risks, and enables mass integrations across clinics. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. Personalized formulations solve response issues, aiding penetration in refractory cases.

Key Industry Developments:

- In March 2025, Smith+Nephew, the global medical technology company, announced that the latest advancements in Sports Medicine for joint repair would be showcased at the American Academy of Orthopaedic Surgeons Annual Meeting in San Diego that week. Some of the highlighted technologies were included in the presentation.

- In March 2025, Johnson & Johnson MedTech, a global leader in orthopaedic technologies and solutions, announced that its latest advancements in digital orthopaedics would be highlighted at the American Academy of Orthopaedic Surgeons (AAOS) 2025 Annual Meeting in San Diego, California.

Companies Covered in Enthesopathy Treatment Market

- Accuray Inc.

- Boston Scientific Corporation

- R. Bard, Inc.

- Eli Lilly and Co. Ltd

- Janssen Biotech, Inc.

- Pfizer, Inc.

- Siemens AG

- Varian Medical Systems, Inc.

- Ultragenyx Pharmaceutical, Inc.

Frequently Asked Questions

The global enthesopathy treatment market is projected to reach US$219.6 billion in 2026.

The rising prevalence of musculoskeletal disorders and geriatric population growth are key drivers.

The enthesopathy treatment market is poised to witness a CAGR of 6.6% from 2026 to 2033.

Next-generation biologics, point-of-care regenerative therapies, and value-based outpatient models are key opportunities.

Eli Lilly and Co. Ltd, Janssen Biotech, Inc., Pfizer, Inc., Boston Scientific Corporation, and Ultragenyx Pharmaceutical, Inc are the key players.