- Semiconductor Materials & Components

- EMI/RFI Filters Market

EMI/RFI Filters Market Size, Share, and Growth Forecast, 2026 - 2033

EMI/RFI Filters Market by Product Type (Single Phase Filter, DC Filters, Medical Filters, Power Entry Modules, Three Phase Filters, Others), Application (Consumer Electronics, Automotive, Telecommunications, Industrial Equipment, Medical Devices, Aerospace & Defense, Renewable Energy Systems), End-User (Original Equipment Manufacturers (OEMs), Aftermarket, System Integrators, Electronics Manufacturing Services Providers), and Regional Analysis for 2026 - 2033

EMI/RFI Filters Market Share and Trends Analysis

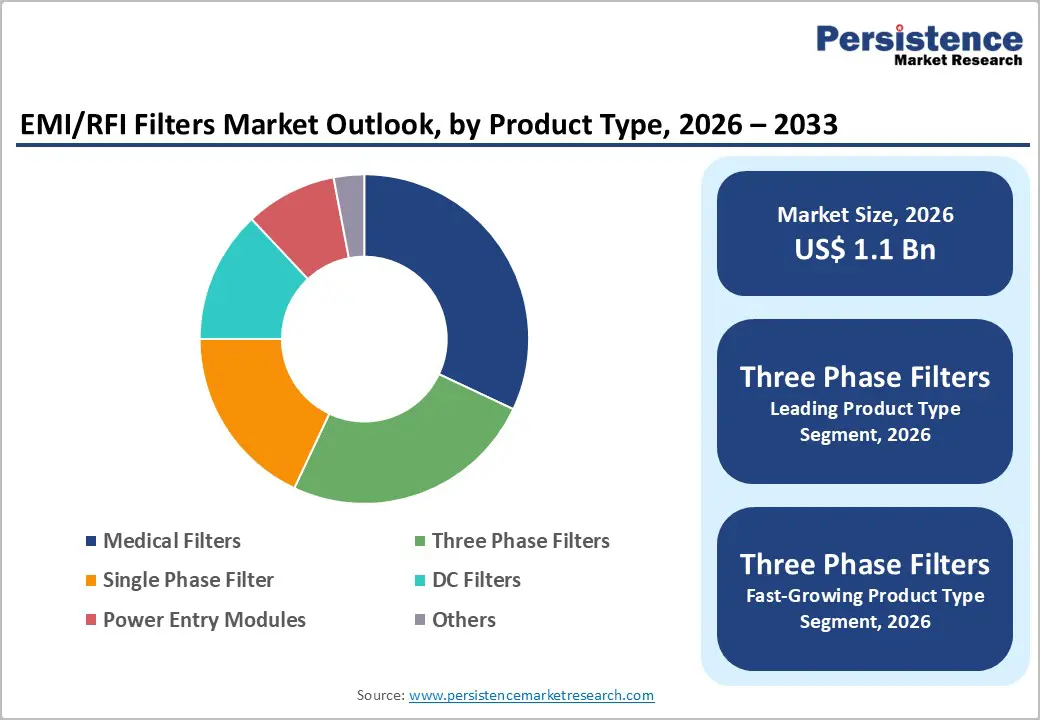

The global EMI/RFI filters market size is likely to be valued at US$ 1.1 billion in 2026, and is projected to reach US$ 1.4 billion by 2033, growing at a CAGR of 3.5% during the forecast period 2026−2033. Market expansion reflects structural integration of advanced electronic systems across critical infrastructure, mobility platforms, healthcare networks, and industrial automation environments. Growth is driven by increasing electronic device density across automotive electrification, renewable energy installations, industrial robotics, medical equipment, and telecommunications infrastructure. Strengthening regulatory enforcement on electromagnetic compatibility by agencies such as the Federal Communications Commission (FCC) and the International Electrotechnical Commission (IEC) compels manufacturers to incorporate certified filtering and suppression components into electrical architectures.

Rapid urbanization accelerates the deployment of smart infrastructure, connected transport systems, and energy-efficient buildings, increasing system complexity and exposure to electromagnetic interference. Technological convergence across electric vehicles, 5G networks, edge computing platforms, and distributed renewable grids expands the installed base of power electronics, requiring effective mitigation of conducted and radiated noise. Healthcare infrastructure modernization increases reliance on sensitive diagnostic and monitoring equipment, where signal integrity remains essential for clinical precision and operational reliability.

Key Industry Highlights

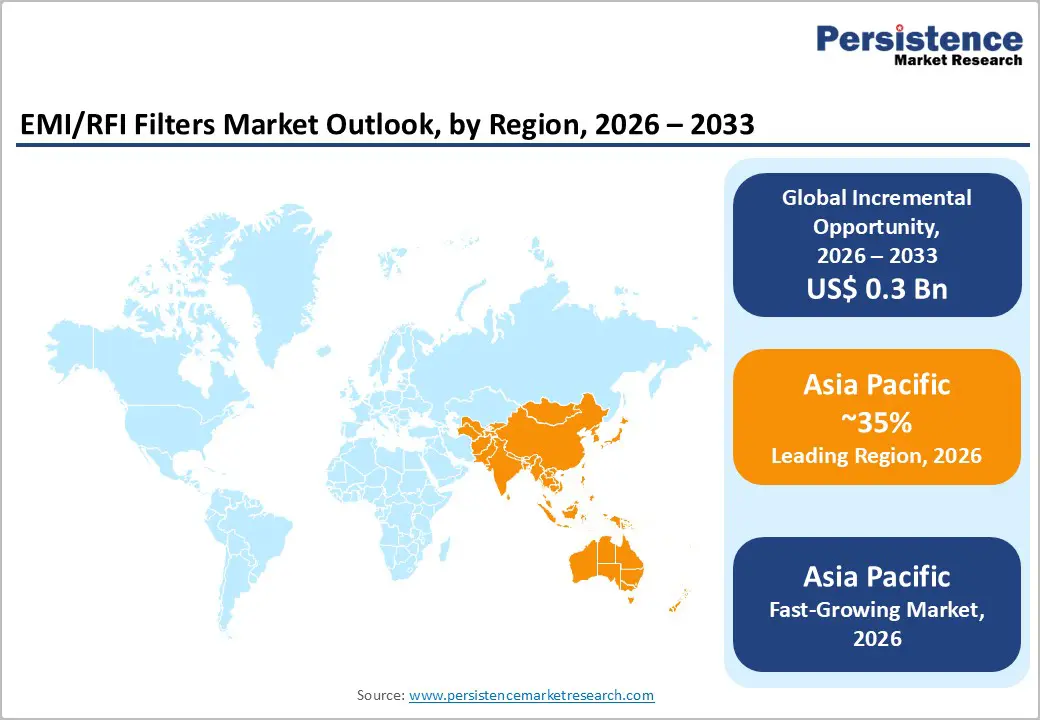

- Dominant Region: Asia Pacific is projected to hold about 35% of EMI/RFI filters demand in 2026, driven by China’s electronics output and India’s automotive expansion.

- Fastest-growing Regional Market: Asia Pacific is forecasted to record the fastest growth between 2026 and 2033, fueled by digital expansion in China and India.

- Leading Product Type: Three-phase filters are projected to hold around 32% share in 2026, supported by industrial high-power applications.

- Fastest-growing Product Type: Medical filters are projected to register the fastest growth during 2026–2033, fueled by expanding interference-sensitive medical equipment deployment.

| Key Insights | Details |

|---|---|

|

EMI/RFI Filters Market Size (2026E) |

US$ 1.1 Bn |

|

Market Value Forecast (2033F) |

US$ 1.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

3.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

2.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expansion of Electrification and Power Electronics Integration

Rapid adoption of electrified systems in transportation, energy, and industrial sectors is driving demand for robust interference control solutions. Widespread deployment of electric vehicles and associated charging infrastructure requires sophisticated power conversion and control electronics, increasing the quantity and complexity of semiconductor-based inverters, converters, and DC-DC modules embedded within these platforms. Electrified transportation, distributed energy resources, and smart grid assets operate at higher switching frequencies and elevated power densities, amplifying conducted and radiated noise across system boundaries. Electrification in buildings and industrial applications similarly replaces mechanical and combustion-based equipment with electronically controlled drives, sensors, and communication interfaces, expanding the installed base of high-speed power electronics that can degrade system performance through electromagnetic emissions.

Growing integration of power electronics in renewable energy systems, microgrids, and advanced manufacturing environments introduces multiple noise sources on shared power networks and signal pathways. Electrified systems often interface with sensitive measurement, control, and communication subsystems that require pristine signal fidelity to operate effectively at scale. Power conversion topologies essential for battery charging, regenerative braking, and grid-tied inverters generate harmonics and switching transients that propagate through cabling and conductive structures. Filtering networks mitigate these effects, protect downstream components, and preserve interoperability among heterogeneous subsystems in complex electrified architectures.

Regulatory Enforcement and Global EMC Compliance Standards

Stringent enforcement of electromagnetic compatibility (EMC) requirements compels manufacturers to integrate validated suppression and filtering technologies into electrical architectures prior to commercialization. In the United States, equipment subject to federal oversight must comply with emission and immunity thresholds defined under 47 C.F.R. Part 15 administered by the Federal Communications Commission before market entry or import authorization. Similar conformity obligations apply across international jurisdictions under IEC frameworks, where harmonized standards define limits for conducted and radiated emissions. These regulatory structures transform electromagnetic performance from a design preference into a mandatory certification criterion embedded within product development lifecycles.

Global EMC compliance frameworks elevate technical accountability across automotive electronics, industrial automation, telecommunications infrastructure, renewable energy systems, and medical equipment. Enforcement mechanisms extend beyond documentation review to accredited laboratory testing, technical file verification, and ongoing market surveillance. Non-conformity exposure introduces operational risks, including shipment detention, product recalls, financial penalties, and reputational impact. Design engineers therefore prioritize integration of certified filtering components to control signal distortion, stabilize power delivery, and prevent interference with adjacent systems operating within dense electronic environments.

Price Sensitivity and Margin Compression in High-Volume Electronics

In high-volume electronics manufacturing, pervasive price sensitivity stems from intense competition and constrained ability to pass cost increases through to customers. The commodity-like nature of many components and contract manufacturing arrangements leaves buyers highly responsive to even marginal price changes, forcing suppliers to compete primarily on unit price rather than differentiated performance. This dynamic is accentuated when raw material and labour costs rise faster than end-product pricing power, leading to margin compression as manufacturers absorb part of the cost burden to secure or retain volume contracts.

Data from the U.S. Federal Reserve shows the producer price index for semiconductor and other electronic component manufacturing remained modest at 61.047 in December 2025, indicating limited pricing strength relative to historical peaks and underscoring ongoing pricing pressure in the sector. Margin contraction reduces suppliers' financial flexibility for key electronic components, placing downward pressure on investment in advanced processes and quality improvements. Large original equipment manufacturers often demand aggressive pricing to meet end-market cost targets in consumer, automotive, and industrial segments, keeping suppliers in a low-profit equilibrium. At the same time, buyers leverage global sourcing and long-term contracts to secure incremental cost reductions, reinforcing price sensitivity as a structural constraint.

Design Complexity and Integration Constraints in Compact Architectures

Compact system architectures in modern electronic products significantly limit available board and enclosure space, creating a fundamental design and integration constraint for engineers tasked with ensuring EMC compliance. Squeezing multiple high-speed digital, analog, and power circuits into minimal footprints increases proximity between noise-generating and sensitive elements, intensifying coupling of electromagnetic interference (EMI) and complicating placement of effective suppression components such as filters, choke coils, and shielding. Tight layouts tend to exacerbate parasitic effects such as unintended capacitance and inductance, degrading filter performance and requiring more sophisticated modelling and bespoke component designs to maintain attenuation targets within stringent size constraints.

Small form factor requirements drive the use of multi-layer boards and integrated subsystems with limited space for discrete filtering, meaning systems often require custom filter topologies and tighter integration of EMI suppression into power and signal paths. Engineers face pressure to balance thermal management, signal integrity, and mechanical constraints without sacrificing EMC performance, particularly as system complexity escalates with advanced wireless, automotive, and industrial applications. The interaction between compact physical designs and stringent EMC requirements can extend validation timelines and inflate development costs, making integration of effective interference mitigation solutions more resource-intensive in constrained architectures.

Renewable Energy and Grid Modernization Expansion

Expansion of renewable generation capacity and large-scale grid modernization programs creates a structural demand shift toward advanced electromagnetic interference and radio frequency interference mitigation components. Solar photovoltaic inverters, wind turbine converters, battery energy storage systems, and high-voltage direct current transmission platforms rely on high-frequency power electronics that introduce conducted and radiated emissions into interconnected networks. Grid digitization initiatives integrate smart meters, automated substations, distributed energy resources, and real-time monitoring systems, increasing electrical noise density and system sensitivity. According to the U.S. Energy Information Administration (EIA), renewable energy accounted for approximately 24% of total United States electricity generation in 2025, reflecting sustained integration of inverter-based resources across transmission and distribution infrastructure.

Grid modernization programs prioritize resilience, bidirectional power flow management, and digital control architecture, leading to greater deployment of semiconductor-based switching systems operating at elevated frequencies. Such architectures increase susceptibility of protection relays, communication modules, and control processors to harmonic distortion and high-frequency interference. Utilities and engineering procurement contractors integrate suppression components at both equipment and network levels to safeguard operational continuity and voltage stability. Electrification of transport fleets and distributed storage integration further intensifies load variability, driving installation of advanced converters across substations and microgrids.

5G Infrastructure, Data Centers, and Digitalization of Industry

Accelerated deployment of advanced wireless networks, hyperscale data centers, and connected industrial systems is generating sustained demand for high-reliability interference mitigation technologies. Dense radio access architectures, distributed antenna systems, and high-frequency transmission environments increase exposure to conducted and radiated noise across base stations, small cells, and core network equipment. Elevated data throughput requirements intensify signal sensitivity within transceivers, routers, and optical transport systems, raising the risk of performance degradation from electromagnetic disturbance.

Large-scale data processing facilities and digitally enabled manufacturing ecosystems further elevate system complexity and electrical density. High-capacity servers, switching equipment, power conversion units, and backup energy systems operate in close proximity, creating concentrated electromagnetic environments that demand structured suppression strategies to preserve operational continuity. Industrial digitalization, including robotics, programmable logic controllers, and sensor networks, depends on stable low-noise power distribution to maintain precision and avoid production downtime. Increasing reliance on edge computing nodes, renewable energy interfaces, and automated logistics platforms extends these requirements beyond centralized facilities into distributed environments.

Category-wise Analysis

Product Type Insights

Three-phase filters are anticipated to secure around 32% of the EMI/RFI filters market revenue share in 2026, reflecting widespread deployment in industrial automation, renewable energy inverters, and high-power motor drives. Industrial facilities operate three-phase power systems to support heavy machinery and robotics. These systems generate substantial electromagnetic emissions that require robust filtering at input and output stages. Provider preference centers on reliability, high current tolerance, and compliance with industrial electromagnetic compatibility norms. Innovation focuses on compact high-current modules with improved thermal resilience and vibration resistance. Accessibility through established industrial distribution networks supports broad adoption. Treatment effectiveness in this context refers to measurable attenuation of harmonics and conducted emissions within regulated thresholds.

Medical filters are expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by rising deployment of diagnostic imaging systems, patient monitoring devices, and surgical equipment operating in interference-sensitive environments. Healthcare providers prioritize electromagnetic immunity to ensure signal accuracy and patient safety. Regulatory compliance with medical electrical standards drives integration of certified filter modules within device architecture. Innovation emphasizes low leakage current design, compact form factors, and enhanced isolation characteristics. Expansion of digital healthcare infrastructure and telemedicine platforms broadens application scope. Provider preference favors validated suppliers with documented compliance history. Accessibility improves through collaboration with original equipment manufacturers specializing in medical technology.

Application Insights

Industrial equipment extracts are poised to dominate with a forecasted market share of over 30% in 2026, powered by factory automation, robotics deployment, and programmable control systems integration. Industrial environments generate persistent electromagnetic disturbances due to variable frequency drives and heavy machinery switching operations. Consumer trust in industrial reliability translates into mandatory electromagnetic mitigation strategies embedded during system design. Cultural acceptance of automation across manufacturing economies supports continued investment in emission control infrastructure. Retail penetration is less relevant in this context; instead, direct procurement through industrial supply chains drives adoption. Preventive system protection strategies align with long-term operational continuity objectives.

Renewable energy systems is estimated to be the fastest-growing segment from 2026 to 2033, fueled by grid-connected solar and wind installations incorporating advanced inverters and battery management systems. Preventive power quality management supports grid stability and investor confidence in renewable assets. Digital monitoring platforms enhance transparency in power performance metrics, reinforcing filter integration as a protective measure. Retail penetration through residential solar adoption increases distributed demand. Consumer trust in clean energy technologies encourages broader system deployment. Cultural acceptance of sustainability initiatives supports regulatory incentives for grid modernization. Expansion of digital commerce channels simplifies procurement for small-scale installers.

Regional Insights

North America EMI/RFI Filters Market Trends

North America demonstrates strong demand concentration driven by rigorous regulatory enforcement and advanced system integration across aerospace, defense, medical technology, and digital infrastructure. Electromagnetic compatibility compliance frameworks enforced by the FCC, aligned with international standards issued by the IEC, elevate baseline filtering specifications across commercial and industrial platforms. Aerospace and defense programs deploy mission-critical avionics, radar systems, satellite electronics, and secure communications equipment operating in high-interference environments, requiring precision-engineered suppression components validated for operational resilience. Expansion of electric mobility manufacturing and renewable energy interconnections increases reliance on advanced power filtering to stabilize inverter-driven architectures and high-capacity charging infrastructure.

Sustained expansion is reinforced by healthcare modernization and acceleration of artificial intelligence workloads in enterprise computing environments. Diagnostic imaging systems, robotic surgical platforms, and remote patient monitoring devices depend on controlled electromagnetic conditions to maintain clinical precision and system interoperability. Defense modernization strategies emphasize resilience in electronic warfare and secure communications, intensifying technical requirements for shielded and high-frequency interference suppression modules.

Europe EMI/RFI Filters Market Trends

Europe holds a substantial position in the global landscape for electromagnetic interference and radio-frequency interference filtering technologies, supported by strong regulatory enforcement and advanced industrial specialization. Harmonized electromagnetic compatibility directives under the European Commission establish strict emission and immunity thresholds across automotive, medical, rail, and industrial equipment categories. This regulatory architecture compels early-stage integration of certified filtering components within system designs, particularly in high-reliability sectors such as electric mobility platforms, traction systems, and renewable power converters. Electrification strategies across transport and energy networks increase deployment of inverters, onboard chargers, and high-frequency switching modules that require robust suppression to prevent conducted noise propagation.

Growth momentum is reinforced by rapid scaling of offshore wind installations, electric vehicle charging corridors, and digital rail signaling modernization programs. High penetration of electric vehicles and hybrid drivetrains expands the installed base of power electronics operating at elevated switching frequencies, increasing filtering complexity. Data sovereignty initiatives stimulate investment in regional data center capacity, creating concentrated electrical environments that require structured mitigation of harmonic distortion and electromagnetic leakage. Aerospace and defense manufacturing programs also contribute to demand for ruggedized, high-reliability interference control components designed for extreme operating conditions.

Asia Pacific EMI/RFI Filters Market Trends

Asia Pacific is expected to lead with an estimated 35% of the EMI/RFI filters market share in 2026, supported by concentrated industrial demand and structural electronics integration across diversified high-growth sectors in China and India. Manufacturing ecosystems in China anchor high-volume production of complex electronics that require stringent interference control across power conversion, signal processing, and communications hardware. India’s rapid expansion of automotive assembly capacity and industrial automation creates parallel demand for filtering solutions calibrated for power dense architectures. Investment into layered network infrastructure, including layered access nodes and core transport systems, increases the density of high-frequency circuits that depend on advanced suppression to maintain performance thresholds.

Asia Pacific is forecasted to be the fastest-growing market for EMI/RFI filters between 2026 and 2033, stimulated by digitalization of legacy industry and expansion of edge-centric computing ecosystems in China’s technology corridors and India’s digital services infrastructure. Integration of factory automation platforms raises baseline requirements for electrical noise tolerance, compelling adoption of next-generation interference management at both power and signal interfaces. Distributed energy resource deployments and smart grid nodes in these countries increase bidirectional power conversion events where conducted and radiated disturbances can propagate across networks, driving demand for adaptive filtering topologies.

Competitive Landscape

The global EMI/RFI filters market structure demonstrates moderate fragmentation, characterized by the presence of multinational electronics manufacturers operating alongside specialized regional suppliers. TDK Corporation, TE Connectivity, EMI Solutions, Eaton, and Delta Electronics collectively represent influential participants shaping competitive intensity across core application verticals. These organizations leverage diversified exposure across industrial automation, electric mobility, telecommunications infrastructure, renewable energy systems, and medical electronics. Scale advantages enable integration of research and development with advanced materials engineering, allowing rapid adaptation to evolving electromagnetic compatibility standards. Multinational suppliers benefit from vertically integrated production networks and established relationships with original equipment manufacturers, facilitating early-stage design integration and long-term supply agreements.

Competitive positioning within this environment centers on regulatory compliance expertise, engineering customization capability, and global distribution reach. High-frequency applications in 5G radio units, electric vehicle inverters, and industrial robotics demand compact, thermally efficient filtering architectures that meet stringent certification thresholds. Market participants differentiate through proprietary core materials, miniaturized designs, and modular platforms that simplify system-level integration. Supply chain resilience and multi-site manufacturing strategies mitigate geopolitical and logistics risks, strengthening reliability for mission-critical applications. Strategic investment in simulation tools and electromagnetic modeling enhances product validation accuracy, reducing qualification timelines for complex systems.

Key Industry Developments

- In December 2025, Tech Etch introduced a new enclosure shielding gasket line engineered for superior electromagnetic interference and radio-frequency interference protection in demanding electronic enclosure and cabinet applications, reinforcing shielding performance and long-term reliability for mission-critical systems.

- In September 2025, Mobix Labs’ custom electromagnetic interference filter technology was officially cleared for deployment across U.S. Navy communications systems following military evaluation and was integrated fleet-wide to enhance secure data transmission on naval vessels.

- In April 2025, Spectrum Control introduced an emission security power EMI filter featuring a space-saving design that eliminates conducted electromagnetic interference emanations to enhance data protection in rack-mount and secure electronic environments.

Companies Covered in EMI/RFI Filters Market

- TDK Corporation.

- TE Connectivity.

- EMI Solutions Pvt Ltd.

- Eaton.

- Delta Electronics, Inc.

- Murata Manufacturing Co., Ltd.

- Panasonic Corporation

- ABB

- Amphenol Aerospace

- Littelfuse, Inc.

Frequently Asked Questions

The global EMI/RFI filters market is projected to reach US$ 1.1 billion in 2026.

Increasing electronic complexity and stringent electromagnetic compatibility regulations enforced by the FCC and the IEC are driving the demand for EMI/RFI filters.

The market is poised to witness a CAGR of 3.5% from 2026 to 2033.

Expansion of 5G infrastructure, electric vehicle (EV) platforms, renewable energy systems, data centers, and industrial automation presents key growth opportunities for market players.

Some of the key market players include TDK Corporation, TE Connectivity, EMI Solutions Pvt Ltd, Eaton, Delta Electronics, Inc., and Murata Manufacturing Co., Ltd.